CIE AS Level Accounting: Control Accounts

A control account is like the ‘total‘ account for all sales and purchases ledgers from their books of prime entry. The balance on a control account should equal the total of the balances in the ledger it controls.

- control accounts check the arithmetical accuracy of the individual ledger accounts

- control accounts summarise the ledgers it controls for easier posting to the trial balance and other financial statements

- control accounts protect against fraud as the work between preparing the individual ledgers and preparing the control accounts can be delegated to other employees

However, control accounts still have their own limitations;

- control accounts don’t provide specifics of a transaction as it is more like a summary account

- control accounts can only be used in businesses which use the double-entry system

- due to the preparation of these systems, additional staff may have to be hired OR computerised accounting systems may need to be introduced which also may entail more staff to either be hired or trained

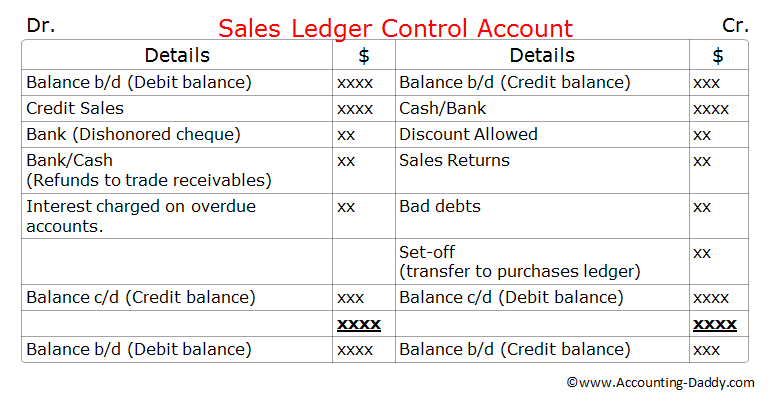

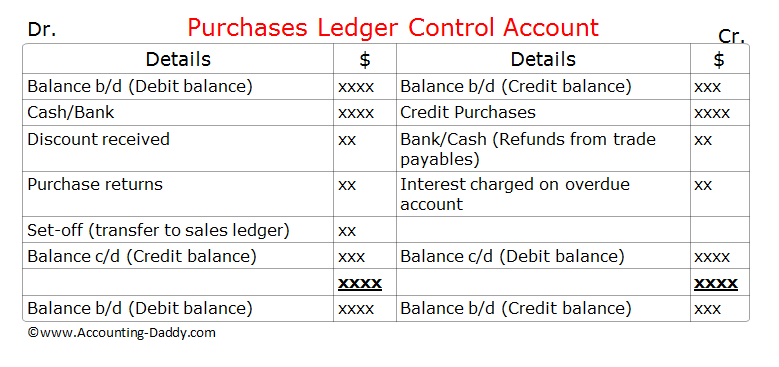

Preparation of Control Accounts

Note: irrecoverable/bad debts written off are to be included in the individual sales ledgers and the control accounts

Some entries in the sales control accounts that aren’t usual are:

- dishonoured cheques — these are cheques from customers who have tried to pay off their balance but do not have enough money to cover it, hence it is sent back and the business is not paid

- credit balances — these are balances as a result of a customer;

- overpaying their invoice

- paying in advance

- paying a deposit before the delivery of the goods and the creation of the invoice

- have paid the invoice in full but were later sent a credit note due to problems discovered later

- contra — two businesses may be each other’s trade receivable and trade payable and so owe each other money; the contra entry is found on the opposite side of the opening balance (balance b/d)

Reconciliation of Control Accounts

When there is a difference between the balance on a control account and the total balances in the ledger it controls, corrections must be made and reconciled.

However, there are a few types of errors that the trial balance will not identify:

- error of omission — if the figures do not appear in any of their respective accounts, the control account and individual ledgers cannot identify this error; the records will be incorrect but the trial balance will still balance

- error of original entry — the entry is found in both its individual ledger and the control account

- error of compensation — two or more errors cancel each other out

- error of reversal — the right amounts have been posted but on the wrong sides; debit entry is credited and vice versa

- error of original entry — the incorrect amounts have been posted but are still on the right sides and accounts

These will not be identified as the trial balance will still balance. On the other hand, the errors that the control accounts will identify are:

- error of principle — the correct amounts have been posted but one is posted in the wrong type of account

- error of commission — the correct amounts have been posted in the right type of account but to the wrong specific account e.g a sale to E Brown has accidentally been recorded as a sale to F Brown

- error of partial ommision — only one side of the double entry has been posted

- error of transposition — the same transaction has been recorded in the individual ledgers and the control accounts but their figures differ

These will be identified as the control account will not agree with the total of all the individual ledgers.

If the error affects a total, it should be reconciled in the control account. If the error affects one ledger account, it should be reconciled in that individual ledger account.