Chapter 4 - Accrual Accounting Concepts

4.1 Accrual-Basis Accounting and Adjusting Entries

Accounting divides the economic life of a business into artificial time periods.

Periodicity assumption - An assumption that the economic life of a business can be divided into artificial time periods.

Accounting periods are generally a month, a quarter, or a year.

Fiscal year - An accounting time period that is one year long.

Since many business transactions affect more than one time period, companies allocate the cost to the periods of use.

To easily determine the amount of revenues and expenses to report in a given accounting period, two principles are used as guidelines:

Revenue recognition principle

Expense recognition principle

The Revenue Recognition Principle

Performance obligation - When a company agrees to perform a service or sell a product to a customer.

Revenue recognition principle - It requires that companies recognize revenue in the accounting period in which the performance obligation is satisfied.

Five-Step Revenue Recognition Process

Identify the contract with customers

Identify the separate performance obligations in the contract

Determine the transaction price

Allocate the transaction price to the separate performance obligations

Recognize revenue when each performance obligation is satisfied

The Expense Recognition Principle

There is one rule that must be followed:

Let the expense follow the revenues.

The expense should be reported in the same period in which it recognizes the service revenue.

The critical issue is recognizing when the expense makes its contribution to revenue.

It might not be the same period in which the expense is paid.

Expense recognition principle - It requires that companies recognize expenses in the period in which they make efforts to generate revenue.

Accrual vs Cash Basis of Accounting

Accrual-basis accounting - It means that the transactions that change a company’s financial statements are recorded in the periods in which the events occur, even if cash was not exchanged.

It uses the revenue recognition principle and the expense recognition principle.

Even though different accounting standards are used by companies in other countries, the accrual basis of accounting is central to all of these standards.

Cash-basis accounting - Companies record revenue when the cash is received and record expenses when they pay out cash.

This method is not in accordance with GAAP. It produces misleading financial statements.

The Need for Adjusting Entries

Adjusting entries - Entries made at the end of an accounting period to ensure that the revenue recognition and expense recognition principles are followed.

They are required every time a company prepares financial statements.

Every entry will include one income statement account and one balance sheet account.

They’re necessary since the trial balance may not contain updated and complete data for several reasons:

Some events aren’t recorded daily because it’s not efficient, like the use of supplies and the earning of wages by employees.

Some costs aren’t recorded during the accounting period because these costs expire with time rather than as a result of recurring daily transactions. Ex. → Charges related to the use of buildings an equipment, rent, and insurance.

Events that are unrecorded due to unreceived documents like an utility service bill.

Types of Adjusting Entries

Deferrals

Prepaid expenses - Expenses paid in cash before they’re used or consumed.

Unearned revenues - Cash received before services are performed.

Accruals

Accrued revenues - Revenues for services performed but not yet received or recorded

Accrued expenses - Expenses incurred but not yet paid in cash or recorded

4.2 Adjusting Entries for Deferrals

Deferrals - Expenses or revenues that are recognized a date later than the point when cash was originally exchanged.

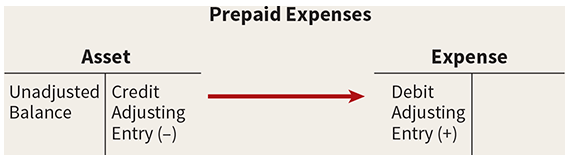

Prepaid Expenses

Prepaid expenses - Expenses paid in cash before they are used or consumed.

When expenses are prepaid, an asset account is debited (increased) to show the service or benefit that the company will receive in the future.

Prepaid expenses are costs that expire with time (rent and insurance) or through use (supplies).

Since the expiation of these costs doesn’t require daily entries, companies postpone their recognition until they prepare financial statements.

At each statement dates, adjusting entries are made to record the expenses applicable to the current accounting period and to show the remaining amounts in the assets accounts.

Before adjustment, assets are overstated and expenses are understated. This means that an adjusting entry for prepaid expenses increases the expense account (debit) and decreases the asset account (credit).

