Macroeconomics

Lessons

- People make choices that arise in scarcity

- People respond to incentives

- Importance of division of labor and specialization

- Standard of living is higher due to specialization

- Importance of supply chains

Economics - the study of choices that arise from scarcity

Economic goods - scarce, prices > 0

Free goods - abundant, free = 0

Economics is the study of how individuals and organizations allocate scarce resources among alternative uses to satisfy unlimited human wants

Economics As a Production Function

resources (inputs) —> production process —> goods and services (outputs)

Microeconomics

- individual decision - making households, firms, markets

Macroeconomics

- aggregate economics variables

- Economy as a whole

- Ex: GDP, inflation, unemployment, money supply, interest rates

Positive Analysis

- “what is”

- Descriptive

- Factual testable statements

- True or false

- Objective

- “Value-free”

- Causative

- If X, then Y

Normative Analysis

- “what ought to be“

- Prescriptive

- Opinion

- Not testable

- Subjective

- Values are explicit

- Not causative

The Methodology of Economics

- How do economists study the world?

- Model - Building

- Complex reality —> Simple Model

- Use of assumptions

Overriding Assumptions

- Rational self-interest

- More is better

- Ceteris Paribus: everything else held constant

Scientific Methods

- recognize a problem—> make assumptions

- Build model —> derne predictions

- Test Model

Opportunity Costs

- The benefit foregone from not choosing the next best alternative

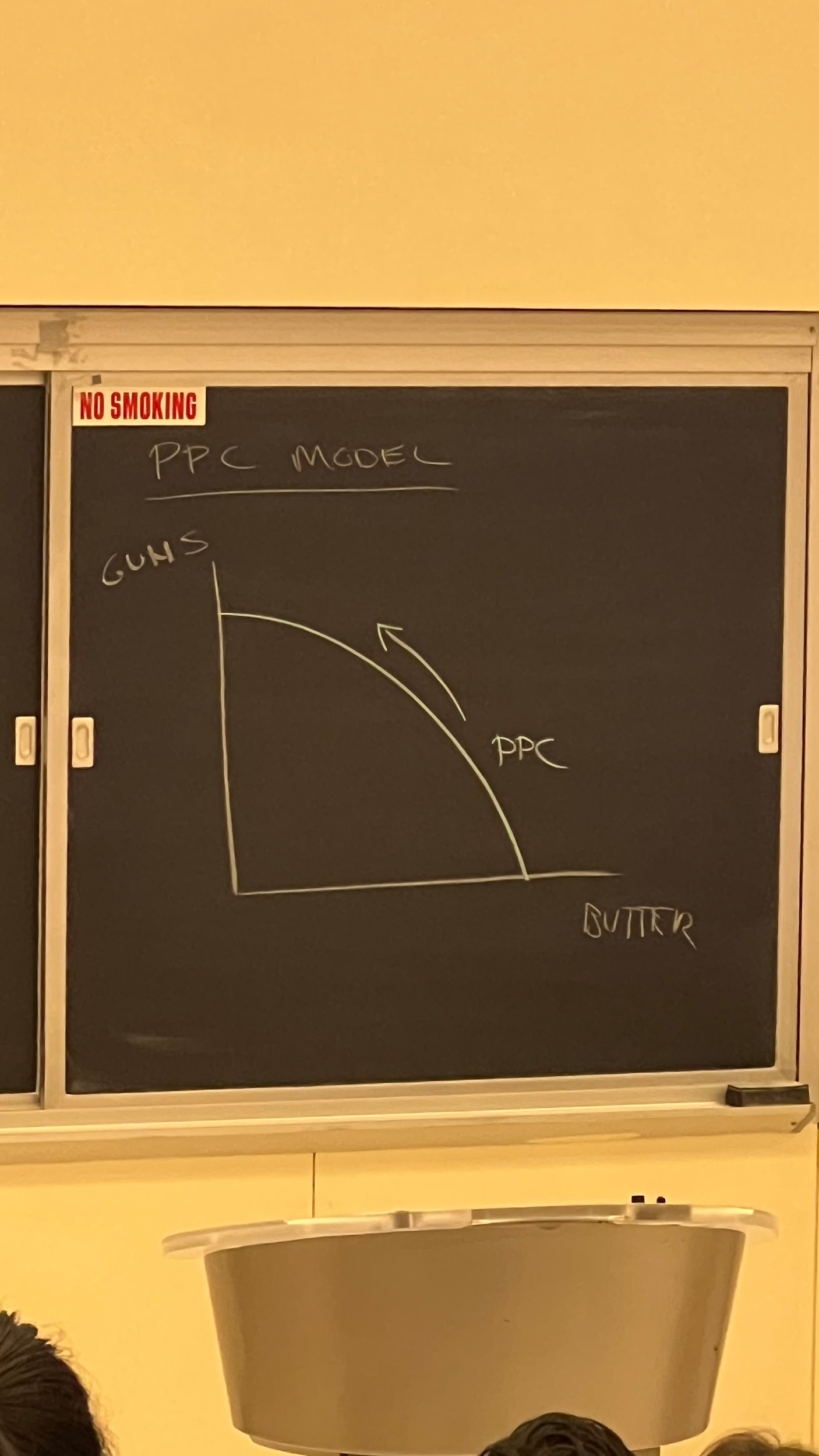

Production Possibility Curves (PPC)

- First model

- A model that shows the maximum combinations of two goods that can be produced, given certain quantity of resources and state of technology

