QUIZ 2 and 4 NOTES (MCGRAW & QUIZ)

CHAPTER 16: NOTES PAYABLE AND NOTES RECEIVABLE

Notes:

360 day period= banker’s year

cash is yung buong value, then notes payable and trade are separated

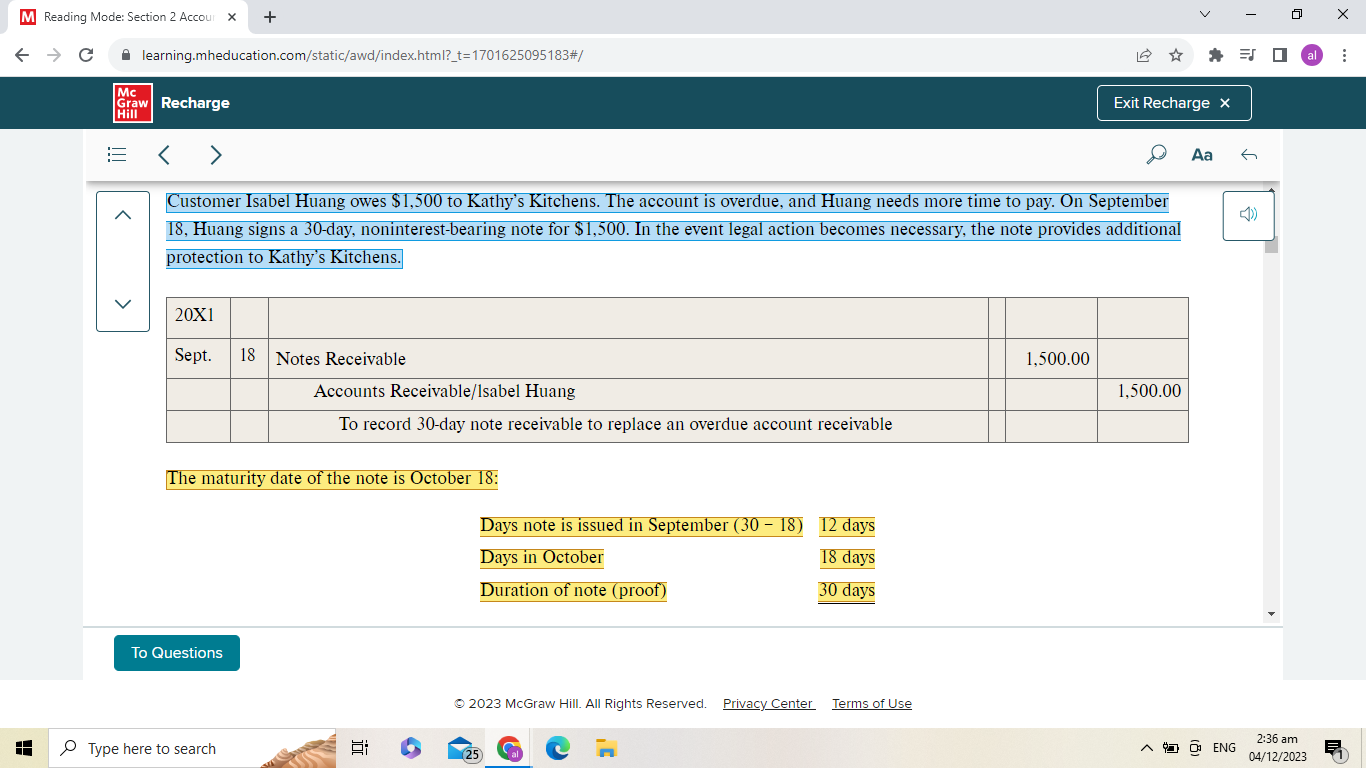

Issue date is not counted. For example, for a 30-day note issued on January 1, you start counting at January 2 — thus, January 31 ang maturity date.

Interest expense is a nonoperating expense, deducted from income from operations

To-do:

PROBLEM-SOLVING NOTES:

FDN Accounting Services has the following information related to its Accounts Payable:

• On September 1, 2023, the Accounts Payable balance was ₱60,200.

• During September, a purchase of equipment amounting to ₱300,000 was made on terms

20% down, balance on account.

• Total payments made to various suppliers during the month amounted to ₱170,400.Compute the balance of Accounts Payable on September 30, 2023.

