ch. 6 - inventory and cost of goods sold

pt. a ) reporting inventory and cost of goods sold

types of inventory

inventory - items a company intends for sale to customers in the ordinary course of business

report as a current asset in the balance sheet b/c it represents a valuable resources to the company; current b/c the company expects to convert it to cash in the near term

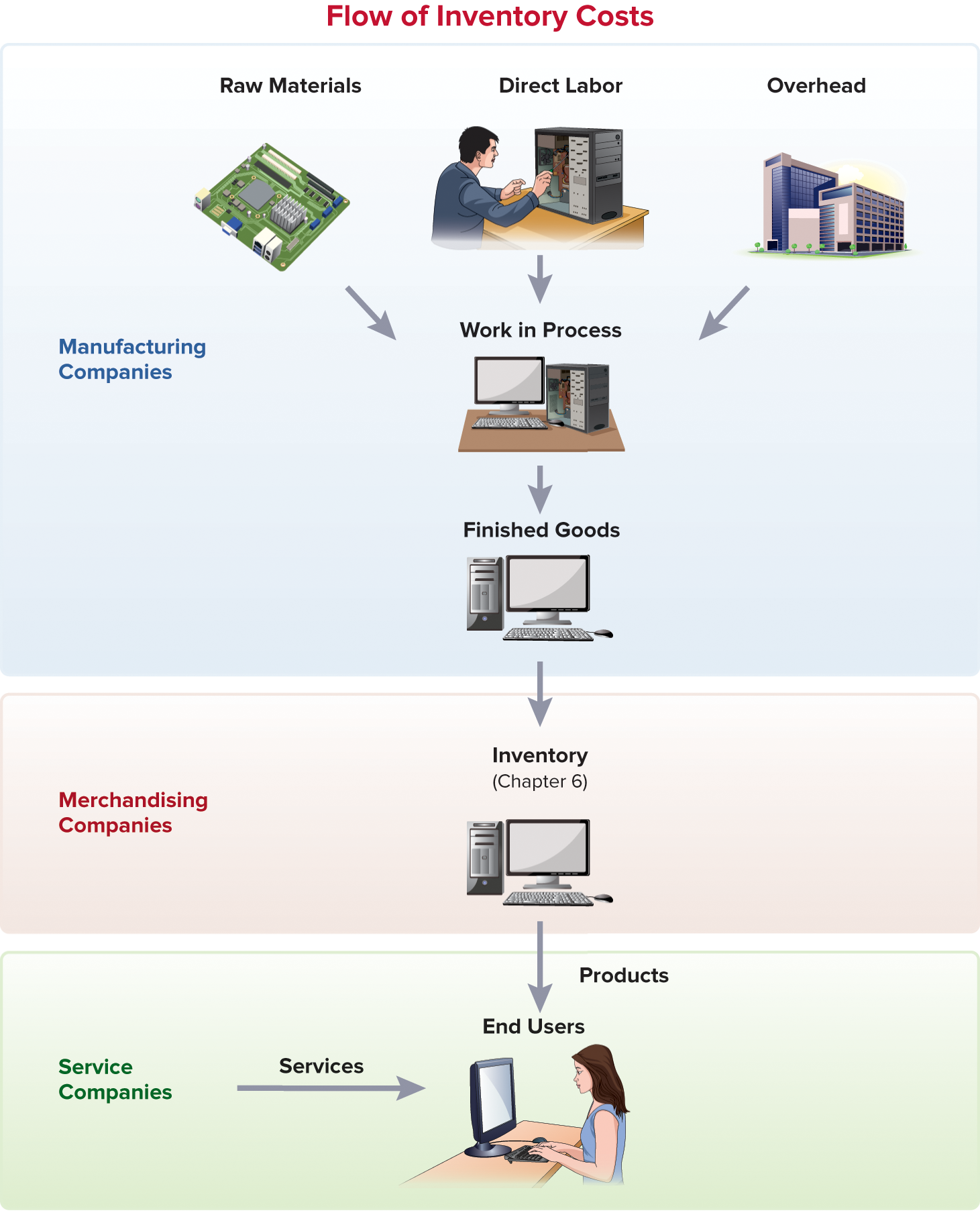

obj. 6.1 - understand that inventory flows from manufacturing companies to merchandising companies and is reported as an asset in the balance sheet

manufacturing companies

manufacturing companies produce the inventories they sell, rather than buying them in finished form from suppliers; they buy the inputs for the products they manufacture

inventory is classified for a manufacturer into three categories;

raw materials - includes the cost of components that will become part of the finished product but have not yet been used in production

work in process - refers to the products that have been started in the production process but are not yet complete at the end of the period; total cost includes raw materials, direct labor, and indirect manufacturing costs called overhead

finished goods - the cost of full assembled but unshipped inventory at the end of the reporting period

merchandising companies

merchandising companies don’t manufacture computers or their components, they purchase finished products to sell to customers; serve as intermediaries

they may assemble/sort/repackage/redistribute/store/refrigerate/deliver/install, but do not manufacture

inventory acounts ($ in millions) | intel | best buy |

raw materials | $840 | |

work in process | 6225 | |

finished goods | 1679 | |

merchandise inventories | $5174 | |

total inventories | $8744 | $5174 |

wholesalers and retailers

merchandising companies can be classified as wholesalers or resalers

wholesalers resell inventory to retail companies or professional users

retailers purchase inventory from manufacturers or wholesalers and then sell this inventory to end users

service companies record revenues when providing services to customers. merchandising and manufacturing companies record revenues when selling inventory to customers.