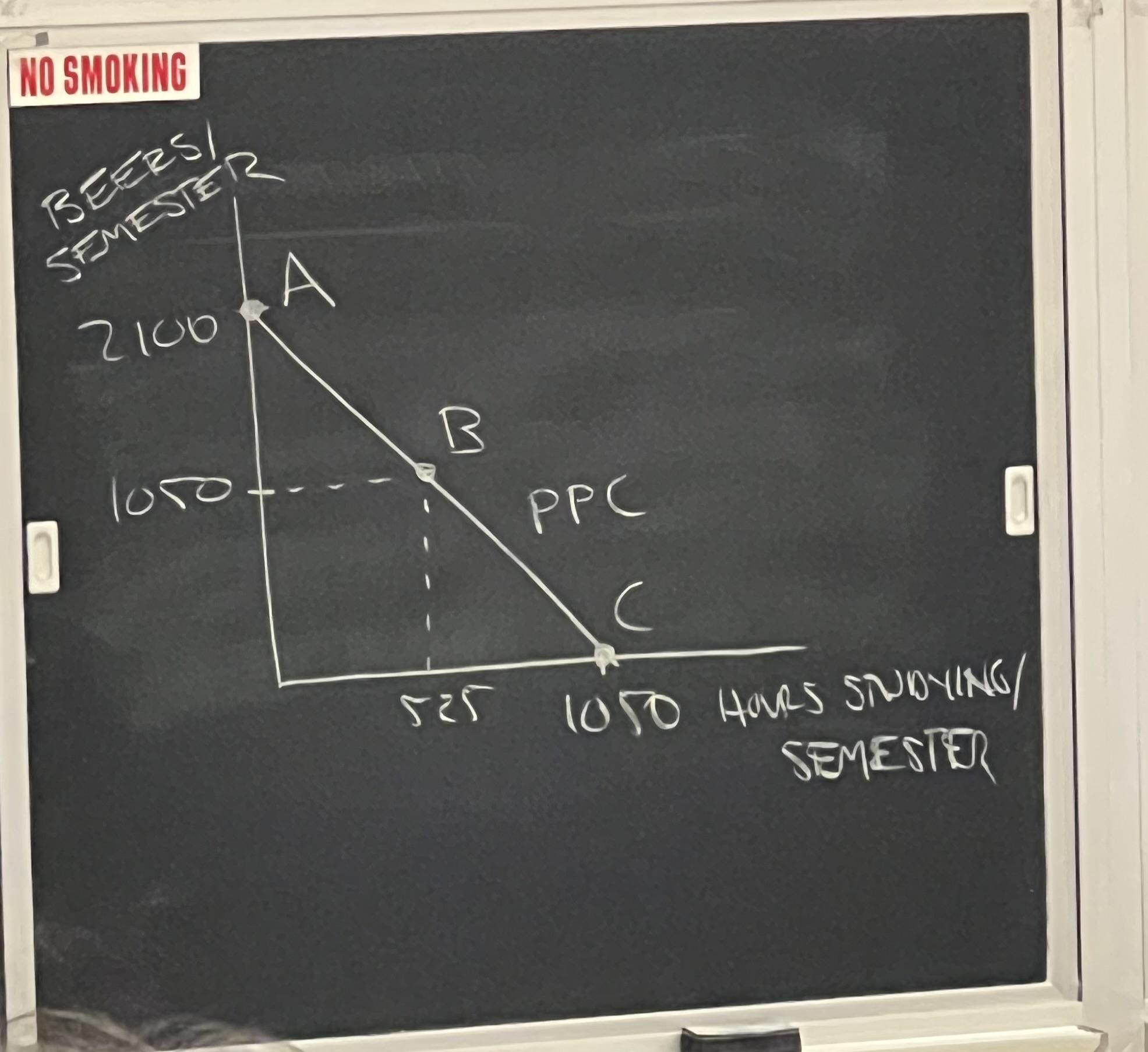

Example I

- Choices of college students

- Assumptions

- Can spend time either on academic life v social life

- Academic time: hours studying

- Social life: beer drinking

- Beer is free

YOU CANNOT STUDY AND PARTY AT THE SAME TIME

- Can drink two beer per hour

- 10 hours per day x 7 days a week = 70 hours per week x 15 weeks/semester = 1050 hours per semester

Points A, B and C are efficient

Point D is inefficient

Point E is unattainable

Score = rise/run = -2100/1050 = -2 = opportunity cost of good on horizontal axis

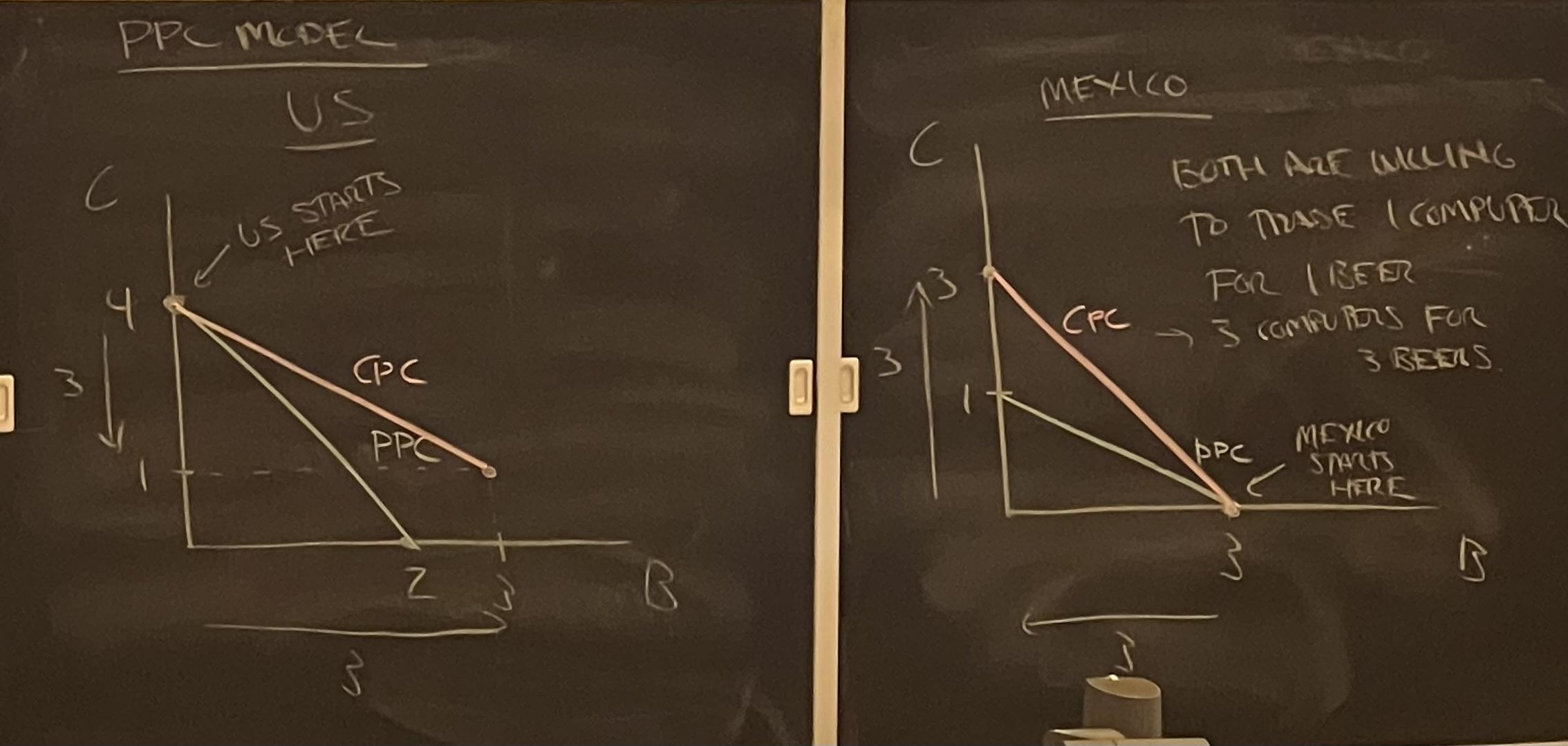

The Principle of Comparative Advantage

- Each party of the trade should specialize in the production of that good in which it is relatively more efficient (or has lower opportunity costs)

Corollary

- Mutual gains arise from specialization and trade

Absolute Advantage

- Lower resource cost

Comparative Advantage

- Lower opportunity cost

Example: US + Mexico

- Can produce computers and beer

- absolute advantage

US Mexico

Computer/year 4 1

Beer/year 2 3

(in millions)

- Determine Opportunity Cost

US Mexico

4C = 2B 1C = 3B

1C = ½B 1C = 3B

1B = 2C 1B = ⅓C

- Assign Tasks

US → has lower opportunity cost in computers (½B vs 3B)

- Should specialize in computers

Mexico → has lower opportunity cost in beer (⅓C vs 2C)

- Should specialize in beer

- Show Results of Trade

w/o specialization w/ specialization

US → ½ yr each US → 1 yr comp

Mexico → ½ yr each Mexico → 1 yr beer

__________________ _________________

Computers: ½(4) + ½(1) = 2.5 4

Beer: ½(2) + ½(3) = 2.5 3

- Terms of Trade

- Rate at which both countries would be willing to make a trade

- Defend on opportunity cost

- US → is willing to trade 1 computer for anything greater than ½ beer

- Mexico → is willing to trade 1 computer for anything less than 3 beers

- Both willing to trade 1 computer for 1 beer

- Assume opportunity cost are constant

CPC: Consumption Possibilities Curve

- Shows all combinations that are possible through trade

Example II

- US builds new breweries

- Comparative Advantage

US Mexico

Computer/year 4 1

Beer/year 4 3

(in millions)

