Monopolistic Competition and Oligopoly Chapter 12

Monopolistic Competition

Monopolistic Competition:

Firms can freely enter, each offering a unique brand or version of a differentiated product.

Oligopoly:

Only a few firms compete with one another, entry is impeded

Cartel:

Some or all firms explicitly collude, coordinating prices and output level to maximize profit

The Makings of Monopolistic Competition

Key characteristics:

Differentiated Products: Competing firms sell products that are highly substitutable but not perfect substitutes. Cross-price elasticities of demand are large but not infinite.

Free Entry and Exit: New firms can easily enter with their brands, and existing firms can exit if their products become unprofitable.

Equilibrium in the Short Run and the Long Run

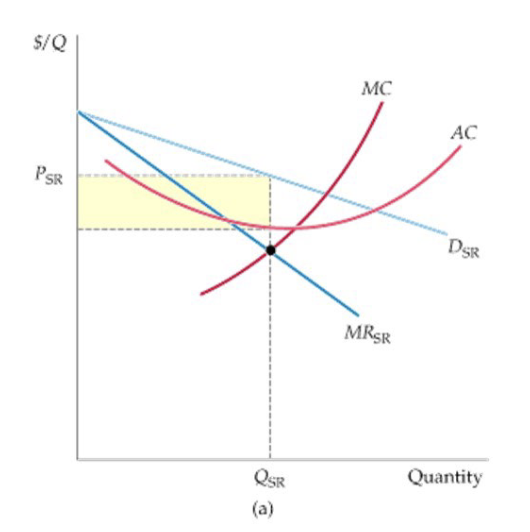

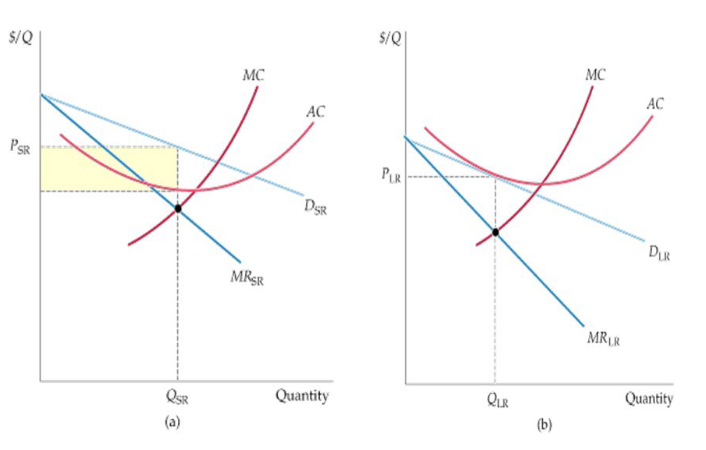

Short Run:

Firms face a downward-sloping demand curve due to their unique brand.

Price exceeds marginal cost, indicating monopoly power.

Price can also exceed average cost, leading to profits.

Long Run:

Profits attract new firms, increasing competition.

Each firm's market share decreases and their demand curve shifts downward.

In equilibrium, price equals average cost, resulting in zero profit despite monopoly power.

Monopolistic Competition and Economic Efficiency

Perfect Competition:

Price equals marginal cost.

Demand curve is horizontal, and the zero-profit point aligns with minimum average cost.

Monopolistic Competition:

Price exceeds marginal cost, creating a deadweight loss.

Downward-sloping demand curve positions the zero-profit point to the left of the minimum average cost.

Entry occurs until profits are driven to zero in both market types.

Social Desirability:

Limited Monopoly Power: With many competing firms and substitutable brands, individual firms possess minimal monopoly power, resulting in small deadweight losses. Demand curves are fairly elastic, keeping average costs near the minimum.

Product Diversity: Consumers value the ability to choose from a variety of competing products and brands with diverse attributes. The gains from product diversity can outweigh the costs of downward-sloping firm demand curves.

Monopolistic Competition in the Markets for Colas and Coffee

Markets for soft drinks and coffee exemplify monopolistic competition with various brands that are close substitutes. Elasticities of demand for Colas and Coffee:

RC Cola:

Coke: to

Folgers:

Maxwell House:

Chock Full o’ Nuts:

Most colas and coffees exhibit notable price elasticity (around to ), indicating limited monopoly power typical of monopolistic competition.

