Accounting 211 Terms

Unknown

Accounting 211

W1 Class 1

Word of the day: Haphazard

“Marked by lack of a plan or order”

Lacking any obvious principle of organization (Aimless, arbitrary, disorganized, helter skelter)

What is accounting?

Record keeping

Communicating (tells the story)

Financial statements tell stories

“Fundamental language of business”

Accounting is storytelling (really controlled, rigid form of communication)

Accounting is called the “language of business” because all organizations set up an accounting information system to communicate data to help people make better decisions.

External users:

Shareholders own part of the company

Lenders

Eternal auditors

Boards of directors

Regulations

Regulations

Vendors

Internal users:

Leadership

Purchasing managers

Human resource managers

Production managers

Research and development managers

Marketing managers

Why do people use accounting?

Managers - to figure out which stores/division to close because they are underperforming.

Investors - to figure out which company to invest in.

Competitors - to better understand company strategy and opportunities to take market share.

Banks - to decide whether to loan money to your business.

Unions - to help in upcoming contract negotiation.

Ethics are critical

When things go bad there's the Employee Retention Credit(ERC)

Trust: firm belief in the reliability, truth, ability, or strength of someone or something

Ethics: moral principles that govern a person's behavior of the conducting of an activity

Accounting-Putting the Pieces Together

Record-keeping

Communication the “story” of the company

Users of the “language of business” are internal and external to the company

Trust in the information requires strong ethics

Rules of accounting are called GAAP

Accounting applies to business entities

GAAP-Generally Accepted Accounting Principles*

Overseers of GAAP

Financial Accounting Standards Board (FASB)

Securities and Exchange Commission (SEC)

International accounting standard board (IASB) (different from those 2 above)

Basic characteristics:

Relevance

Reliable

Comparable

4 key Accounting Principles

Management Process Principle (Cost Principle)

Accounting information is based on actual cost

Actual cost is considered objective

Revenue Recognition Principle

Recognize revenue when goods and services are provided to customers

At an amount expected to be received from the customer

Revenue must be earned*

Expense Recognition Principle (Matching Principle)*

A company record its expenses incurred to generate the revenue reported

Rev - expenses = net income (needs to match)

Full Disclosure Principle

A company reports the details behind financial statements that would impact users decisions in the notes to the financial statements

Anything that the lender needs, financial statements needed

4 key Accounting Assumptions

Going Concern Assumption

The business is presumed to continue operation instead of being closed or sold

Molistery Unit Assumption

Transactions and events are expressed in monetary, or money, units

Time Period Assumption

The life of a company can be divided into time periods, such as months and years

Business Entity Assumption

A business is accounted for separately from other business entities, including its owner

