AP Microeconomics Unit 4

3.7 Perfect Competition in the Short Run

4.1 Introduction to Imperfectly Competitive Markets

4.2 Monopoly

4.3 Price Discrimination

4.4 Monopolistic Competition

4.5 Oligopoly and Game Theory

Some info/photos taken from Jacob Clifford and ReviewEcon on youtube. Check out their review videos :)

Types of Markets (3.7, 4.1, 4.2, 4.4, and partial 4.5)

Perfect Information - A market’s information about materials, production, blueprints, design, etc, is all known by all firms

Imperfect Information - A market’s information about materials, production, blueprints, design, etc, is not known by all firms

Barriers to Entry - Anything that may prevent a new firm from entering a market, like high fixed costs, patents, regulations, etc.

Allocative Efficiency - the best distribution of goods in an economy that meets the needs and wants of society.

Productive Efficiency - the point that maximizes output while minimies input resources

Perfect Competition -

A Market where there are many suppliers offering the same product. It is easy to enter and the products are often cheap. Ex: Agriculture

Many Firms (100+)

No barriers to entry

Perfect Information

Identical Products

No long-run profits

Price Takers (dont choose price, it’s determined by the market)

Perfectly Elastic Demand

Always Allocative Efficiency, Productive Efficient in the long-run.

Monopolistic Competition -

A market where companies pretend they are a monopoly and work to create a unique brand. They’re the “only place to get a real American burger,” but definitely not the only place to get a burger. Ex: Coffee Shops

Many Firms (10-100)

Low barriers to entry

Imperfect Information

Differentiated Products - lots of advertising

No long-run profits

Price Maker

Relatively inelastic Demand

Neither Allocative or Productive Efficient

Oligopoly -

A market is controlled by a few sellers. Ex: Insulin, Soft Drinks

Few firms (2-7)

High barriers to entry

Imperfect Information

Differentiated or standardized products

Long-run profits

Price Maker

Inelastic demand

Neither Allocative or Productive Efficient

Monopoly -

A market is dominated by one seller. All Ex: De Beers

One firm

High barriers to entry

Imperfect Information

Unique product - only one of its kind

Long-run profits

Price Maker

Inelastic demand

Neither Allocative or Productive Efficient

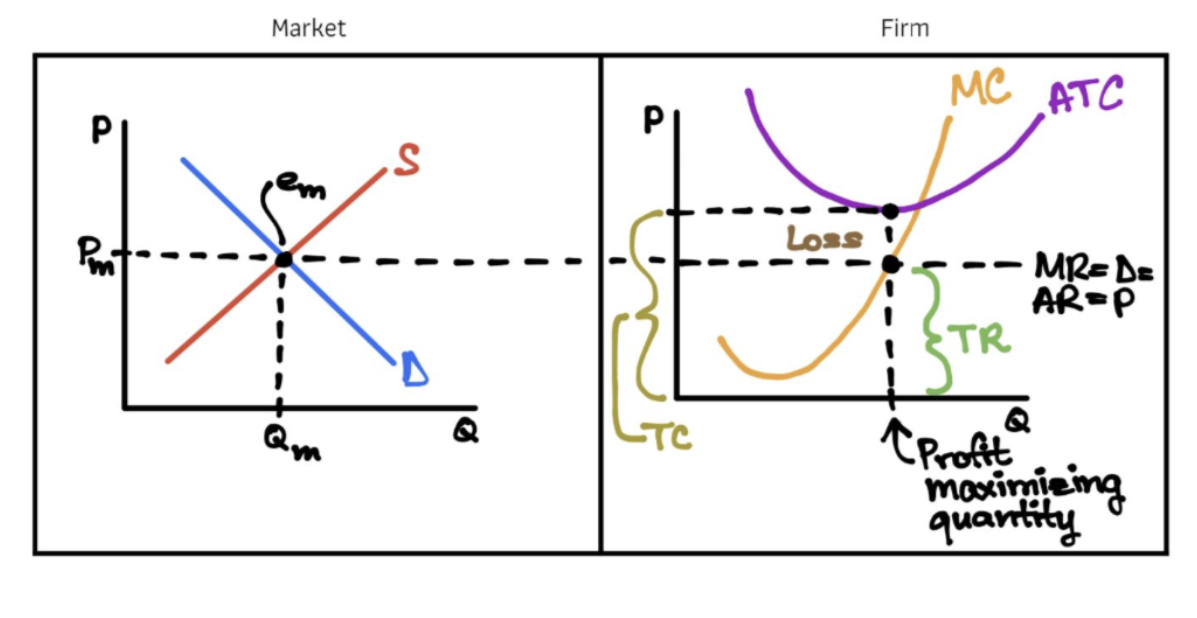

How to tell if firms are earning a profit

P - Price

ATC - Average total Cost

TC - Total Costs

TR = Total Revenue

MR - Marginal Revenue

MC - Marginal Cost

If P = ATC or TR = TC, zero (normal) profit

If P > ATC or TR > TC, SR Profit

P < ATC or TR < TC, SR Loss

The profit maximizing quantity is still MR=MC, always is.