129800

doon sa equipment, ang kinuha yung 80%

FDN Accounting Services has the following ledger balances as of September 30, 2023:

Cash ₱ 265,000

Accounts Receivable 57,000

Equipment 179,400

Prepaid Expenses 28,000

Accounts Payable 177,500

F. D. Nakpil, Capital (before Net Income/Loss) 259,800

Service Revenue 180,000

Operating Expenses 87,900

Compute the total amount indicated in the Debit Column of the Trial Balance of FDN as of

September 30, 2023.Cash ₱ 265,000

Accounts Receivable 57,000

Equipment 179,400

Prepaid Expenses 28,000

Operating Expenses 87,900

Total debit ₱ 617,300these are basically just the assets.

the drawings are debit normal side

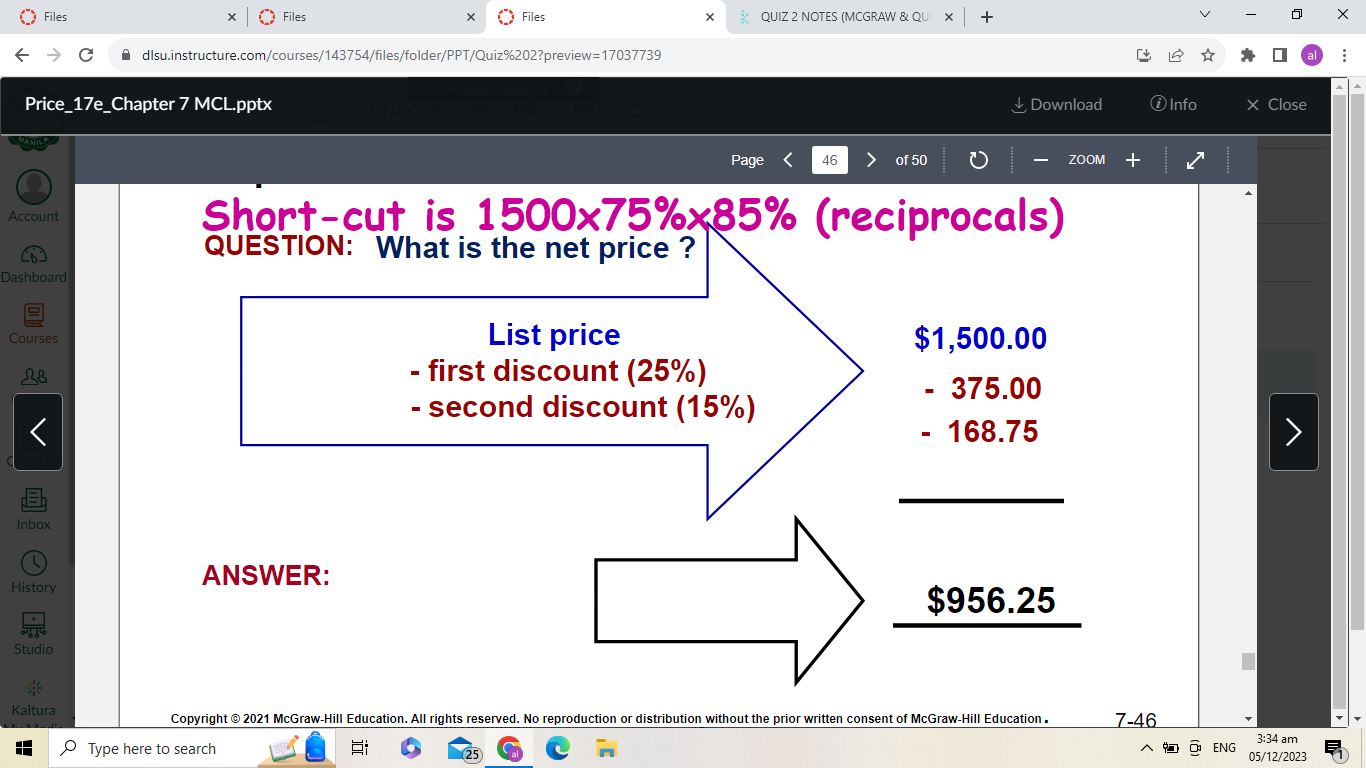

FDN Trading made sales with a list price of ₱40,000 and trade discount of 8%. Compute the