Oligopoly

Products may or may not be differentiated.

Few firms account for most or all of total production.

Firms can earn substantial long-run profits due to barriers to entry.

Examples: automobiles, steel, aluminum, petrochemicals, electrical equipment, and computers.

Reasons for Oligopoly

Scale economies may limit the number of firms that can profitably operate.

Patents or exclusive access to technology can exclude competitors.

Significant spending on name recognition and market reputation can deter new entrants.

These are "natural" entry barriers inherent to the market structure.

Incumbent firms may also employ strategic actions to discourage entry.

Managing an oligopolistic firm involves complex strategic considerations in pricing, output, advertising and investment decisions.

Equilibrium in an Oligopolistic Market

Firms set price or output based on strategic considerations regarding competitors' behavior.

The underlying principle to describe an equilibrium is similar to competitive and monopolistic markets:

When a market is in equilibrium, firms are doing the best they can and have no reason to change their price or output.

Nash Equilibrium

Set of strategies or actions in which each firm does the best it can given its competitors’ actions.

Each firm is optimizing its actions, considering the actions of competitors.

Duopoly

Market with two competing firms.

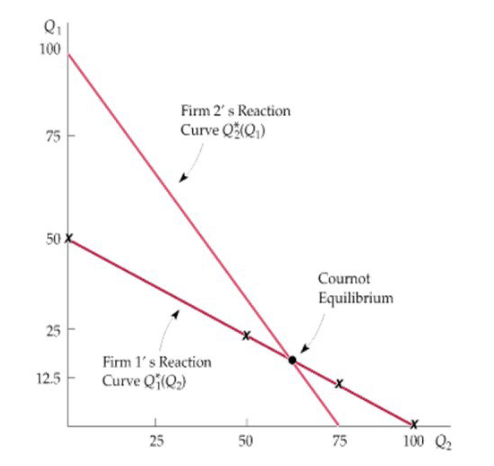

The Cournot Model

Firms produce a homogeneous good.

Each firm treats the output of its competitors as fixed.

All firms decide simultaneously how much to produce.

Reaction Curves

Relationship between a firm’s profit-maximizing output and the amount it thinks its competitor will produce.

In Cournot equilibrium, each firm correctly assumes the output of its competitor and maximizes its own profits.

Cournot Equilibrium

Equilibrium in the Cournot model where each firm accurately predicts its competitor's output and sets its production level accordingly.

Cournot equilibrium is an example of a Nash equilibrium.

No firm has an incentive to unilaterally change its behavior.

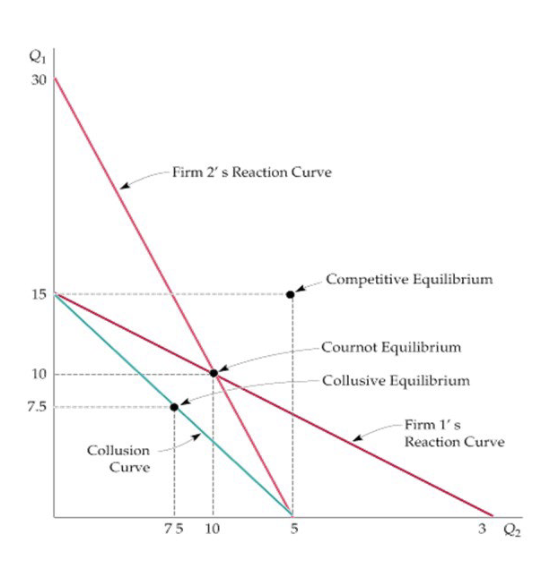

Duopoly Example

Demand curve:

Both firms have zero marginal cost.

In Cournot equilibrium, each firm produces 10.

If the firms collude and share profits equally, each will produce 7.5.

Competitive equilibrium: price equals marginal cost, and profit is zero.

