Chapter 2 Accounting for Business Transactions

C1: Describe an account and its use in recording transactions.

Business transactions and events are the starting points of financial statements. The process to go from transactions and events to financial statements includes the following.

Identify each transaction and event from source documents.

Analyze each transaction and event using the accounting equation.

Record relevant transactions and events in a journal.

Post journal information to ledger accounts.

Prepare and analyze the trial balance and financial statements.

“Account” Underlying Financial Statements

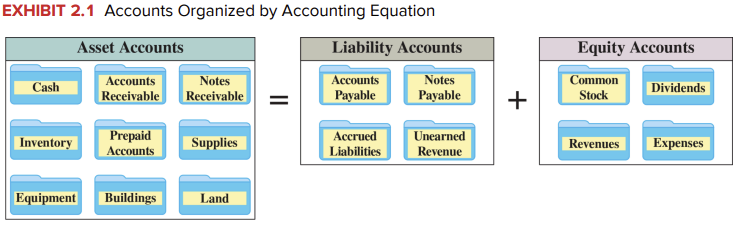

An account is a record of increases and decreases in a specific asset, liability, equity, revenue, or expense. The general ledger, or simply ledger, is a record of all accounts and their balances. The ledger is often in electronic form. While most companies’ ledgers have similar accounts, a company often uses one or more unique accounts to match its type of operations

Asset Accounts: Assets are resources owned or controlled by a company. Resources have expected future benefits. Most accounting systems include (at a minimum) separate accounts for the assets described here.

Cash: A Cash account shows a company’s cash balance. All increases and decreases in cash are recorded in the Cash

account. It includes money and any funds that a bank accepts for deposit (coins, checks, money orders, and

checking account balances).

Accounts Receivable: Accounts receivable are held by a seller and are promises of payment from customers to sellers. Accounts receivable are increased by credit sales or sales on credit (or on account). They are decreased by customer payments. We record all increases and decreases in receivables in the Accounts Receivable account. When there are multiple customers,

separate records are kept for each, titled Accounts Receivable—‘Customer Name’

Notes Receivable: A note receivable, or promissory note, is a written promise of another entity to pay a specific sum of money on a specified future date to the holder of the note; the holder has an asset recorded in a Notes Receivable account. It is different than accounts receivable because it comes from a formal contract called a promissory note. Notes receivable usually require interest, whereas accounts receivable do not.

Prepaid Accounts: Prepaid accounts (or prepaid expenses) are assets from prepayments of future expenses (expenses expected to be incurred in future accounting periods). When the expenses are later incurred, the amounts in prepaid accounts are transferred to expense accounts. Common examples of prepaid accounts are prepaid insurance, prepaid rent, and prepaid services. Prepaid accounts expire with the passage of time (such as with rent) or through use (such as with prepaid gift cards).

Supplies Accounts: Supplies are assets until they are used. When they are used up, their costs are reported as expenses. Unused supplies are recorded in a Supplies asset account. Supplies often are grouped by purpose—for example, office supplies and store supplies.

Equipment Accounts: Equipment is an asset. Its cost is allocated over time to expense, called depreciation. Equipment often is grouped by its purpose—for example, oce equipment and store equipment.

Buildings Accounts: Buildings such as stores, oces, warehouses, and factories are assets. Cost of buildings is allocated over time to

expense, called depreciation. When several buildings are owned, separate accounts are sometimes kept for each of

them.

Land: The cost of land is recorded in a Land account. The cost of buildings located on the land is separately recorded in

building accounts

Liability Accounts: Liabilities are obligations to transfer assets or provide products or services to others. They are claims by creditors against assets. Creditors are individuals and organizations that have rights to receive payments from a company. Debtors are those who owe money. Common liability accounts are described here.

Accounts Payable: Accounts payable are promises to pay later. Payables can come from purchases on credit or on account of merchandise for resale, supplies, equipment, and services. We record all increases and decreases in payables in the Accounts Payable account. When there are multiple suppliers, separate records are kept for each, titled Accounts

Payable—‘Supplier Name’

Notes Payable: A note payable is a written promissory note to pay a future amount. Notes payable are different from accounts payable because they come from a formal contract called a promissory note and usually require interest.

Unearned Revenue Accounts: Unearned revenue is a liability that is recorded when customers pay in advance for products or services. Examples of unearned revenue include magazine subscriptions collected in advance by a publisher, rent collected in advance by a landlord, and season ticket sales by sports teams. The seller would record these in liability accounts such as Unearned Subscriptions and Unearned Rent. When products and services are later delivered, unearned revenue is

transferred to revenue.