Micro 8,10,11

Chapter 8 - Perfect Competiton

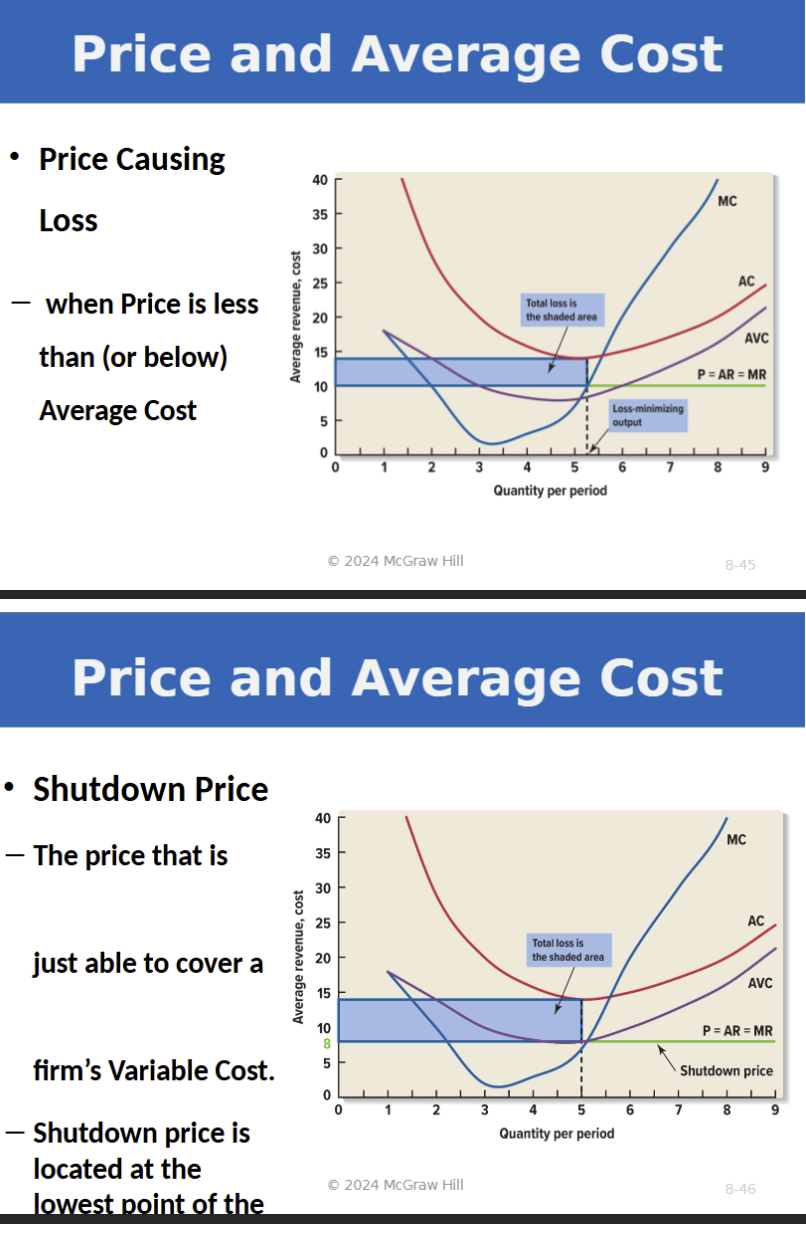

Order of curves on graph: MC, ATC, AVC, and then demand curves, which illustrate the relationship between price and quantity in the market.

Profitable Price: price greater then average cost. Sales - cost + Profit

As long as a company makes profit, competition will continue to join the market, causing the supply curve to shift right and decrease prices

Break-Even point of graph: MC=ATC, which indicates the level of production at which total revenue equals total costs, resulting in neither profit nor loss.