4 Business Entity Types

Sole proprietorship

Partnership

Corporation

Limited liability company

Accounting equation*

Assets = liabilities + owners equity

Assets = liabilities + common stock + retained earnings

Assets = liabilities + common stock + net income(rev - expenses) - dividends *

Equity and Liabilities are how we get the money and Assets are how we use it

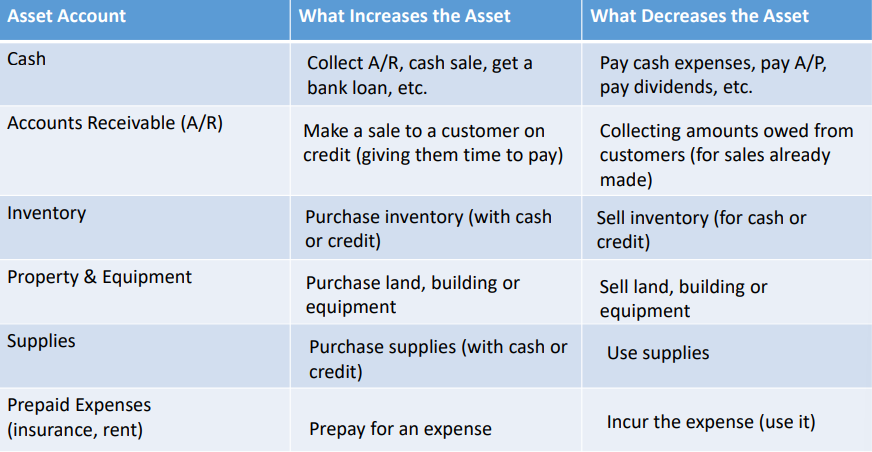

Assets

Assets are resources owned or controlled by the company

Cash - actual cash and bank accounts

Investments - stocks and bonds

Accounts Receivable - amounts due from customers

Inventory - items held for selling to customers

Prepaid Expenses - amounts paid in advance for items used by the business

Supplies - items used in the business

Properties & Equipment - land, building, chachines, computers and more

When you use up an asset, it is an expense

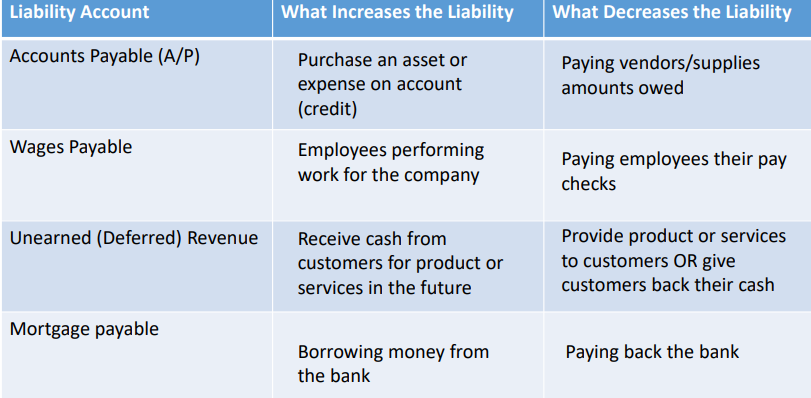

Liabilities

Liabilities are claims on assets that require repayment(not ownership)

Accounts Payable - amounts owed to suppliers and vendors (short term)

Wages Payable - amounts owed to employees

Taxes Payable - taxes owed to governments (sales, income)

Unearned (deferred) revenue - services or goods owed to customers

Notes Payable - loans (long term)

Mortgage - loans for buildings/land

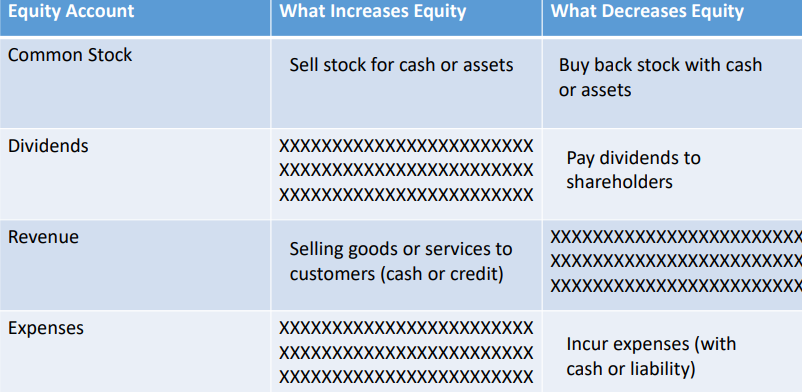

Equity

Equity residual claims on assets that do not require repayment(ownership)

Common Stock - investment in the company by owners

Retained Earnings - cumulative earning(net income) of the company not paid out as dividends to shareholders. Earnings that have been retained.

Service Revenue - amounts changed to customers for services provided

Sales Revenue - amounts changed to customers for products provided

Cost of Good Sold - cost of products sold to customers

Retained Earnings - dividends, revenues, expenses

Operating Expenses - cost of services and product used by the business

Wages and benefits paid, facility rents, utilities and maintenance, costs like supplies, insurance and marketing

Other Items - interest revenue, interest expense, gains, loses on sale of property

Dividend is not an expense*

Dividend is not an expense*

10 basic transactions

Investment by owner

Purchase supplies for cash

Purchase equipment for cash

Purchase supplies on credit

Provide services for cash

Payment of expenses in cash

Provide services for credit ‘

Receipt of cash from accounts receivable

Payment of accounts payable

Payment of cash dividend

W1 Class 2

Word of the day: Maelstrom - noun

“He was caught in a maelstrom of emotions after reading chapter one in his accounting text”

A maelstrom is a powerful, often violent whirlpool that sucks in objects within a given radius.

Maelstrom is also often used figuratively to refer to a situation resembling the turbulence of maelstrom.

