Unit 3

==3.1 Source of Finance==

- capital needed by an entrepreneur to set up a business

- the capital needed to pay for raw materials, day-to-day running costs and credit offered to customers. In accounting terms: working capital=current assets–current liabilities

- raised from the business’s own assets or from profits left in the business (ploughed-back or retained profits)

- Personal Funds

- Profits Retained

t - the profit left after all deductions, including dividends, have been made; this is ‘ploughed back’ into the company as a source of finance

- Sales of Assets

- Managing Working Capital More Efficiently

- the ability of a firm to pay its short-term debts

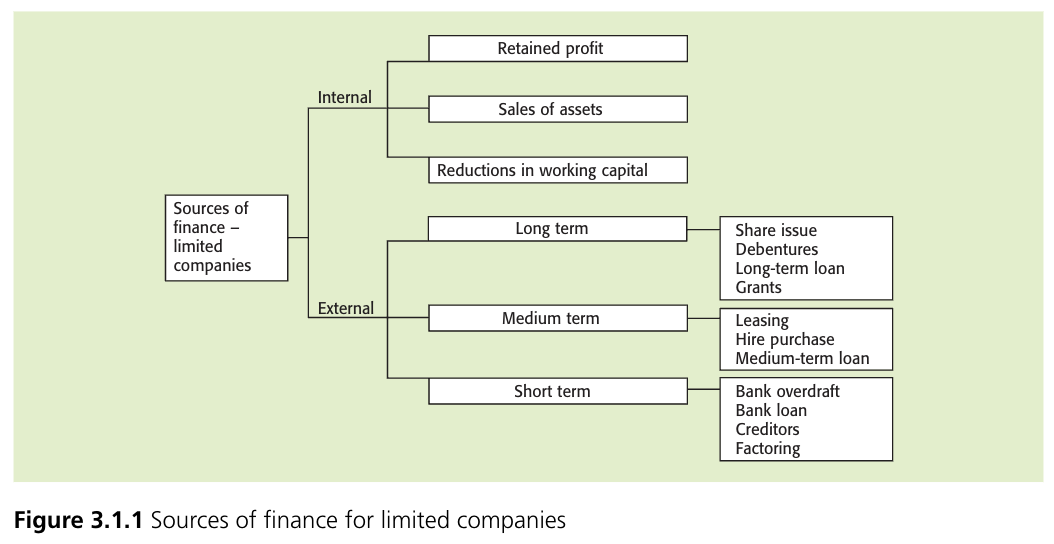

- raised from sources outside the business

- Short-term Finance; bank overdrafts, trade credit, debt factoring

- bank agrees to a business borrowing up to an agreed limit as and when required

- selling of claims over debtors to a debt factor in exchange for immediate liquidity; only a proportion of the value of the debts will be received as cash

- Medium-term Finance; hire purchase and leasing

- an asset is sold to a company which agrees to make fixed repayments over an agreed time period; the asset belongs to the company

- obtaining the use of equipment or vehicles and paying a rental or leasing charge over a fixed period. This avoids the need for the business to raise long-term capital to buy the asset; ownership remains with the leasing company

- Long-term Finance; long-term loans, debentures, debt, equity finance

- permanent finance raised by companies through the sale of shares

- loans that do not have to be repaid for at least one year

- bonds issued by companies to raise debt finance, often with a fixed rate of interest

- existing shareholders are given the right to buy additional shares at a discounted price

[[!! Do not assume that a profitable business is cash rich – and that it can use all of its profits as a source of finance for future projects. In practice, profits are often ‘tied up’ in money owed to the business by debtors or have been used to finance increased stocks or replace equipment !

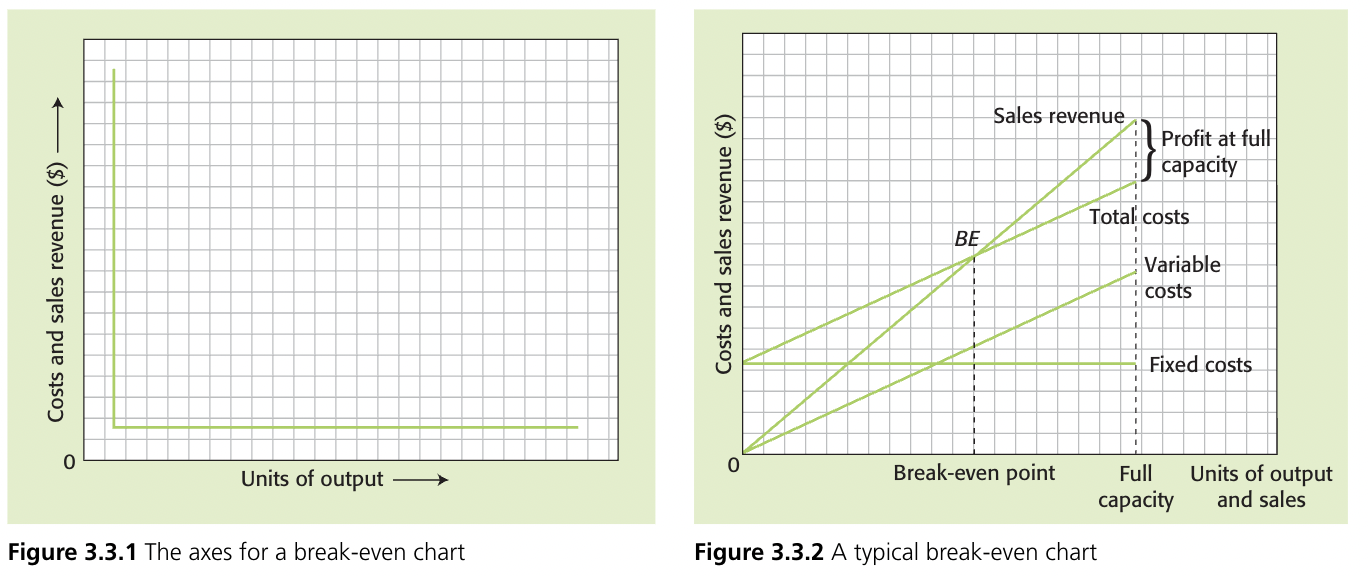

==3.3 Break Even Analysis==

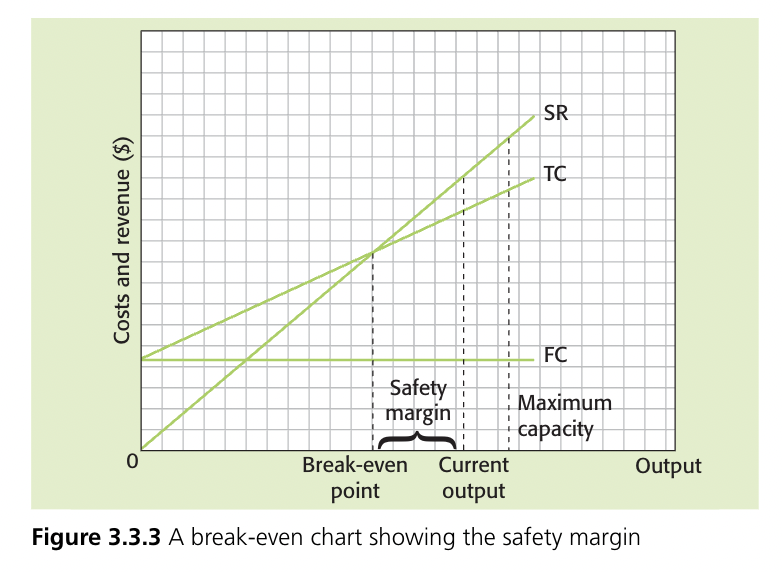

- the level of output at which total costs equal total revenue

total revenue - total costs

Calculating the Break Even - The Break Even Chart (Video included)

- the amount by which the output level exceeds the break-even level of output

production in excess of break - even point = 200 = 50.0%

- selling price of a product minus direct costs per unit

- unit contribution × output

What can you use Break Even analysis for?

