Banking and Money Creation - Section 5, Module 25

bank deposits are a large part of money supply

bank = financial intermediary that uses bank deposits [liquid assets] to finance borrowers’ investments in illiquid assets such as businesses/homes

banks cant lend out ALL their funds bc they need to be able to satisfy a depositor’s request to withdraw

need to keep large amounts of liquid assets on hand → either in the banks valus or in the deposits in the bank’s account in the federal reserve

federal reserve account can be converted to currency ± easily

bank reserves - currency in bank vauls and bank deposits held at the federal reserve → not a part of currency in circulation bc they are in vaults and not held by the public

T-account = helps analyze a banks financial position → summarizes a bank’s financial position by showing the banks assets/liabilties in a single table

owner’s equity = assets - liabilities → shows owner’s financial investment in the business

assets of banks HAVE to be larger than liabilities

reserve ratio - the fraction of bank deposits that a bank holds as reserves

required reserve ratio - the smallest fraction of bank deposits that a bank must hold

bank run - in which many of a bank’s depositors try to withdraw their duns due to fears of a bank failure → the reason why banks have a reserve ration

bank loans are illiquid

bank regulation: system put into place after GD w/ 3 features → deposit insurance, capital requirements, and reserve requirements + discount window

deposit insurance - guarantee provided by FDIC that depositors will be paid even if the banks can’t come up w the funds up to a maximum amount per account

→ doesnt protect JUST the depositors but also elimates one of the main reasons for bank runs → people KNOW they will get their money back so they won’t panic

however, it incentives risky behavior bc depositors will not be checking [since they are protected] and owners are more likely to engage in overly risky investment behavior bc they will profit but if smth goes wrong than govt will cover it

capital requirements - owners of banks have to hold more assets than the value of their bank deposits → to reduce the inventive for excessive risk taking

bank’s capital - excess of a bank’s assets over its bank deposits and other liabilities

capital must be ≥ 7% of its asset’s value

reserve requirement - rules set by the FED that detemrine the required reserve ratio for banks

discount window - the channel through which a bank can borrow the FEDs money from → this way even in a bank run bank doesn’t have to sell off assets to satisfy depositors, it can j borrow money from FED

banks change money supply: decr money supply [when money is sitting in the bank vault instead of w ppl] and incr money supply [thru loans]

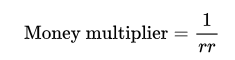

money multiplier!!

however, not all funds that banks lend out end up being deposited → some get saved → leaks in banking system that reduce the money multiplier

excess reserves - bank’s reserves above its required reserves → gets lent out

if the complication of borrowers saving part of their loan as currency is ignored, then:

monetary base - the sum of currency in circulation and the reserves held by banks → controled by federal reserve

diff from money supply bc bank reserves is included in MB, but checkable bank deposits [which ARE a part of MS aren’t included in MB]

money multiplier - the ratio of the money supply to the monetary base

tells the total number of dollars created in the banking system by adding $1 to the MB