AOS 4 - Depreciation

Depreciation

Allocation of the cost a non-current asset incurs over its useful life, though not all non-current assets are depreciated. Only those with a Finite Life - limited time the asset will exist.

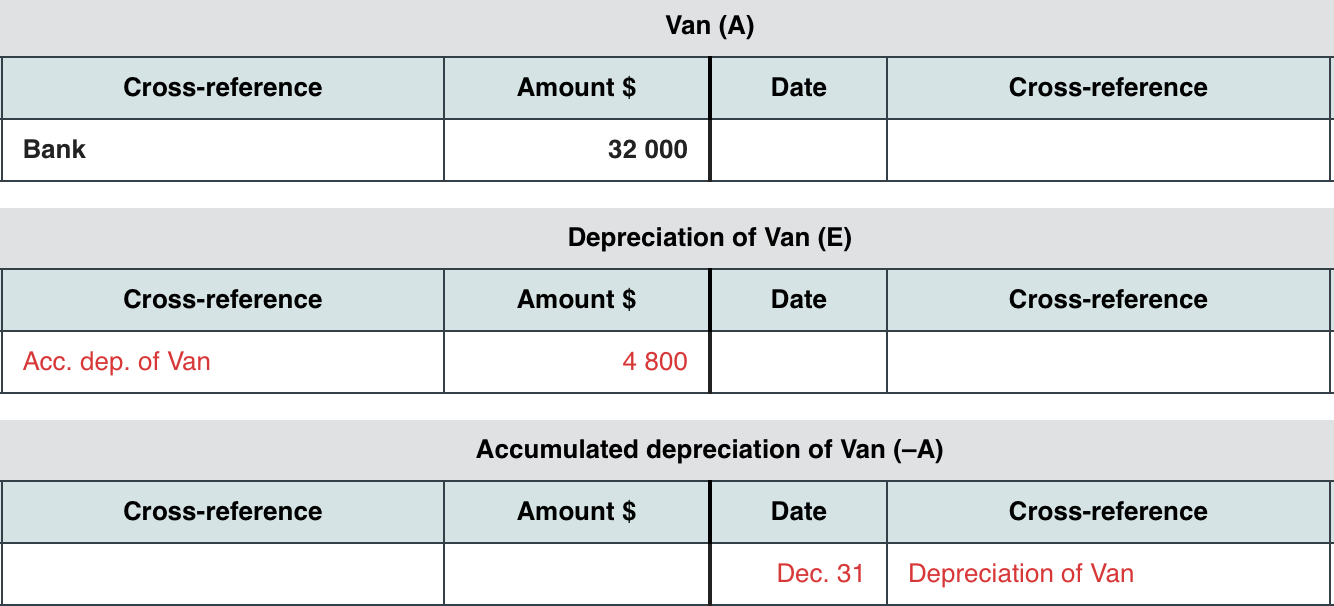

Depreciation Expense: The allocation of a NCA cost over its useful life, reported as an expense in the Income Statement for one specific period.

Accrual Basis - as the non-current asset is losing value form use, this must be recorded as an expense incurred

Faithful Representation - as the real world value decrease, this should be accurately depicted in their finances as the asset’s value decreases.

Accumulated Depreciation: The total depreciation a non-current asset has incurred over its life to date,

Carrying Value: value of a non-current asset that is yet to be incurred, plus any residual value.

Historical Cost: the original purchase price of a non-current asset

Residual Value: the estimated value of a non-current asset at the end of it’s useful life

Useful Life: the estimated period of time the NCA will be used by the current entity.

Depreciation Methods

The depreciation method should match the revenue earning pattern of the asset (Faithful Rep)