Examples of assets:

cash

accounts receivable inventory

supplies

prepaid expenses

Investments

plant, property and equipment

Examples of liabilities:

accounts payable

wages payable

taxes payable

uneared (deferred) revenue

notes payable

mortgage payable

Examples of equity:*

common stock (investment in company),

retained earnings (rev = exp - div)

Transactions

A transaction generally includes an exchange or interaction.

Transactions always affect at least 2 items (not sides) from the acc equation.

Events of a company occur through transactions

Companies transact with:

Employees (payroll)

suppliers (venders)

Shareholders (owners)

Banks (lending)

Customers (revenue)

Other companies

When payments are on “credit” or on “account”

When the company buys something:

Supplier (vendor) has given out company time to pay them (typically 30 days)

Use the accounts payable (liabilities) account to track amounts owed to others

When the company sells something:

Company has given a customer time to pay us (typically 30 days)

Use the accounts receivable (asset) account to track amounts owed to us

Transaction practice:

Investment by owner increases an asset and increases equity

Purchase of supplies for cash increases an asset and decreases an asset

Purchase equipment for cash increases an asset and decreases an asset

Purchase supplies on credit increases an asset and increase a liability

Provide services for cash increase an asset and increase equity

Payment of expenses in cash decreases an asset and decreases equity

Provide services for credit increases an asset and increases equity

Payments of accounts payable decreases an asset and decreases a liability

Payment of cash dividend decreases an asset and decreases equity

Pay for next month’s rent early with cash increases an asset and decreases an asset

Receipt of cash from customers against accounts receivable increase an asset and decreases an asset

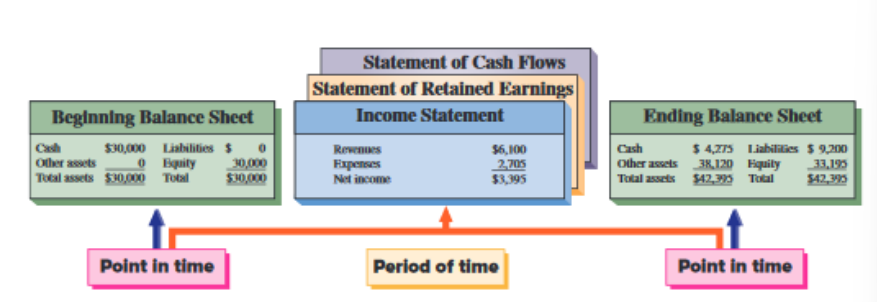

Financial statements - 4 Parts

Account records result in financial statements

Balance Sheet

Describes a company's financial position (types and amounts of assets, liabilities, equity) at a point of time (snap shot)

Income Statement

Describes a company's revenues and expenses and computes net income or loss over a period of time (movie)

Statement of Retained Earnings

Explains changes in retained earnings from net income or loss and from nay dividends over a period of time

Statement of Cash Flows

Identifies cash inflows (receipts) and cash outflows (payments) over a period of time

Asset accounts:

Liability accounts:

Equity accounts:

Classification of Cash Flows:*

The statement of cash flows includes the following 3:

Operating activities

From income statement plus notes (use + (inflows)-(outflows))

inverting activities

Cash paid for purchase of long-term assets (PPE)

financing activities

Cash component of transactions with owners (investments by them and payment of dividends to them)

What is the change in the bal of account

Current assets/current liabilities + net income is in the cash flow*

Statements of Cash Flow

1. Net increase or decrease in cash

2. Net cash from or used by operating activities

3. Net cash from or used by investing activities

4. Net cash from or used by financing activities

5. Add up the cash from all sources, and then prove it by adding it to the

beginning cash balance to get ending cash balance.

What is a ratio and why do we use them?

A ratio is a way of expressing the relationship between one accounting data point to another

A ratio must show an economically important relationship

Useful: Cost of good sold to sales

Not useful: Freight costs to patients

Under conditions trends difficult to detect by looking at individual accounts

Types of rations:

Liquidity and Efficiency

Availability of resources to pay short-term cash requirements

How productive a company is in using its assets

Solvency

Ability to meet long-term obligations and generate future revenues

Profitability

Ability to earn an adequate return

Market Prospects

Analyzing corporations with publicly traded stock

Return on Assets (ROA)

Return on assets equation measures the assets that are making you earn things.

