Money Growth and Inflation

Money Growth and Inflation

Introduction

Inflation is the increase in the overall level of prices in an economy.

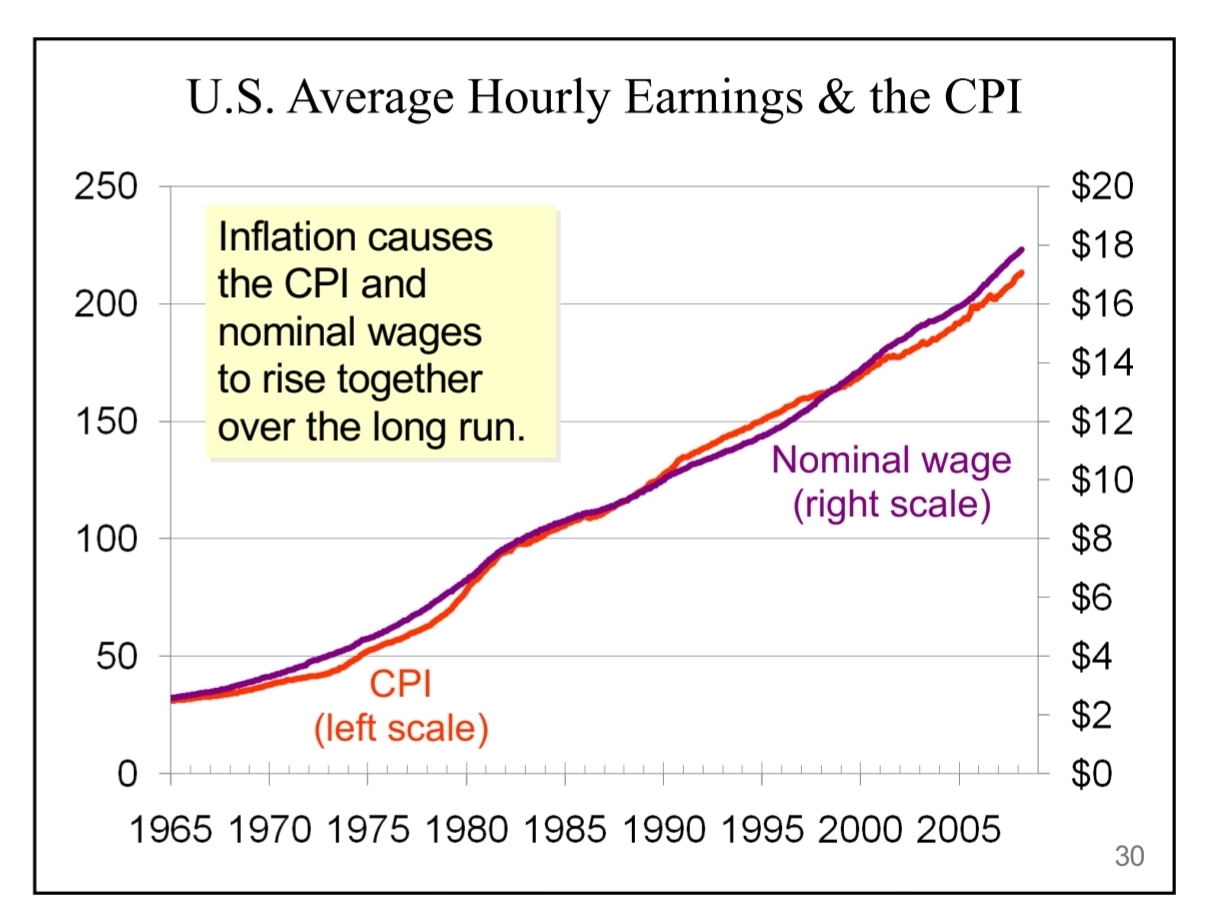

In the United States, over the past 80 years, prices have risen on average by 3.6% per year, leading to a seventeenfold increase in the price level.

Deflation is when most prices fall, which happened during long periods in the 19th century.

From 2005 to 2015, prices rose at an average rate of 1.2% per year, while in the 1970s, prices rose by 7.8% per year.

Hyperinflation - An extraordinarily high rate of inflation.

The Classical Theory of Inflation

The Level of Prices and the Value of Money

Inflation is more about the value of money than about the value of goods.

The economy’s overall price level can be viewed in two ways.

The price of a basket of goods and services.

A measure of the value of money.

If is the price level, then the quantity of goods and services that can be bought with $1 equals .

= price of a cone.

When the price of a cone is $2, then the value of a dollar is half a cone.

When the price rises to $3, the value of a dollar falls to a third of a cone.

Money Supply, Money Demand, and Monetary Equilibrium

The supply and demand for money determines the value of money.

Money supply is determined by the Federal Reserve (the Fed) and the banking system.

The Fed sells bonds = contracts the money supply.

The Fed buys government bonds = expands the money supply.

Money demand reflects how much wealth people want to hold in liquid form.

A higher price level (a lower value of money) increases the quantity of money demanded.

In the long run, money supply and money demand are brought into equilibrium by the overall level of prices.

If the price level is above the equilibrium Level, people will want to hold more money than the Fed has created, so the price level must fall to balance supply and demand.

If the price level is below the equilibrium level, people will want to hold less money than the Fed has created, and the price level must rise to balance supply and demand.

At the equilibrium price level, the quantity of money that people want to hold exactly balances the quantity of money supplied by the Fed.

Figure 1 illustrates these ideas.