Invoice Price to be recorded as SalesList Price ₱ 40,000

Trade discount -3,200

Invoice Price ₱ 36,800trade discount yung babaligtarin percent

FDN Trading sold merchandise to a customer on credit in the amount of ₱45,000. FDN issued a credit memo for ₱4,000 due to damages during shipping. The invoice is dated September 15

with terms 1/15, net 45. If the customer chooses not to take the cash discount, compute the

balance of the accounts receivable account pertaining to this customer by September 3041k

sales account - sales returns and allowances

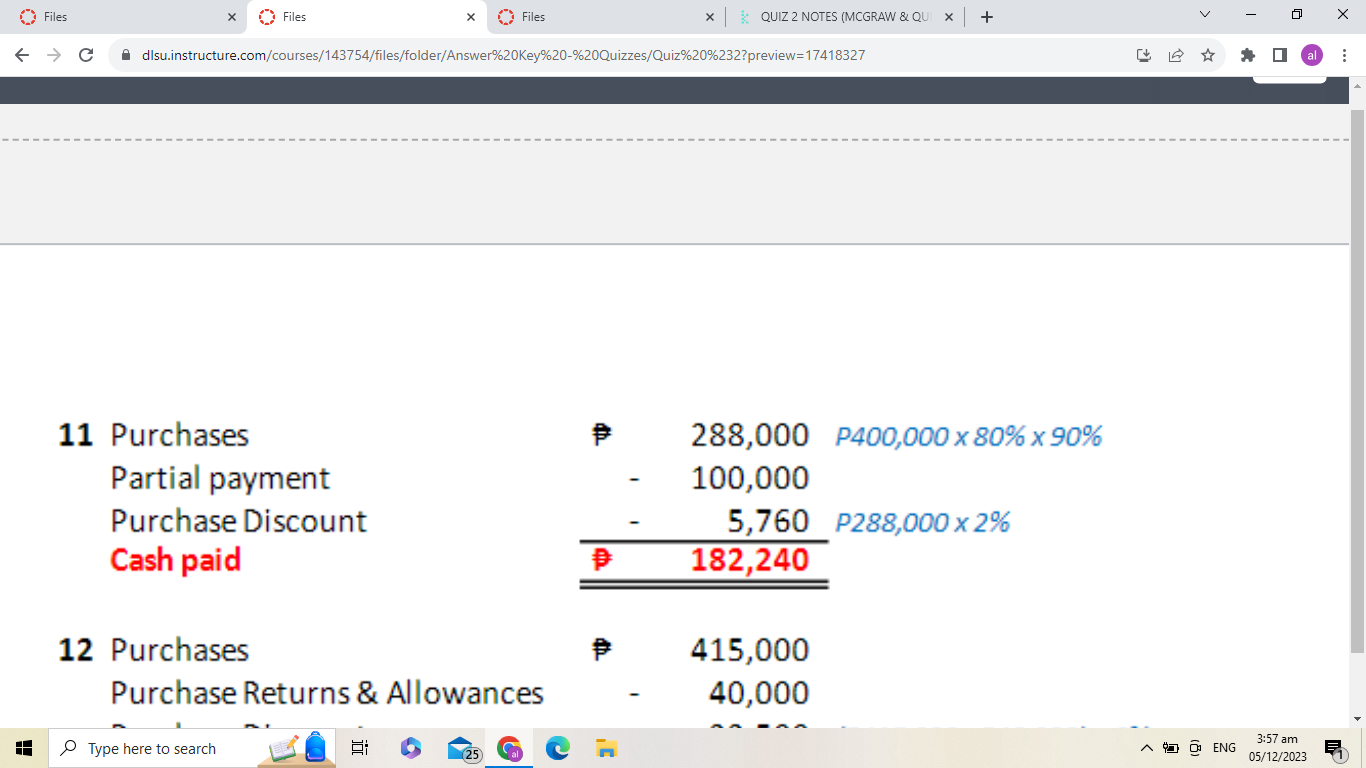

FDN Trading recorded the following events involving a recent purchase of merchandise:

• Purchased goods for ₱400,000, less 20% and less 10%, on terms 2/10, n/30.

• Paid ₱500 freight on terms, FOB Shipping Point, Collect

• Made a partial payment of ₱100,000.

• Paid the invoice within the cash discount period.

Compute the cash payment to the seller on the final date of settlement.