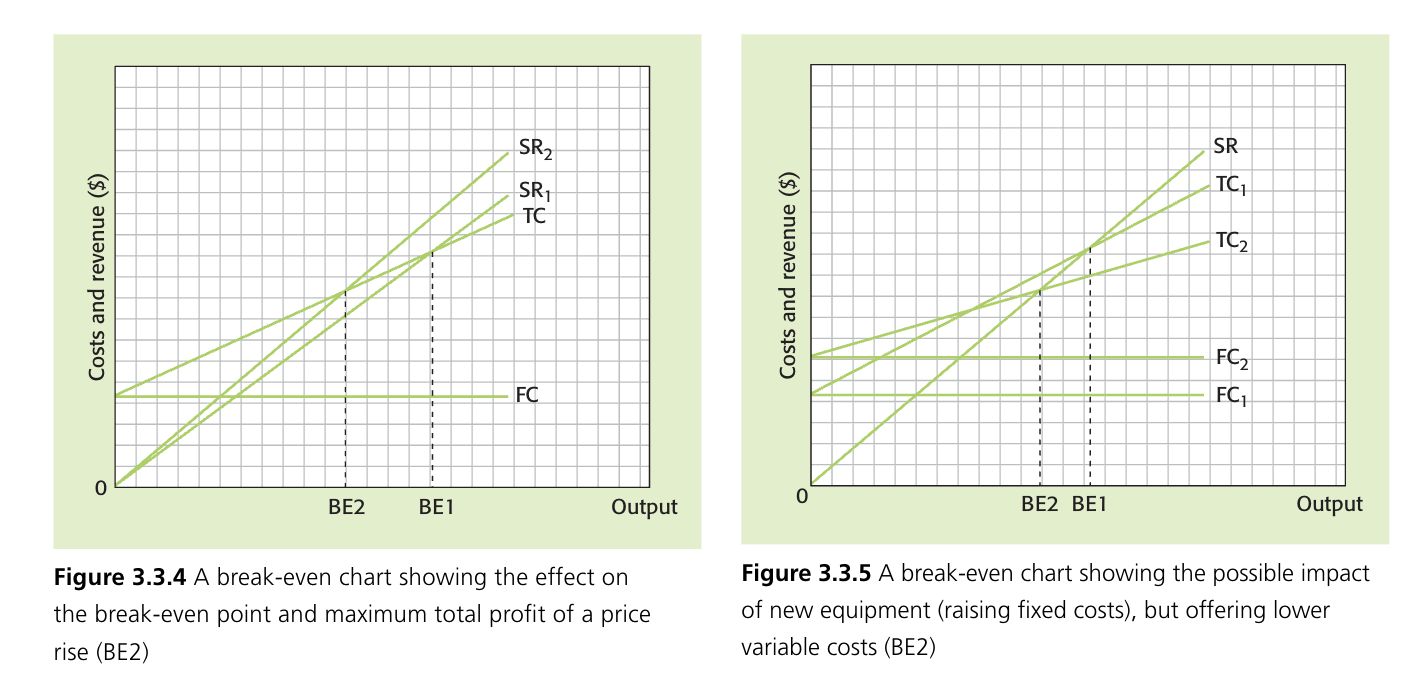

- A marketing decision – the impact of a price increase. This raises the sales revenue line at each level of quantity sold. The assumption made in this example is that maximum sales will still be made. With a higher price level, this may well be unlikely.

- An operations management decision – the purchase of new equipment with lower variable costs. This will lower the variable costs line at each level of quantity.

- Choosing between two locations for a new factory – with different fixed and variable costs.

target profit level of output = fixed costs + target profit / contribution per unit

- the amount of revenue needed to cover both fixed and variable costs so that the business breaks even

break-even revenue = fixed costs / 1 − (direct cost/price)

break-even target price = fixed costs / production level+ direct cost

%%Pros of Break Even Analysis%%:

- Charts are relatively easy to construct and interpret.

- It provides useful guidelines to management on break-even points, safety margins and profit/loss levels at different rates of output.

- Comparisons can be made between different options by constructing new charts to show changed circumstances. In the example above, the charts could be amended to show the possible impact on profit and break-even point of a change in the product’s selling price.

- The equation produces a precise break-even result.

- Break-even analysis can be used to assist managers when taking important decisions, such as location decisions, whether to buy new equipment and which project to invest in.

==Cons==:

- The assumption that costs and revenues are always represented by straight lines is unrealistic. Not all variable costs change directly or ‘smoothly’ with output.

- Not all costs can be conveniently classified into fixed and direct costs. The introduction of semi-variable costs will make the technique much more complicated.

- There is no allowance made for stock levels on the break-even chart. It is assumed that all units produced are sold. This is unlikely to always be the case in practice.

- Cost and price data are often estimated when break-even analysis is undertaken and the actual data might vary from those used in the break-even calculation.

- It is also unlikely that fixed costs will remain unchanged at different output levels up to maximum capacity.

==3.4 Final Accounts==

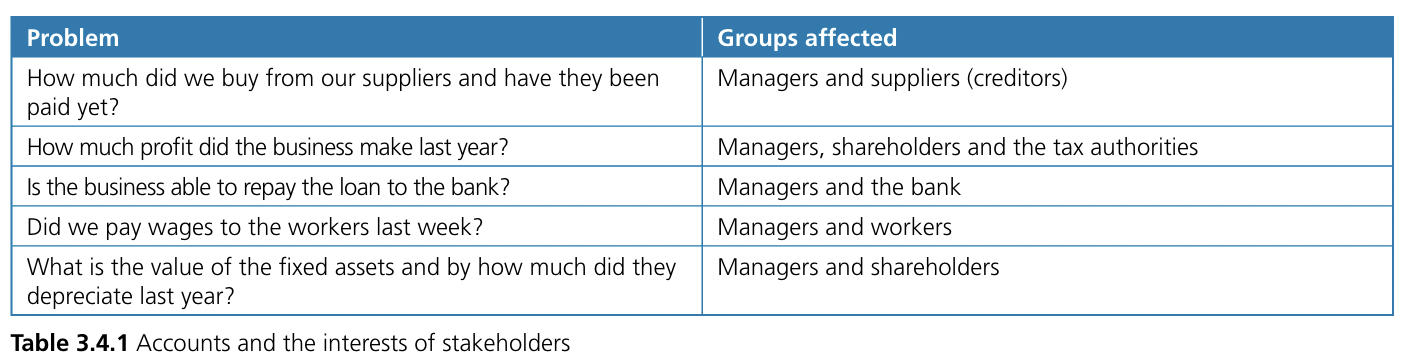

Stakeholders and Accounting Information:

- Business managers

- Measure the performance of the business to compare against targets, previous time periods and competitors.

- Provide information for taking decisions such as new investments, closing branches and launching new products.

- Control and monitor the operation of each department and division of the business.

- Set targets or budgets for the future and review these against actual performance.

- Workforce

- Assess whether the business is secure enough to pay wages and salaries.

- Determine whether the business is likely to expand or be reduced in size.

- Determine whether jobs are secure.

- Find out whether, if profits are rising, a wage increase can be afforded.

- Find out how the average wage in the business compares with the salaries of directors.

- Banks

- Decide whether to lend money to the business.

- Assess whether to allow an increase in overdraft facilities.

- Decide whether to continue an overdraft facility or a loan.

- Creditors such as suppliers

- Assess whether the business is secure and liquid enough to pay off its debts.

- Assess whether the business is a good credit risk.

- Decide whether to press for early repayment of outstanding debts.

- Customers

- Assess whether the business is secure.

- Determine whether they will be assured of future supplies of the goods they are purchasing.

- Establish whether there will be security of spare parts and service facilities.

- Government and tax authorities

- Calculate how much tax is due from the business.

