Chapter 13 The Cost of Production

13-1 What are Costs?

13-1a Total Revenue, Total Cost, and Profit

Total Revenue = the amount a firm receives for the sale of its output

Total Cost = the market value of the inputs a firm uses in production (ex. flour, workers)

Profit = total revenue minus total cost

13-1b Costs as Opportunity Costs

cost of production include all opportunity cost of making its output of goods and services

pays $1,000 for flour, that $1,000 is opportunity cost cause no longer use that to pay something else

Explicit costs = input costs that require an outlay of money by the firm

implicit costs = input costs that do not require an outlay of money by the firm

work as programer and earn $100 and not make cookies, gives up $100 income.

total cost = explicit + implicit costs

13-1c The Cost of Capital as an Opportunity Cost

implicit cost is the opportunity cost of the financial capital that has been invested in the business

use 300,000 to buy factory. If instead left this money in saving account that earn interest rate of 5%, would’ve earned 15,000 per year. To owns this factory, gave up 15,000 a year. So 15,000 is one of implicit opportunity cost.

13-1d Economic Profit versus Accounting Profit

Economic Profit = total revenue minus total cost, including both explicit and implicit costs

Accounting Profit = total revenue minus total explicit cost

accounting profit usually larger than economic profit

13-2 Production and Costs

13-2a The Production Function

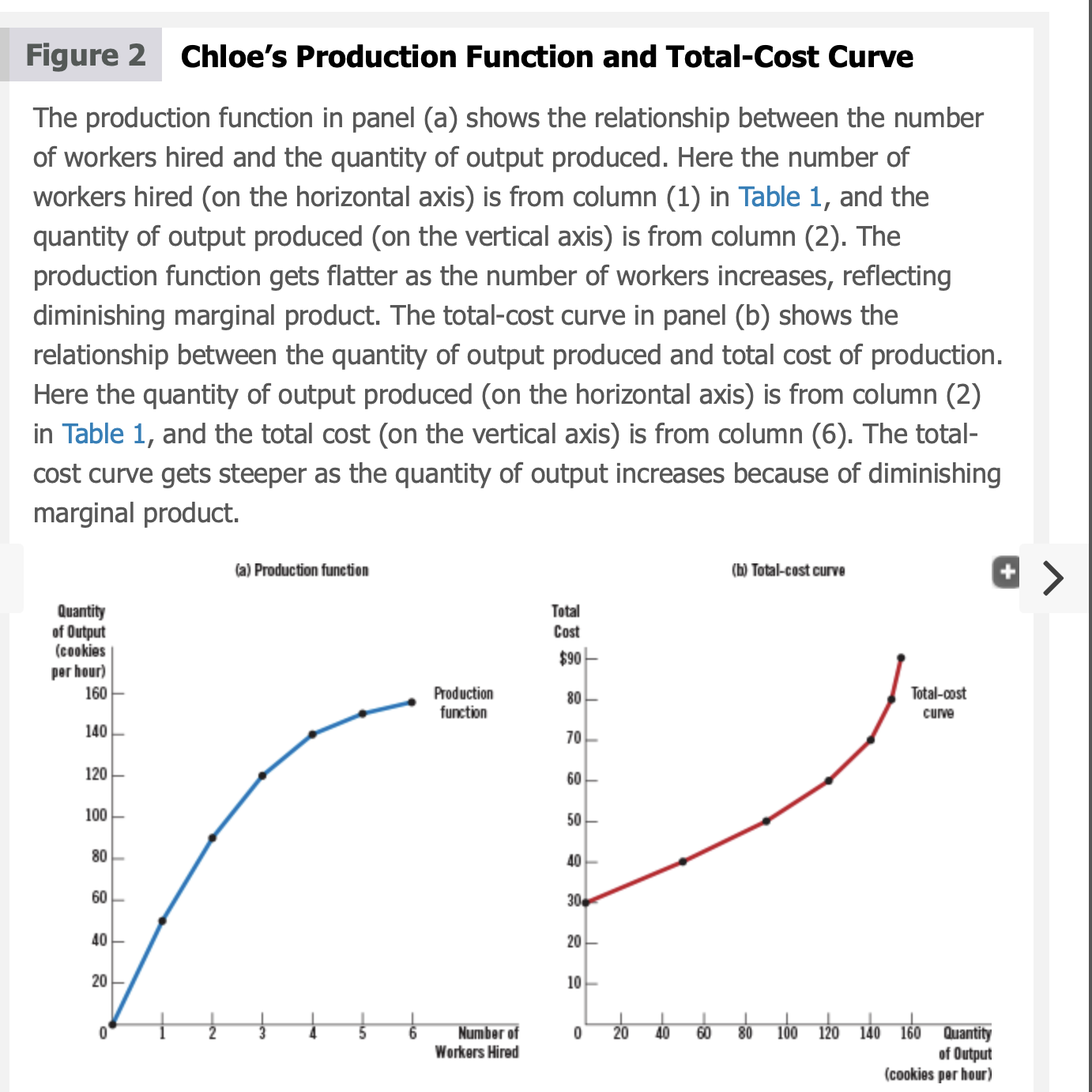