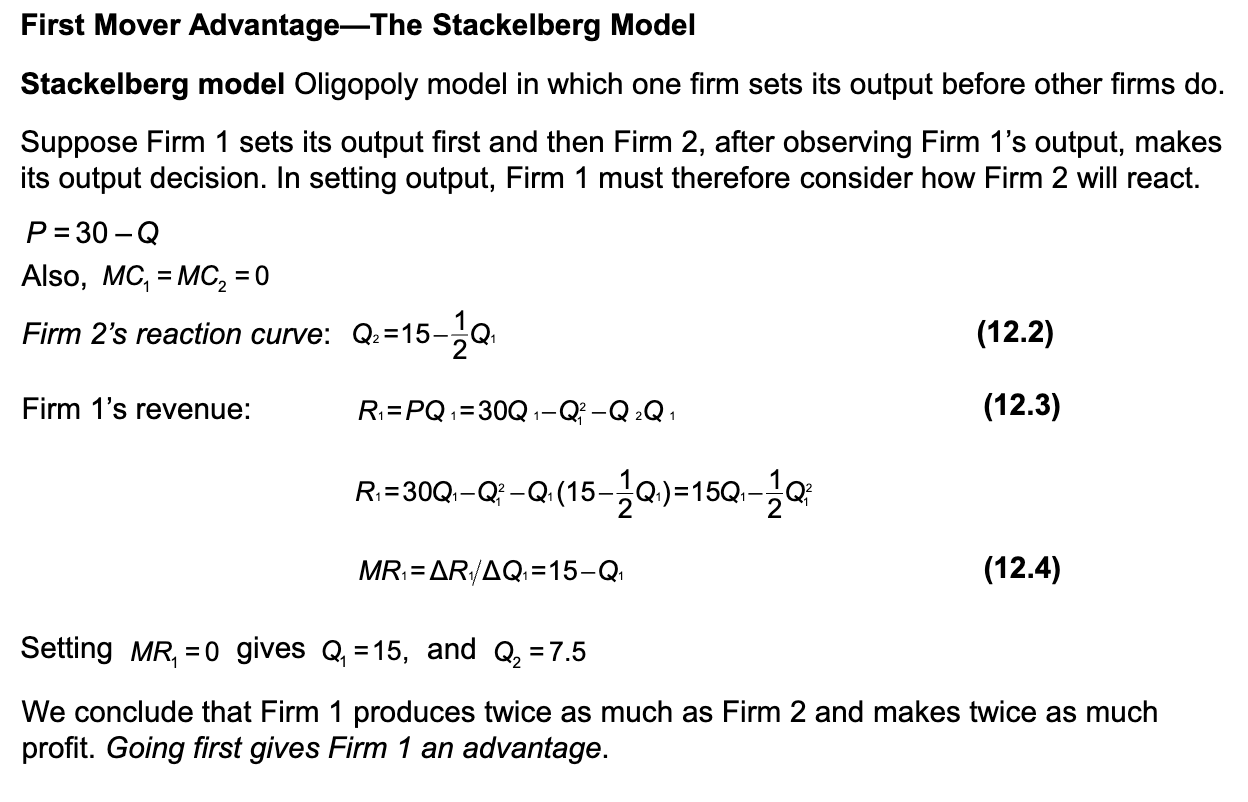

First Mover Advantage—The Stackelberg Model

Cartels

Producers explicitly agree to cooperate in setting prices and output levels.

If enough producers adhere to the cartel’s agreements and market demand is sufficiently inelastic, the cartel may drive prices well above competitive levels.

Cartels are often international.

U.S. antitrust laws prohibit American companies from colluding, but other countries’ laws are weaker.

Countries or companies owned/controlled by foreign governments may form cartels (e.g., OPEC).

Conditions for Cartel Success

A stable cartel organization must be formed whose members agree on price and production levels and then adhere to that agreement.

The potential for monopoly power. Even if a cartel can solve its organizational problems, there will be little room to raise price if it faces a highly elastic demand curve.

Successful cartelization requires:

Total demand for the good must not be very price elastic.

The cartel must control nearly all the world’s supply, or the supply of noncartel producers must not be price elastic.

Most international commodity cartels have failed because few world markets meet both conditions.

The Auto Parts Cartel

In September 2011, the U.S. Department of Justice (DOJ) announced the settlement of its investigation into an international auto parts cartel.

The cartel engaged in bid-rigging and price-fixing across a wide range of auto parts industries.

The investigations have led to criminal indictments of more than 58 individuals and 38 companies and have generated more than billion in fines.

The successful operation of the cartel was aided by regular communications, in which agreements were reached not only with respect to price but also on ways of monitoring the actions of the cartel members.

The extent to which the auto parts cartel has adversely affected car buyers is unclear.