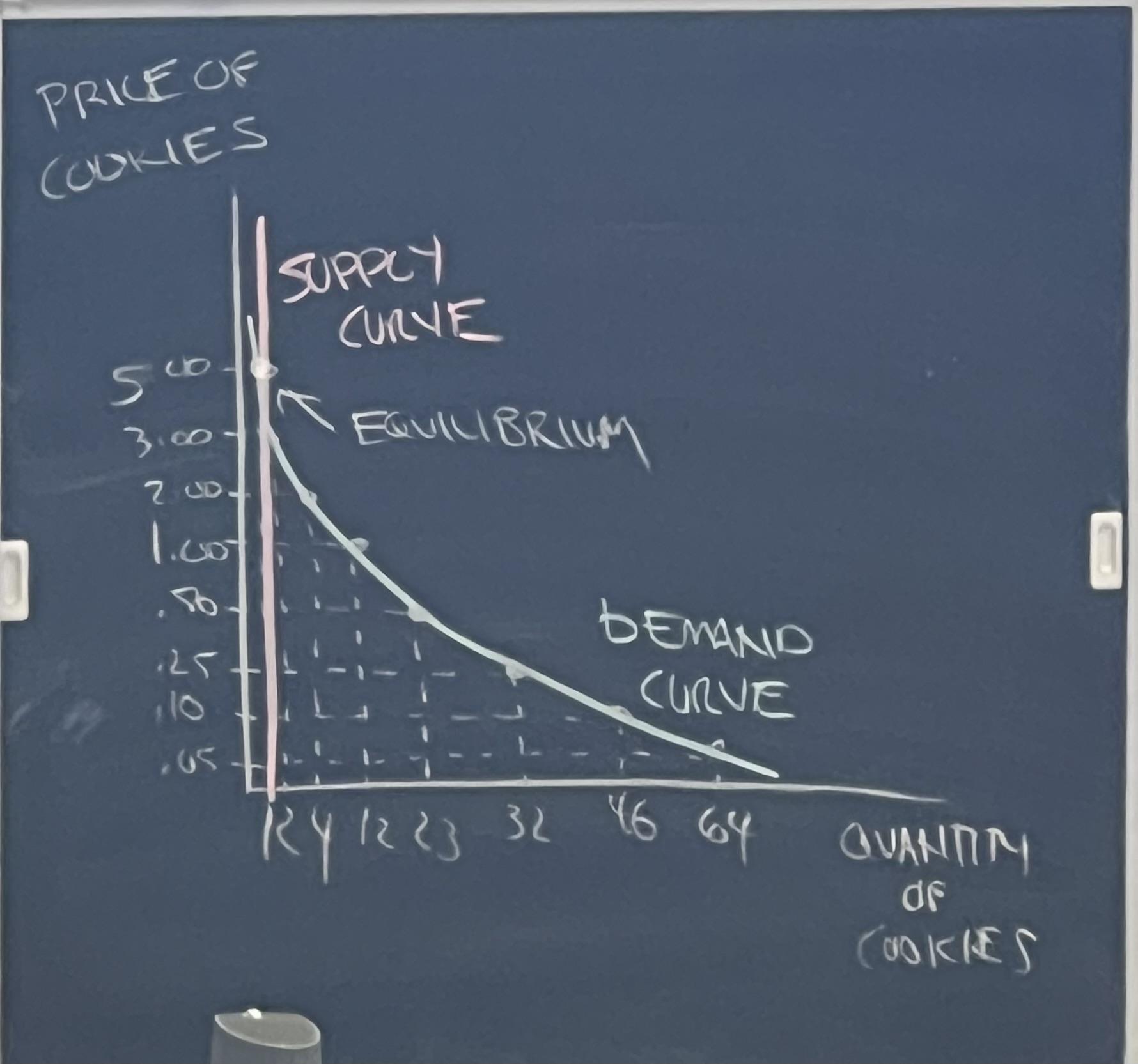

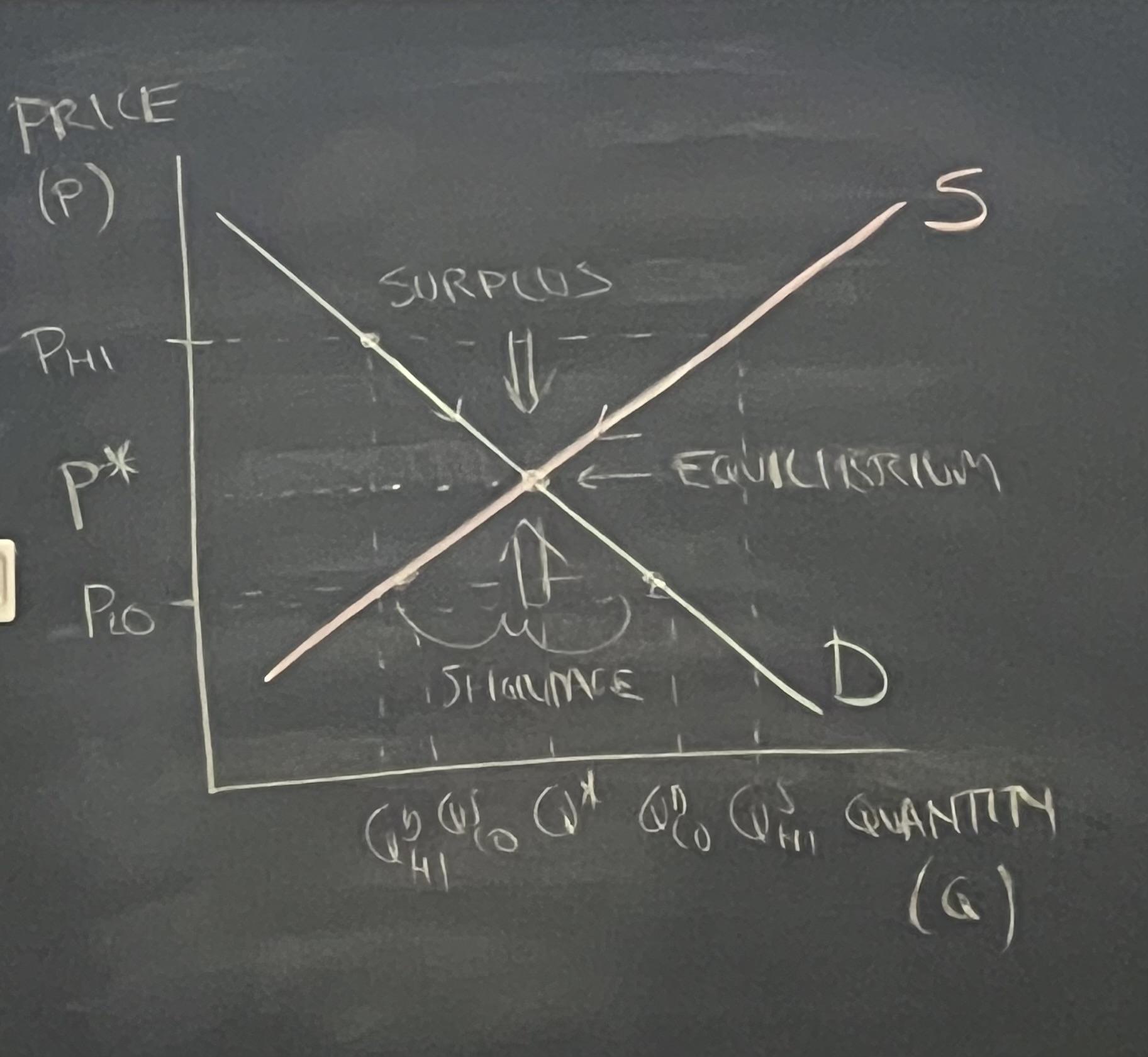

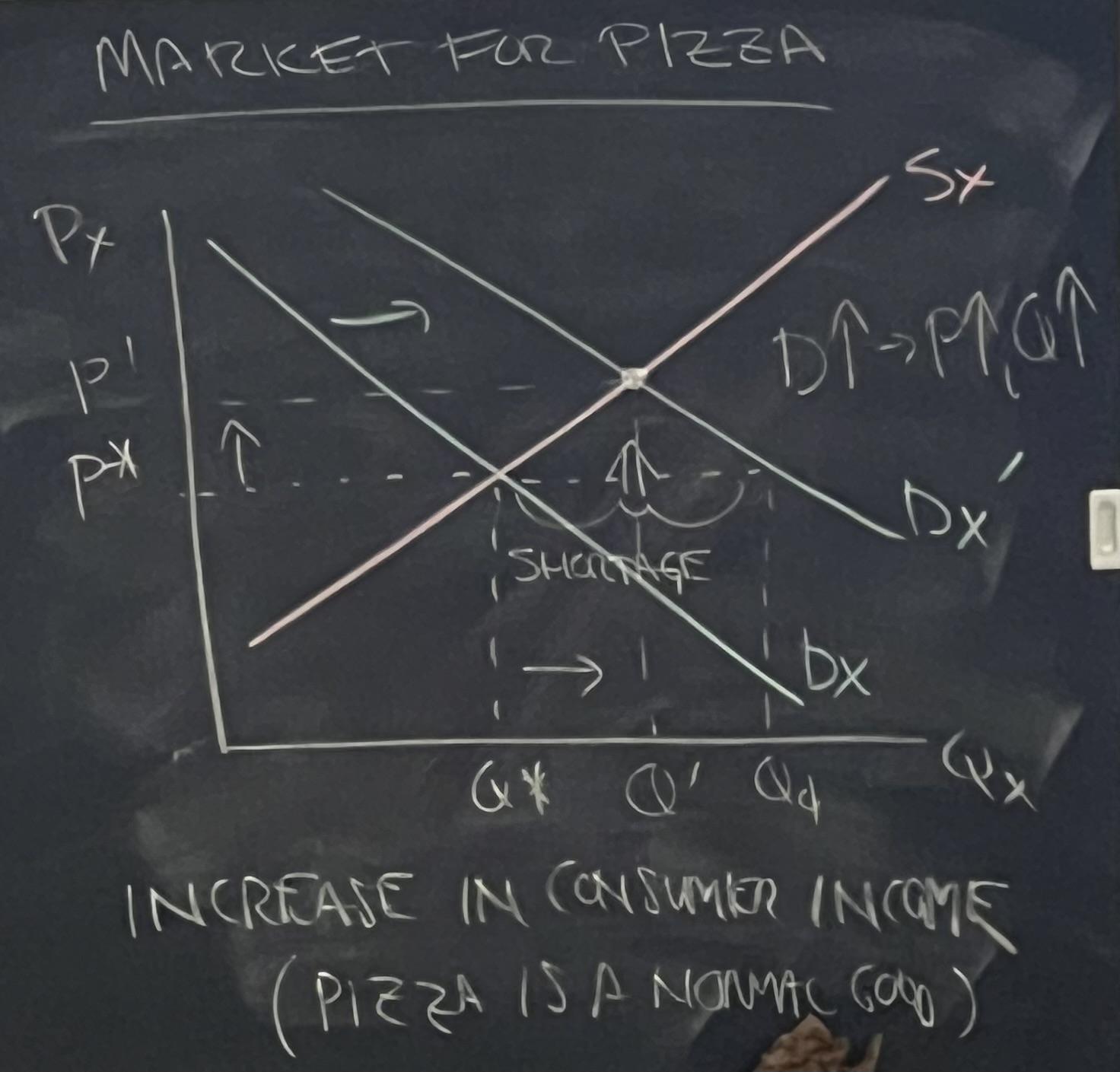

Demand + Supply Analysis

- Demand Curve - a model that describes the behavior of consumers in a market

- Supply Curve - a model that describes the behavior of producers in a market

- Market - a collection of buyers and sellers where exchange takes place

Three Characteristics

- Geographic Space

- Time Period

- Product Space

Types of Resources: Allocation Mechanisms

- Government Edict

- Merit-Based criteria

- Arbitrary criteria

- Egalitarianism

- Lottery/Random

- First Come, First Serve

- Queuing

- Markets

Lessons

- The Law of Demand

- There is an inverse relationship between the price of a good and the quantity demanded of that good, Ceteris Paribus

- Equilibrium occurs at the intersection of the supply and demand curve

- Market allocate resources to their most value uses

- Markets are efficient resources of the distribution of income

EFFICIENCY V EQUITY

Equilibrium

- A situation that will tend to persist over time

Demand Curve

- A model that shows the quantity of output that consumers in a market are willing and able to purchase at different prices

Determinants of Demand

- Price of good X (Px)

- Price of substitutes and complements (Py)

- Income (I)

- Tastes + expectations (T)

- Population (POP)

Demand Evaluation

= F(PX, Py, , , )

