Capital Flows and Balance of Payments - Section 8, Module 41

economists keep track of domestic economy using the national income and product accounts

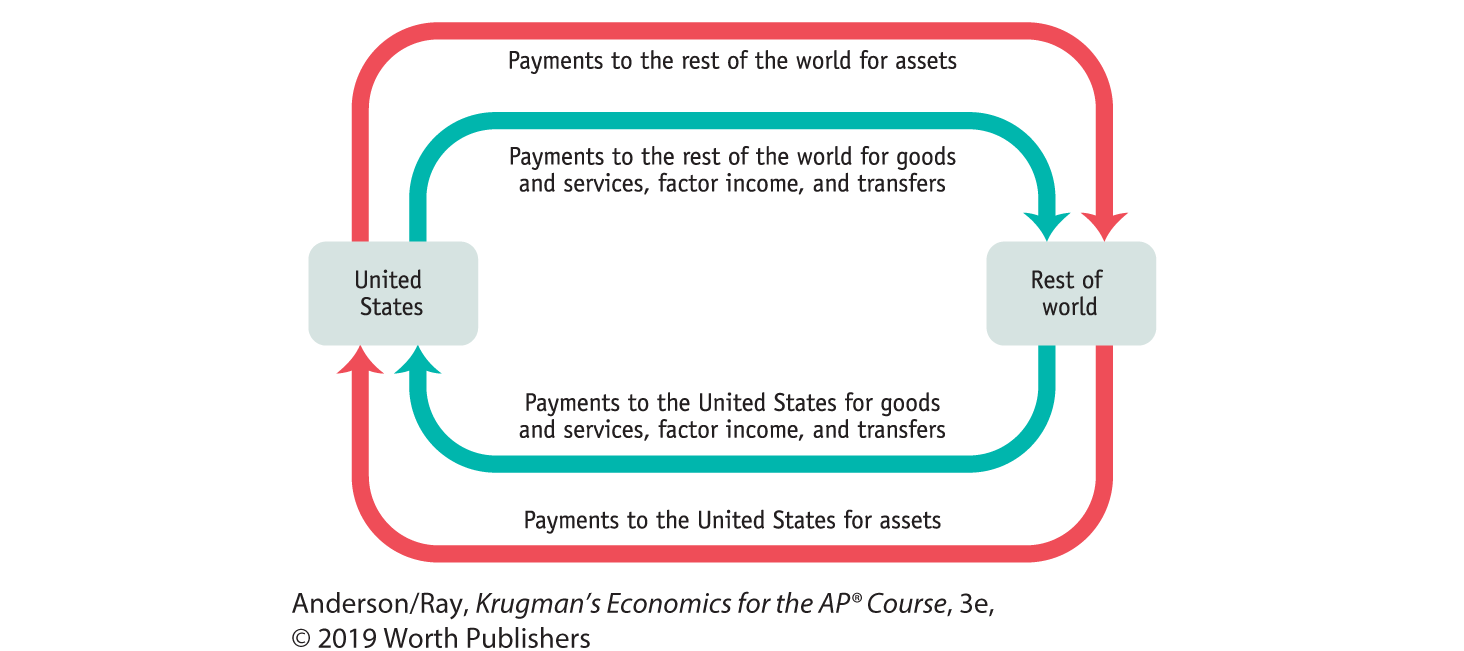

to keep track of international transactions - balanace of payment accoutns

balance of payment accoutns - summary of the country’s transactions with other countries

balance of payments on the current account/current account - BOP of g/s, factor income, and net international transfer payments

balance of payments on goods and services - most important part of current account, and is the difference between the value of exports and the value of imports

merchandise trade balance (trade balance) - difference between a country’s exports and imports, NOT INCLUDING SERVICES

factor income = payments for the use of factors of production owned by residents other countries

mainly investment income - interest paid on loans from oversees, profits of foreign corps in the US, etc.

but also, labor income - ex if an american is working abroad

international transfers - funds set by residents of one country to residents of another

mainly immigrant residents of one country sending money back home

balance of payments on the financial account (financial account) (called capital account in the past) - transactions that involve the sale/purchase of assets and create future liabilities

BOP includes currenta account and financial account

CA AND FA = ZERO ALWAYS

sources of case must equal uses of cash:

financial assets are exhcnaged for financial capital - funds from savings that are available for investment spending

