LN4

New businesses and Venture capital

- New businesses can’t usually get bank financing without revenue or collateral

- They are considered too risky

- They don’t meet the minimum “time in business requirements” and haven’t built a credit history

- Venture capital investors can provide equity financing in exchange for an ownership share in the company

Seed Capital

- Seed capital refers to the financing used in the formation of a startup

- Typical sources of seed capital are:

- Founder’s own money

- FFF (“Friends, Family, and Fools”)

- Angel Investors

- Startup accelerators

- Fixed-term, cohort-based programs, that include mentorship and educational components

Angel investors

- Angel investors are wealthy individuals who invest in startups

- They also frequently serve as mentors

- They are willing to invest in promising but unproven business ideas

Startup accelerators

- Startup accelerators and incubators are mentor-based programs that provides guidance, support and limited funding in exchange for equity

- They typically have a competitive application process

- Famous ones are for example Y Combinator and TechStarts

How do founders meet investors?

- Personal network and introductions

- Online communities

- Pitch competitions

- Startup events

- i.e. Refresh Miami & eMerge Americas

- Often founders try to make connections with investors already before raising money

- “I’m not raising money yet, but I will be in the next 6 months or so.”

Signals that can help a founder

- Receiving an investment from a top-tier investor

- Especially if the “star investor” invests on the same terms that the startup is offering to others

- Media attention in a top outlet

- A top-tier entrepreneur or advisor is recommending the company and is throwing their time and reputation behind it

- Introductions made through other investors even if they have chosen not to invest in the company

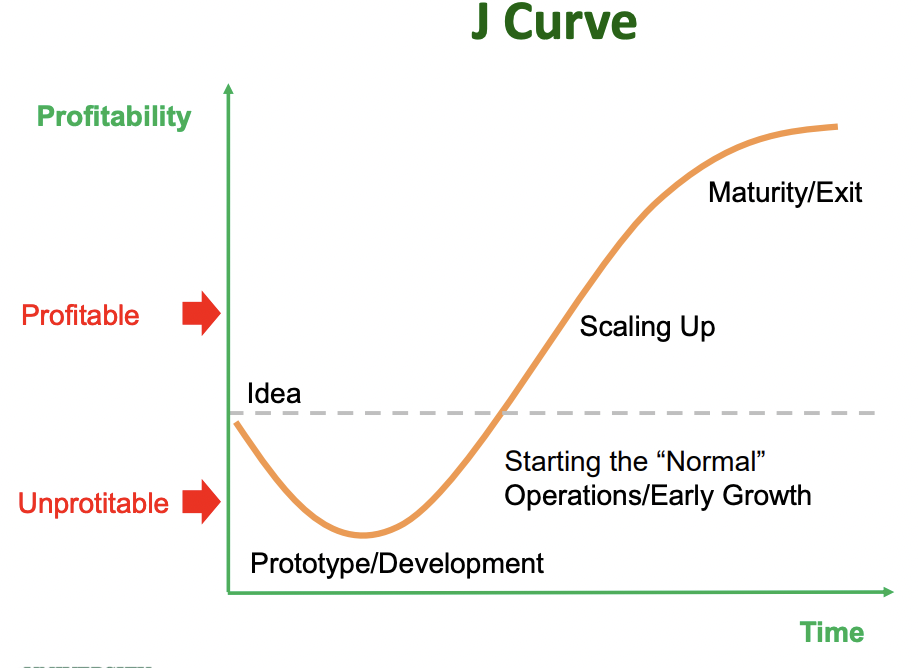

J Curve

- The “J Curve” depicts how startup profitability varies over time

- The stages are illustrative and vary across businesses

Valley of Death

- Valley of death refers to the time period when a startup has begun operations but has not yet generated revenue

- The name comes from the shape of a startup company’s cash flow burn when plotted on a graph

- During this period, the company depletes the initial equity capital provided by its shareholders

- Many companies fail simply because they run out of money

Most startups fail

- The conventional wisdom is that 90% of startups fail

- Failure can be hard to define but

- 2/3 of startups never show a positive return

- Approx. 20% of new small businesses don’t survive the first 12 months

Startup budgeting

- “How did you go bankrupt?” “Two ways: gradually and then suddenly”

- Many startups die simply because they run out of money - realistic budgeting is important both for the founder and the investors

Cash burn rate

- Cash burn rate represents the speed at which an unprofitably company burns its cash reserves

- Gross burn rate = total monthly operating costs

- Net burn rate = gross burn rate - (monthly revenue - cost of goods sold)

- As a rule of thumb, a startup should have 6 to 12 months of expenses on hand

Runway

- A related concept is “runway,” which tells the amount of time the company has before it runs out of money

- Runway = total capital available for expenses / monthly operating expenses

- Example: if a company has $1 million in bank and spends 100k per month, its runway is 10 months

- This is a metric that both the founders and investors should be interested in

- Basically you gotta “take off” before the runway runs out or you’re going to crash