↑ ↑

Quantity is a - X is

Demand function of held constant

of some

Good X

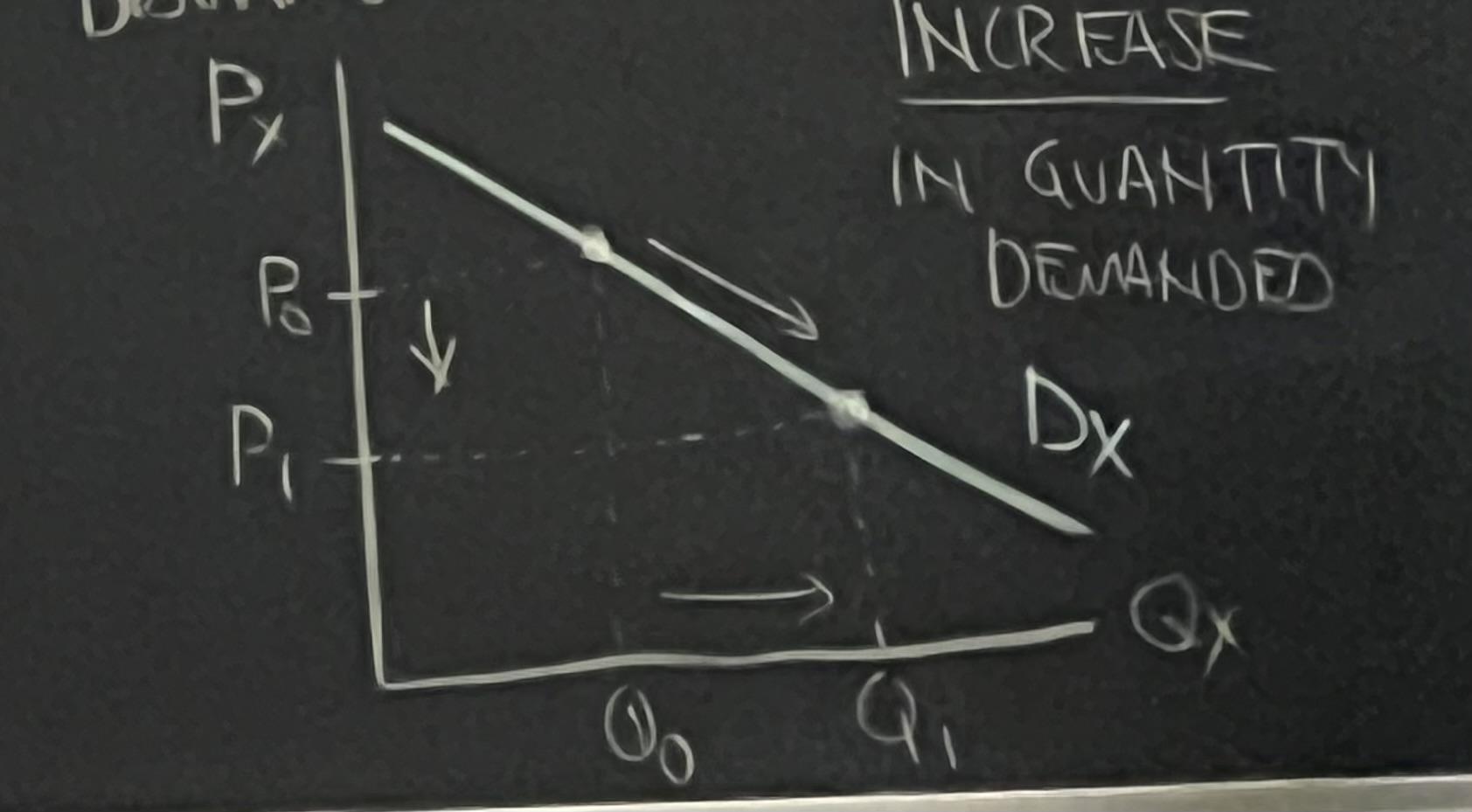

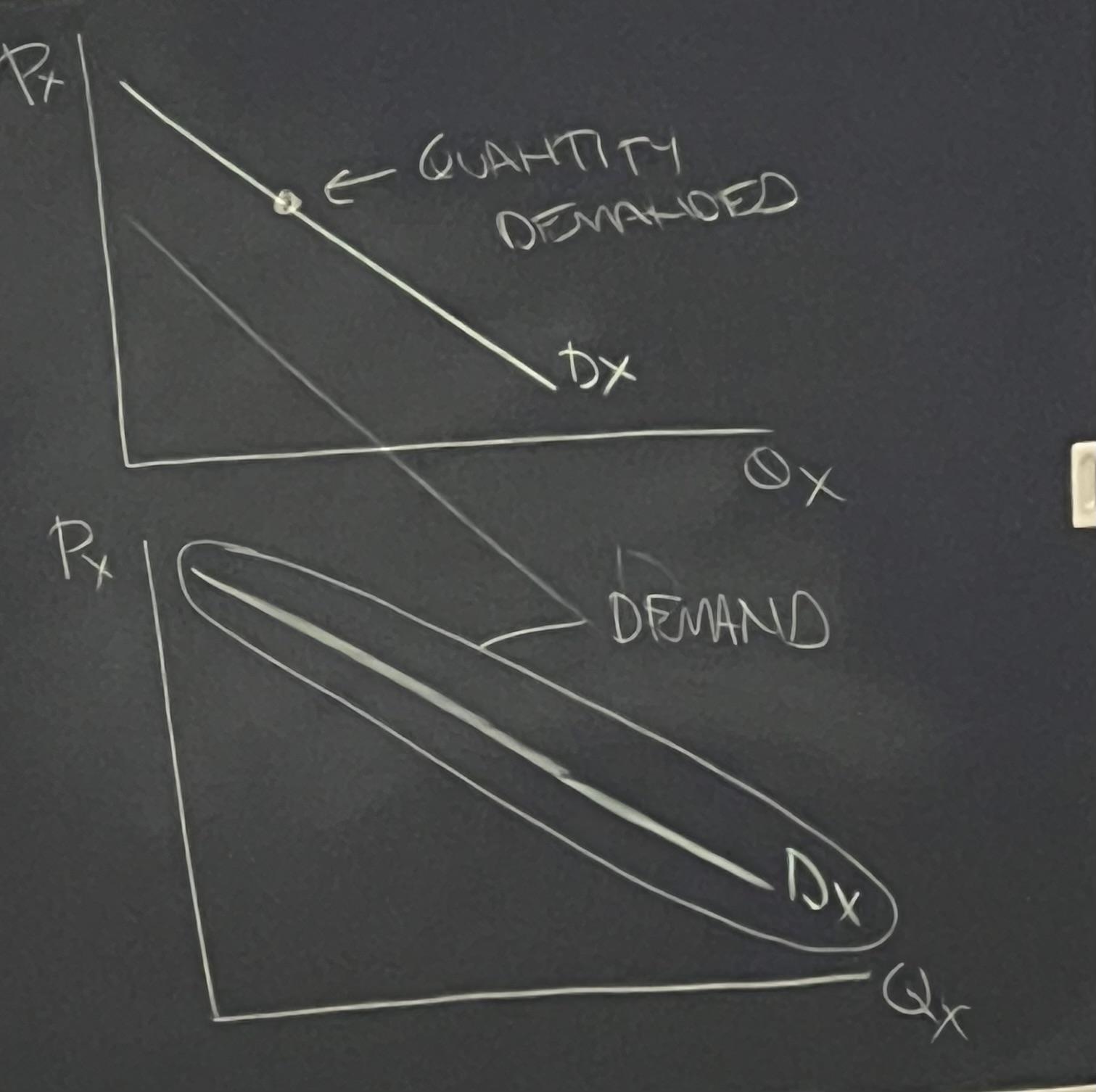

Change in Quantity Demanded

- Results from a chance in Px only

- Movement along a new demand curve

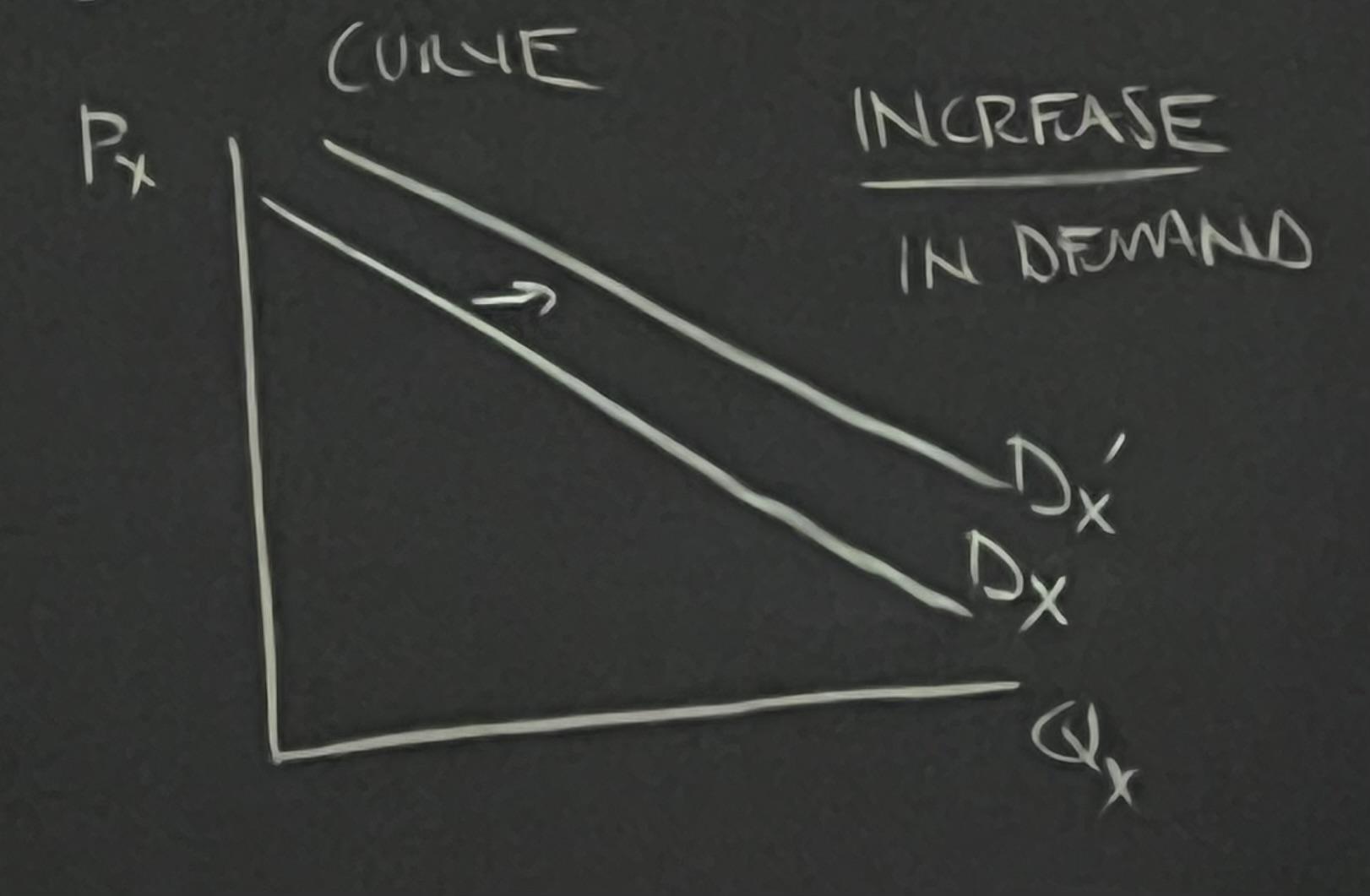

Change in Demand

- Results from a chance in Py, I, T, POP