Stated in ratio form as a net income divided by the average total assets invested

ROA = Net Income/Average Total Assets

4 Steps (sort of) to Record Transactions:

Step 1 - identify the transaction and any source documents

Step 2 - analyze the transaction sing the accounting equation

Step 3 - record the transaction in journal entry from applying double-entry accounting

Step 4 - post the entry (for simplicity, we use T-accounts to represent ledger accounts)

Very quickly you should be comfortable enough going directly to step 3 and/or 4

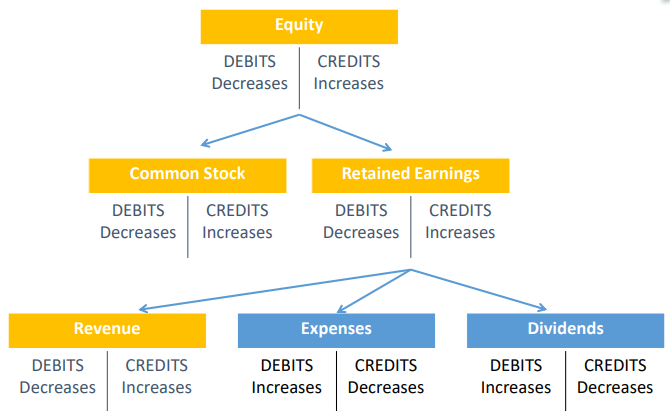

T-accounts and debits and credits:*

T-accounts are a representation of increases and decrease in individual accounts

Debit (DR) is on the left

Credit (CR) is on the right

Double-entry accounting*

Accounting equation

Assets = Liabilities + Equity

Debits = Credits

Double entry accounting also requires for each translation:

Total Debits = Total Credits

Exs:

Purchase equipment on account = debit (increase) asset and credit (increase) liability

Issue common stock for cash = debit (increase) asset and credit (increase) equity

Debits and credits for equity:*

W2 Class 1

Accounts

An account is a consolidated record of increases in a specific asset, liability, equity, revenue or expense item.

Asset Accounts

Cash, accounts receivable (A/R), inventory, prepaid expenses, supplies, equipment, building, land

Liability Accounts

Accounts payable, note payable, uneared (deferred) revenue, mortgage payable, wages payable

Equity Accounts

Common stock (or contributed capital), retained earnings, dividends

Revenue ( sales to customers)

Expenses (cost of good sold, advertising, rent, salaries, utilities, insurance)

Transactions

Always affect at least 2 items from the accounting equation

Financial statement has 4 parts

Ratio - return on assets

Classification of Cash Flows

Operation activities - What is being measured here?

Day to day activities: Net income + non-cash + (Current assets minus current liabilities)

Are you generating cash from the everyday activities

Investing activities - What is being measured here?

Long term investing in assets

Investing for revenue in the future

Financing activities - What is being measured here?

Where are they getting the finance

Debt and equity

Transactions

Transactions represent exchange of assets, goods or services between parties

Transactions are recorded in the accounting books, which are a set of journals and ledgers and can be paper (but today are almost always electronic)

Source documents - paper or electronic form

Invoices, purchases orders, checks, receipts bank statements

Typically define when a transaction has taken place

Debit and Credit Balances Normal Balance Increases*

Accounts with Debit Bal:

Assets

Expenses

Dividends

Accounts with Credit Bal:

Liabilities

Stock/investment

Revenue

Normal Balances

Each account has an expected debit or credit balance, called the normal balance

That normal balance is usually whatever increases the account

For assets, we expect a debit balance

For liabilities, we expect a credit balance

For equity, we expect a credit balance

Journals and Ledgers*

Journals provide the detail to each transaction or accounting entry

A journal is a listing of journal entries: This everything

A ledger is the collection of all the accounts: this is specific accounts

We use t-accounts to represent ledgers

Posting reference column often called PR, is a column in the general journal that is used to indicate when entries have been posted to the ledger accounts

Trial balance lists all ledger accounts and their balances at a point in time.

