Making Informed Financial Decisions

Financial Products (7.1)

Financial Products are contracts that consumers enter into with financial service providers to manage their money, whether saving, investing or taking out a loan.

FSPs - firms that operate in the financial industry e.g. banks, credit unions, insurance companies

Savings

the proportion of our income we choose not to spend

to pay back debt

children’s education

home improvement

new car

Where to save?

commercial banks e.g. BOI

the Credit Union

An Post

As European residents, Irish citizens can also shop around for banks/ financial providers in other EU countries.

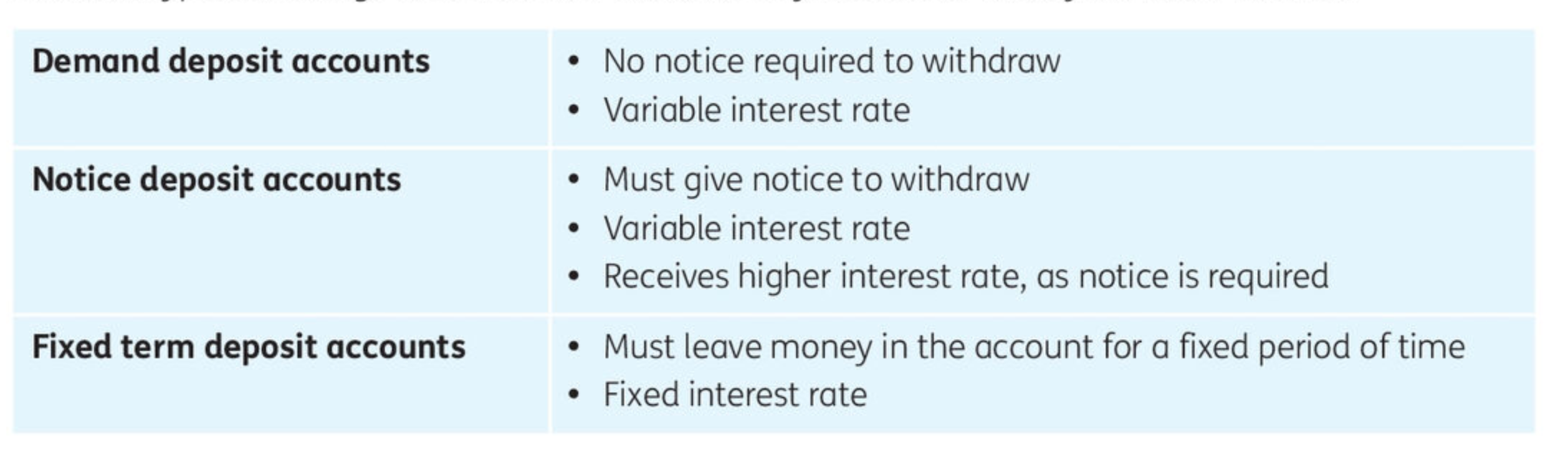

Types of saving accounts

Interest is the reward for saving or the cost of borrowing.

Interest rates can be:

Fixed - stay the same for a set period of time

Variable - change over time based on market conditions

Investments

Investments are assets or ventures that money is put into, with the goal of earning a profit

Types of investments

Shares/Stocks - Represent ownership in a company

Advantage - Potential for good returns and to diversify risk in investing in different sectors or countries

Disadvantage - Share prices can fall, holding shares in one company is very high risk

Bonds - Loans given to businesses or the government.

In return, the issuer:

pays interest

repays the original value at an agreed date

Advantage - Regular income in the form of interest payments.

Disadvantage - Money isn’t accessible for a specific time

Property - money invested in commercial or residential property. Earn money through rental income/ property appreciation.

Advantage - Potential for long-term growth

Disadvantage - High minimum investment

Cryptocurrency - digital or virtual currencies (i.e. bitcoin). Bought and held in an investment in hope that their value will increase.

Pension/Retirement planning

Pension and retirement planning combines strategic long-term savings with a variety of investments to build a strong pension plan.

Ensures financial stability and manages risk

It’s important to strart planning early to make sure they have enough resources to support their retirement.

Borrowing

Types of finance

Overdraft (short term) - Bank gives current account holder permission to withdraw more money than they have in their account, up to an agreed limit

Used for bills e.g. phone and internet

Only pay interest on amount used

Credit Cards (short term) - allow an individual to buy goods and services up to a certain limit

Used for concert tickets, online purchases

When the balance is paid within an agreed period of time (interest-free period), no interest is charged.

Holder pays stamp duty, annual government tax

Trade Credit (short-term finance) - Credit for 30 days when you buy an item; you don’t have to buy up front

Businesses use it so they can have some leeway to sell products and then pay the supplier

Personal Loan (medium term) - type of unsecured loan provided by banks, used for personal expenses, monthly payments.

Used for car or home improvement for example.

Leasing/Renting (medium term) - individual signs a lease to use an asset for a set period in exchange for regular payment. e.g. property rental, car, computer equipment.

Immediate use of the item

No large deposit or collateral

Lesee never owns the item

Item reposessed if payments arent made

Hire purchase - paying for an item in installments with interest. e.g. car, laptop, tv.

Immediate use of the item

Customer doesn’t own the item until the final installment is paid.

High interest

Personal Contract Plan (PCP) - car financing option. low monthly payments and a final payment based on the guaranteed minimum future value(GMFV). Choose to keep, enter into a new contract or return the car.

Lower monthly payments than traditional car loans.

Monthly repayments and fina baloon are set at the start

Customer doesn’t own the car until final payment is made.

Exceeding mileage limit can incurr extra charges.

Mortgage (long-term) - Long-term loan to buy property.

Can be offered up to 35 years.

Repaid monthly with interest

property deed is collateral

Types:

Fixed rate - Monthly payments fixed for a set period.

Variable rate - interest rate set by lender and can change at any time.

Tracker: Interest rate follows the rate of the ECB(European Central Bank)

Allows for purchase of a home without paying the full price upfront

Offers potential financial gains as property prices may increase.

Collateral must be provided

Interest over life of the loan can be significant

Long-term loan - Loan with repayment period over 5 years. for home extension/improvements

Allows for borrowing a large sum of money

If variable rate of interest and rate increases, repayment increases.

Factors to consider when choosing a source of finance

Purpose - Matching principal dictates that the source of finance should match the time frame of the item being bought

Cost - APR(Annual percentage rate) is the yearly cost of borrowing, shown as a percent. Includes interest payable and any other fees

Collateral - valuable item given to the lender as a repayment guarantee, which lender takes if the borrower defaults(fails to make agreed payments)