- Shift of entire demand curve

An Increase in Demand May Be Caused By

- An increase in price of a substitute

- A decrease in the price of a complement

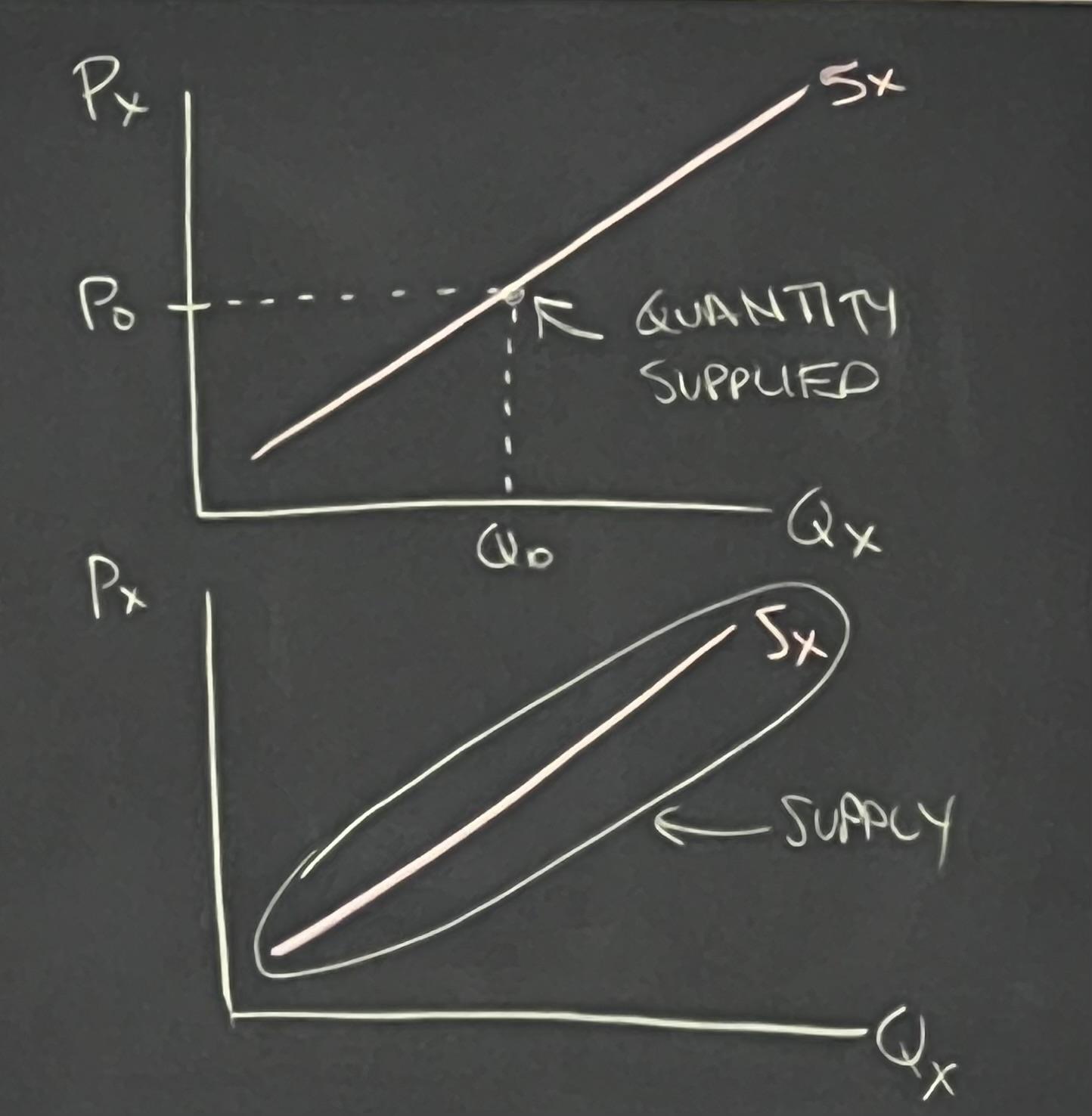

Supply Curve

- A model that seeks the quantity of output that is produced in a market is willing and able to sell at different prices. Ceteris Paribus