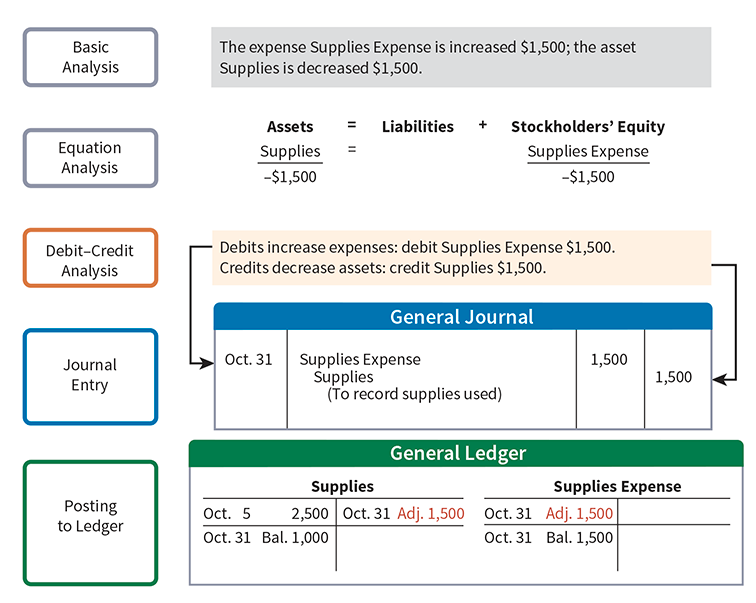

Supplies

The purchase of supplies increases the asset account (debit).

Instead of recording supplies expense as the supplies are used, companies recognize supplies expense in a single entry, at the end of the accounting period.

The difference between the unadjusted balance in the supplies (asset) account and the actual cost of supplies on hand represents the supplies used (expense) for that period.

Adjusting entries have no effect on cash flows, so the cash flow effects are not represented.

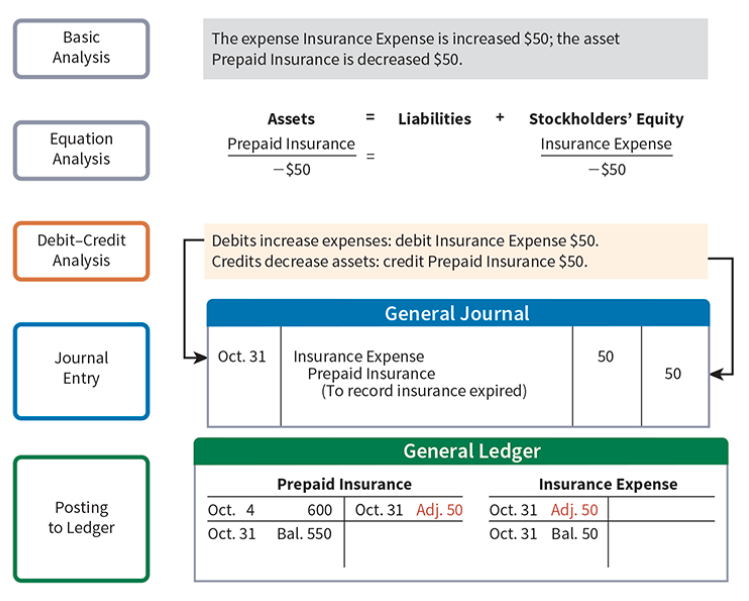

Insurance

The cost of insurance paid in advance is recorded as an increase (debit) in the asset account Prepaid Insurance.

At the financial statement date, companies increase (debit) Insurance Expense and decrease (credit) Prepaid Insurance for the cost of insurance that has expired during the period.

Depreciation

Useful life - The length of service of a productive asset.

Since a building is expected to be in service for many years, it’s recorded as an asset, not as an expense.

To follow the expense recognition principle, companies allocate a portion of the cost to expense during each period of the asset’s useful life.