If the books are in balance, the total debits will equal the total credits

Journal entries are t-accounts are 2 ways to represent transactions Posting from the journal to the ledger isn't that tangible of a step

W2 class 2

Preparation Order of Statements:

Income statement records activity over a period of time

Retained earnings as the income flows to retained earnings

Balance sheet records the business at a moment in time

Cash flow statement analyzes where the cash was used

Types of Rations:

Liquidity and efficiency

Availability of resources to pay short-term cash requirements

How productive a company is in using its assets

Solvency

Ability to meet long-term obligations and generate future revenue

Profitability

Ability to earn an adequate return

Debt Ratio Equation:

Evaluates the level of debt risk.

Debt ratio = total liabilities/total assets

Financial leverage = debt ratio

A higher ratio indicates that there is a greater probability that a company will not be able to pay its debt in the future

The Accounting Period *

What time period are you working with, monthly, yearly, quarterly?

Cash and Accrual Accounting

Accrual Accounting*

Adjustments to financial statements to “properly” state balance sheet elements, and to match operating activities to period during which they occurred

More accurately reflects economic profit (net income)

Improves compatibility, across time and across firms

Accrual basis = total

Cash Accounting (cash accounting is for another school term)

The inflows and outflows of cash reflects revenue and expenses

No Accounts Receivable or Accounts Payable

No adjustments are made for assets purchased and used up

W3 Class 1

Key Accrual Principles:

Revenue recognition principle:

Recorded when the company has provided the goods or services to the customer (has the company “earned” it?)

At the amount the company expects to receive from customers

Matching principles (expense recognition):

Expenses are recorded in the same period as the revenues are recorded as a result of those expenses

We generally record expenses in the period in which the cost was used, consumed, incurred

Adjusting Entry Steps*

Analyze transactions and accounts for adjustments

Determine if an adjustment is needed (what should the balance be)

Make adjusting journal entry (amount necessary to get the account to the right balance

Adjust the ledger account

Make an adjusted trial balance

4 types of adjustments

Deferrals (cash paid” early”)

When we record the amount on the income statement. Cash is being paid, but the revenue or expense is deferred.

Prepaid expense

Unearned revenue

Accruals (cash paid “late” )

Menas “to come into existence as a legally enforceable claim”. Expenses and revenue need to be recorded but have not received the cash.

Accrued expense

Accrued revenue

Deferred Revenue:

When cash is received in advance of providing products or services.

It's in the liability account since it creates an obligation.

Deposit

Retainer

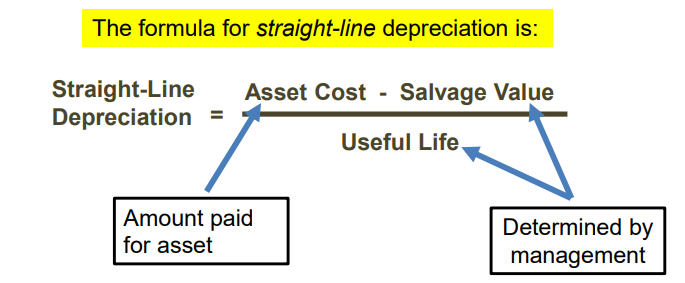

Use of Plant & Equipment: Depreciation

“the allocation of cost for long-lived assets over the expected useful life”

Long-lived assets (anything with expected useful life over a year)

Building

MRI scanner in a hospital

Computer systems

Allocation: spread the expense over a long period of time to match expenses to revenues

Depreciation *

Instead of expending the cost of a plant asset (equipment, building, cars, and more) in the year it is purchased we allocate, or spread out, the cost over their expected useful lives.

Contra Accounts

An account linked to another account that records adjustments or decreases to the account separately

Has an opposite normal balance and is reported as a subtraction from the other accounts balance

Contra accounts will show up again in later chapters

Straight-line Depreciation

Net cost (amount to depreciate)

Original cost - salvage value = net cost (this is what we depreciate)

Adjusting for Depreciation*

Non-cash expense

Accumulated Depreciation Contra Asset Account*

Is linked to the asset that is being depreciated. It will lower the book value of the asset. It's fixed in place, permanent. Contra means the opposite.

Depreciation Expense - Adjusting Entry

An adjusting journal entry is needed at the end of each period to reflect the use of buildings and equipment and equipment for the period.