- Determine whether the business is likely to expand and create more jobs.

- Assess whether the business is in danger of closing down, creating economic problems.

- Confirm that the business is staying within the law in terms of accounting regulations

- Investors and potential investors in a business

- Assess the value of the business and their investment in it.•Establish whether the business is becoming more or less profitable.

- Determine what share of the profits investors are receiving.

- Decide whether the business has potential for growth.

- As potential investors, compare these details with those from other businesses before making a decision to buy shares in a company.

- As actual investors, decide whether to consider selling all or part of their holding

- Local community

- See if the business is profitable and likely to expand, which could be good for the local economy.

- Determine whether the business is making losses and whether this could lead to closure.

Limitations of Accounting Information to Stakeholders:

- One set of accounts is of limited use

- Accounts do not measure items which cannot be expressed in monetary terms

- The accounts of one business do not allow for comparisons

- Business accounts will only publish the minimum information required by law

- Accounts are historic

- - presenting the accounts of a business in the best possible, or most flattering, way which could potentially mislead users of accounts

- - the decline in the estimated value of a fixed asset over time

- - items of monetary value that are owned by a business

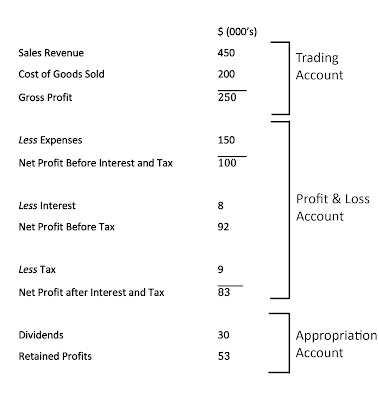

- records the revenue, costs and profit (or loss) of a business over a given period of time

- a financial obligation of a business that it is required to pay in the future

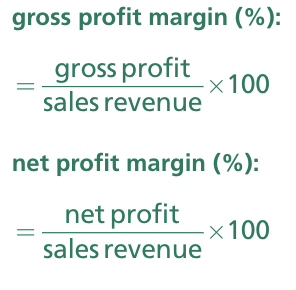

- equal to sales revenue less cost of sales

(or sales turnover) - the total value of sales made during the trading period = selling price × quantity sold

- this is the direct cost of purchasing the goods that were sold during the financial year

(net profit or profit before interest and taxation) - gross profit minus overhead expenses

- operating profit minus interest costs and corporation tax

- the share of the profits paid to shareholders as a return for investing in the company

- the profit left after all deductions, including dividends, have been made; this is ‘ploughed back’ into the company as a source of finance

- one-off profit that cannot easily be repeated or sustained

- profit that can be repeated and sustained

The use of profit and loss accounts:

- They can be used to measure and compare the performance of a business over time or with other firms – and ratios can be used to help with this form of analysis.

- The actual profit data can be compared with the expected profit levels of the business.

- Bankers and creditors of the business will need the information to help them decide whether to lend money to the business.

- Potential investors may assess the value of investing in a business from the level of profits being made. However, when doing this it is essential to try to differentiate between ‘low-quality’ and ‘high-quality’ profit. Low-quality profit – for example, the sale of an asset for more than its balance sheet value – cannot easily be repeated each year so this is a poor basis for making investment decisions.

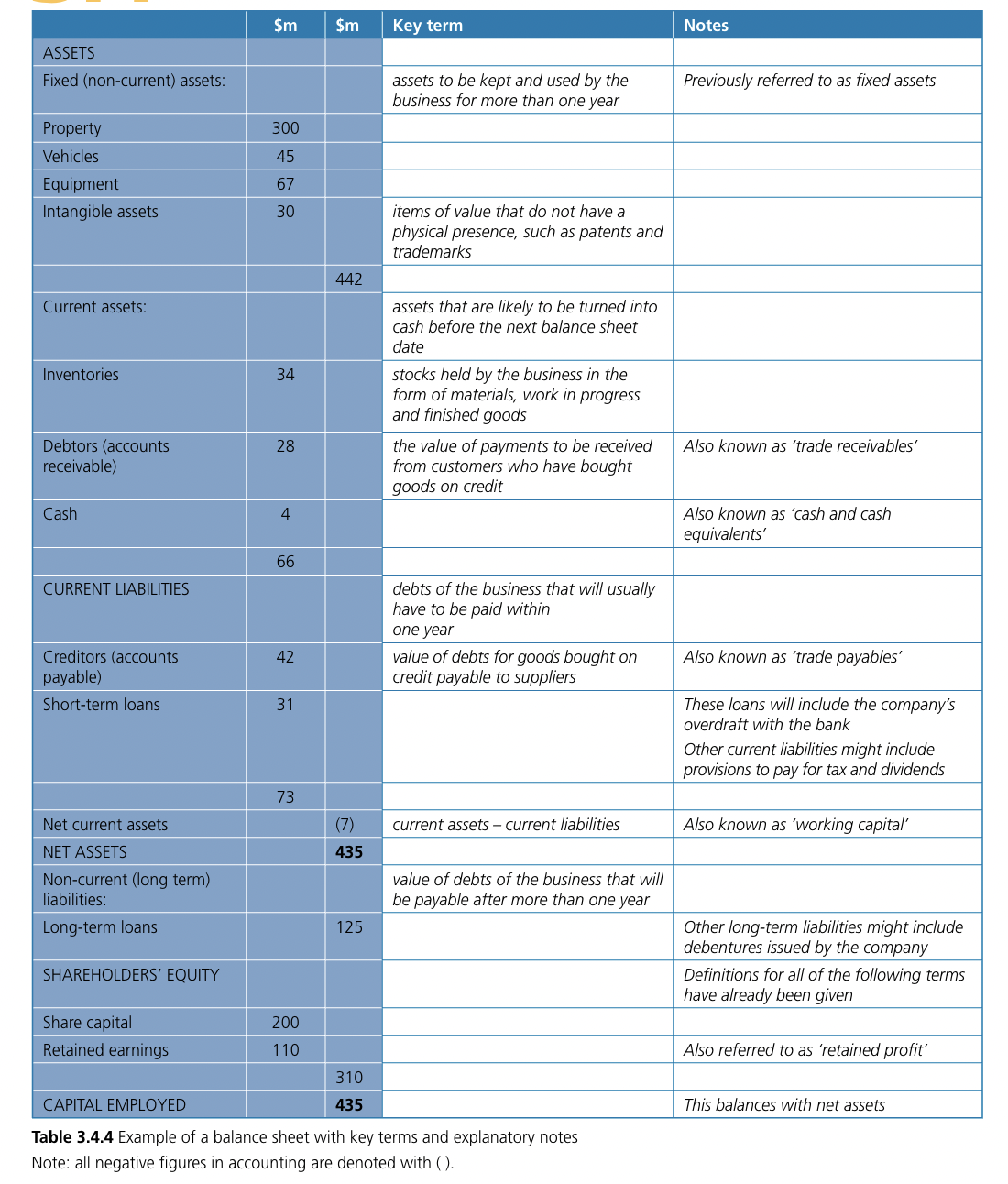

- an accounting statement that records the values of a business’s assets, liabilities and shareholders equity at one point in time

- total value of assets less total value of liabilities

- the total value of capital raised from shareholders by the issue of shares

- customers who have bought products on credit and will pay cash at an agreed date in the future

- debts of the business that will usually have to be paid within one year

- assets that have no physical substance and are not financial instruments (such as bank accounts and accounts receivables). They include asset types such as copyrights and goodwill.

Types of Intangible Assets:

- - are used to market or promote products or services. Trademarks, logos or trade names are words, phrases or symbols that distinguish or identify a company or its products.

- - arises when a business is valued at or sold for more than the balance sheet values of its assets

- - result from business relationships with outside parties.

- - give ownership rights to plays, literary works, musical works, pictures, photographs, and video and audiovisual material.