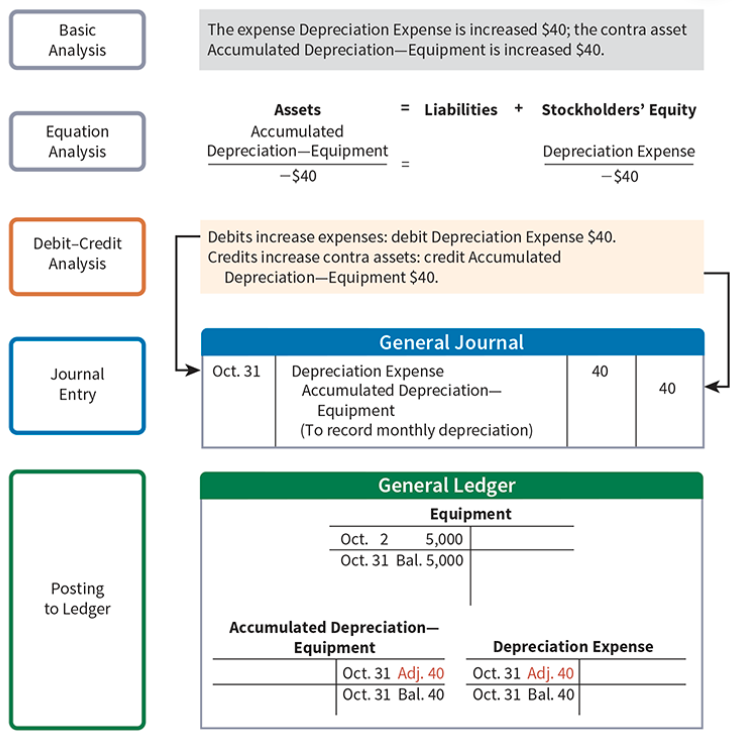

Depreciation - The process of allocating the cost of an asset to expense over its useful life.

The acquisition of long-lived assets is essentially a long-term prepayment for the use of an asset.

An adjusting entry for depreciation is needed to recognize the cost that has been used (expense) during the period and to report the unused cost (asset) at the end of the period.

Depreciation is an allocation concept, not a valuation concept.

It allocates an asset’s cost to the periods in which its used

Contra asset account - An account that is offset against an asset account on the balance sheet.

Accumulated depreciation

All contra accounts have increases, decreases, and normal balances opposite to the account to which they relate.

The balance in Accumulated Depreciation—Equipment account will increase $40 each month, and the balance in Equipment remains 5,000.

The normal balance of a contra asset account is a credit.

An alternative to using a contra asset account is to decrease (credit) the asset account by the amount of depreciation each period.

But the contra asset account is preferable because it discloses both the original cost of the equipment and the total cost that has expired to date.

Book value (Carrying value) - The difference between the cost of any depreciable asset and its related accumulated depreciation.

Book value and fair value are different things.

The purpose of depreciation isn’t valuation but a means of cost allocation.

Depreciation expense identifies the portion of an asset’s cost that expired during the period.

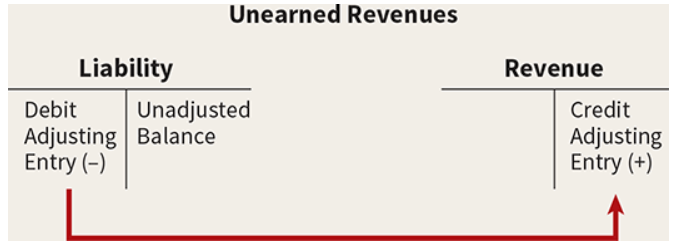

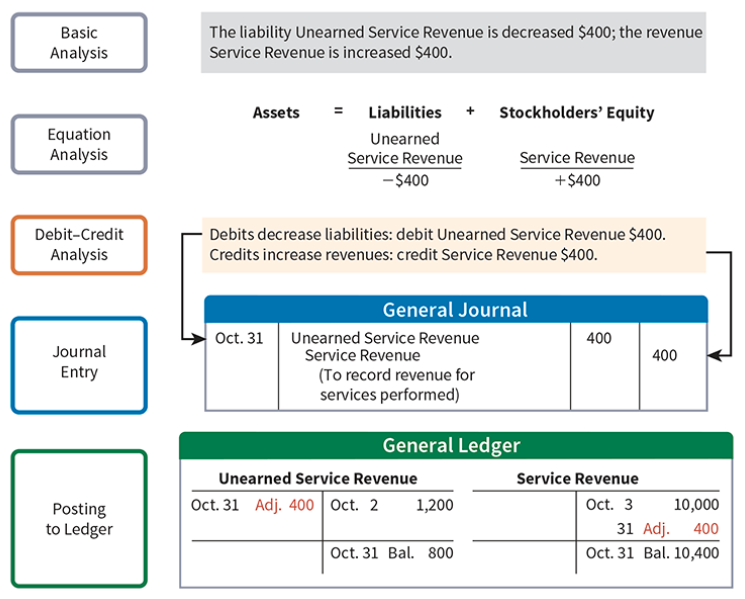

Unearned Revenues

Unearned revenues - Cash received and a liability recorded before services are performed.

