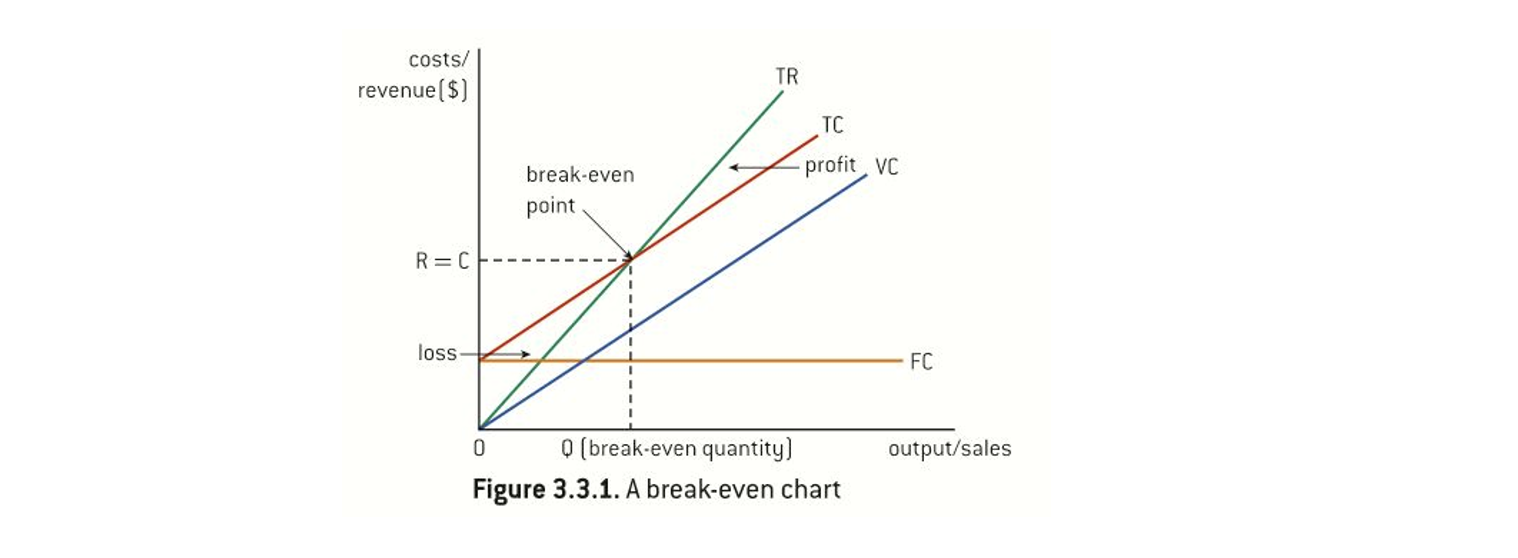

5.5 Break-Even Analysis

Break-Even:

When a business sells enough products to cover all its costs of production.

Break-Even analysis:

Break-Even analysis:

A visual tool that enables managers to interpret the relationship between fixed costs, variable costs, price, revenues, and profits.

Limitations: assumes that costs and revenues are static; Price and costs are assumed to be constant; not always easy to classify certain costs by only using FC and VC; not useful for multi-product businesses; the effectiveness depends on how reliable the data are; pricing strategies differ the prices in this analysis, ignored qualitative issues in decision-making.

Contribution per unit = P - AVC

The break-even quantity (Qbe) = FC/(P - AVC)

Total contribution = (P - AVC)*Q = TR - VC

Profit: When TR > TC, Loss: When TC > TR

Profit = TR - TC = Total contribution - FC

Target profit output (Qt)= (FC + Target profit)/(P - AVC)

Target price = Average FC + AVC = FC/Q + AVC

Margin of safety (MOS)= current output - Qbe