Economic and Monetary Union - Economic Governance

University of Answers: Faculty of Social Sciences - European Integration

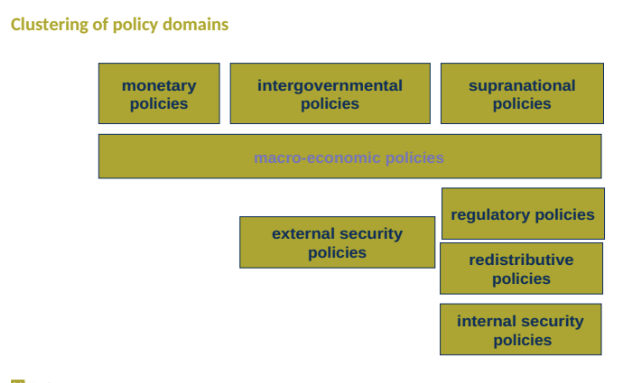

Clustering of Policy Domains

Types of Policies:

Intergovernmental Policies

Supranational Policies

Macro-Economic Policies

External Security Policies

Internal Security Policies

Redistributive Policies

Regulatory Policies

Monetary Policies

Policy Domains: Definitions

Regulatory Policies:

Description: Rules regarding the single market and related areas like competition, social, and environmental policies (including external dimensions).

Redistributive Policies:

Description: Allocation of resources from the EU budget to various social groups or regions, primarily through agriculture and cohesion subsidies.

Internal Security Policies:

Description: Policies aimed at safeguarding the economic, social, and political rights of EU citizens regarding asylum, migration, police, and judicial cooperation.

External Security Policies:

Description: Policies where the EU acts as a single entity toward the international landscape, managing trade, development, external security, and defense.

Reasons for the Introduction of EMU

Economic Reasons:

Optimize the single market.

Ensure fair play by preventing competitive devaluations.

Reduce exchange rate risks within a single market.

Lower transaction costs.

Enhance price transparency.

Political Reasons:

Promote further integration of EU member states.

Transform German monetary leadership into a pooled joint leadership, in line with French preferences.

Full incorporation of Germany into the European project.

Considered one of the ultimate steps towards integration.

Early Attempts at EMU

Plan Werner (1970):

Objective: Achieve EMU by 1980 in reaction to monetary instability post-Bretton Woods.

Outcome: Failed.

European Monetary System (1979):

Goal: Keep exchange rate fluctuations within strict limits (Exchange Rate Mechanism - ERM).

Single European Act (1987):

Initiated the single market and indicated the long-term establishment of EMU.

The Delors Report (1989)

Objective: Set conditions for creating a European Economic Union.

Three out of four preconditions identified:

Single market

Cohesion policy

Competition policy

Condition Still Pending: Macro-economic coordination.

Additional measures proposed:

Free movement of capital necessitates cooperation among member state central banks regarding monetary and macro-economic policies.

Introduction of a European System of Central Banks for coordination and reduced exchange rate margins within the ERM.

Eventually, the irreversible fixing of member states' currencies and the transfer of monetary policies to an overarching European level (European Central Bank).

Note: A new Treaty was required for these measures.

The 1990-1991 Intergovernmental Conference (IGC)

Core Discussion Points:

National Sovereignty Concerns:

France viewed EMU as regaining pooled monetary sovereignty (opposing Deutsche Mark dominance).

UK considered EMU an ultimate loss of national sovereignty.

Germany saw loss of the Deutsche Mark as a trade-off for reunification.

Other Questions Raised:

Is the EU an optimal currency area (considering economic heterogeneity, labor mobility, tax competition)?

Is EMU primarily an economic or political project?

Does EMU encompass both economic and monetary union, or strictly monetary union?

Can monetary union endure without economic and political union, including shared fiscal and budgetary policies?

The Treaty of Maastricht

Significance: Explicitly stated the ambition of a single currency as the pinnacle of economic integration.

Maastricht Criteria: Member states must meet these requirements:

Price Stability: Inflation must not exceed 1.5% above the average of the three best-performing member states.

Budgetary Discipline: Budget deficit should not exceed 3% of GDP, and public debt must not exceed 60% of GDP.

Exchange Rate Stability: National currency’s exchange rate must remain within ERM margins for two years without devaluation.

Interest Rate Stability: Long-term interest rates cannot exceed 2% above the average of the three best-performing member states.

Stage 3 of EMU: Scheduled for commencement on January 1, 1997, or by January 1, 1999 at the latest—entailing the fixation of exchange rates and establishment of the European Central Bank (ECB).

The Post-Maastricht Crisis

Challenges:

Ratification difficulties in Denmark (1992) related to EMU.

ERM crisis (1992/93):

Speculative attacks against several currencies

Notable events:

Devaluation of the Italian Lira

Withdrawal of the Lira and British Pound from the ERM system

Devaluation of the Spanish Peseta and Portuguese Escudo

Loosening of ERM margins from 2.5% to 15%.

ERM crisis led to an unlikely participation of Italy and the UK in stage 3.