FOB here, buyer pays directly not to seller

purchase discount is applied as purchases full ah

pag partial payment, - sa cash paid

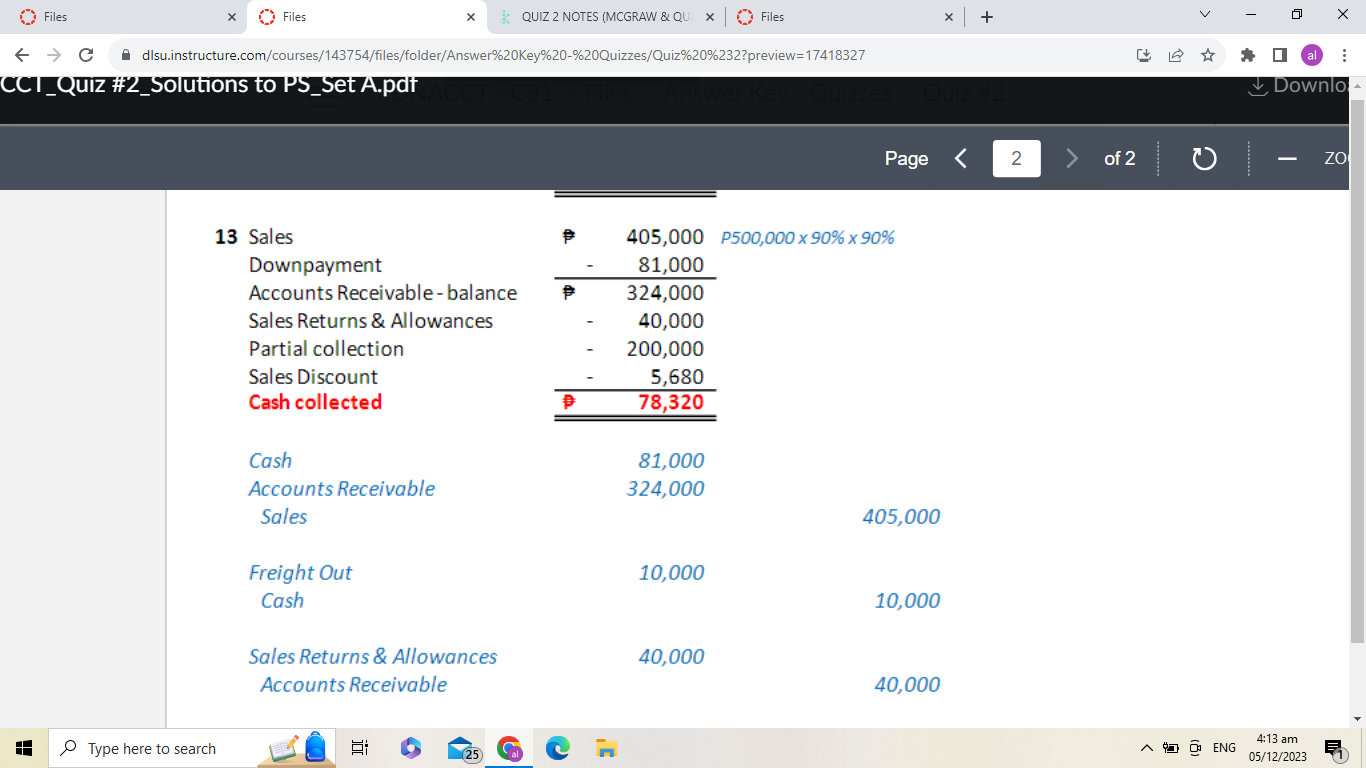

On September 1, 2023, FDN Trading sold merchandise for ₱500,000 less 10% and 10% on

terms 20% down, balance 2/20, n/90. The related freight amounted to ₱10,000 on terms FOB

Destination, Prepaid. The customer returned goods amounting to ₱40,000 and made a partial

payment of ₱200,000. The account was collected on September 21. Compute the final amount

of cash collected on September 21.

GENERAL NOTES

Net sales= sales - sales returns allowances - sales discounts

Net cost of purchases= purchases + freight in - purchase discounts - purchase returns and allowances

net purchases= purchases - returns - discount

how to get total goods available= get purchases, purchase cost, then add mi, beg to purchase cost to get total goods available

credit memo= sales return and allowances

cost of goods= net purchases + freight in

Net 30 days or n/30:

Payment in full is due 30 days after the date

of the invoice.

Net 10 days EOM, or n/10 EOM:

Payment in full is due 10 days after the end

of the month in which the invoice was

issued.