- - come from the value of rights arising from contractual arrangements, such as franchises, licensing agreements, construction permits, broadcasting rights, and service or supply contracts.

- - arise from patents taken out on innovations or technological advances.

- an intangible asset that has been developed from human ideas and knowledge

- the estimated total value of a company if it were taken over

- a constant amount of depreciation is subtracted from the value of the asset each year

- calculates depreciation by subtracting a fixed percentage from the previous year’s net book value

annual depreciation charge = original or historic cost of asset − expected residual value / expected useful life of asset (years)

- the current balance sheet value of a non-current asset = original cost–accumulated depreciation

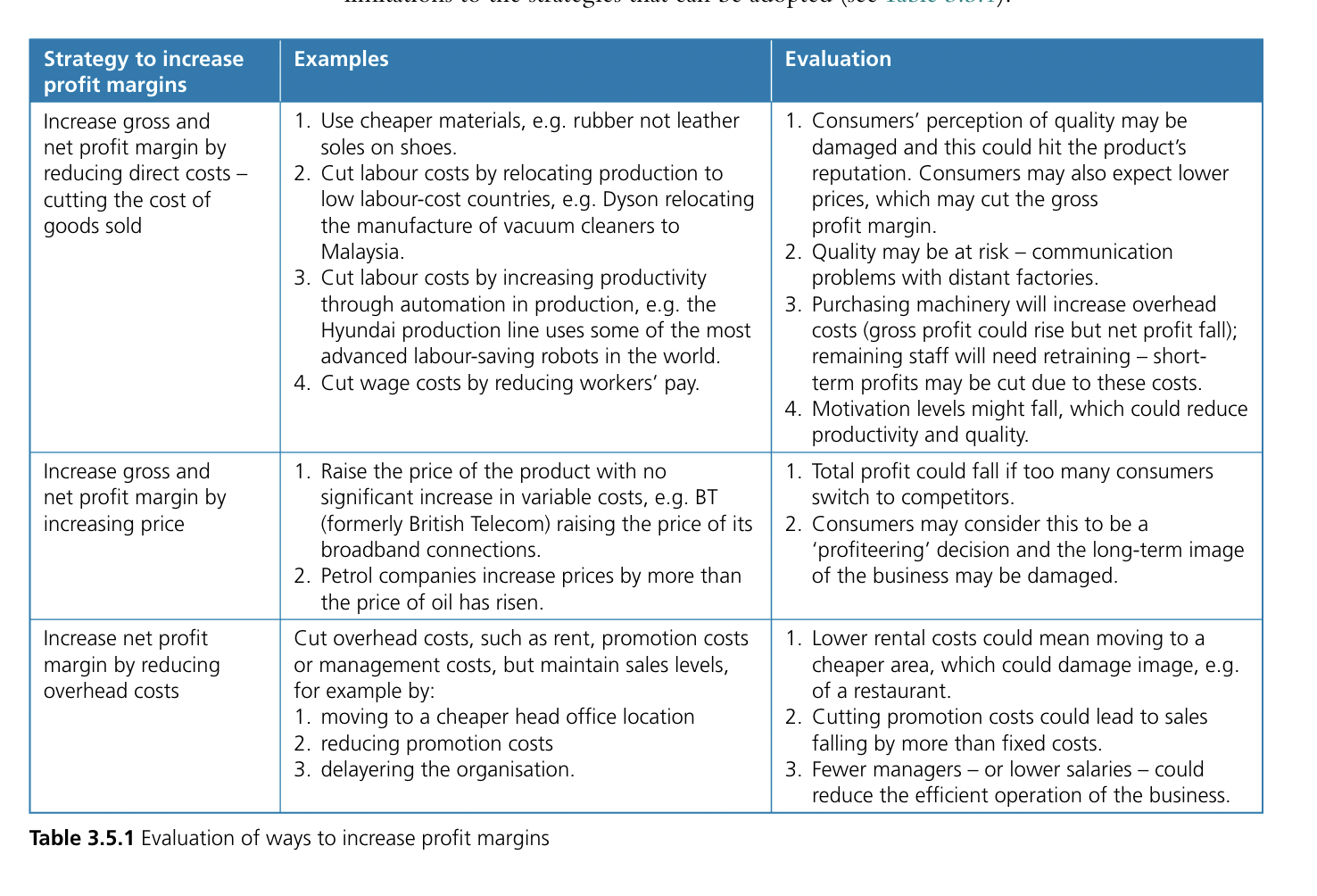

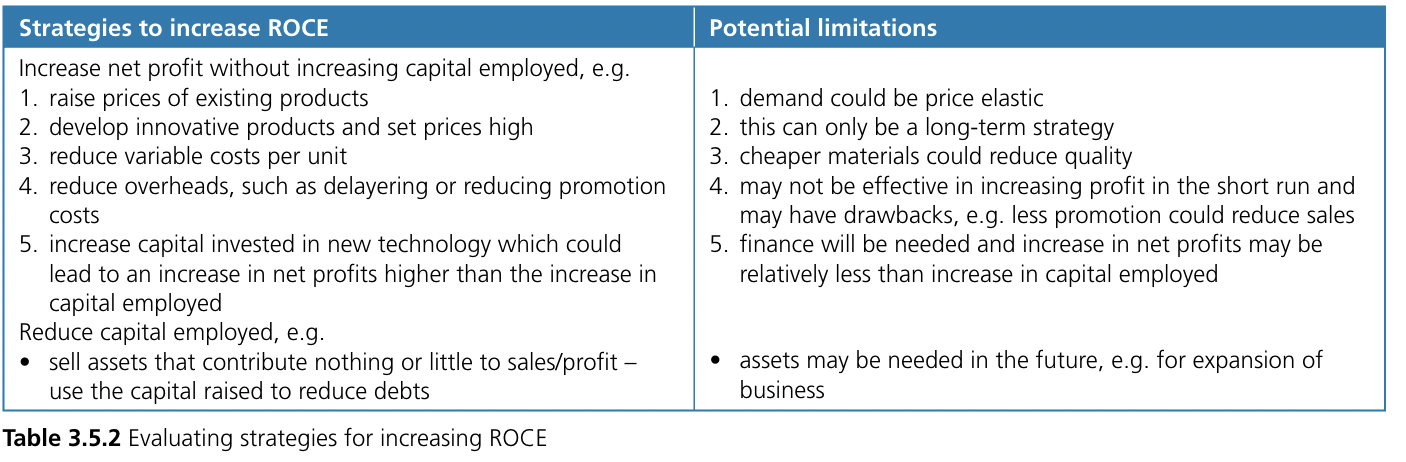

==3.5 Profitability and Liquidity Ratio Analysis==

- the ability of a firm to pay its short-term debts

and are used to assess how successful themanagement of a business has been at converting sales revenue into both gross profit and net profit. They are used to measure the performance of a company and itsmanagement team.

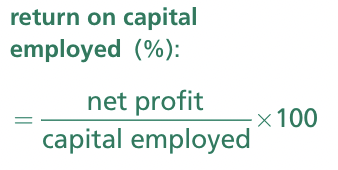

Capital employed = (non-current assets + current assets) – current liabilities or non-current liabilities + shareholders’ equity. The total capital invested in the business.

- an accounting ratio used in finance, valuation, and accounting. It is a useful measure for comparing the relative profitability of companies after taking into account the amount of capital used.

