Lecture 1 Coporate finance

Right side of the balance sheet: Assets (Debit)

Assets are resources that help create value and belong to the company.

Current assets: Short-term assets that can be converted into cash within a year.

Examples: cash, inventory, accounts receivable.Financial assets: Long-term investments or assets held for more than a year.

Property, Plant, and Equipment (PP&E): Tangible assets and intangable used in operations.

Assets don’t have just one value. There’s the market value (what someone is willing to pay) and the book value (historical purchase price).

When you add everything together, you get Total Assets (current + financial assets).

Left side of the balance sheet: Liabilities and Equity (Credit)

This side shows how the company’s assets are financed — either through debt (money owed to others) or equity (owners’ investment).

Liabilities:

Short-term liabilities: debts to be repaid within a year.

Long-term liabilities: debts due after more than a year.

Equity:

Represents the owner’s capital — money invested at risk (not always guaranteed to be returned).Components include:

Common stock / paid-in capital: money shareholders invested.

Retained earnings: profits kept in the company instead of being distributed as dividends.

Income Statement Overview

Revenue (Sales)

– Cost of Goods Sold (COGS)

= Gross Profit

– Operating Expenses

= EBIT (Earnings Before Interest and Taxes)

– Interest Expenses

Interest Income

= PBT (Profit Before Tax)

– Taxes (TC)

= Net Profit (positive or negative)

Main Goal of Corporate Finance

The main goal is shareholder value maximization — increasing the value of common stock and retained earnings.

To achieve this, a company should:

Increase the value of its assets, and

Use financing as efficiently (and cheaply) as possible.

NPV = -CF0 +

-CF0 = point in time (time is 0 ) so buy the assets that they need so albert hijen want to open a store in vienna

PV =

This is discoutning (you could make a market analysis so you could predict where it what you furure earingins are but you dont know the discountrate) Wacc formule

Company it can finance itself

rd is pre-tax on debt, re is the …

(1-tc) = after tax of D

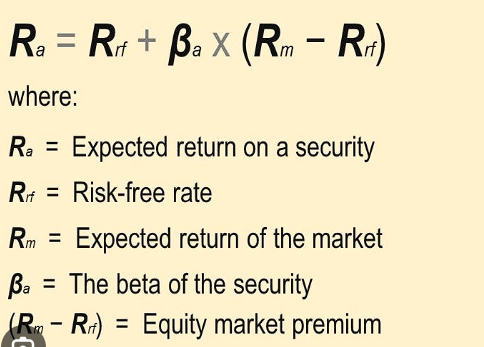

CAPM to calculate re =

Return (compentation)

Time and risk

RF is risk free rate (or time)

RE = RA

BA * (rm - rf) is compenstation from risk