Public skepticism increased; however, political backing was maintained.

Economic crises impeded the initial 1997 deadline; consequently, the European Council of Madrid (1995) postponed stage 3 to January 1, 1999.

Preparations for EMU Stage 3

European Council of Madrid (1995):

Selected the name "Euro" for the future single currency.

Stability and Growth Pact (1996): Implemented permanent budgetary discipline (3% budget deficit) post-EMU introduction, including penalties for non-compliance (excessive debt procedure).

Broad Economic Policy Guidelines: Focused on coordination of national reform plans, which would be the initial steps toward economic governance coordination.

Discussion on the political oversight over the ECB was initiated, leading to the establishment of the "Euro-X" Council composed of finance ministers from EMU countries to monitor the ECB.

1999 Deadline Feasibility: Achieved through German and French commitments, economic recovery, relaxation of criteria, and absence of public resistance against EMU.

EMU Stage 3 Commencement

Convergence Reports: Provided by the European Commission and European Monetary Institute (EMI).

European Council of Brussels (1998): DETERMINED: 11 out of 15 member states qualified for EMU effective January 1, 1999:

Exclusions:

Greece (criteria not met; joined January 2001)

UK, Denmark, Sweden (opt-outs).

ECB Leadership: Wim Duisenberg (Netherlands) appointed president, later succeeded by Jean-Claude Trichet (France) mid-term, followed by Mario Draghi (2011-2019) and Christine Lagarde (current).

Significance of Dates:

January 1st, 1999: Beginning of EMU.

January 1st, 2002: Launch of euro coins and notes.

EMU Membership Since 1999

Euro-Referendums:

2001: Denmark voted against joining EMU.

2003: Sweden voted against joining EMU.

Subsequent Accessions to Eurozone:

Greece (2001), Slovenia (2007), Cyprus and Malta (2008), Slovakia (2009), Estonia (2011), Latvia (2014), Lithuania (2015), Croatia (2023).

Total: 20 EU member states have adopted the euro by this point.

Institutions of EMU

European System of Central Banks (ESCB):

Comprises the European Central Bank alongside 27 national banks.

Eurosystem:

Comprises the European Central Bank and the 20 national banks of member states that have adopted the euro.

ECB Governance Structure:

General Council: Comprising all 27 national bank governors and the ECB executive board (intergovernmental).

Governing Council: Comprising the 20 governors and executive board (intergovernmental).

Executive Board: Composed of the President, Vice-President, and 4 members (supranational).

Eurogroup: Subset of the ECOFIN Council focusing on economic coordination within the Eurozone on an intergovernmental basis.

EMU Monetary Policy Goals

Main Policy Objectives of Eurosystem / ECB:

Price Stability: Aim to maintain inflation around 2%.

Instruments: Adjusting basic interest rates as primary tools for managing inflation.

Historical Policy Approaches:

Pre-2008: Cautious interest rates balancing growth support and inflation control.

2008-2022: Implemented very low or negative interest rates and cheap lending to commercial banks to mitigate banking and sovereign debt crises.

2022-2023: Rapid interest rate hikes to combat rising inflation; signs of stabilization towards 2% in 2024.

Inflation Rate Data (HICP): Significant fluctuations over the years with various peaks and troughs.

Interest Rate and Monetary Policy Adjustments: Documented changes in deposit facility rates, refinancing operations, and marginal lending facility rates from 2015-2025 to illustrate the ECB's monetary policy evolution.

ECB Support for Economic Policies

Monetary Policy Support:

Lending to national banks and private banks; funding private firms purchasing sovereign debt bonds.

Exchange Rate Policies:

Initial reference: 1:1 with the US dollar since 1999; growth trajectory shifted with the euro becoming stronger, peaking at 1.58 in April 2008, current (October 2025) rate at approximately 1.16.

Key Issues in Economic and Fiscal Policies of EMU

Survival Conditions of Monetary Union:

Involves examination of economic divergence, weak economic/fiscal integration, and political integration.

Questioning if EMU constitutes an optimal currency area as per theories by Krugman, Sims, De Grauwe:

Examination of the economic convergence, labor mobility, and capacity for fiscal transfers.

Risks of Limited Integration:

Inherent risks of a single ECB interest rate that may not fit all eurozone members.

Inability to adjust individual interest rates or utilize individual exchange rates for competitive advantage leads to reliance on internal devaluation (lower wages).

Recognition of the need for complementarity between monetary union and economic/fiscal federalism, prompting steps towards economic governance and policy coordination.

Banking Crisis to Sovereign Debt Crisis

2008 Banking Crisis:

Triggering factors include over-leveraging by banks in Ireland and Spain supporting housing markets leading to a collapse.

Resultant implications included public debt arising from state intervention to bail out banks and ensuing loss of confidence in banks and states.

Subsequent contraction of lending and adoption of austerity measures to reduce sovereign debt intensified issues.

Tackling the Banking Crisis

EU Response:

Recovery Plan (2008) called for coordination and member-state level implementation.