2% 10 days, net 30 days; or 2/10, n/30:

If payment is made within 10 days of the

invoice date, the customer can take a 2%

discount. Otherwise, payment in full is due

in 30 days.

OTHER NOTES

2 forms of income statement": natural and functional

financial statement is presented in 3: income, soe, balance sheet

1/15, net 45- 1% discount if paid within 15 days, 45 days

NEED TO WORK ON:

normal balance

financing, investing, operating

QUIZ 4

net income= get net sales, multiply it with gross profits, then subtract operating expenses

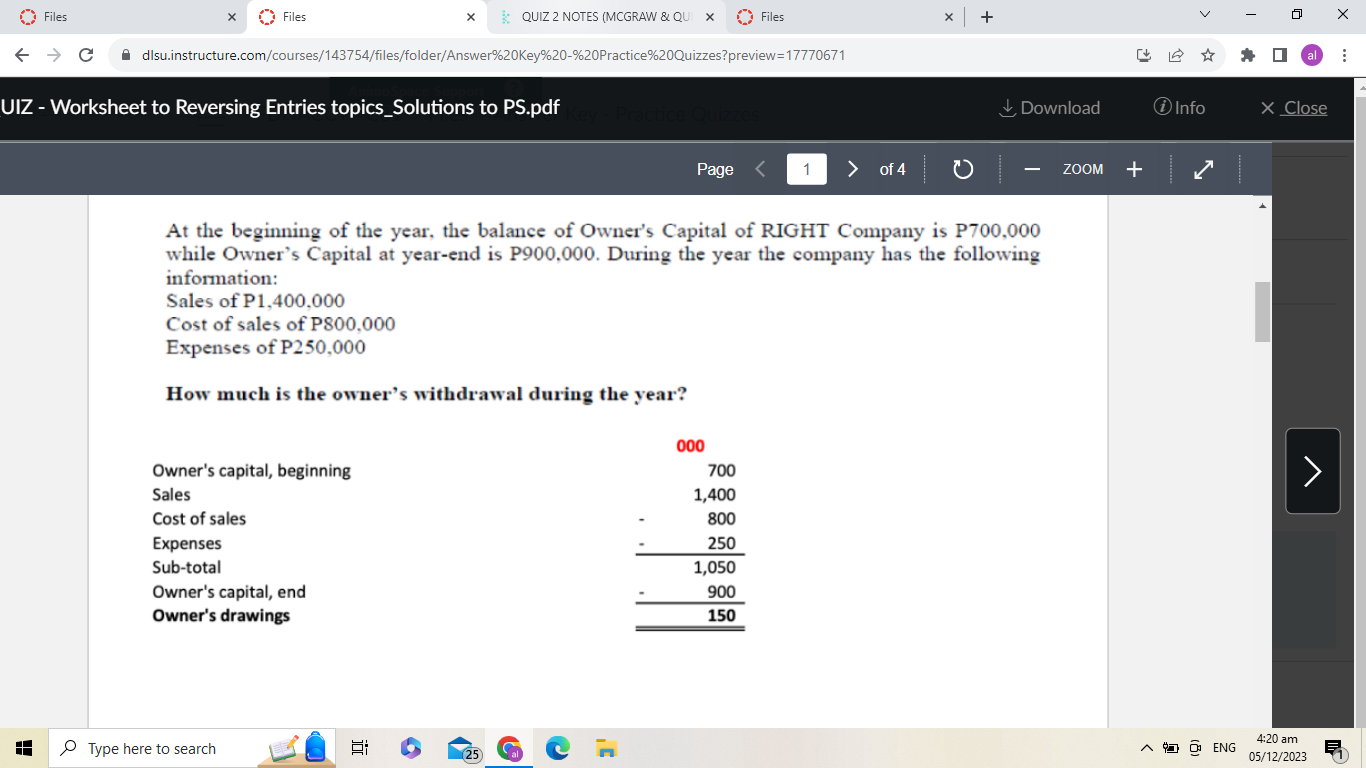

owner’s drawings= pagadd lahat sa beg. capital, then subtract subtotal with end. capital

cogs= beg. inv + net cost of purchases + cogs avail for sale - end. inv

get cogs avail for sale muna

cogs at its core is = cogs available for sale - ending inventory

beg. inv + net cost = total goods available

total goods - ending inv.= cost of goods sold

total assets- total current/noncurrent = the other type of asset