BAR Summary

B1

Supply and Demand curve: supply goes up with quantity & price, demand goes down with price.

:max_bytes(150000):strip_icc()/ChangeInDemand2-bd35cddf1c084aa781398d1af6a6d754.png)

B2

M1 - Capital Structure (CS)

debt vs equity, how company funds itself

WACC - Weighted Average Cost of Capital

LOWEST WACC = BEST Value for firm & best CS

WACC Formula: (A)* (B) *(C)

A. ((Cost of Stock %) * Proportion of CS that is Stock )

B. ((Cost of Preferred Stock%) * Proportion of CS that is Preferred Stock )

C. ((Cost of Debt %) * Proportion of CS that is Debt)

Cost of Retained Earnings

How much a firm should grow to keep stockholders happy (otherwise stockholders = mad and take money away)

Market risk premium = market return rate - risk free rate

3 Methods to calculate “Expected Return of Investment” (for investor) or “Cost of Retained Earnings” (for company):

#1. CAPM - Capital asset pricing model

Cost of equity = Risk-free rate + Beta * Market Risk Premium

Beta of investments = % change in price / % change in market

:max_bytes(150000):strip_icc()/dotdash_INV_final_Calculating_CAPM_in_Excel_Know_the_Formula_Jan_2021-01-547b1f61b3ae45d7a4908a551c7e7bbd.jpg)

#2. DCF: Discounted Cash Flow

[Cash flow / Market value price per stock] x Growth Rate

#3. BYRP: Bond Yield plus Risk Premium

Market Risk Premium + Pretax cost of long term debt.

Analyzing Capital Structure

Loan covenant - requirements from lenders to secure debt. Positive debt covenants ensure you maintain certain levels or ratios. Negative debt covenants restrict you from doing things.

Retention - Increase in RE / Net Income. AKA- portion of income not paid out in dividends.

Growth Rate - (Return on Assets x Retention) / [1 - (Return on Assets x Retention)]

High Financial leverage - when there’s less owners so existing owners get more profits → less equity + more debt CS = more EBIT to cover interest

Operating Leverage - when company has less variable costs → higher contribution margin.

Levered firm - company that has debt in its CS. unlevered = all equity no debt. levered firm can deduct interest on debt from taxes = good.

M2 - Working Capital

How businesses use cash, collect cash, and manage payments to get the most return on capital.

Net working capital = current liabilities - current assets

AR Management

Factoring - a company gives you a % of your AR $$ now in exchange for a fee and interest payments. You get benefit of money now instead of waiting and less administrative work. Con = expensive.

Inventory Management

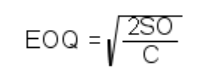

Reorder point = safety stock + (sales during lead time)

Economic Order Quantity = SQUARE ROOT of [(2 * Annual Sales * Cost to place each order)/ Annual carrying cost per unit]

Make sure that the time measure (like annual/quarterly/weekly all match up).

Order size gets larger as "S" or "O" gets bigger (numerator) or as "C" gets smaller (denominator).

EOQ | = | Order size |

S | = | Annual Sales quantity in units |

O | = | Cost per purchase Order |

C | = | Annual cost of Carrying one unit in stock for one year |

SCOR - Supply Chain Operations Reference Model. Plan, Source, Make, Deliver.

3 types of Inventory Management Issues:

Just in time - order gets placed → manufacture starts → gets to customer = less lag & more efficient

JIT is a pull-through inventory system, as the customer's order drives the need for inventory.

Push systems begin with forecasting customer demand.

Kanban - “hit me over the head with a can” → OOPS we ran out = order more.

Computerized - computer tells when to order more when stock is running low.

AP Management

Annual Cost of NOT taking a cash payment discount =

Effective Interest on Missed Discount Rate x Cycles of days of delayed payment per year

another way to look at it is…

[Forgone discount % / (100% - Foregone Discount %)] x [360 / (Pay period - Discount period)]

Short-term financing - debt that matures <1 yr

Pros: faster conversion of operating cycle, lower interest rates.

Cons: higher interest rate risk from fluctuating market/economy, credit worthiness can be affected impacting future funding for capital.

Long-term financing - debt that matures >1 yr. pros and cons are opposite of short term financing.

M3 - Valuation

Methods to value stocks & equity

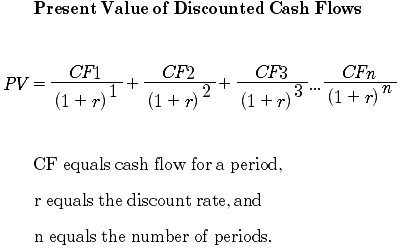

Absolute Value Models: Assigns an intrinsic value to an investment by calculating the PV of the cash flow.

Relative Valuation Model: Uses price multiples, (financial ratios) to determine if the stock is undervalued, fairly valued, or overvalued.

Types of absolute value calculations:

Annuities: same cash flow each period for certain time period.

Annuity Due = beginning of period

Ordinary annuity = end of period

Perpetuities (aka Zero Growth Stock): same cash flow forever = like a dividend.

Present value of a perpetuity = the stock price.

Stock price = Dividends / Required Rate of Return %

Constant (Gordon) Growth Dividend Discount Model (DDM): assumes dividend will grow at same rate every year.