Total is the “Net Book Value”

Term used at the individual asset level category asset level or for all fixed assets

Incurred = Expense

Accrued = Unearned

Deferred = Prepaid

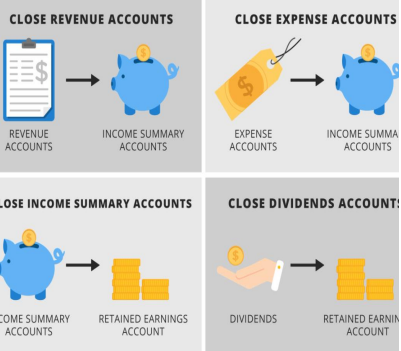

Closing Process*

It identifies accounts for closing, records and post closing entries, and prepares post-closing trial balance.

Resets revenue, expenses , and dividends (temporary) accounts balances to zero at the end of the period

Helps summarize a periods revenues in the income summary account

Balance sheet accounts: are permanent.

They retain their balances from one period to the next

Revenue, expenses, gains, and loss accounts: are temporary.

Their balances accumulate but start with a zero balance at the beginning of the next period (fiscal year)

Closing Temporary Accounts

At the end of the period, revenue, expenses, and dividends are in separate accounts. Closing entries just moves those to retained earnings.

First close each revenue and expense account balance to zero

Then offsetting account is “income summary”

After that close “income summary” to retained earnings

Finally close “dividends” to retained earnings

Post-closing Trial Balance

List of permanent accounts and their balances after posting closing entries

Total debits and credits must be equal

Temporary accounts are closed to retained earrings

Income Statement Accounts - close out yearly

Since income statements cover a period of tie, we need to close these accounts at least annually.

We want to start each year with a fresh start = zero balance

Balance sheet carries over each account balance

Classified Balance Sheet

Assets: Current assets, long term investments, plant assets or property plant and equipment, and tangible assets

Current assets

Cash

Accounts receivable

Inventory

Supplies

Prepaids

Less than one year

Long-term assets

Property (land)

Buildings

Equipment

Notes receivable

More than one year

Liabilities

Current or short-term liabilities, and long-term liabilities

Current liabilities

Accounts payable

Wages payable

Taxes payable

Interest payable

Unearned revenue

Less than one year

Long-term liabilities

Notes payable

Mortgages

Long-term lease

More than one year

Equity

Contributed capital

Common stock

Retained earnings

Net income (+ -)

Dividends (-)

Profit Margin

Profit margin ratio measures the company's net income to net sales

Profit margin = net income/net sales

Current Ratio

Current ratio helps assess the companies ability to pay its debts in the near future

Current ratio is the ability to meet

Current ratio = current assets/current liabilities

Financial Statement Ratio Equations

Return on Assets = Net Income/Average Total Assets

Debt Ratio = total liabilities/total assets

Current Ratio = current assets/current liabilities

Profit Margin = net income/net sales

Benefits of a Worksheet

Reduces risk of errors

Links accounts and their adjustments

Helps in preparing financial statements

Shows the effects of proposed transactions

Use of a Worksheet

Enter unadjusted trial balance

Enter adjustments

Prepare adjusted trial balance

Sort adjusted trial balance accounts to financial statements

Total statement columns, compute income or loss, and balance column

W3 class 2

Framework for adjustments

Step 1 - determine hat the current account balance equals

Step 2 - determine what the current account balance should equal

Step 3 - record on AJE to get from step 1 to step 2

We wanna close account to start the timeline fresh

We wanna come back to 0

Depreciation

Instead of expending the cost of a plant asset (equipment, building, cars and more) in the year it is purchased we allocate, or spread out, the cost over their expected useful lives.

Midterm study 4/20

Chapter 1:

Permanent accounts are in the balance sheet

There are beginning and end balances in the balance sheet

Temporary accounts are in the income statement

Dividends in a debit account on a normal balance

Chapter 2:

Double entry accounting is debits = credits

T-accounts are post account ledgers that go to trial balance that go to the financial statements

Cash received before revenue recognition is unearned (deferred( revenue (liability)

Cash paid after expense recognition is accrued expenses, cash incurred during fiscal period, unpaid and unrecorded, payables, salaries, (liability)

Cash paid after revenue recognition accounts receivable, internet receivable

Cash re

When talking about interest rent charge percentage you have to divided by 12 months

Income summary is a temporary account ( have to make it 0 to close the account)