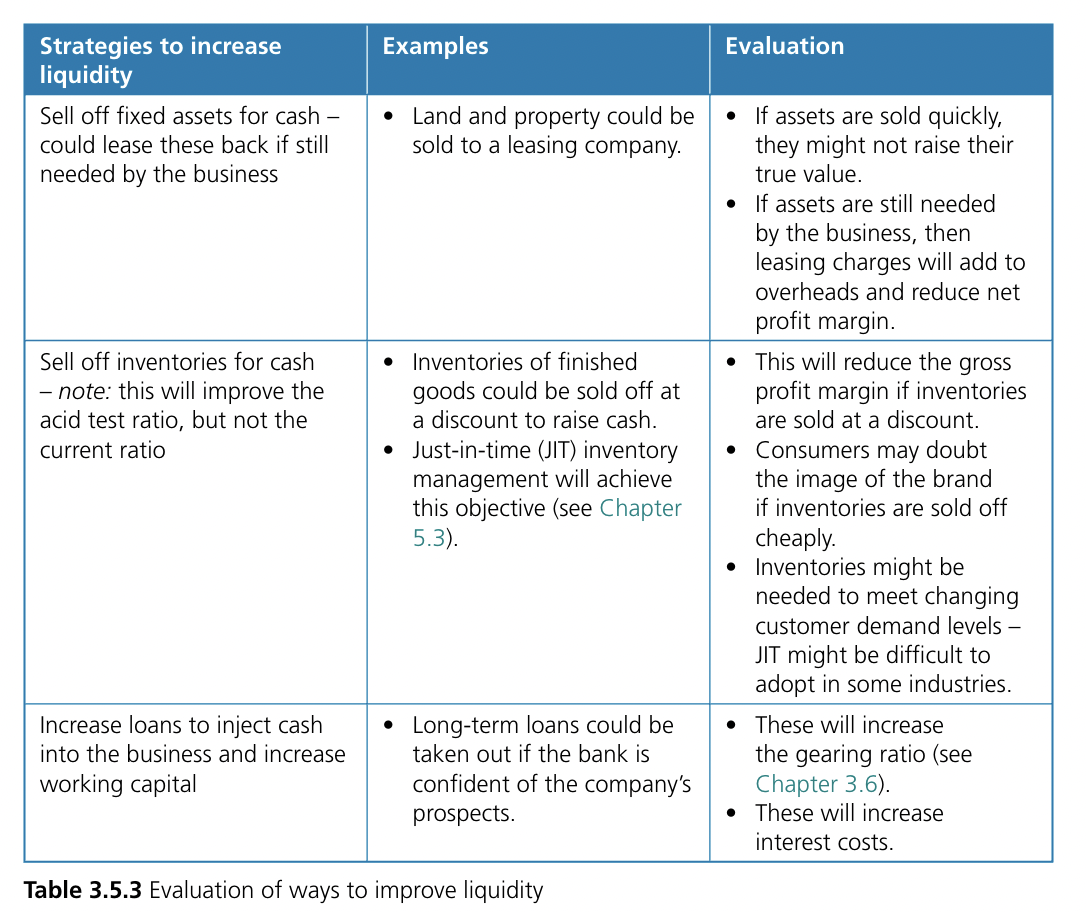

Liquidity Ratios:

- (current assets / current liabilities) - that measures a company's ability to pay short-term obligations or those due within one year (a good current ratio is 2 or higher)

- Acid Test Ratio (liquid assets / current liabilities) - stricter test of a firm’s liquidity (1.0 or more is good)

==3.6 Efficiency Ratio and Analysis==

Efficiency Ratios:

- (cost of goods sold/inventory level) - measures how efficiently a company uses its inventory (between 5 and 10 is good)

- Debtor Days Ratio (debtors (accounts receivable) × 365 / revenue) - measures how quickly it's taking your debtors to pay you (between 30-60)

- Creditor Days (trade creditors / credit purchases × 365) - the average number of days your business takes to pay suppliers. (between 30-60)

- Gearing Ratio (long-term loans / capital employed x 100) - a group of financial metrics that compare shareholders' equity to company debt in various ways to assess the company's amount of leverage and financial stability. (between 25% and 50%)

Limitations of Ratio Analysis:

- One ratio result is not very helpful – to allow meaningful analysis to be made, a comparison needs to be made between this one result and either:•other businesses, called inter-firm comparisons or•other time periods, called trend analysis.

- Inter-firm comparisons need to be used with caution and are most effective when companies in the same industry are being compared. Financial years end atdifferent times for businesses and a rapid change in the economic environment could have an adverse impact on a company publishing its accounts in June compared to a January publication for another company.

- Trend analysis needs to take into account changing circumstances over time which could have affected the ratio results. These factors may be outside the companies’ control, such as an economic recession.

- As noted above, some ratios can be calculated using slightly different formulae, and care must be taken only to make comparisons with results calculated using the same ratio formula.

- Companies can value their assets in different ways, and different depreciation methods can lead to different capital employed totals, which will affect certain ratio results. Deliberate window dressing of accounts would obviously make a company’s key ratios look more favourable – at least in the short term.

- Ratios are only concerned with accounting items to which a numerical value can be given. Increasingly, observers of company performance and strategy are becoming more concerned with non-numerical aspects of business performance, such as environmental audits and human rights abuses in developing countries that the firms may operate in.

- Ratios are useful analytical tools, but they do not solve business problems. Ratio analysis can highlight issues that need to be tackled – such as falling profitability or liquidity – and these problems can be tracked back over time and compared with other businesses. On their own, ratios do not necessarily indicate the true cause of business problems and it is up to good managers to locate these and form effective strategies to overcome them.

