Analyzing Transaction to Start a - Business

the financial structure of a business

financial position

assets

liabilities

owner’s equity

financial performance

revenues

expenses

Assets

resource obtained from a past event

enterprise has control over it

future economic benefits will be received from it use

Liabilities

present obligation

arose from a past event

settlement is expected to be mad in the future in the form of an outflow of resources

equity

residual right or interest of the owner(s) over the entity’s net assets

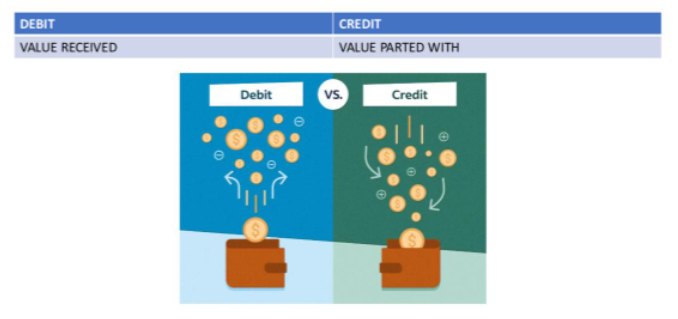

Double entry bookkeeping or venetian model

for every value received there is an equal value parted

Qualitative Attributes

fundamental attributes

relevance - the quality of the information should make difference to enable the statement user to make informed judgment

faithful representation - objective and free from errors or misstatements.

enhancing attributes

understandability - users have enough knowledge of finance, accounting and economics to be able to appreciate the financial reports.

verifiability - data given in the reports may be duplicated by independent measures or methods that will give the same results confirming

timeliness - reports be submitted promptly or within the time needed by the statement user to come up with a sound judgement that will enable him to make informative decisions.

compatibility - helps one identify changes taking place in the entity between two or more periods so users ill be able to determine the change or trend and its financial performance or position.

consistency - uniformity of accounting treatment from on period to another period or from one entity to another entity or else comparison is not valid

Generally Accepted Accounting Principles (GAAP)

rules which are universally used in identifying, measuring and reporting financial information that guide that conduct and practice of the profession

Going Concern Principle

it is expected that the business will continue to exist indefinitely (PAS 1 par. 25) that financial statement should be prepared on a going concern basis unless management intends to close the business or cease trading.

Business Entity Concept

assumes that the business enterprise is separate and distinct from its owner or investor

Exchange Price or Cost Principle

cost is the amount agreed upon is an arm’s length transaction

Measurement in Terms of Money

all business transaction are measured and recorded using one unit of measurement.

Accrual Assumption

cash accounting

record income when you receive it

record an expense when you pay it

accrual accounting

record income when you earn it

record an expense when you incur it

Objectivity

Assets acquired must be verifiable and substantiated by documents such as invoices, vouchers or official receipts.

Reporting

how often should the accountant prepare the financial statements especially since it is assumed that the business is a continuing concern?

Accounting Equation

Assets = equity

whereas

equities = liability + equity

thus

assets = liabilities + equity

debit = credit

/

rules of debit and credit

rules and debit and credit

rules of debit and credit CONT

notes

for every transaction, DEBITS = CREDITS

the objective of accounting is not simply to have a balanced equation but to have a correct analysis of the transactions