Ch 21 - Macroeconomic objectives: economic growth

Economic growth: a increase in real GDP over time

- Rates of economic growth vary over time and depends from country to country. Economies face economic fluctuations known as the business cycle

- Real GDP: measure of a country’s GDP that has been adjusted for inflation

- Nominal GDP: Measure of a country’s GDP without adjusting it for inflation

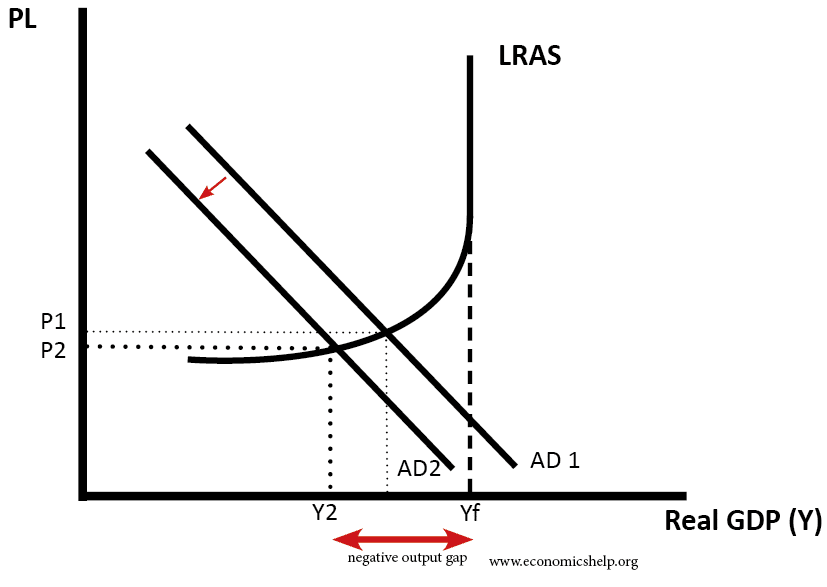

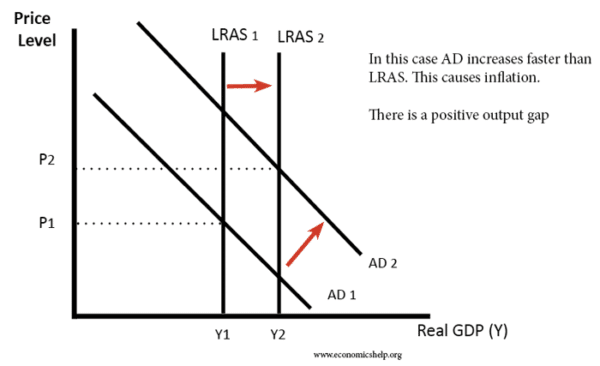

Deflationary gap (output gap): may be the result of a fall in economic growth or negative economic growth in the short run, and may be solved using demand management policies. These demand management policies are expansionary fiscal or monetary/

Measuring economic growth:

- Growth rate= real GDP in Y1 - real GDP in Y2 / real GDP in Y1 * 100

Positive consequences of economic growth:

- Household income: rising GDP means that people afford to buy more goods and services

- Reduced poverty

- Greater employment

- Availability of goods and services

Negative consequences:

- Decreased sustainability

- Income disparities

- Inflation

- Balance of payment

Government policies which affect economic growth:

- Investment in infrastructure: infrastructure is physical capital which is public, and investing in infrastructure increases the capital stock of a country. It also improves quality of life of the citizens and consumers. However, it must be maintained to remain in good condition

- Policies to improve capital accumulation and technological change: These policies help encourage savings, therefore increasing long run consumption and increasing economic growth. Investing in technology makes a country more developed and increases tourism and economic growth.

- Labour force incentives: By providing a reason to join the workforce to citizens, governments can receive more money from taxes and productivity increases which increases economic growth as well.

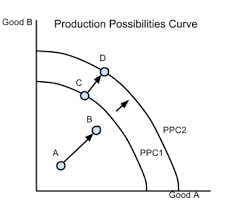

Production Possibility Curve in economic growth:

A Production Possibility Curve (PPC) is a model which shows opportunity cost choices and scarcity when given the chance to produce two goods simultaneously

Conveys the maximum combination of output of two goods that an economy can produce, such as capital goods and consumption goods. The capacity to produce decreases if the curve shifts outward.