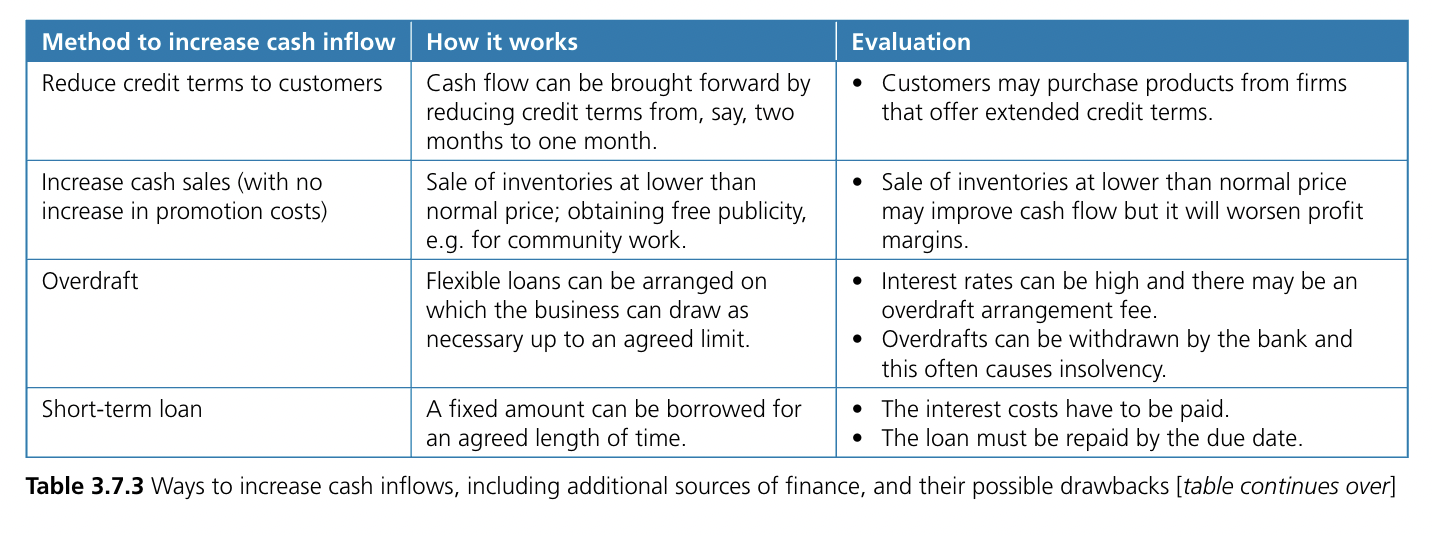

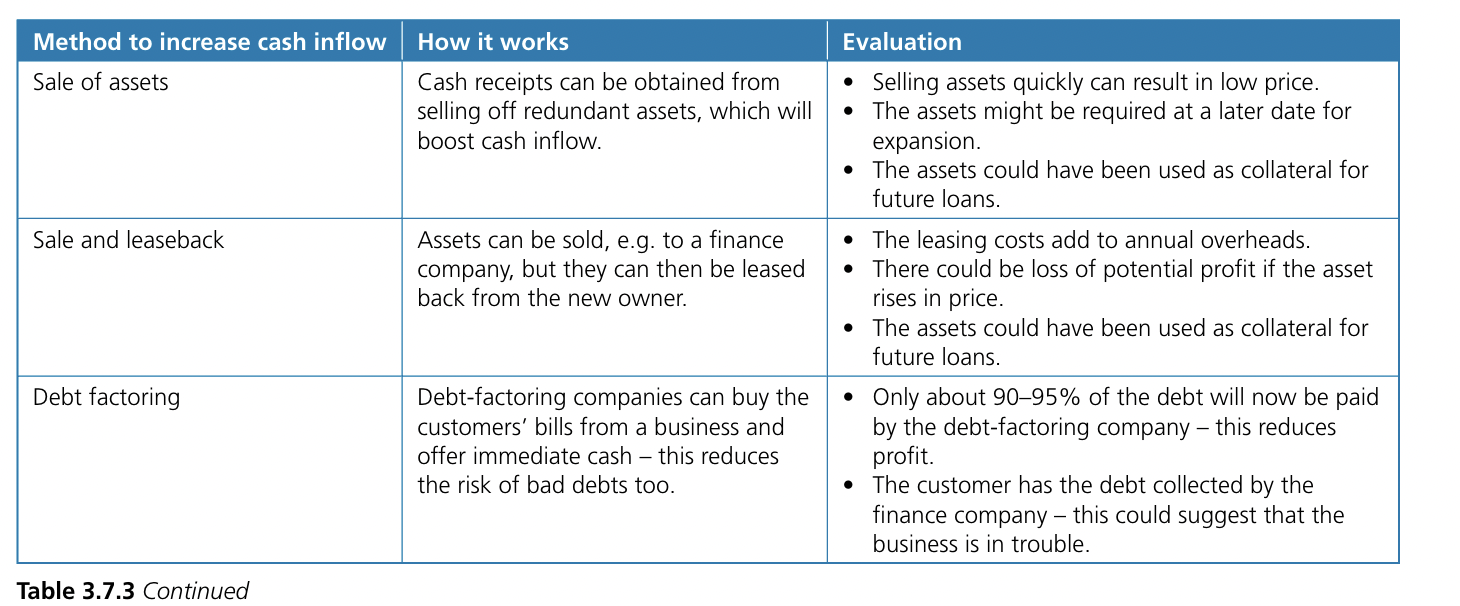

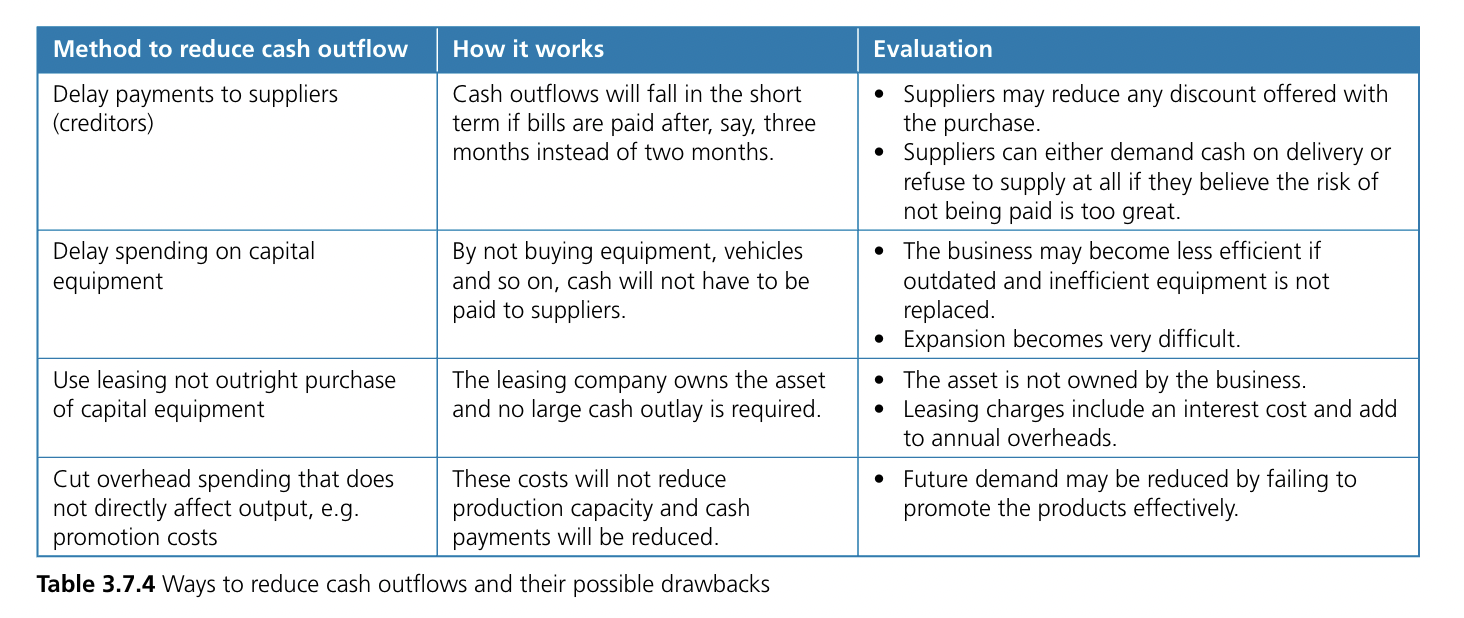

==3.7 Cash Flow==

- when a firm ceases trading and its assets are sold for cash

- when a business cannot meet its short-term debts

- the sum of cash payments to a business (inflows) less the sum of cash payments made by it (outflows)

- payments in cash made by a business, such as those to suppliers and workers

- payments in cash received by a business, such as those from customers (debtors) or from the bank, e.g. receiving a loan

- debts of the business that will usually have to be paid within one year

- customers who have bought products on credit and will pay cash at an agreed date in the future

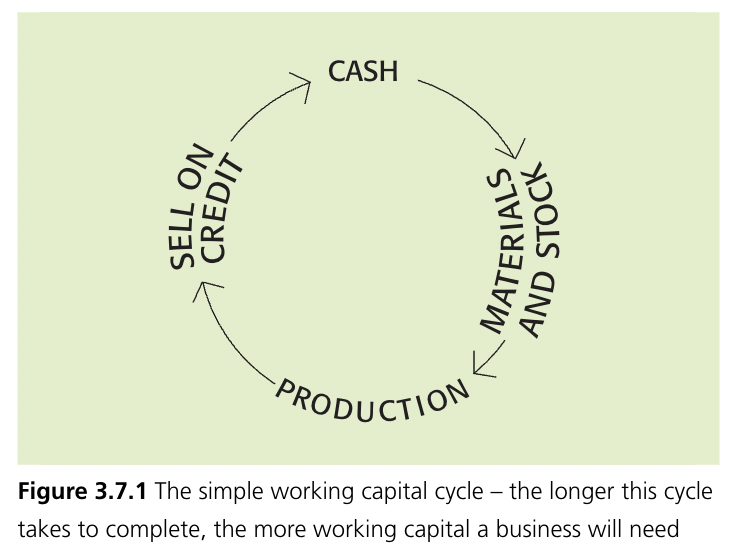

- the period of time between spending cash on the production process and receiving cash payments from customers

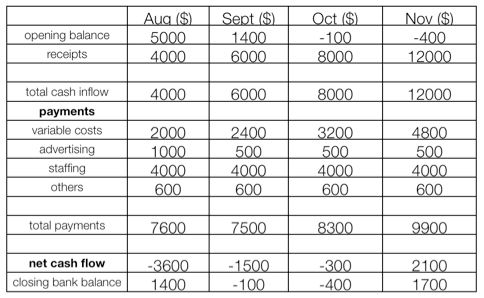

- estimate of a firm’s future cash inflows and outflows

- estimated difference between monthly cash inflows and outflows

- cash held by the business at the start of the month

- cash held at the end of the month becomes next month’s opening balance

%%Pros%%:

- By showing periods of negative cash flow, plans can be put in place to provide additional finance – for example, arranging a bank overdraft or preparing to inject more owner’s capital.