Typical components of a business plan

- market analysis

- company and product description

- Competitive analysis

- Execution plan: operations, development, management, marketing

- Current ownership structure

- Current and projected financial information

- Planned budget and use of capital

- Information on the management team

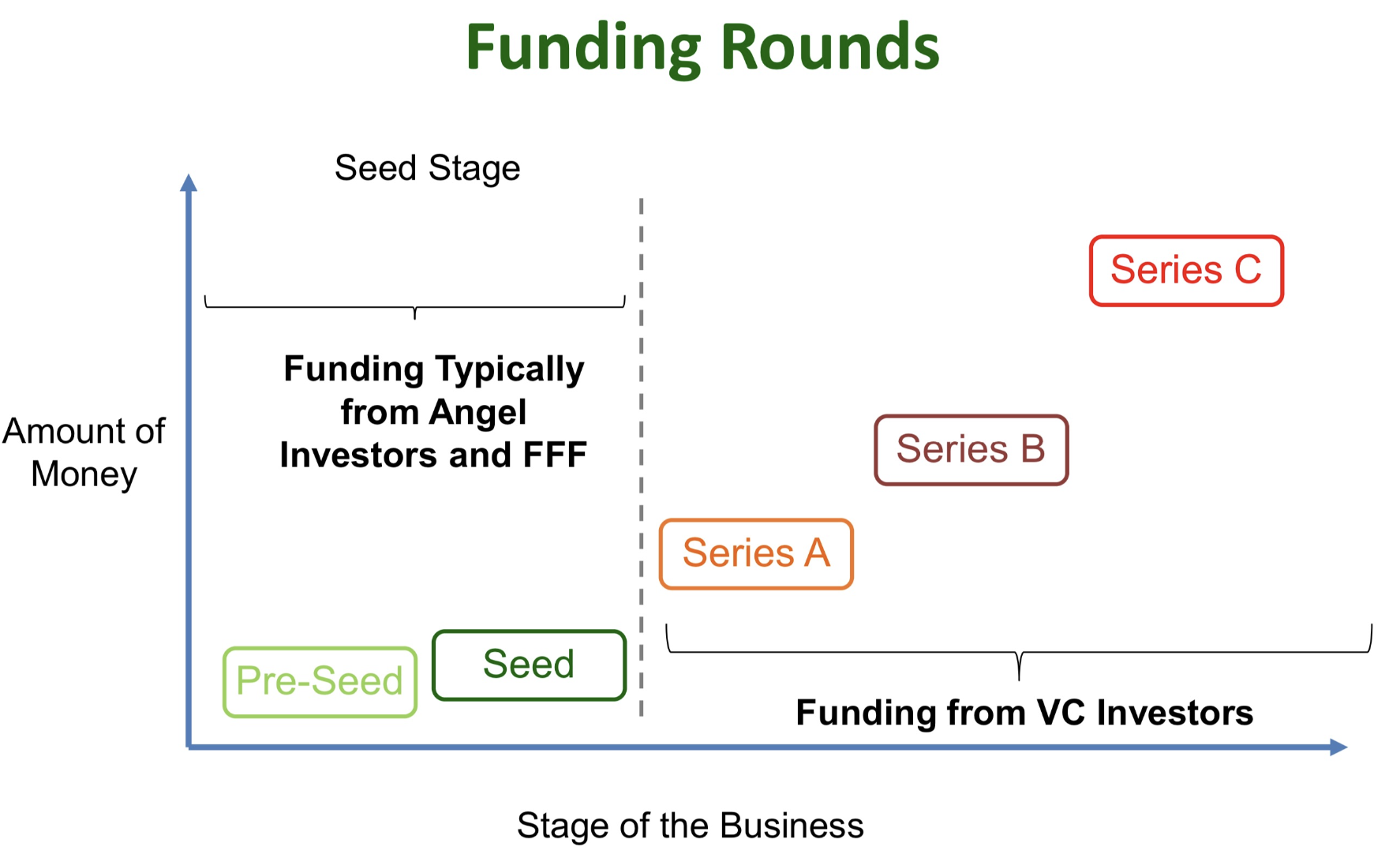

Funding rounds

- Startups raise money from investors through funding rounds

- At each round, the startup receives more money from investors and typically new investors come along

- Funding rounds are typically categorized as

- Seed (sometimes preceded by pre-seed)

- Series A

- Series B

- Series C

- Series D, E

- There are no strict formal definitions for these terms, but they are connected to the stage of the business

Founding rounds

What happens during a funding round?

- The startup receives more capital, which helps it reach the next milestone

- New investors come along

- Ownership structure changes

- The original investors get diluted (own a smaller fraction of the company)

- The startup gets revalued

- Board composition may change

- Operational and strategic changes

- The startup often enters a new lifecycle stage with different goals

- Sometimes the business strategy and goals change

- Employee compensation plans may get revamped

Pre-seed

- Description:

- In this round, the founders are first getting their operations started

- Money is used for early-stage product development

- There is a business/product idea and often the goal is to develop a minimally-visible product as “proof of concept”

- The plan is to prepare the startup for more serious fundraising

- Planned use of funds:

- Early-stage product development

- Who invests in this round?

