5.6 - Production Planning

Local and Global Supply Chain Process

Managing relations w/ all the other partners involved in the production process is known as supply chain management

Managing a supply chain involves:

Deciding what to produce yourself and what to buy from others

Choosing which suppliers to work with

Setting out the terms and conditions of the supplier relationships like penalty clauses for any delays

Deciding on the assurances from the suppliers on the operations

A business who wants to protect its brand + image has to be careful who it’s buying from

Deciding how much direct involvement to have w/ suppliers

Deciding on how centralized purchasing should be, like should all offices have to buy their supplies from a certain company or does it not matter

The Value of Managing the Supply Chain Process Effectively

Management of the supply chain will affect:

The extent to which suppliers meet the requirements of the business reliably

Costs of the business

Ability of the business to be flexible to customer requirements

Quality of supplies

Consumers’ perception of the ethics of the business

Sometimes, businesses will take control of their supply chain process by owning more of the stages in it

Vertical integration

Changing Supply Chain Process

Managers looking for the best value for money may be using suppliers thousands of miles away, and their suppliers will also be global

This can make the supply chain complex, in tracking who is involved

Tech developments are also changing the nature of the supply chain in certain industries

Customers can now access more products straight from the provider w/o many intermediaries

Managing supply chain has become more important since customers want to know how their products are being produced

Bc of this managers should be able to track back more of their supplies

An ethical business needs to be wary of their supply chain

Local vs Global Procurement

Some companies now choose to procure their supplies locally rather than globally

When procuring locally a business looks for supplier in the country of the operating borders instead of getting it from another company

Some businesses build a competitive advantage through promoting their locally sourced goods to attract consumers who are concerned either ab the carbon footprint associated w/ goods transported over long distances

Difference Between JIT and Just-in-Case (JIC)

A key aspect of operations management involves managing stocks

Depending on the business + conditions it faces, it might be beneficial to hold large amounts of stock, or it might be better to get deliveries of resources shortly before they’re needed

JIT Production

The principle of placing smaller, regular orders for resources, which are delivered just in time for them to be used

This reduces storage costs + waste

This method has been challenged through a variety of ‘supply shocks’ in the global supply chain

Including international trade wars, and COVID

Benefits of JIT | Limitations of JIT |

|---|---|

Improved cash flow and reduces costs - businesses can reduce costs by reducing their inventory, and can use the money for other operations | Reduced economies of scale - businesses will make smaller orders, reducing purchasing economies of scale |

Improved operations - employees know they need to be careful in operations since there’s no spare stock | High risk - production can halt if a small part of the supply chain breaks down, and any delivery delay is bad |

Increased capacity - w/ less storage space needed for stock, more space can be allocated to production | Reduced resilience - businesses may be unable to adapt to changes in the internal or external environment |

JIT needs:

Good supplier relationship

Reliable employees

A flexible workforce

JIC Production

Buffer stocks are additional quantities of inventory kept by a company in case of need

JIC stock control involves holding relatively large levels of buffer stocks so a business can keep operating when faced w/ unforseen events

This results in higher storage costs, but makes the business more resilient to disruptions

Benefits of JIC | Limitations of JIC |

|---|---|

Resilience - production can keep going for a time even w/ disruptions to supply chains | Less working capital - purchasing large quanitites of stock reduces liquidity, so less cash is available for operations |

Economies of scale - the business can order larger quantities of supples resulting in lower costs thru purchasing economies of scale | Higher storage costs - holding large quantities of stock is costly bc of space needs |

Less risk - business is less exposed to changes in the external environment like increases in resource costs | Waste - business may not be able to use all the large quantities of stock it purchased, leaving wasted resources |

Stock Control Charts

Easy way to monitor and analyse stock levels + better control costs

Records when stocks are delivered and when they’re sold, and it can then be used to make decisions ab when to order new stocks and in what quantities

Contains:

Max stock level: The total amount of inventory a company wants to hold

Buffer stock level: Stock held just in case there is an unexpected order or late delivery

Lead time: Time it takes a supplier to fulfil an order; the difference between when an order is placed and when it’s delivered

Reorder level: The point when new stock is ordered from a supplier

Reorder quantity: Amount of stock ordered from a suppliers

Operations Calculations

Operations managers need tools to track the performance of their departments

Productivity Rate

Measures the average efficiency of production and is expressed as a ratio of output to inputs in the production process

Formula is:

Total output/total input X 100

Labour Productivity

Measures the output per worker over a defined period of time

Formula is:

Total output/number of employees

Capital Productivity

Measures how efficiently a business utilizes its capital to generate output

The higher the capital productivity rate, the mroe efficient a business is at utilizing its fixed assets

Formula is:

Total output/capital input

Defect Rate

There’s a risk that pushing workers and capital to produce more can cause more mistakes, called product defects

Defect rate is the percentage of output that doesn’t meet expected quality standards

Formula is:

Defects/output tested X 100

Capacity Utilisation

Important for fixed costs

The percentage of a company’s total capacity that is currently being used

When these rates are higher, the average fixed costs will fall bc they’ll be divided by a larger output

Formula:

Actual output/productivity capacity X 100

Capacity = total ouput a company can produce using its current resources

High capacity utilisation means a company is using its resources efficiently, and should reduce average costs + increase profits

Downside is that workers/machines will be working flat out. raising stress levels of staff

Drop in quality

Costs to buy and Costs to make

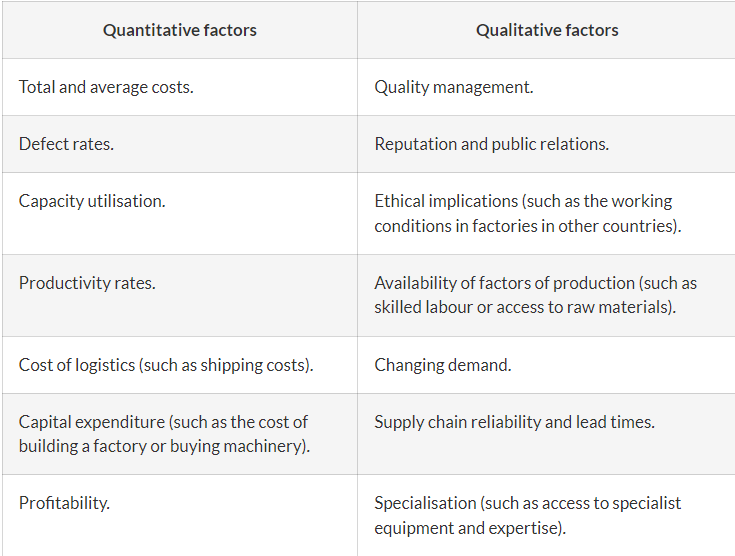

Many quantitative and qualitative factors are considered when deciding whether to make or buy the products they sell

Businesses can calculate how much it’d cost to make the product inhouse and compare that to the cost of outsourcing production

Cost to make

The total cost of production if manufacturing is kept inhouse

Formula:

(Average variable costs x quantity) + fixed costs

Cost to buy

The total cost of subcontracting production to a supplier

Formula:

Price x quantity

Reasons to make

Quality and cost control thru vertical integration

More control over quality and costs

Protecting intellectual property

Meeting global and local responsibilities

Reasons to buy

Specialisation and expertise

Low costs bc of economies of scale

Lower fixed costs