Fundamentals of Finance M1T2: Present Value

I. Time Value of Money: Foundations and Formulas

A. Simple vs. Compound Interest

Simple Interest:

Gains are linear over time:

FV=P(1+rt)

Compound Interest:

Returns are exponential due to reinvestment:

FV= P(1 + r)^t

Insight: The reinvestment effect becomes dramatic over long horizons (e.g., 100 years: $100 grows to $800 under simple interest, but $86,771 under compounding at 7%).

Conclusion: Compound interest dominates in real-world finance, as it reflects reinvestment and compounding frequency.

B. Present Value (PV)

To reverse compound growth and determine today’s equivalent of a future cash flow:

Where:

Ct: cash flow at time t

r: discount rate

: Discount factor

II. Annuities and Perpetuities

A. Ordinary Annuities (Finite Streams)

Definition: A series of fixed, periodic payments.

PV Formula:

Application: Mortgage payments, retirement savings, coupon bonds.

Annuity Factor Notation:

Case Example:

$0.5M loan over 15 years at 4% ⇒ Annual payment ≈ $45,000.

Annual payment = Cashflow x Annuity Factor

B. Future Value of Annuity

C. Perpetuities

Definition: A stream of fixed payments forever.

If r doubles, PV halves — explains high interest rate sensitivity in valuation (e.g., preferred stock, utilities).

III. Growing Annuities and Perpetuities

A. Growing Annuity (Finite Horizon with Growth)

IF r = g:

Use Case: Salaries, dividends, education costs with consistent growth.

B. Growing Perpetuity

, only valid if r > g

Application: Dividend discount model for equities (Gordon Growth Model).

C. Delayed Annuities and Perpetuities

PV of a perpetuity starting in s years:

PV of t-year annuity starting in s years:

Insight: Break complex cash flows into present-valued components to simplify valuation.

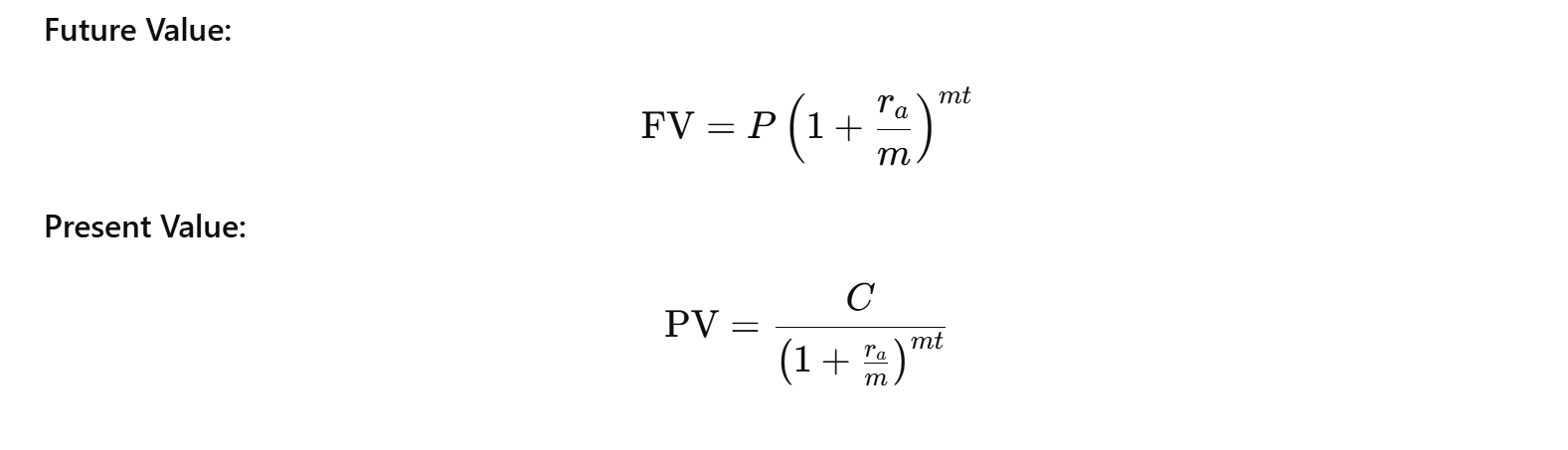

IV. Compounding Frequency and Interest Rate Comparisons

A. Compounding within the Year

Let:

ra : Stated Annual Interest Rate (SAIR)

m: Number of compounding periods per year

Period Rate: ra/m

Key Variables in Present Value and Annuity Formulas

Symbol | Meaning |

|---|---|

C | Cash Flow – The amount of money received or paid at each time period (usually annually). |

r | Discount Rate / Interest Rate – The rate used to discount future cash flows to the present. Also called the required rate of return or opportunity cost of capital. |

t | Time Periods – The total number of periods (usually years) over which the cash flows occur. |

s | Start Delay – The number of periods before the first cash flow begins (used in delayed annuities/perpetuities). |

g | Growth Rate – The rate at which cash flows grow over time in a growing annuity or growing perpetuity. |