Chapter 11 Banking Industry

Banking Structure and History

The chapter examines historical trends in the banking industry that explain the unique structure of the U.S. banking system.

Learning Objectives

Explain how financial innovation led to the growth of the shadow banking system.

Identify key structural changes in the commercial banking industry.

Summarize factors that led to consolidation in the commercial banking industry.

Assess reasons for separating banking from other financial services through legislation.

Summarize distinctions between thrift institutions and commercial banks.

Identify reasons for U.S. banks to operate in foreign countries and for foreign banks to operate in the United States.

Historical Context of U.S. Banking

Role of Government in Banking:

Alexander Hamilton, the 1st Treasury Secretary, argued for greater central control over banking.

he believed a strong, centralized national government was essential for the new United States to survive and grow

Fear of central power was a major impediment to the establishment of a strong centralized banking system.

Americans believed national authority could easily become tyrannical, threaten state sovereignty, and endanger the individual freedoms they had just fought to win.

Historical tension existed between agricultural interests and merchants.

Key Banking Institutions and Events

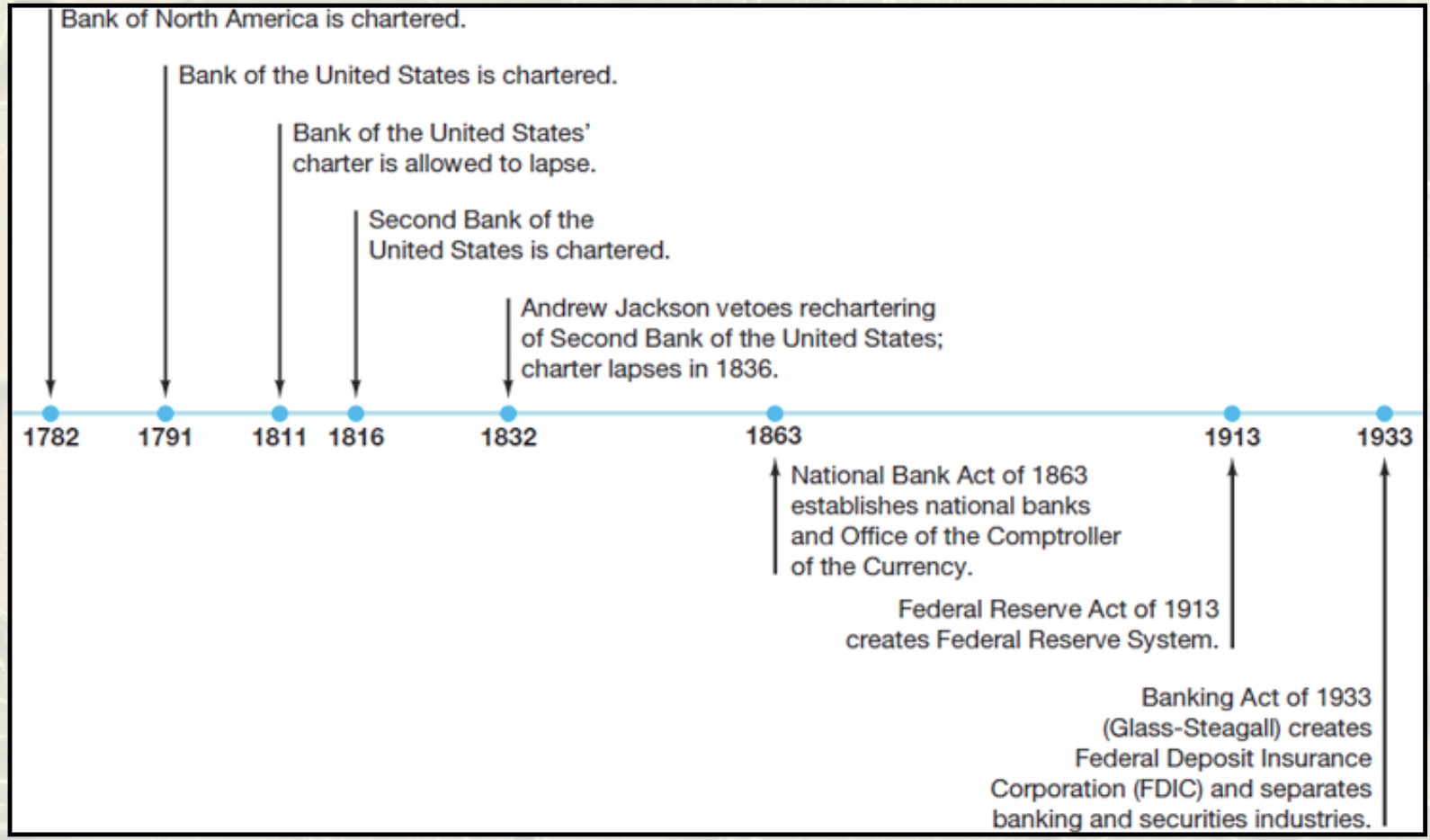

Timeline of Significant Banking Institutions:

Chartering Issues:

Bank of North America chartered in 1782 faced controversy.