- If negative cash flows appear to be too great, then plans can be made for reducing these – for example, by cutting down on purchase of materials or machinery or by not making sales on credit, only for cash.

- A new business proposal will never progress beyond the initial planning stage unless investors and bankers have access to a cash flow forecast – and the assumptions that lie behind it.

==Cons==:

- Mistakes can be made in preparing the revenue and cost forecasts or they may be drawn up by inexperienced entrepreneurs or staff.

- Unexpected cost increases can lead to major inaccuracies in forecasts. For example, fluctuations in oil prices can cause the cash flow forecasts of even major airlines to be misleading.

- Incorrect assumptions can be made in estimating the sales of the business, perhaps based on poor market research, and this will make the cash inflow forecasts inaccurate.

- monitoring of debts to ensure that credit periods are not exceeded

- unpaid customers’ bills that are now very unlikely ever to be paid

- expanding a business rapidly without obtaining all the necessary finance so that a cash flow shortage develops

[[!! If you suggest ‘cutting staff and cheaper materials’, this may reduce cash outflows, but what will be the negative impact on output, sales and future cash inflows? This suggestion will nearly always be inappropriate for an examination question on improving cash flow !

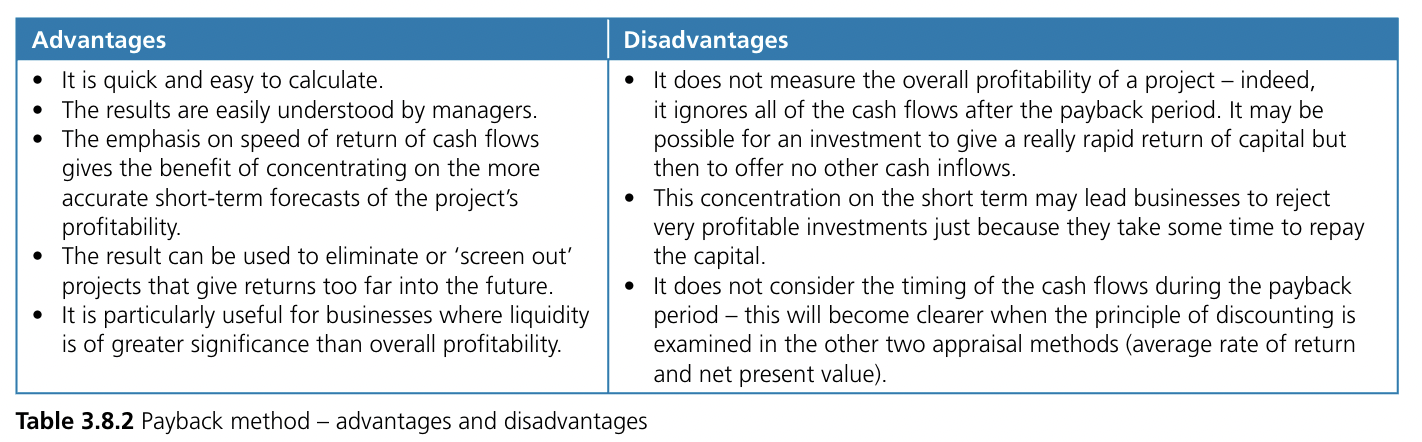

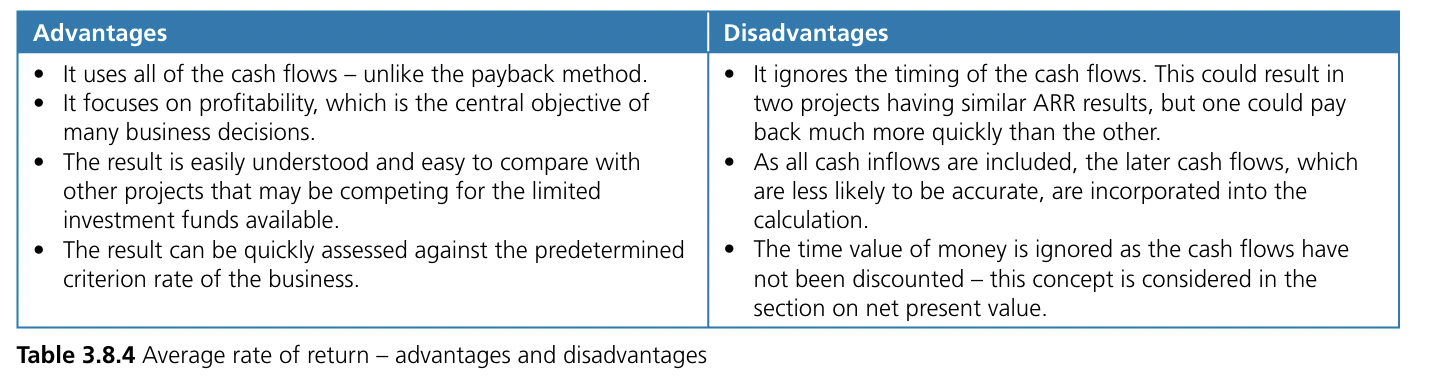

- measures the annual profitability of an investment as a percentage of the initial investment

ARR (%) = annual profit (net cash flow) / initial capital cost × 100

- the minimum level (maximum for payback period) set by management for investment appraisal results for a project to be accepted