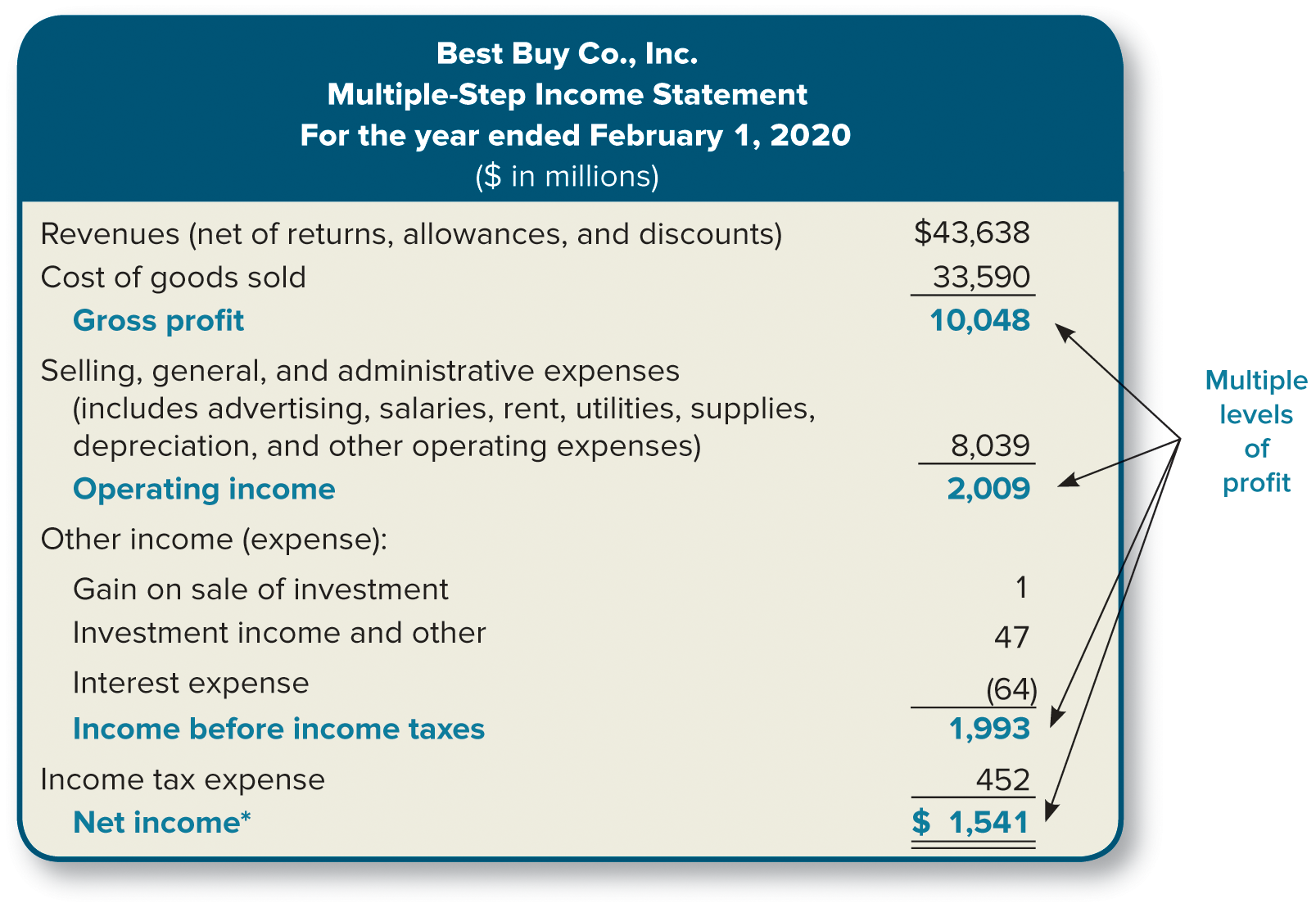

multiple-step income statement

cost of goods sold - cost of the inventory that was sold during the period

obj. 6.2 - understand how cost of goods sold is reported in a multiple-step income statement

example

assume that a best buy begins the year with $20k of inventory of headphones = how much best buy spent to purchase inventory of headphones on hand at the beginning of the year

during the year, bb purchases additional headphones for $90k,

the total cost of headphone inventory is now $110k (=$20,000+$90,000)

of the $110k in inventory, by the end of the year the purchase cost of the remaining headphones unsold is $30,000, and $80,000 (= $110,000-$30,000) was sold) this is the amount reported for cost of goods sold as an expense in the income statement

inventory is a current asset reported in the balance sheet and represents the cost of inventory unsold at the end of the period. cost of goods sold is an expense reported in the income statement and represents the cost of inventory sold

multiple-step income statement - an income statement that reports multiple levels of income (or profitability)

most companies choose to report their income statement to show the revenues and expenses that arise from different types of activities.

by separating revenues and expenses into their different types, investors and creditors are better able to determine the source of a company’s profitability.

understanding the source of current profitability often enables a better prediction of future profitability

levels of profitability

gross profit - the difference between net sales and cost of goods sold

since inventory transactions are important for merchandising companies, they must report the revenues and expenses directly associated with these transactions in the top section of a multiple-step income statement

revenues include the sale of products and services to customers.

inventory sales are referred to as sales revenue

providing services is referred to as service revenue

the net amount of revenues is referred to as net sales

cost of goods sold is the cost of inventory sold during the year

operating income - profitability from normal operations that equals gross profit less operating expenses

after gross profit, operating expenses are reported (selling, general, and administrative expenses)

measures profitability from primary operations, a key performance measure for predicting the future profit-generating ability of the company

income before income taxes