Present value (aka: price at specified period)

Get the required rate of return from the CAPM

higher dividends → higher value

Discounted Cash Flow Analysis:

Dividend discount model (DDM) - expected dividends = basis for PV of future CF

Free cash flow model (FCFF) - available cash after covering working capital needs = basis for PV of future CF

Types of relative valuation calculations:

Price Earnings (P/E) Ratio = Stock Price / Earnings per Share for 1 Fiscal Year

PE Ratio x Earnings for 1 year = Current stock price

Forward vs Trailing P/E Ratio:

Forward = future earnings & future EPS.

Trailing = past earnings & past EPS

high P/E → growth expectations

low P/E → undervalued or risky

PEG Ratio: P/E/G → the lower the better

Price-to-Sales Ratio: more stables than PE Ratios

Price-to-Cash-Flow Ratio: price per share / cash flow per common shares outstanding

A metric showing how much the market pays for each $1 of projected cash flow. A P/CF of 15 means each $1 of next year’s cash flow is valued at 15 times.

Price-to-Book Ratio: price per share / common stockholders’ equity per common shares outstanding

Options

Option: contract where a person can buy or sell a stock (or other asset) at a specific price within a certain period of time. American option → exercised any time. European option → exercised at maturity.

Buy → call option (the stock sings: “call me maybe!”)

Sell → put option (the stock says: “put me down!”)

The Black-Scholes Model: option value now; price, time, volatility, interest rate. Assumes a constant risk-free interest rate over the option's term in the calculation

Binomial (Cox-Ross-Rubinstein) Model: option value over time; price, steps, up/down, probabilities

Debt

Bonds pay interest (coupons) each period

Then return principal at the end

To calculate price of a bond:

Discount each coupon payment

Discount the final principal

Add them all up

Fair Value

Hierarchy of inputs: ranking of valuation inputs by reliability (Level 1–3).

Level 1 = quoted price for item.

Level 2 = comparable item’s price.

Level 3 = estimates, not observable price.

Fair value measurement: if principal market exists (market where most units is sold), then FV = value in principal market. if no principal market, then FV = most advantageous.

Market, income, cost approach: ways to value asset.

Market = comparables

Income = present value cash flows

Cost= replacement cost

M4 - Financial Decision Models

Cash Flows: Direct = actual cash; Indirect = adjusts NI → cash; both → same net CF

Asset Disposal: Sell old asset → gain/loss affects taxes → impacts CF → use after-tax proceeds = SP – tax on gain

Depreciation: non-cash but saves taxes → tax shield = Dep × tax rate → treat as cash inflow

NPV steps: PV cash savings/inflows = PV net cash outflows

Initial Investment (first yr when buying t=0): purchase + install + WC → always negative

Operating CF: savings/revenues are taxable → use after-tax CF = inflow × (1 – tax rate)

Salvage value: after tax gain/loss from last yr

NPV: Initial investment (which is negative) - PV inflows → NPV > 0 accept, < 0 reject

Ask:

👉 “Is this ONE payment or MANY?”Pick:

one payment → “PV of $1”

many → annuity

THEN multiply

Discounting: PV factor = FV / (1+r)^n; time=0 = no discount

Profitability Index: PI = PV inflows / initial → >1 accept

IRR (internal rate of return): rate where NPV = 0 → IRR > hurdle → accept

tells us “related interest rate”

Payback method: initial investment / annual CF → liquidity focus, ignores time value

Discounted Payback (BET): same but uses PV

EVA (economic value added): after-tax income (excluding interest expense) – (Required return)

Required return = Investment * WACC.

positive = accept

M5 - Marginal Analysis

Marginal analysis = only include costs/revenues that change; ignore sunk costs, include opportunity costs.

Opportunity cost is the potential benefit lost by selecting a particular course of action. If the land is developed rather than sold, the potential selling price foregone is an opportunity cost.

the next best use of productive capacity.

Sunk costs are costs incurred in the past that will not change as a result of any decision made in the future. These costs are considered irrelevant in marginal analysis decisions because they do not change.

Special order: if extra capacity → accept if price > variable cost; if full → include opportunity cost.

Make vs buy: choose lower relevant (avoidable) cost.

Sell or process further: process if incremental revenue > incremental cost.

Keep or drop: keep if lost contribution margin > avoidable fixed costs.

B3

M1 - Cost Accounting

Prime cost = Direct materials + Direct labor

Conversion cost = Direct labor + Manufacturing overhead

Overhead cost: all indirect costs to manufacturing a product. there is fixed overhead which is going to be there regardless and there is variable overhead which can increase your indirect costs based on how much you produce.

Relevant range = range where cost behavior assumptions hold

→ Outside it, fixed costs may change and cost formulas break

Job order costing = customized products/projects (each job tracked separately)

Ex: building a custom house

Process costing = mass production (use averages across units)

Ex: making identical bottles of soda

Equivalent units = % complete units expressed as full units

Used to allocate costs between completed units & ending WIP

Ex: 100 units at 50% completion = 50 full units

FIFO vs Weighted Avg

FIFO = current period costs only. Ex: only this year’s production costs

WA = mix of beginning + current costs. Ex: blends last year’s + this year’s (like mixing batches)

ABC (Activity-Based Costing)

Allocates overhead based on actual activities (cost drivers)

More accurate than traditional because it matches cost → cause

Ex: if product uses more machine setups → gets more overhead

Direct vs Step-down (support allocation)

Direct = ignores support-to-support services

Ex: HR costs production only (ignores any IT costs helping HR)

Step-down = partially accounts (one-way allocation)

Ex: IT → HR → production (one direction)

Joint product costing

Costs incurred before split-off point

Allocate joint costs based on relative sales value (usually)