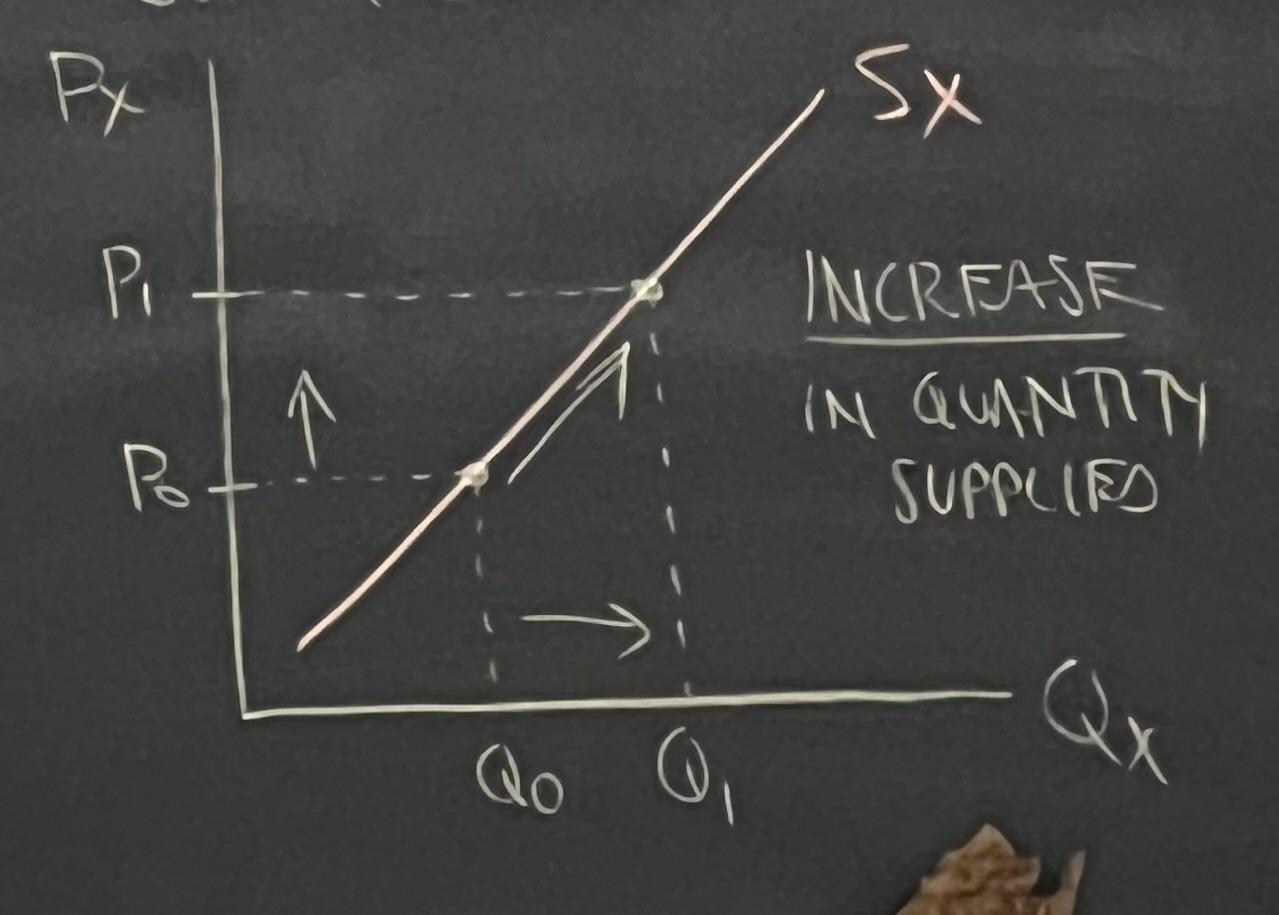

Law of Supply

- There is a direct relationship between the price of a good and the quantity supplied of that good, Ceteris Paribus

Determinants of Supply

- Price of good X (Px)

- Resource price (Pr)

- Technology (TECH)

- Business expectations (EXP)

- Number of firms (N)

- Price of Related Goods (Pz)

Supply Equation

= F (PX, PR, TECH, EXP, N,PZ)

↑ ↑

Quantity is a - X is

Demand function of held constant

of some

Good X

Change in Quantity Supplied

- Results from a change in Pz only

- Movement along a given supply curve

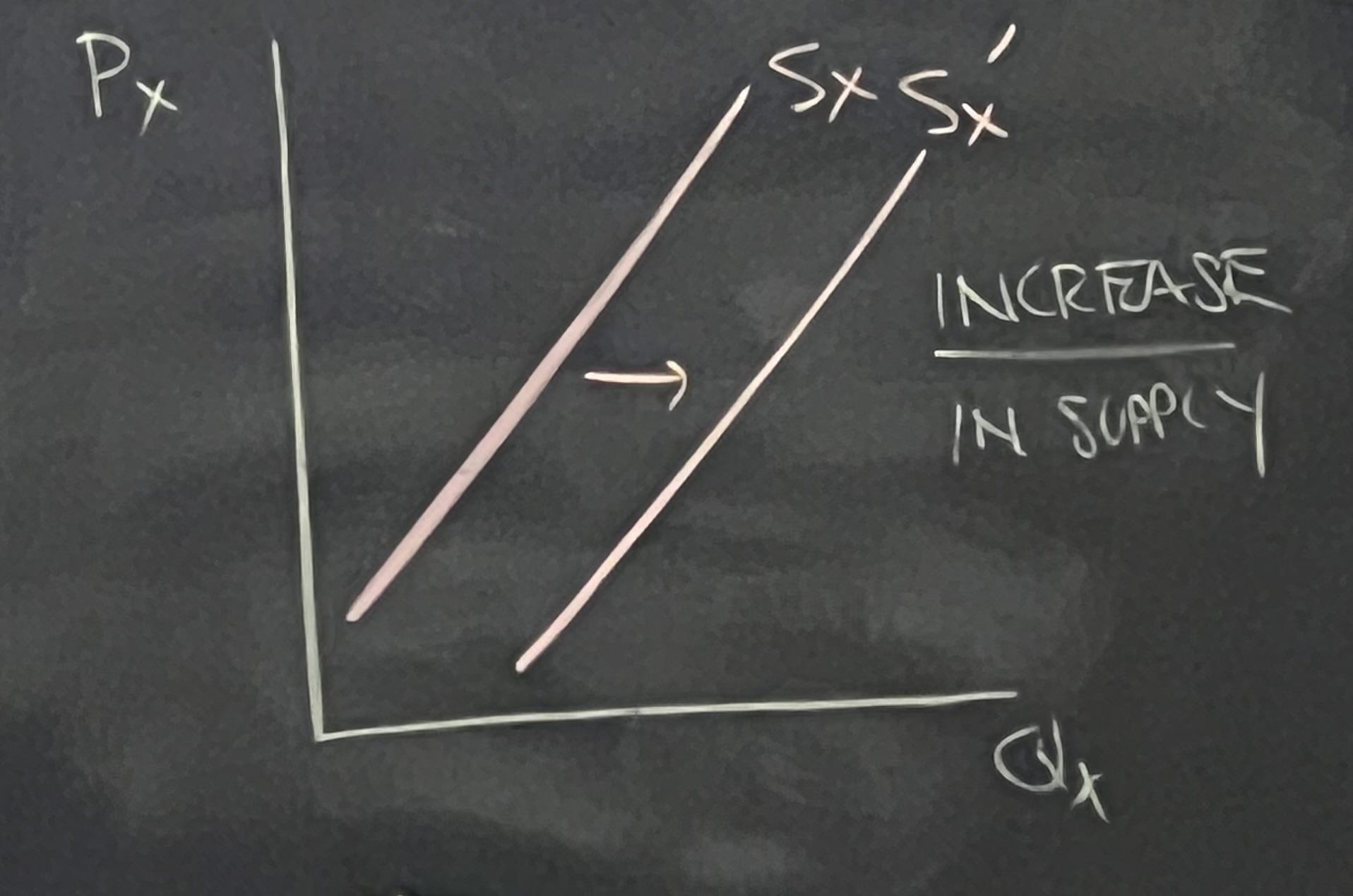

Change in Supply

- Result from a change in PR, TECH, EXP, N, or PZ

- Shift of entire supply curve

An increase in Supply May Be Caused By:

- A decrease in resource prices

- An increase in technology

- An increase in business expectations

- An increase in the number of firms

- A decrease in the price of related goods

How Market Works

How do markets allocate resources in an economy?