The company has a performance obligation to provide a service for one of its customers.

They are the opposite of prepaid expenses.

It is a liability account used to recognize the obligation exists.

When a company receives payment for services to be performed in a future accounting period, it increases (credits) an unearned revenue account.

It delays recognition of revenue until the adjustment process.

Then, it makes an adjustment entry to record the revenue for services performed during the period and to show the liability that remains at the end of the accounting period.

Before adjustment, liabilities are overstated and revenues are understated.

The adjusting entry for unearned revenue results in a decrease (debit) to a liability account and an increase (credit) to a revenue account.

4.3 Adjusting Entries for Accruals

Accruals - Expenses or revenues that are recognized at a date earlier than the point when cash is exchanged.

Before adjustment, the revenue account and the related asset account or the expense account and the related liability account are understated.

The adjusting entry will increase both a balance sheet and an income statement account.

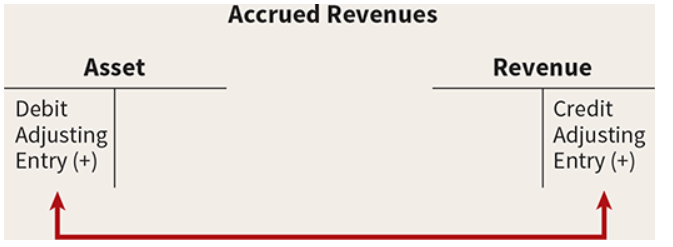

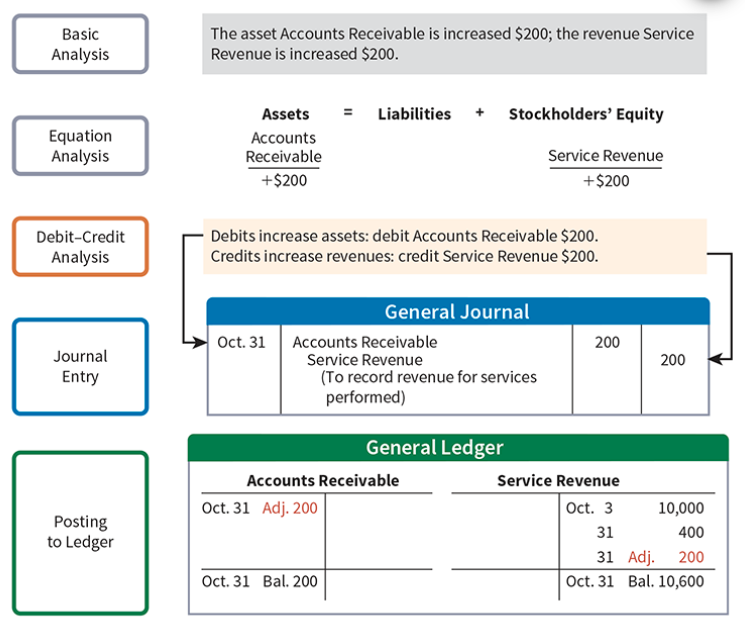

Accrued Revenues

Accrued revenues - Revenues for services performed but not yet received or recorded at the statement date.

Accrued revenues may accumulate with time, like interest revenue. These are unrecorded because the earning of interest doesn’t involve daily transactions.

They also may result from services that have been performed but not yet billed or collected, like commissions and fees. These may be unrecorded since only a portion of the total service has been performed and the clients won’t be billed until the service has been completed.

An adjusting entry for accrued revenues results in an increase (debit) to an asset account and an increase (credit) to a revenue account.

For accruals, there may have been no prior entry, and the accounts requiring adjustment may both have zero balances prior to adjustment.

Without the adjusting entry, assets and stockholder’s equity on the balance sheet are understated as well as revenues and net income on the income statement.

