Impact of inventory

Effects of purchasing and selling inventory

Assets = Liabilities + Equity

The relationship between a business’s resources (assets), its debts or obligations (liabilities), and the ownership interest in the business (equity)

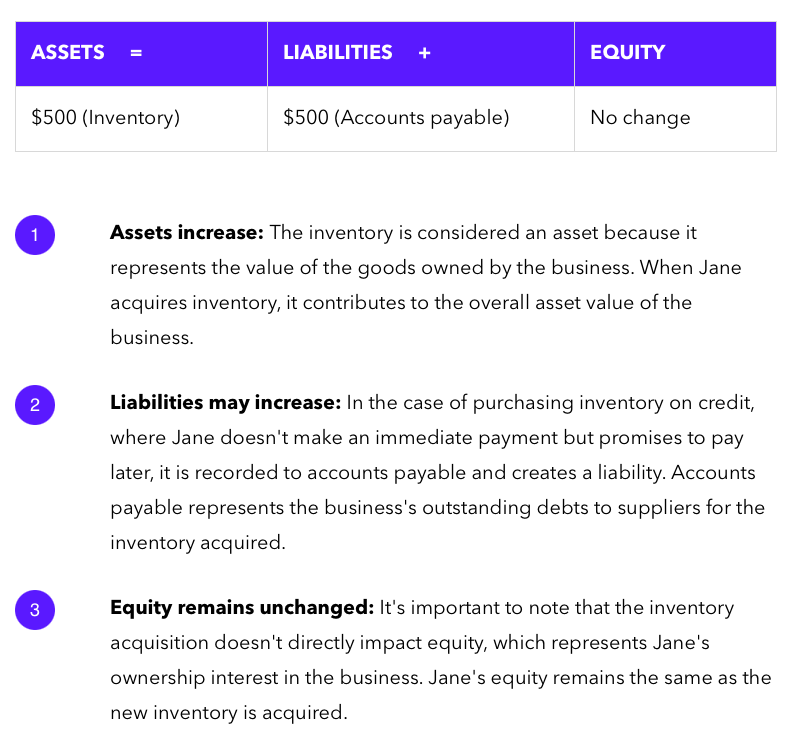

Purchasing inventory

When Jane purchases $500 in inventory from suppliers on credit, it affects the accounting equation in the following manner:

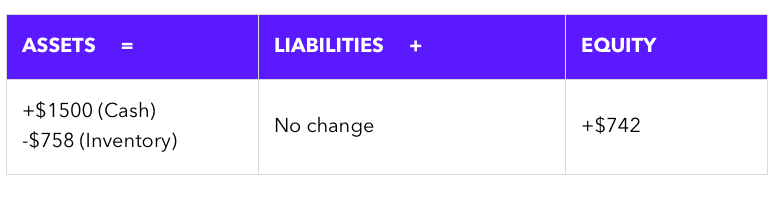

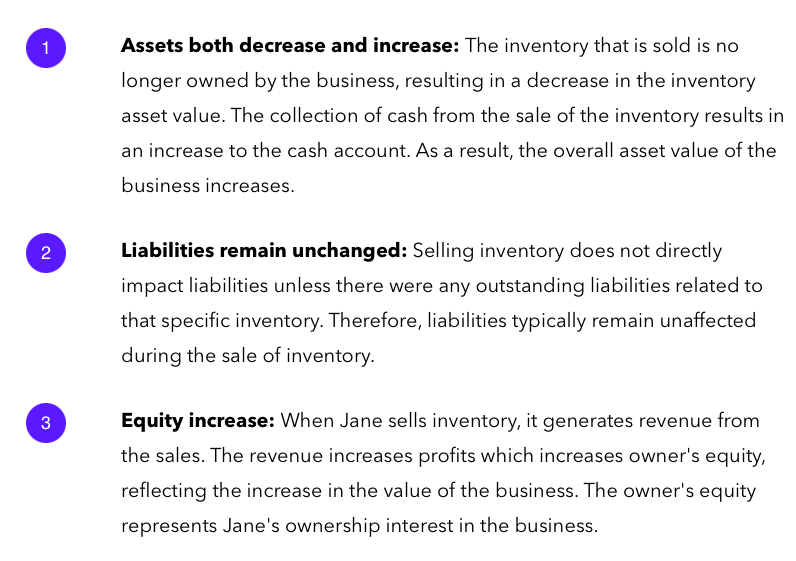

Selling inventory

Selling inventory

When Jane sells $758 of her inventory to customers for $1500, the following changes occur:

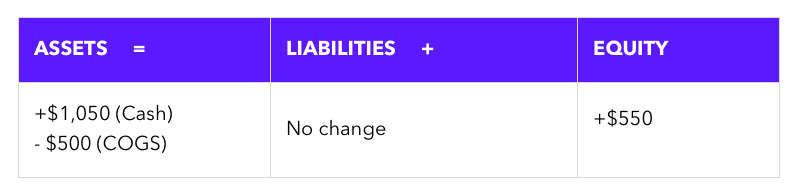

COGS raw material to finished goods

COGS raw material to finished goods

$500 of finished goods is sold and generates $1,050 in sales (finished goods). The goods are paid for with cash.

If ending inventory is overstated

If ending inventory is overstated

Assets are overstated

Ending inventory is an asset, but if mistakenly recorded at a higher value, it inflates the overall asset value, leading to over reporting of the business’s assets

Equity is overstated

Overstating assets affects equity directly as assets are a part of the accounting equation.

Equity is affected by net income, and COGS affects net income, so a lower COGS value results in an overstatement of equity

Liabilities remain unaffected

Inventory counting errors have no direct impact on the liabilities of the business.

Inaccurate inventory records could indirectly affect liabilities if they lead to wrong expense or payable calculations

If ending inventory is understated

Assets are understated

Since ending inventory is an asset, this decreases the overall reported asset value

Equity is understated

Similar to the effect on assets, an understatement of assets directly affects equity

With lower asset values, the equity of the business is also decreased

Liabilities remain unaffected

Inventory counting errors generally do not directly impact liabilities.

If they result in incorrect calculations of expenses or payable amounts, they could indirectly affect liabilities