The 1791 Bank of the United States served as a private central bank but had its charter not renewed in 1811 due to globalization and conflict between local control versus broader interests.

The War of 1812 renewed interest in a central banking institution due to state bank abuses, leading to the chartering of the 2nd Bank of the United States in 1816.

Post-1836 Developments:

From 1836 to 1863, banks were largely state-chartered with no national currency.

Banks issued notes that were theoretically backed by gold deposits.

The National Bank Act of 1863 created a system of federally chartered banks and introduced national currency but instability persisted.

Creation of the Federal Reserve:

The Federal Reserve System was established in 1913 as a true central bank.

The 1930-1933 period marked the beginning of the Great Depression with a financial crisis resulting in approximately 9,000 bank failures.

In response, the FDIC and the Glass-Steagall Act were passed in 1933 to separate commercial and investment banking and provide deposit insurance.

Banking Operations and Regulatory Changes

1950s and 60s:

Banking was characterized as boring with stable interest rates due to regulations that prevented competition and kept banks from becoming too large.

Standardized products led to the metaphor of the “bank toaster” from uniform interest rates and conditions.

Banks gave away toasters and small appliances to lure customers

Economic Challenges in the 1970s:

Inflation introduced uncertainty into the banking landscape.

The 1980s saw deregulation under the Reagan administration, leading to innovations and significant changes in the banking industry.

Summary of American Banking History

Early Impressions:

Concerns about centralization persisted; early banking featured small institutions, lack of regulations, and complicated structures.

Boom and bust periods were prevalent, culminating in the Great Depression, which brought about extensive regulation.

The banking sector remained small but stable post-regulation until inflation and deregulation prompted further consolidation and innovation.

Banking Innovation

Drivers of Financial Innovation:

Financial innovation is primarily driven by the desire for profit, stimulating the search for new profitable products.

Financial Engineering:

use of math models, statistics, and computer programming to design financial products, manage risk

Demand Side Changes (Inflation and Interest Rates):

The inflation of the 1970s and the end of interest rate regulations introduced volatility.

Introduction of adjustable-rate mortgages (ARMs) allowed banks to maintain profitability during periods of rising interest rates. Lower initial rates on ARMs made them attractive to homebuyers.

Development of financial derivatives enabled institutions to hedge interest rate risks with payoffs linked to previously issued securities.

Supply Side Changes (Technology):

Advancements in computer technology lowered transaction costs and facilitated data computations necessary for pricing new products. Key innovations included:

Bank credit and debit cards

Electronic banking

ATMs, home banking, and virtual banking

Junk bonds

The commercial paper market

Securitization

Securitization and Its Impact

What is Securitization?:

Securitization is the process of transforming illiquid financial assets into marketable capital market securities. This played a crucial role in developing the subprime mortgage market in the mid-2000s.

Ex: like mortgages, car loans, student loans, or credit card debt) and turning them into tradable securities that investors can buy

Decline of Traditional Banking:

A shift occurred from borrowers seeking loans directly from banks funded by depositors to a market where companies and individuals acquired funds directly through bonds, commercial paper, and mortgage-backed securities.

Traditional banks increased their reliance on fees and services, prompting a push for consolidation in the industry.