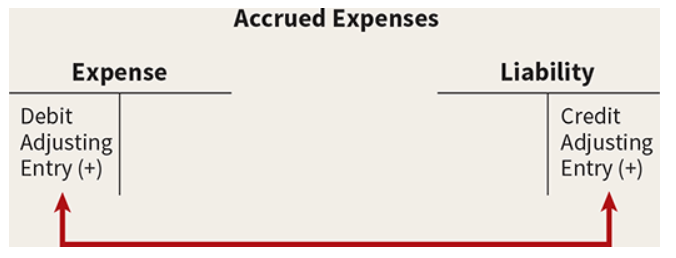

Accrued Expenses

Accrued expenses - Expenses incurred but not yet paid or recorded at the statement date.

Interest, taxes, and utilities.

Adjustments are made to record the obligations that exist at the balance sheet date and to recognize the expenses that apply to the current accounting period.

Before adjustment, liabilities and expenses are understated.

An adjusting entry for accrued expenses results in an increase (debit) to an expense account and an increase (credit) to a liability account.

Accrued Interest

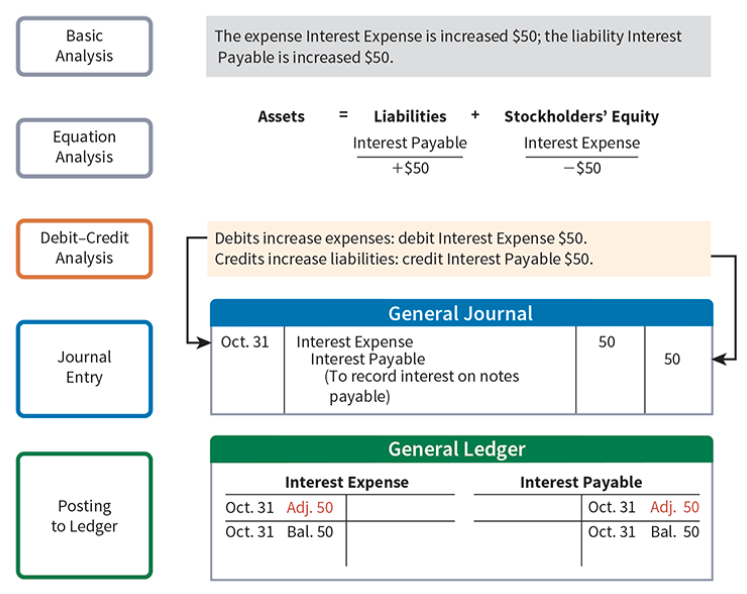

The amount of the interest recorded is determined by three factors:

The face value of the note

The interest rate, always expressed as an annual rate

Length of time the note is outstanding

In compounding interest, we express the time period as a fraction of a year.

Interest Expense shows the interest charges for the month of October.

Interest Payable shows the amount of interest the company owes at the statement date.

Companies use the Interest Payable account instead of crediting Notes Payable to show two different types of obligations (interest and principal) in the accounts and statements.

Without the adjusting entry, liabilities and interest expense are understated while net income and stockholder’s are overstated.

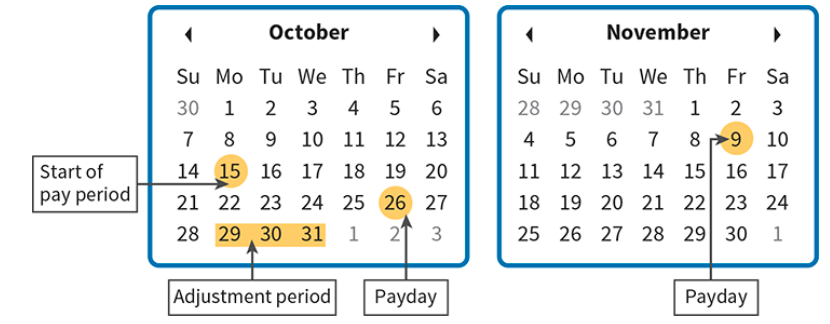

Accrued Salaries and Wages

Companies paid salaries on October 26 for its employees’ first two weeks of work (Oct 15 - Oct 26). The next payments won’t occur until Nov 9 leaving three working days of unpaid salaries and wages in October.

At Oct 31, the salaries for these three days represent an accrued expense and a related liability to the company. Employees receive total salaries of $2,000 for a 5 day work week or $