==FOR HL !!==

==FOR HL !!==

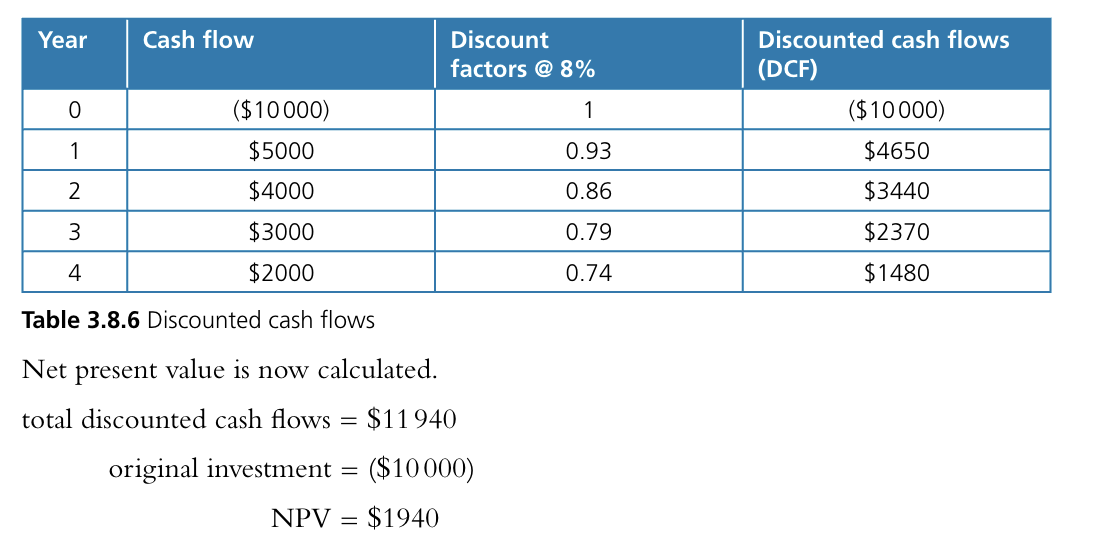

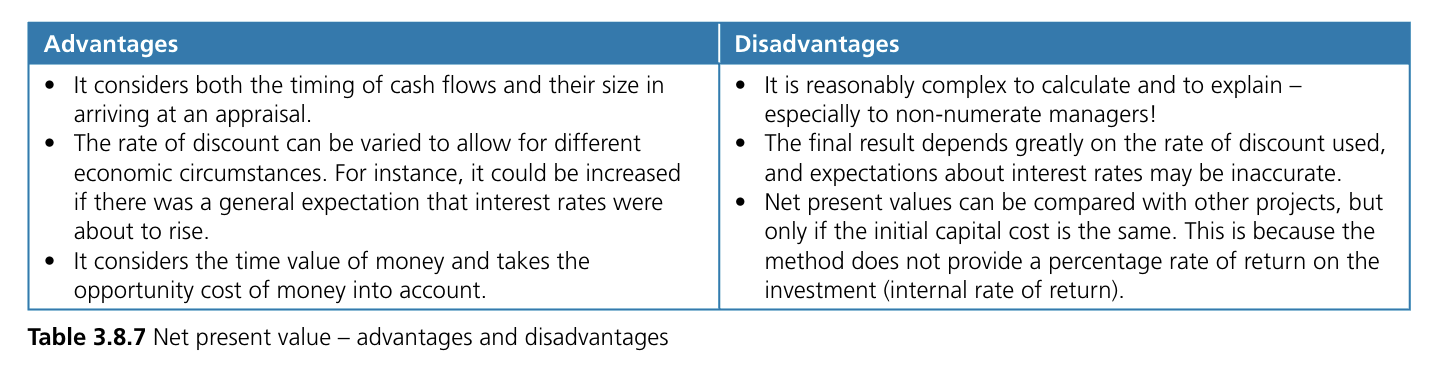

- today’s value of the estimated cash flows resulting from an investment

Stages of calculating NVP:

- Multiply discount factors by the cash flows. Cash flows in year 0 are never discounted as they are today’s values already.

- Add the discounted cash flows.

- Subtract the capital cost to give the NPV

==3.9 Budgeting==

- a detailed financial plan for the future

- individual responsible for the initial setting and achievement of a budget

Purposes of budgeting:

- Planning

- Effective allocation of resources – budgets can be an effective way of making sure that the business does not spend more resources than it has access to

- Setting targets to be achieved – most people work better if they have a realisable target at which to aim. This motivation will be greater if the budget holder or the cost- and profit-centre manager has been given some delegated accountability for setting and reaching budget levels.

- Coordination – discussion about the allocation of resources to different departments and divisions requires coordination between these departments.

- Monitoring and controlling – plans cannot be ignored once in place.

- Modifying – if there is evidence to suggest that the objective cannot be reached and that the budget is unrealistic, then either the plan or the way of working towards it must be changed.

- Assessing performance – once the budgeted period has ended, variance analysis will be used to compare actual performance with the original budgets.

- control over budgets is given to less senior management

Preparation of Budgets:

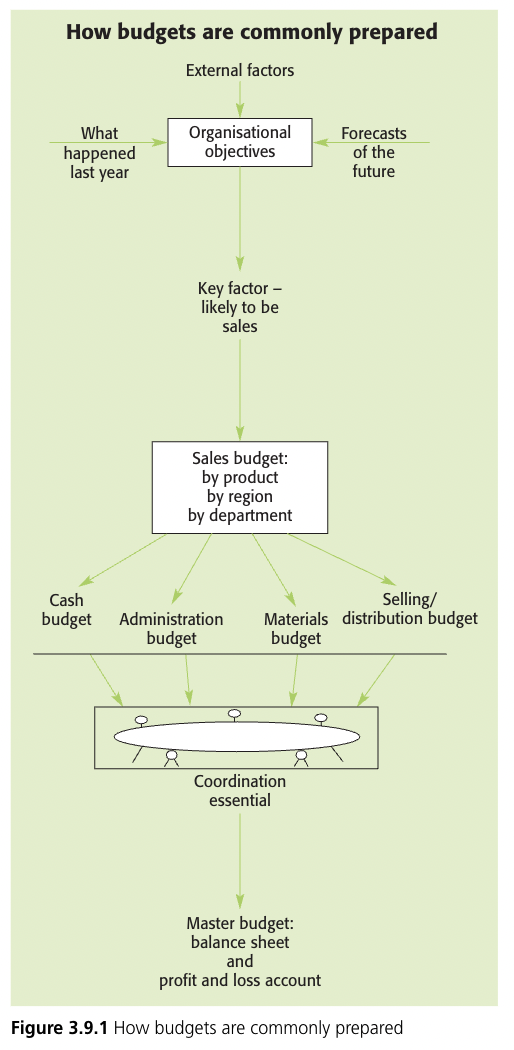

- The most important organisational objectives for the coming year are established – these will be based on:

- the previous performance of the business

- external changes likely to affect the organisation

- sales forecasts based on research and past sales data.

- The key or limiting factor that is most likely to influence the growth or success of the organisation must be identified – usually sales. The sales budget will be the first to be prepared.

- The key or limiting factor that is most likely to influence the growth or success of the organisation must be identified – usually sales. The sales budget will be the first to be prepared.

- Subsidiary budgets are prepared, which will now be based on the plans contained in the sales budget. These will include cash budget, administration budget, labour cost budget, materials cost budget, and selling and distribution budget.

- These budgets are coordinated to ensure consistency. This may be undertaken by a budgetary committee with special responsibility for ensuring that budgets do not conflict with each other and that the spending level planned does not exceed the resources of the business.

- A master budget is prepared that contains the main details of all other budgets and concludes with a budgeted profit and loss account and balance sheet.

- The master budget is then presented to the board of directors for its approval.

- uses last year’s budget as a basis and an adjustment is made for the coming year

- setting budgets to zero each year and budget holders have to argue their case to receive any finance

==Limitations of budgeting==:

- They lack flexibility.

- They are focused on the short term. Budgets tend to be set for the relatively short term, for example the next 12 months.

- They result in unnecessary spending

- Training needs must be met. Setting and keeping to budgets is not easy and all managers with delegated responsibility for budgets will need extensive training in this role.

- Revised budgets may need to be set for new projects.

- a section of a business, such as a department, to which costs can be allocated or charged

- a section of a business to which both costs and revenues can be allocated

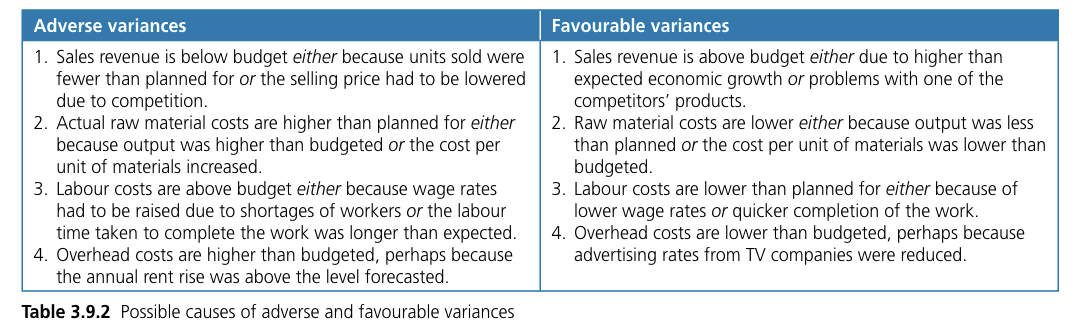

- the process of investigating any differences between budgeted figures and actual figures

- %%Favourable variance%% - exists when the difference between the budgeted and actual figures leads to a higher than expected profit

- ==Adverse variance== - exists when the difference between the budgeted and actual figures leads to a lower than expected profit