The supply curve is vertical because the Fed has fixed the quantity of money available.

The demand curve for money slopes downward, indicating that when the value of money is low (and the price level is high), people demand a larger quantity of it to buy goods and services.

At the equilibrium point A, the quantity of money demanded balances the quantity of money supplied. This equilibrium of money supply and money demand determines the value of money and the price level.

The Effects of a Monetary Injection

The Fed doubles the supply of money by printing some dollar bills.

The monetary injection shifts the supply curve to the right, and the equilibrium moves from point A to point B. As a result, the value of money decreases and the equilibrium price level increases.

Quantity Theory of Money - According to the quantity theory, the quantity of money available in an economy determines the value of money, and growth in the quantity of money is the primary cause of inflation.

A Brief Look at the Adjustment Process

The immediate effect of a monetary injection is to create an excess supply of money.

People try to get rid of this excess supply of money in various ways.

They might use it to buy goods and services.

They might use this excess money to make loans to others by buying bonds or by depositing the money in a bank savings account.

The economy’s ability to supply goods and services, however, has not changed.

The greater demand for goods and services causes the prices of goods and services to increase.

The increase in the price level, in turn, increases the quantity of money demanded because people are using more dollars for every transaction.

Eventually, the economy reaches a new equilibrium at which the quantity of money demanded again equals the quantity of money supplied.

The Classical Dichotomy and Monetary Neutrality

Nominal variables - variables measured in monetary units.

Real variables - variables measured in physical units.

Classical dichotomy - the separation of real and nominal variables.

Relative prices are real variables.

According to classical analysis, nominal variables are influenced by developments in the economy’s monetary system, whereas money is largely irrelevant for explaining real variables.

Monetary neutrality - the irrelevance of monetary changes for real variables.

Velocity and the Quantity Equation

Velocity of Money - The rate at which money changes hands.

. V is the velocity of money, P is the price level (the GDP deflator), Y the quantity of output (real GDP), and M the quantity of money.

Quantity equation - . This equation states that the quantity of money (M) times the velocity of money (V) equals the price of output (P) times the amount of output (Y).

The quantity equation shows that an increase in the quantity of money in an economy must be reflected in one of the other three variables: The price level must rise, the quantity of output must rise, or the velocity of money must fall.

The velocity of money is relatively stable.

The Inflation Tax

Inflation tax - The revenue the government raises by creating money.

When the government prints money, the price level rises, and the dollars in your wallet become less valuable. Thus, the inflation tax is like a tax on everyone who holds money.

The Fisher Effect

Real interest rate = Nominal interest rate - Inflation rate.

Nominal interest rate = Real interest rate + Inflation rate.

Fisher effect - The one-for-one adjustment of the nominal interest rate to the inflation rate.

The Costs of Inflation

The Inflation Fallacy

Most people think inflation erodes real incomes

But inflation is a general increase in prices of the things people buy and the things they sell (their labour)

In the long run, real incomes are determined by real variables, not the inflation rate.

Cost of expected inflation

Shoeleather costs: The resources wasted when inflation encourages people to reduce their money holdings.

Includes the time and transactions cost of more frequent bank withdrawals

Menu Costs: The costs of changing prices.

Printing new menus, mailing new catalogs, etc

Relative-Price Variability and the Misallocation of Resources

When inflation distorts relative prices, consumer decisions are distorted, and markets are less able to allocate resources to their best use.

Inflation-Induced Tax Distortions

Inflation malus nominal income grow faster than real income

Taxes are based on nominal income, and some are not adjusted for inflation.

So inflation causes people to pay more taxes even when their real incomes don't decrease

Inflation tends to raise the tax burden on income earned from savings.

One example of how inflation discourages saving is the tax treatment of capital gains—the profits made by selling an asset for more than its purchase price.

Another example is the tax treatment of interest income.

One solution to this problem, other than eliminating inflation, is to index the tax system.

Confusion and Inconvenience

Inflation changes the yardstick we use to measure transactions. Complicates lang-range planning and the comparison of dollar amounts over time

Inflation makes investors less able to sort successful from unsuccessful firms, which in turn impedes financial markets in their role of allocating the economy’s saving to alternative types of investment.

A Special Cost of Unexpected Inflation: Arbitrary Redistributions of Wealth

Higher-than-expected inflation transfers purchasing power from creditors to debtors.

Lower-than-expected inflation transfers purchasing paver from debtors to creditors.

High inflation is more variable and less predictable than low inflation.

So these arbitrary redistributions are frequent when inflation is high.

Unexpected inflation redistributes wealth among the population in a way that has nothing to do with either merit, need or effort

Inflation Is Bad, but Deflation May Be Worse

All these costs are quite high for economies experiencing hyperinflation

For economies with low inflation (<10% per year), these costs are probably much smaller, though their exact size is open to debate.

The Friedman rule - Prescription for moderate deflation.

Just as a rising price level induces menu costs and relative-price variability, so does a falling price level.

Deflation often arises because of broader macroeconomic difficulties.

Conclusion

This chapter explains one of the Ten Principles of economics:

Prices rise when the government prints too much money

We saw that money is neutral in the long run, affecting only nominal variables.

The costs of inflation are more subtle.

Shoeleather costs

Menu costs

Increased variability of relative prices

Unintended changes in tax liabilities

Confusion and inconvenience

Arbitrary redistributions of wealth

In later chapters, we will see that money has important effects in the shart run on real variables like output and employment.