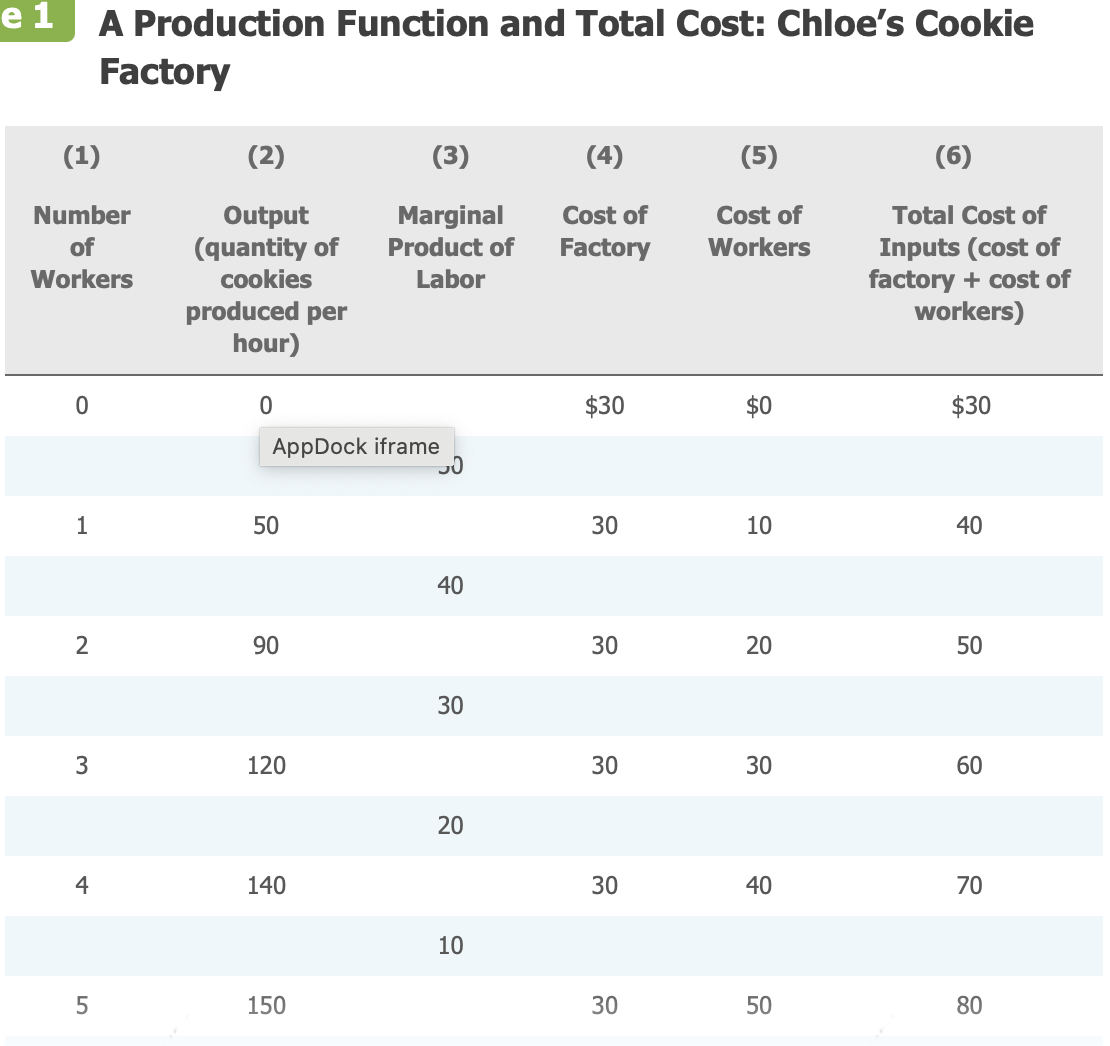

Production function = the relationship between the quantity of inputs used to make a good and the quantity of output of that good

marginal product = the increase (or change) in output that arises from an additional unit of input

Diminishing marginal product = the property whereby the marginal product of an input declines as the quantity of the input increases

Most important relationship: quanitty produced (column 2) and total cost (column 6)

13-3 The Various Measures of Cost

Fixed costs are costs that do not vary with the quantity of output produced. In the short run, a firm cannot alter the size of its operation, so the cost of the factory is a fixed cost. In the long run, however, the firm can choose its size of operation, so the cost of the factory becomes one of the variable costs.

Average fixed cost is fixed cost divided by the quantity of output. As quantity of output increases, average fixed cost falls.

Variable costs are costs that change as the firm alters the quantity of output produced.

The opportunity cost of an action is the value of all those things that must be forgone to take that action.

Explicit costs are the input costs that require an outlay of money by the firm.

Average variable cost is variable cost divided by the quantity of output. Whenever marginal cost is less than average variable cost, average variable cost is falling. Whenever marginal cost is greater than average variable cost, average variable cost is rising.