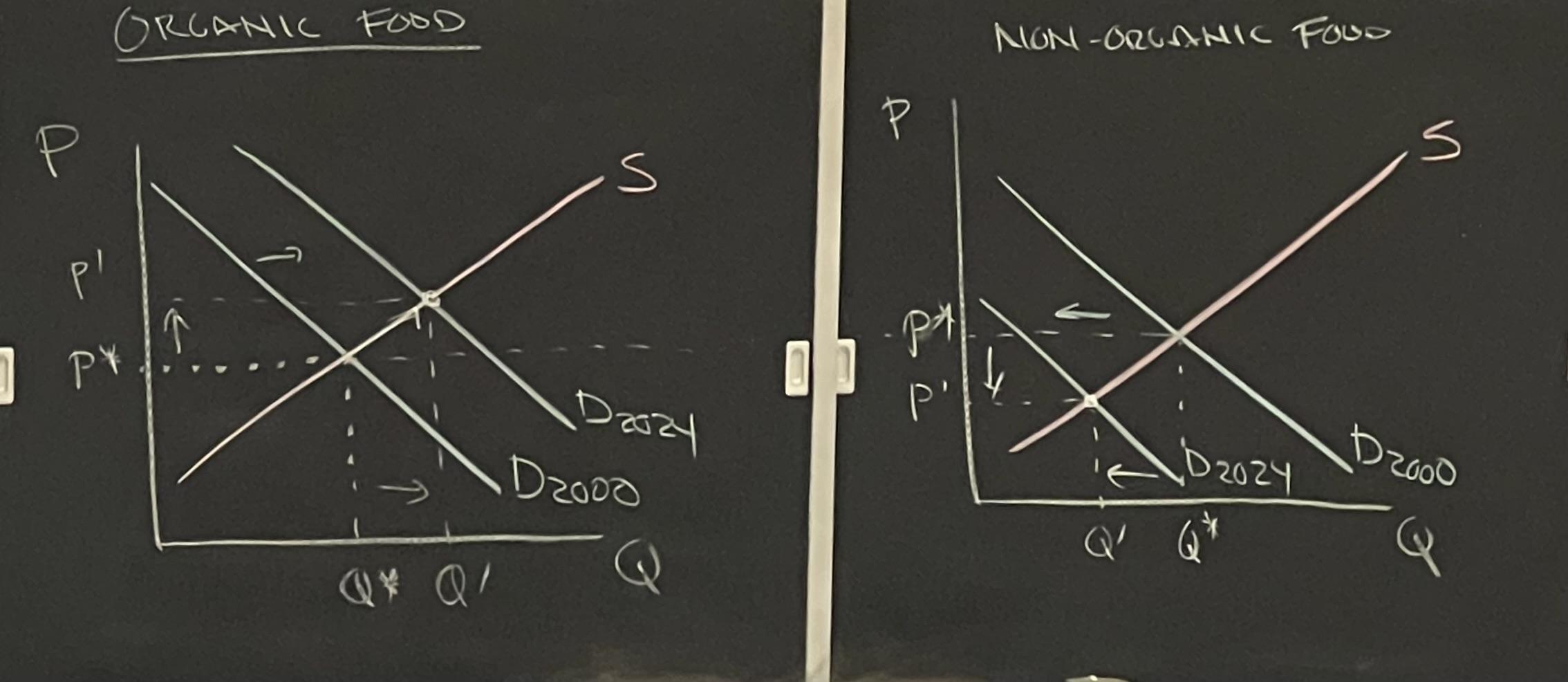

- Two Markets:

- Organic Food

- Non-Organic Food

Organic Equivalency Agreement of 2012

Consumer Sovereignty

Markets respond to change in consumer preferences

Resource allocation

Prices and profits act as signals to firms to produce more where prices + profits are rising and less where prices and profits are falling

Adam Smith : The Wealth of Nations (1776)

- Self interest

- Invisible Hand

- Division of labor + specialization

Four Fundamental Economic Questions

- What + How much to produce?

- How to produce?

- For whom to produce?

- When to consume?

Types of Economic Systems

- Traditional Economics

- Economic decisions are based on what was done in the past

- Command & Control (Central Planning)

- Economic decisions are made by government bureaucrats

- Market Economy

- Economic decisions are decentralized through the price system (capitalism)

If markets work so well, why do we need a government?

- Economic rationale for the existence of government

Necessary Conditions for the Existence of Markets

- Establish Property Rights

- Maintain Law + Order

- Enforce Contracts

Market Failure

- Markets may not always allocate resources efficiently

- Monopoly Power

- A monopolist man restrict output to charge higher prices

- Information Asymmetries

- Parties to a trade may lack information in markets

Adverse Selection

- Occurs before transaction

- When a market lacks information about the quality of products, then that market is dominated by lower quality products

Moral Hazard

- Occurs after transaction

- Incentives change when costs can be passed on to third parties

Externalities

- Costs of benefits that accrue to individuals not directly involved in the transaction

- Negative externalities → impose cost on others

- Positive externalities → provide benefits to others

Public Goods

- Non-Rival

- Non-Excludable

- Free-Rider Problem

Government Failure

- Political Influence

- Myopia

- Voting Paradox

- Price Controls

- Taxes

- Illegal Markets

Overview of Macroeconomics

- Macroeconomics - the study of the relationship between aggregate economic variables, and the choices made by policymakers to influence these variables

Macroeconomics Goals

- Full Employment & Stabilization Act of 1946

- Stable GDP Growth

- High Employment (Low Unemployment)

- Humphrey Hawkins Act of 1978

- Stable Prices

Macroeconomics Variables

- Outputs

- Gross Domestic Product (GDP)

- Normal GDP

- Real GDP

- Gross Natural Product

- Price Level

- GDP price deflator

- Personal Consumption Expenditure (PCE) Price Index

- Consumer Price Index (CPI)

- Producer Price Index (PPI)

- Labor Maker Condition

- Non Farm Payroll Employment

- Unemployment Rate

- Job Opening & Labor Turnover Survey (JOLTS)

- Initial Jobless Claims

- Financial Markets

- Quantity of Money

- Interest Rates

- Stock Prices

- Bond Prices

- International Trade

- Exchange Rates

- Balance of Payment Accounts

- Business Cycles

- Index of Leading Economic Indicators

- Consumer Confidence

- Business Sentiment

Macroeconomic Models

- The Classical Model

- The Keynesian Model

- Aggregate Demand/ Aggregate Supply Model

Macroeconomic Policies

- Fiscal Policy

- Changes in Government Spending and Taxes

- President & Congress

- Monetary Policy

- Changes in Money Supply and Interest Rate

- Federal Reserve System