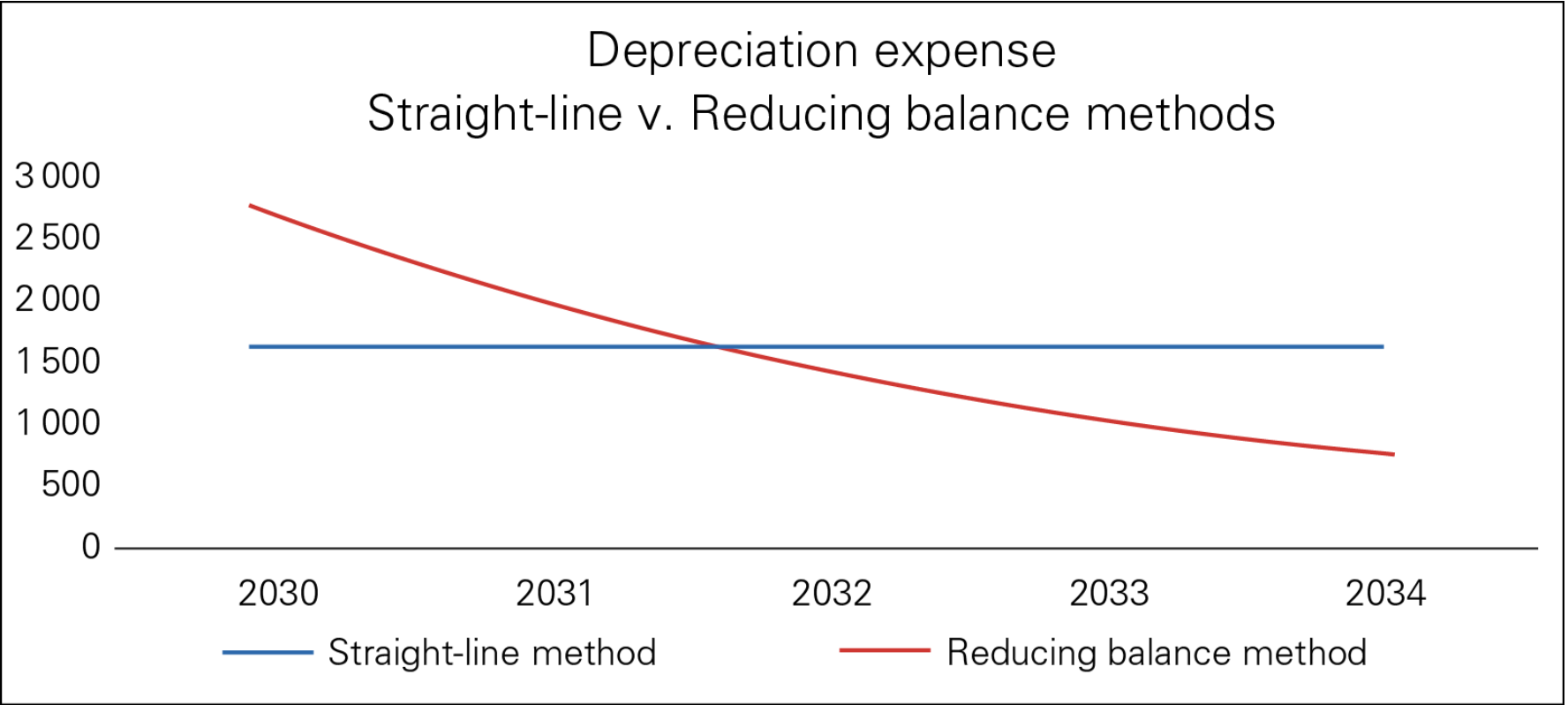

Straight Line Depreciation | Reducing Balance | |

Assumption | Assumes the asset will continuously generate a consistent level of revenue over its useful life. | Assumes the asset will generate greater benefits in its earlier years, which gradually deteriorate over time. |

Asset Type | Few moving parts | Lots of moving parts |

Example |

|

|

Expense Pattern | Same amount each year | More depreciation expense at start |

Rationale | does same job as when its old or new | Likely more efficient and productive at start of life, thus generating more revenue at start of life |

Calculation | percentage of Historical Cost | Percentage of Carrying Value |

Disposal of a Non-Current Asset

We use the temporary Disposal Account for these 4 transactions

Step 1 - Remove the Asset’s Historical Cost

Step 2 - Remove the Accumulated Depreciation

Step 3 - Record the Proceeds of the Sale

Step 4 - Calculate the Profit/Loss on disposal of NCA

Carrying Value - Sold For

Profit - goes under Other Revenues

Loss - go under Less Other Expenses

Prepaid Expense

a Current Asset, as it has been paid in advance in the Current Period but yet to be incurred.

Accrual Basis: recognises expenses when they are incurred not paid.

Then, once incurred they are recorded as an expense.

Accrued Expense

a Current Liability that arises when an expense has been incurred in the period but not paid.

Accrual Basis: recognises expenses when they are incurred not paid.

When paid they are paid alongside the current expense, recording GST for both.

Accrued Revenue

A Current Asset that arises when revenue has been earned, but cash not received.

Interest Revenue

Once paid, they are then paid with the other expense for this period.

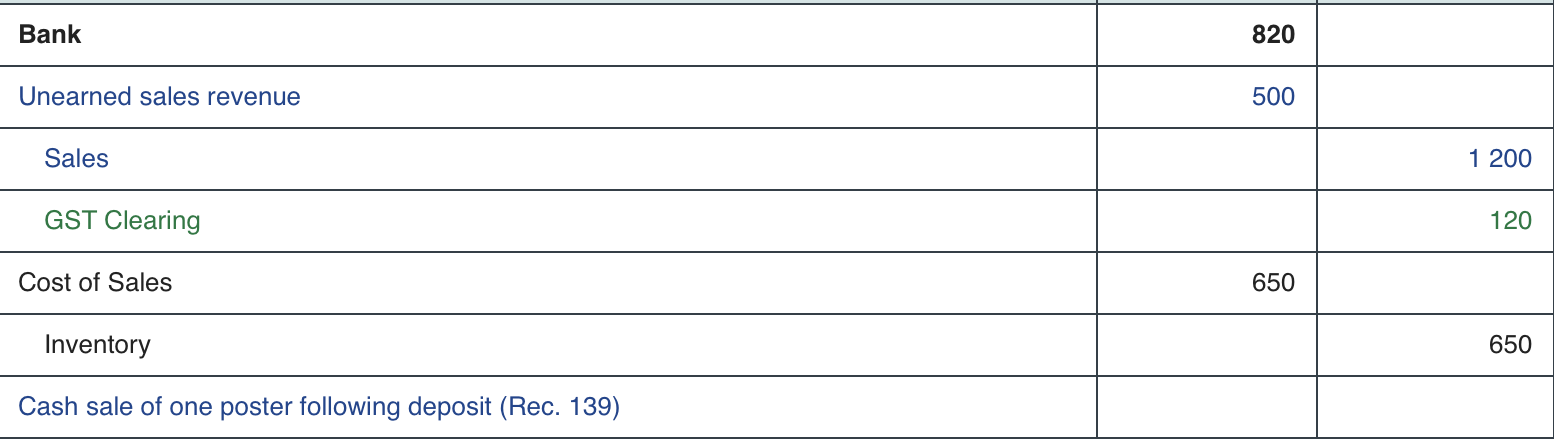

Unearned Sales Revenue

a Current Liability, arising when cash is received in advance for the revenue that is yet to be earned.

Total cost is $1320, but they already payed 500 in deposit so 1,320-500 =820 is still Owed. Thus because we transfer the economic resource the Liability is debited.

When a deposit is involved, GST isn’t recored until the sale!