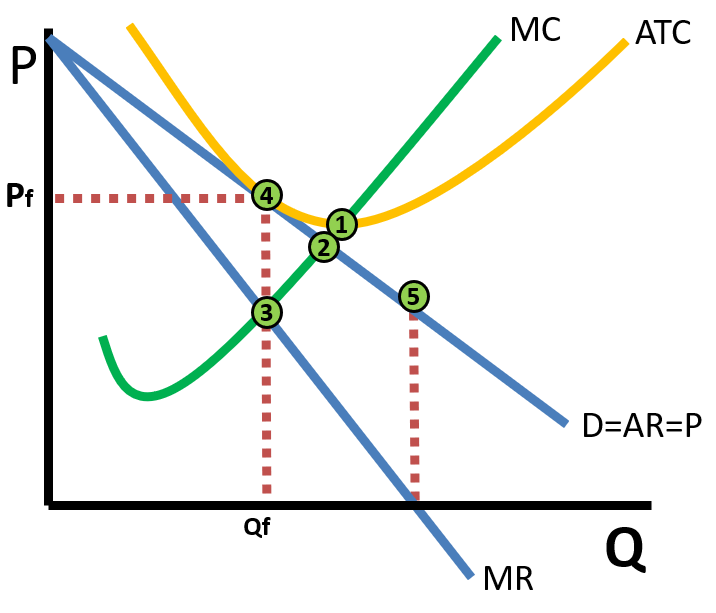

Socially optimal point - P=MC

Fair-return point - P=ATC

DARP Curves

Perfect competition uses the MR DARP curve, where MR=D=AR=P.

Imperfection competition, oligopolies, and monopolies use the DARP curve where D=AR=P, but not =MR.

MR DARP CURVE

Price is determined where s=d

MR DARP Curve for short-run profit. (MC < ATC where Market Price (Pm) intersects)

MR DARP curve for short-run loss (MC > ATC where Market Price (Pm) intersects)

In the LR then there is no profit for perfectly competitive firms: add graph

The DARP Curve - D=AR=P, not MC

How Price is determined on the DARP Graph

Find the price-maximizing quantity, where MR=MC

For price, use go up or down from the price-maximizing quantity to the DARP curve, that is the price

Short run-Profit for monopolies/oligopolies/perfect competition

6.4 - Regulating Monopolies

There are two main governmental solutions to monopoles

Public ownership: Where the government provides the service, such as the postal service. Unfortunately, these often run poorly and do not incentivize lower costs.

Price Ceilings: setting a maximum price for the good. This may require a lump-sum subsidy to cover losses, but not always since prices can be incredibly inflated in monopolies. Price ceilings can be set to where P=ATC with normal (no) profit, or to the socially optimal and allocatively efficient point, aka where MC = D or P.

There are allocative efficient price ceilings (P & D = MC) Or Fair Return Price (P is where ATC=DARP)

6.5 - Game Theory

Game theory - Explains how two or more players make decisions or choose options when their strategies affect participants. It can be shown by the payoff matrix.

This can be explained by the prisoner's dilemma. The prisoner's Dilemma: There are two prisoners and they are both offered a deal in separate rooms. If a prisoner snitches on their partner, they are let go free, and the other prisoner gets a 10-year sentence. However, if they both snitch, they both get a 6-year sentence. But, if neither of them snitch, they both get 1 year sentences. The best outcome is for neither of them to snitch, but they will be concerned their partner will snitch, so often both prisoners will snitch.

Prisoner B’s options:

Prisoner A will either confess and stay silent

If Prisoner A confesses, Prisoner B can either confess and 5 years or deny and get 10 years.

If Prisoner A stays silent, Prisoner B can either stay silent and get 1 years or confess and get off free.

Regardless of Prisoner A’s choice, the best thing— the dominant strategy— for Prisoner B is to confess. The same applies for Prisoner A.

While the best overall option is for them to both stay silent, they will be concerned about the other player’s choice, so they will likely protect themselves will the superior

This can be easily applied to oligopolies.

The best overall outcome is for neither companies to advertise, but they lose 55 million if the other advertises and they don't. They will only lose 20 million by both advertising. So, while the best option would be for neither company to advertise, since the dominant strategy or both companies will force them to advertise.