Credit Card

Credit: Arrangement to receive cash and pay in the future

Consumer Credit: Use credit for personal use, except a home mortgage

Advantage of Credit

Current use of goods and services

Permits purchases when funds are low

Cushion for financial emergencies

Easier to return merchandise

Can take advantage of float/time grace period

Rebates, airline miles, or other bonuses

Disadvantage

Temptation to Overspend

Does not increase total purchasing power (interest)

Credit costs money

Only free if pay balance in full

Closed-End Credit

One-time only loan for a specific purpose and a specific period

Mortgage, automobile, and installment loans for furniture

Open-End Credit

Use a line of credit until max is met.

Credit card, department store cards, bank credit card

Co-Branding

Linking credit cards with businesses offering rebates on products and services.

Travel & Entertainment Cards

These are not credit cards

Monthly balance is due in full

Diners clubs or American Express cards

Debt Payment-To-Income Ratio

Monthly Debt Payments / Net Monthly Income

Goal is to be under 20% after tax income\

Co-Singing A Loan

Being asked to guarantee the debt, so consider if you can afford it if the borrower defaults

Credit Bureaus

Collect Information

Experian, Trans Union, & Equifax

Collect info from banks, finance, companies, merchants.

Fair Credit Report Act

Regualtes credit reports

Must correct inaccurate or incomplete information

Adverse Data

Can be reprted for 7 years; bankruptcy for 10 years

Unless for credit application of $75,000 or buying more than $150,000 of life insurance

What if you’re denied credit?

Check credit bureau for credit file

Ask creditors to clarify reasons for denial

Apply for another creditor

Take steps to improve your creditworthiness

The 5 C’s

Character - Do you pay bills on time?

Capacity - Can you repay the loan

Capital - What are your assets and net worth?

Collateral - What property do you have to pledge that the lender can repossess if you default on a loan?

Conditions - What are the economic conditions?

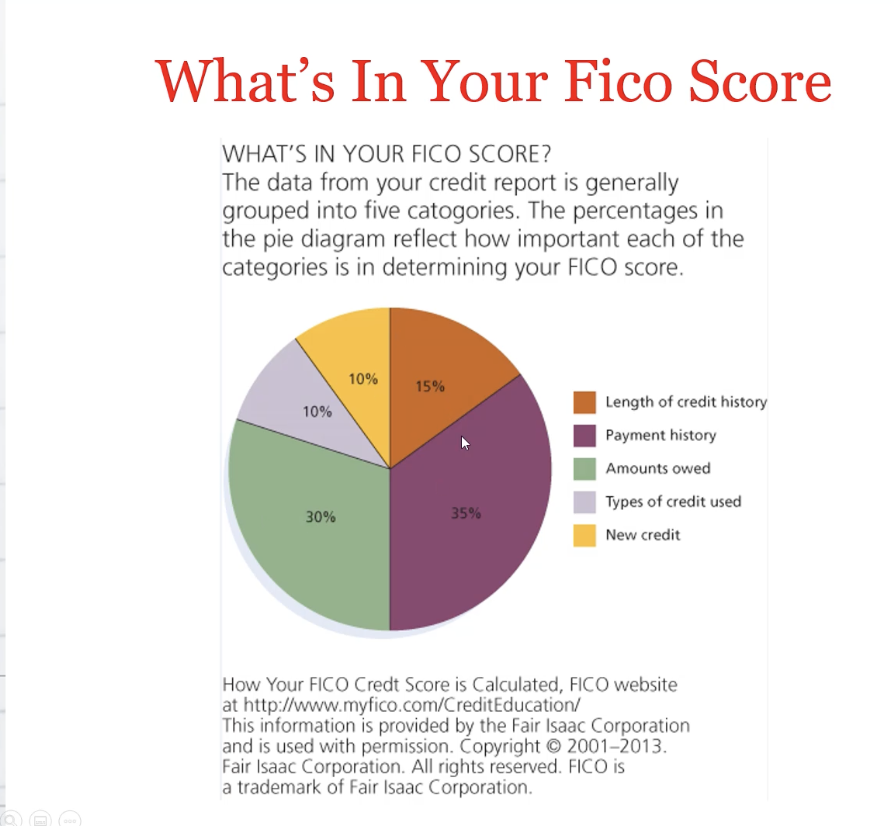

FICO (Credit Score)

Free with the Discover credit card

579 or lower

Indicator of a very risky borrower

580 - 669

Likely to get a loan

670 - 739

Good

740 - 799

Very dependable borrower

800 + (850 max)

Exceptional borrower

How to Improve Credit Score

Copies of credit report-review for accuracy

Pay bills on time

Keep debt low

Longer credit history

More credit cards might hamper growth

FICO Score Improvement