- Typically founders, friends, family, angel investors, and accelerators

- Some companies go directly the seed stage

Seed

- Description:

- The first “official” equity funding stage

- You need to show that there is a market for the product and a good product-market fit

- Planned use of funds:

- Typically financing for product development, market research, and the first steps of the business

- Who invests in this round?

- Angel investors, specialized in seed funds, and VCs who invest in early-stage ventures

- Fewer than 10% of seed-funded companies will go on to raise Series A funds

Series A

- Description:

- In this round, you are usually seeking funding to get the business seriously started

- You need a business model that can generate long-term profit

- You need to tell convincingly how you are planning to make money with the product

- In 2021, the median Series A funding was $10m

- Planned use of funds:

- The funding is often used to get the actual business fully started

- Who invests in this round?

- Typical investors are VC funds, but angel investors invest in this stage too

Series B

- Description:

- In this round, you are usually taking the business to the next level, past the development stage

- To reach this stage, you usually need a substantial user base and evidence that there is potential for success on a larger scale

- Planned use of funds:

- Expanding the business and reaching new markets

- Who invests in this round?

- Typically, the same investors that invested in Series A are also participating in Series B. Additionally, you often get other VC funds or VC funds that specialize in later-stage investments

Series C

- Description:

- Businesses that raise a Series C funding are already successful

- Series C funding is usually used for scaling up the business and preparing for a successful exit through an acquisition or IPO

- Planned use of funds:

- Funding for further growth: For example, expansion into new markets or products, and acquisitions of other companies

- Who invests in this round?

- Previous investors are often accompanied by PE funds, growth equity funds, and other institutional investors

- Often a company ends its external equity funding with Series C

Series D and later

- Companies that continue with Series D funding (or E, F, G…) tend to either:

- Seek capital for a final push before an IPO or exit

- Seek additional funding because they didn’t reach the goals set in Series C

What VC funds do

- Venture capital funds are PE funds that invest in startups and early-stage businesses

- VC funds don’t just provide capital - they also mentor and assist the management team

- VC investors often have board seats in early-stage businesses, and they are involved in key corporate decisions

How VC funds help businesses

- VCs can help businesses in many ways by providing

- expertise through their business knowledge and industry knowledge

- connections with suppliers and distributors

- help with developing marketing, PR, legal, and HR functions

- assistance in financial modeling

- connections to other investors in future funding rounds

- plans and guidance with exits (IPO or getting bought)

Only a fraction of VC investments are profitable

- Most VC investments lose money

- Studies indicate that on average

- 7/10 portfolio companies will not return even the money invested in those startups

- 2/10 are expected to return enough to cover all the losses

- 1/10 generate the 20-30% IRR that investors anticipate

Home runs are important

- Even though most VC investments fail, the few successful ones can provide amazing returns. These are referred to as home runs

- Home run potential is one of the key aspects VCs are looking for

- Everyone wants to find the next Amazon or Google

Due diligence for a startup investment

- Typical things VCs evaluate before an investment

- Financial and ownership information

- Validation of user/product data

- Quality of founders’ projections and forecasts

- Quality of the founding team

VC portfolios

- The number of portfolio companies varies from a dozen to over a hundred

- Smaller funds invest in fewer companies

- Funds that invest in later-stage startups invest in fewer companies

- It is common to reserve 40-60% of the capital for follow-on investments

- This money is reserved for additional investments in successful portfolio companies

Why follow-on matters

- Famous VC firm Andreessen Horowitz invested in Instagram at seed stage and earned an impression 31,100% return

- Unfortunately, they didn’t make any follow-on investments because they also supported a competing firm

- They sold their stake for $78m, which is microscopic compared to their portfolio size

Keys to successful VC portfolio management

- Focus on finding the potential home runs

- Follow-on investments are important: double down on the few winners

- Limit losses in unsuccessful investments where you can

- Don’t throw good money after bad - exit unsuccessful investments early

Pros and cons of VC funding

- Pros

- Can provide crucial capital for growing the business

- Unlike with bank loans, you don’t need cash flow or collateral to secure funding

- VCs provide mentoring and expertise

- VCs have valuable connections

- Cons

- VCs usually want a significant ownership share

- VCs want growth and returns fast, which is not what all founders want

- VCs will be involved in decision-making

- VCs may pressure a company to an early exit

Evaluating a start-up investment

- What kind of things do VCs focus on when evaluating a startup investment?

- Quality of the product

- Business model (“how will you make money with the product”)

- Scalability and potential for growth

- How big is the market?

- What’s the competition?

- Quality and commitment of the management team

- Potential exit strategies

- Current ownership and funding situation