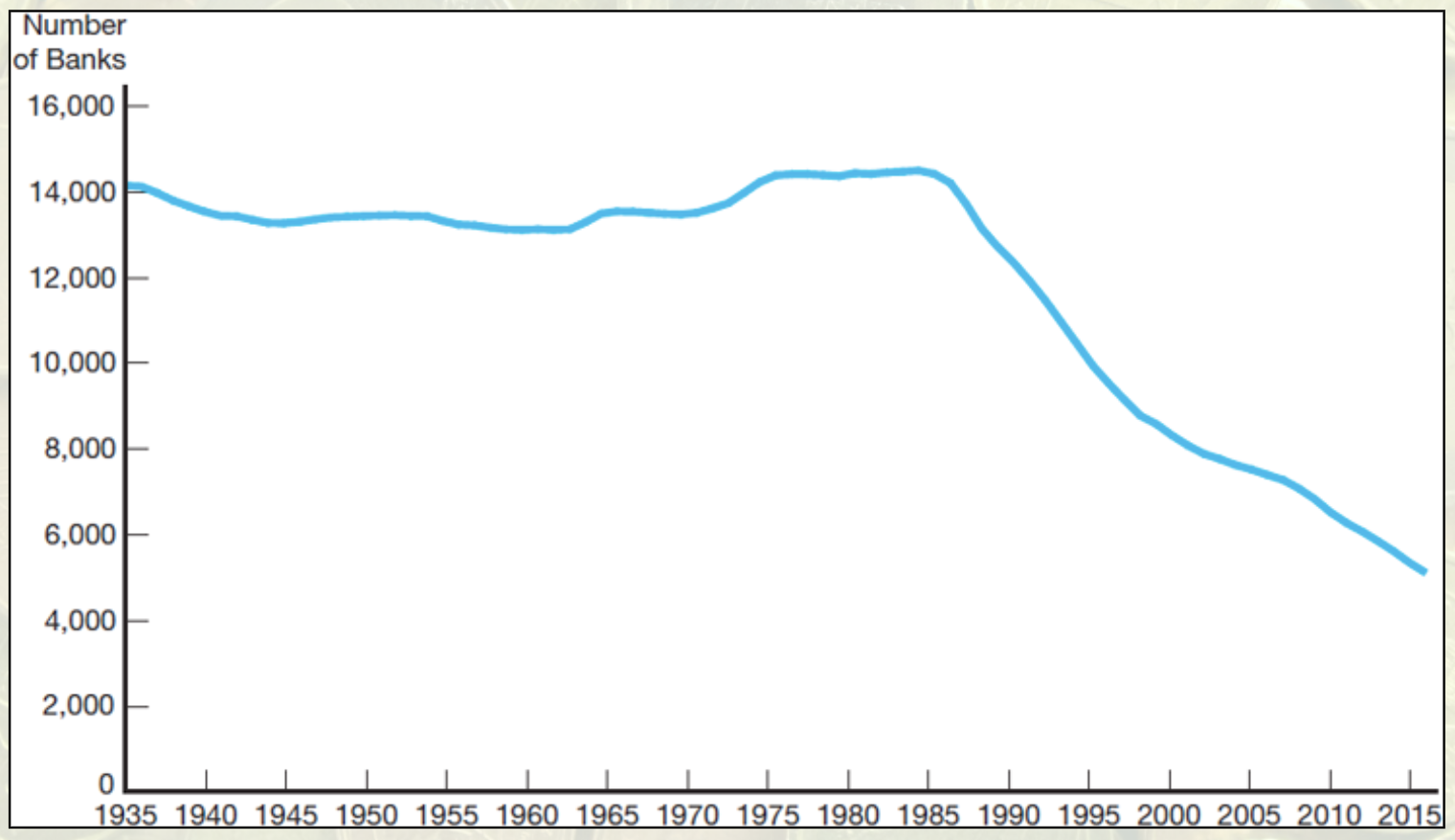

Trends in Number of Banks Over Time:

A dramatic decline in the number of banks has been observed over the last 30 years, attributed to:

Deregulation through the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

Economies of scale and scope enabled by information technology.

The decline results in not only fewer institutions but also a shift of assets towards larger banks.

Evaluating Consolidation in Banking

Pros of Consolidation:

Increased competition forces inefficient banks to close.

Gains in efficiency due to economies of scale and scope can be beneficial.

A more diversified portfolio decreases the probability of bank failures.

Cons of Consolidation:

The elimination of community banks could lead to reduced lending to small businesses.

Expansion risks associated with banks moving into new areas may increase the likelihood of failure.

Legislative Changes Affecting Banking

Gramm-Leach-Bliley Financial Services Modernization Act of 1999:

This act abolished the Glass-Steagall Act, changing the regulatory landscape around banking.

States retained regulatory authority over insurance activities while the SEC continued to oversee securities activities.

The Office of the Comptroller of the Currency regulated banking subsidiaries involved in securities underwriting, and the Federal Reserve maintained oversight of bank holding companies, further incentivizing consolidation in the banking sector.

Globalization and International Banking

Impact of Globalization on Banking:

Increased regulation and a trend towards globalization and international trade supported the growth of international banking.

Expansion of international trade and the activities of multinational corporations made global investment banking highly profitable.

Banks gained access to the Eurodollar market, enhancing the availability of funds.

Eurodollar Definition:

Eurodollars are dollar-denominated deposits held in banks outside the United States, originating during the Communist period as a response to U.S. dollar demand.

These deposits are the most widely used currency in international trade and are outside the scope of U.S. regulations, representing a significant source of funds for U.S. banks.

Concluding Questions

Reflect on whether the trend of deregulation, growing size and complexity of banks, and the sophistication of financial instruments are leading to a more stable or less stable banking system.