Shut down price: the minimum price at which a firm can continue to operate in the short run, covering variable costs. If the market price falls below this point, the firm should cease production until conditions improve. MC=AVC

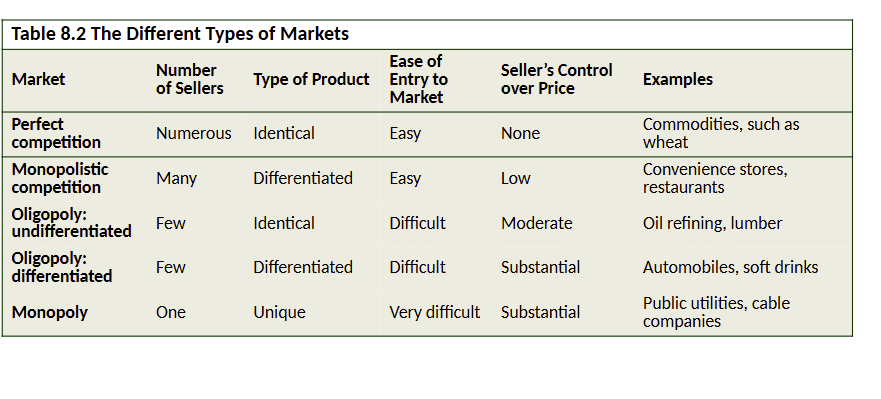

Perfect Completion: Price taker, product is homogenous, price is the min of ATC, consumer pays the least, resources used efficiently, long run producing is most effective

Market Equilibrium: Occurs where the quantity supplied equals the quantity demanded, ensuring that resources are allocated efficiently without surplus or shortage.

Long-Run Adjustments: In the long run, firms can enter or exit the market, leading to adjustments in supply until economic profits are zero, reinforcing the principle of perfect competition.

Industry: A group of producers, all producing a similar product

Market: Interaction of producer and consumers

Hair Salon: Monopolistic comp

Industrial chemicals in Canada - undifferentiated

oligopolyCommercial breweries in Canada - differentiated oligopoly

World market for coffee - perfect competition

Rogers Cable in Ontario - monopoly

Perfect Competition: A market in which all

buyers and sellers are price takers

– Conditions:

– Many small buyers and sellers

– No preferences shown (undifferentiated product)

– Easy entry and exit by both buyers and sellers

– The same market information available to allFor competitive firm, Price=AR=MR

Total Profit: TR-TC

Profit Maximization

MR>MC produce more

MR<MC produce less

MR=MC is maximizing total profit

Different cost curves can be used to illustrate how different decisions are made by the firm.

the AVC curve is used to decide whether to produce at all or shut down

the MC curve is used to decide the best output,

the AC curve is used to determine the level of profit or loss.

Would a firm willingly produce at a loss?

YES, if the losses from production are less than total fixed costs, the firm should continue to product

NO, if the losses from production are more than total fixed costs, the firm should not continue to produce

Firm primary goal: profit maximization

Shut down price is any amount less then…? average variable cost

jdjdjd

Chapter 10 - Monopoly

The one firm is the industry, price maker

Barriers to Enter: technical, legal. economic

Computer operating systems: technical barrier

Commercial aircraft manufacturing: economic barrier

West coast salon fishing: legal barrier

Demand is a downward-sloping curve, must decrease the price in order to sell more

Total revenue increases as more units are sold, then starts to decline

Average revenue is identical to the demand curve

When marginal revenue is positive (or negative), total revenue is rising (or falling)

Total revenue is a maximum when marginal revenue is zero

The top half of any demand curve is elastic, the bottom half

is inelastic. This monopolist would never produce an output greater than 11, i.e., where the demand is inelasticTotal Profits

Max is TR-TC at the greatest amount

Break-even: TR=TC

Total Profit Curve shows the relationship between total profit and output level, indicating how profit varies as production increases. Max was TR slope=slope of TC (MR=MC)

Marginal Cost (MC): The cost of producing one additional unit, which affects total profit as output changes

Total Revenue (TR): The income generated from sales, which is essential for calculating profit.

Profit Maximization: Occurs where MR (Marginal Revenue) equals MC, ensuring that any increase in production will not decrease total profit.

Marginal Revenue less then price in monopoly: Because the lower price of the extra unit of output also applies to all prior units of output, resulting in a decrease in total revenue for each additional unit sold compared to a perfectly competitive market.

To increase its sales, a monopolist must reduce the price on ______: the whole unit of its output

Why are monopolist price maker: control total quantity supplied and control the price

When marginal revenue is ___, total revenue is increasing: positive

What is maximized when MR is equal to zero? Total revenue

Profit maximized for monopolist: MC=MR

an example of price discrimination among units purchased? A coffee shop which offers a free coffee for every six purchased.