Legislation enacted from 2010-2014 aimed at stricter regulations of banks, insurance firms, and financial markets (European Systemic Risk Board consequences).

Establishment of bailout funds in 2012 and agreement on a Banking Union encompassing three elements: supervision, resolution, and common rules.

Background of the Sovereign Debt Crisis

Context from Lisbon Treaty:

Monetary policy transitioned to the ECB while economic and fiscal matters mostly remain with member states, with some intergovernmental coordination through the ECOFIN Council.

Main coordination instruments include non-binding Broad Economic Policy Guidelines (BEPGs) and the Stability and Growth Pact (SGP).

Issue exacerbation occurred due to a prior loose interpretation of SGP without penalties despite rising debts and low growth providing less tax income.

Timeline of the Sovereign Debt Crisis

Key Events:

January-April 2010: Greek sovereign debt issues prompted speculation against the euro, leading to €30 billion emergency aid for Greece.

May 2010: Establishment of a rescue package incorporating loans guaranteed by member states and the IMF while failing to alleviate market uncertainties.

October 2010: Adoption of the European Semester intended to monitor member states’ economic reforms and budgets.

Stability Mechanisms to Aid Member States

2010 Onwards:

Creation of the European Financial Stability Facility (EFSF) for bilateral lending among member states.

Temporary European Financial Stabilisation Mechanism (EFSM) established in 2011, later replaced by the permanent European Stability Mechanism (ESM) in 2012 with a budget of €700 billion to help recapitalize members by purchasing their national bonds under strict conditions.

Preventative Measures Post-Crisis

Legislative Framework Enhancements:

2011 Euro Plus Pact targeting smart, sustainable, and inclusive growth incorporated within the European Semester, yet too voluntary for markets.

2011 Six Pack establishing legislative supervision of economic and fiscal policies, enhancing the SGP with a clearer corrective action framework (Excessive Debt and Imbalance Procedures) with financial penalties.

2012 Treaty on Stability, Coordination, and Governance (TSCG/Fiscal Pact):

Introduced requirements for budgetary and debt goals among member states, ideally as constitutional obligations.

Supplemented by the Two-Pack aimed at closer surveillance of Eurozone members' finances, emphasizing a stringent framework under the European Semester for corrective measures.

From Crisis to Recovery

Enduring Monetary Policy:

Continued low interest rates from the ECB (2013) catalyzed economic recovery across affected regions.

Implementation of quantitative easing commenced in 2015 alongside negotiations regarding Greece’s compliance with EU fiscal programs, concluding with Greece’s eventual return to self-lending in global markets by 2019.

Recent Evolutions in Economic Governance

Post-2018 Developments:

Enhanced emphasis on the European Semester with a focus on structural improvements for public finances.

Increasing debate on austerity versus investment (Keynes vs. Friedman) raised within the EU context.

-Notable institutional shifts: a more intergovernmental EU scenario with a prominent role for the ECB against declining involvement from the European Parliament and Commission, leading to a new economic governance framework following the sovereign debt crises.

Response to Covid-19 Crisis

Pandemic Measures by ECB:

Introduction of qualitative easing strategies termed the ‘ECB Bazooka’ and Pandemic Emergency Purchase Programme (PEPP) meant to stabilize economies by buying securities.

Divergent views on long-term strategies of national debt creation vs. common EU bonds sparked debates across member states, leading to the formation of the Next Generation EU framework integrating recovery and resilience facilities with investments projected at €672.5 billion for member states based on reforms and milestones.

Features included oversight from the Commission, Council approval of national plans, and monitoring processes integrated within the European Semester.

Current Economic Governance Initiatives

Member State Oversight:

The Commission conducts continuous economic assessment of member states through progress reports and compliance with the Stability and Growth Pact (SGP).

Preventative and corrective measures enacted to ensure adherence to economic and budgetary targets, fostering reforms to lower sovereign debt and encourage growth.

Fiscal Data Overview

Member State Balances (2024 Projections):

Detailed balance percentages from various EU member states, including budget deficits and fiscal notifications leading towards improved compliance and economic stability, emphasizing urgent reforms needed to sustain economic viability.

Indicators Post-Covid-19

2022 AMR Scoreboard Indicators: Current accounts, net international investment positions, real effective exchange rates, and house prices across member states reflect varying economic conditions across the Eurozone.

Economic Governance after Covid-19

Future Directions: Transition towards stronger integration and cohesive fiscal policies remain pivotal, with growing expectations for both member states and EU institutions to navigate emerging economic challenges together.

Reflection on EU Common Bonds

Call for Common Bonds: Emergent discussions surrounding the need for the EU to issue common bonds to address funding for security and defense, signifying evolving economic and policy strategies in response to ongoing challenges.

Quiz Questions Related to EMU Membership

Criteria not recognized as Copenhagen criterion for EMU membership?

Correct chronology of EMU membership—identifying accurate sequences from the given options to assess understanding of the EMU's timeline and adherence to Maastricht criteria.