This helps economists evaluate whether a good will aid in economic growth in the long term. If it does not, production is not encouraged.

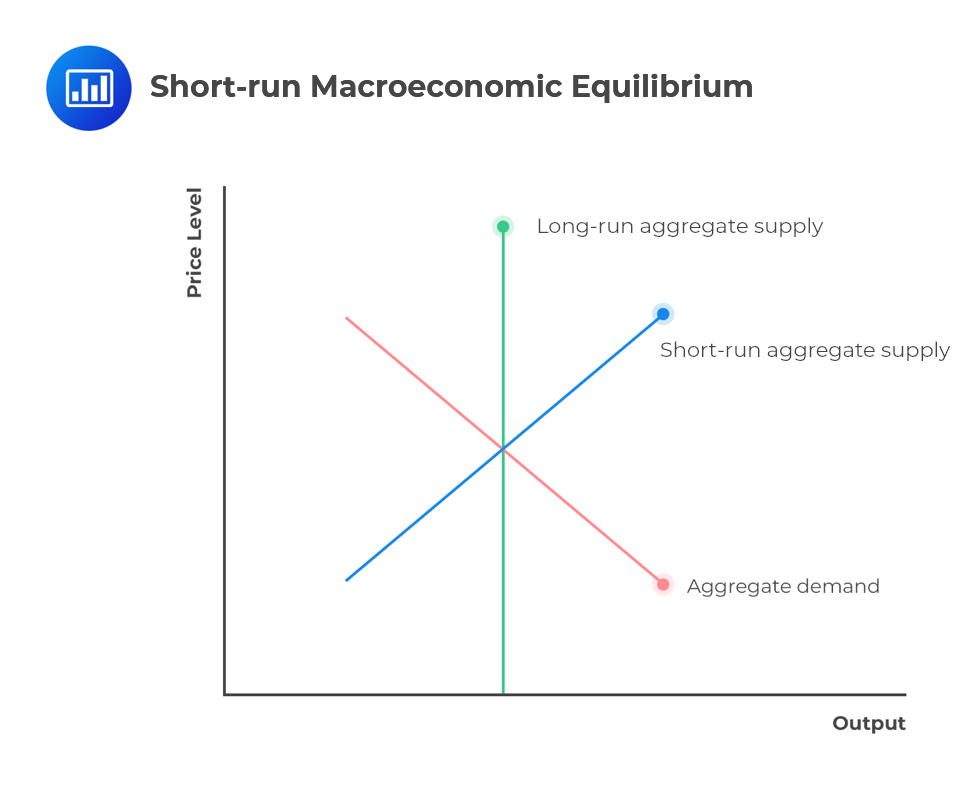

- Short term economic growth:

- Short run in macroeconomics: Is the time period when the economy can change but the cost of production is held constant

- Determined by changes in AD and SRAS

- When there is economic growth in the short run it is described as a change in actual output

\n

Actual output of the economy is the level of output the economy archives with its current resource utilisation

Value of goods and services produced by an economy with land and capital provided

Rise in actual output in the diagram could be caused by an increase in AD which shifts from AD to AD1 and causes real GDP to rise

Actual output will increase if:

- There is an increase in AD, firms produce more, increases the utilisation of available resources

- Firms experience a fall in production costs which leads to SRAS to increase

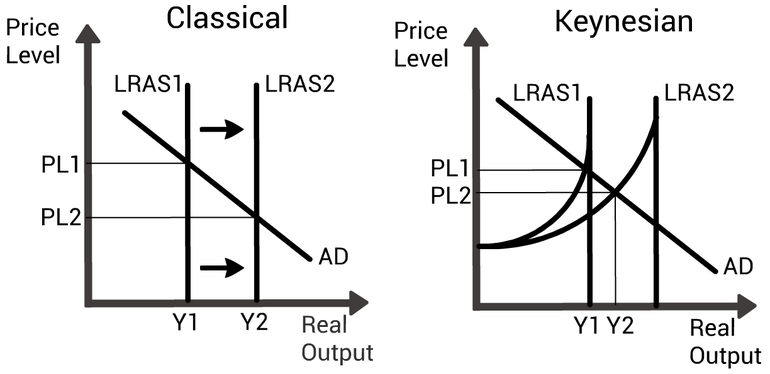

- Long run economic growth:

- Long run in macroeconomics: time period when the price level in the economy can change and the cost of factors of production can change

- In the long run, economic growth occurs because of an increase in potential output