FA = measure of capital inflows in the form of foreign savings that become available to finance domestic investment spenidng

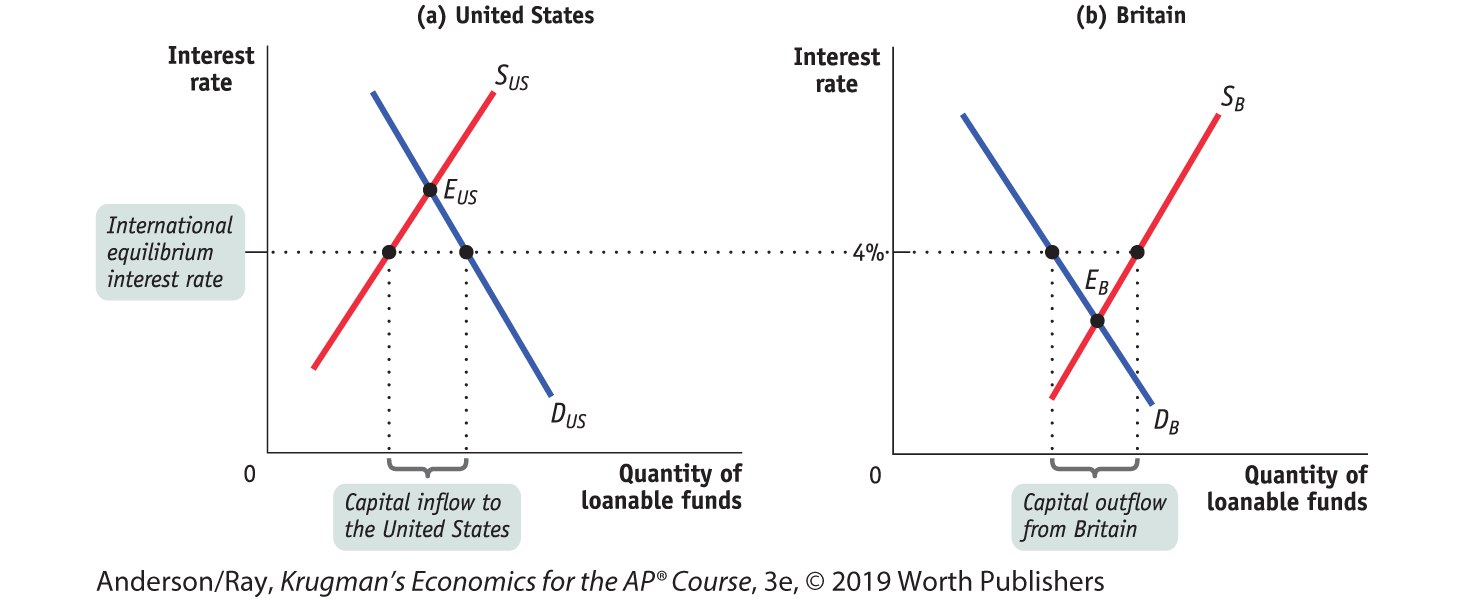

motivations fo rcapital flows that are causd by prviate decisions = can be found throug loanable funds

simplifications are made: internaltioncapital flows are simplified by the assumption that all flows are in the form of loans (but IRL, they take many forms [such as stocks, foreign real estate, foreign direct investment - companies build factories/get other productive assests abroad]); and the effects of expected changes in exchange rates are ignored

basically, country w the higher interest rate attracts investors to send some of their loanable funds to the foreign country - the capital inflow incr loanable funds supply in tht country = brings interest rate down

at the same time, quantity of loanable funds supplied to country a’s borrowers decr = incr in IR

narrows the gap unitl eliminated

example:

capital flows from countries w low IR to countries w high ir

international differences in demand for funds is bc some countries have more investment opportunities (are more rapidly growing) → they ahve a higher D for capital and offer higher returns to investors

internat differences in supply for funds is bc of the diff in savings → private or national

govt budget deficits (reduce overall national spending) can lead to capital inflows

loanable funds market shows the direction of NET capital flows

gross capital flows takes place in both dreictsion, bc IRL, there are other motives for capital flows other than a higher IR

investors want to diversify against risk by buying foreign/domestic stocks

business stratgey

some countries may be intl banking centers - ppl from all over the world put their money into tht country’s financial institutions, which then uses those funds to invets abroad

these lead to 2 way capital flows: economies are both debtors AND creditors