Price Discrimination: when producers charge different customers different prices for the same good or service?

Compared to a perfectly competitive firm, a monopolist finds it profitable to charge a ______ price and supply a ______ quantity. higher, lower

Diminishing marginal utility leads to what kind of price discrimination? Discrimination among units purchased.

Chapter 11 - Imperfect Competition

Product Differentiation allows firms to create a distinct market presence, enabling them to charge higher prices for their unique offerings compared to homogeneous products in a competitive market.

Some control over prices in imperfect comp

Imperfect is split into two kinds

Oligopoly: Many firms offer similar but differentiated products, leading to some degree of pricing power. 4 big brands with over 40% control of the market. Use large advertisement, non-price competition.

When new firms enter a oligopoly, demand shifts left and it become flatter. Leading to normal profits in the long run

Concentration ratio is higher then 40% its a oligopoly

Monopolistic: Many small firms (car repair shops, restaurants), small advertisement, niche markets

Concentration ratio less then 40% its monopolistic, characterized by a higher number of firms competing in the market with limited pricing power.

Concerns with Monopolistic Competition

Produces at a lower output compared to perfect competition, does not achieve productive efficiency, charges higher prices then perfect competition and does not achieve allocative efficiency

Productive efficiency: Long-run equilibrium price does not equal minimum average total cost

Allocative efficiency: Price exceeds marginal cost

Blocking market entry to increase profits: if entry is blocked positive economic profits can be maintained in the long run.

this can be done though licensing, franchising and professional associations

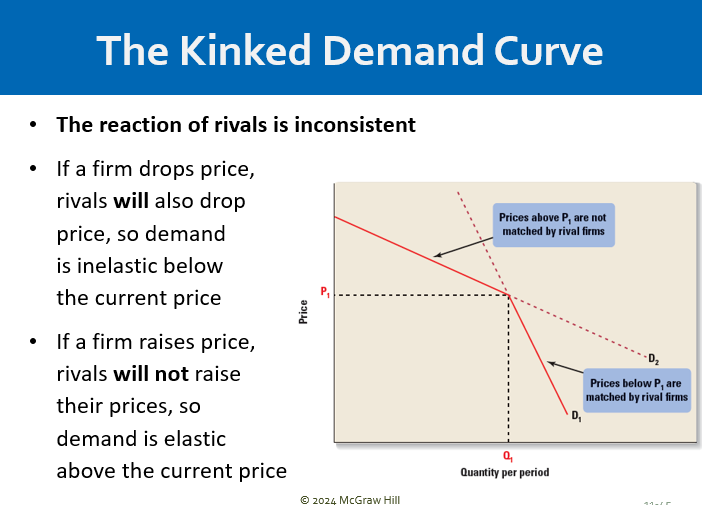

In a oligopoly mutual interdependence exists among firms, meaning that the actions of one firm directly affect the decisions of others, leading to strategic behavior in pricing and output.

Game Theory, Nash Equilibrium: a situation where each rival chooses the best actions given the anticipated actions of the others

Collusive Oligopoly: Cartel

A cartel is a group of sellers that collude by restricting output to drive up prices benefiting members as long as they do not cheat.

A classic example of a cartel is the Organization of the Petroleum Exporting Countries (OPEC). OPEC is a group of countries that collaborate to control the production and pricing of oil on the global market. By coordinating their outputs, they aim to influence oil prices and stabilize the market, benefiting the member countries as long as they adhere to the agreed production levels.

Non-Collusive Oligopoly: Price Leadership

Price leadership occurs when one leading firm sets the price for the industry, and other firms in the market follow suit. This strategy allows the price leader to maintain market stability while also maximizing profits for all firms involved. Unlike a cartel, price leadership does not require formal agreements or collusion, making it a more flexible approach to managing competition within an oligopoly.

Monopolist would never produce in when the marginal revenue in the negative

Rising Moon must be operating in a monopolistically competitive market and is in long-run equilibrium. (This is because at the profit maximizing output, the firm is just breaking even and unlike perfect competition the firm is facing a downward-sloping demand curve.)