Price Elasticity

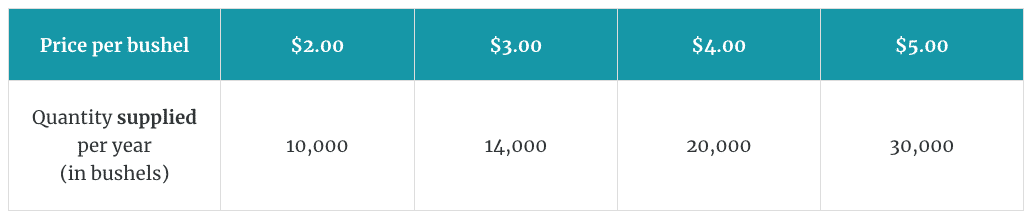

In the last few lessons, you may have noticed that the quantity supplied and quantity demanded for corn reacted differently to changes in price. For example, when the price went from $4.00 to $5.00, the quantity supplied went up by 10,000 bushels; but the quantity demanded only went down by 7,000 (see the supply and demand schedules below).

Elasticity is the degree to which buyers and sellers respond to price changes. In this scenario, the sellers responded more aggressively to the price change than the buyers did. The price elasticity of demand and the price elasticity of supply are usually analyzed separately.

Price Elasticity of Demand

Price elasticity of demand measures the change in quantity demanded relative to the change in price. The more elastic the demand, the more responsive consumers are to price changes. If the quantity demanded for pizza went down 20 percent when the price went up 10 percent, we would say that demand for pizza is very elastic. Notice in the following demand schedule that the quantity demanded decreases 20 percent for every 10 percent that the price increases.

Price elastic demand often occurs with luxury products or products that have good substitutes. If the price of pizza gets too high, consumers can easily start eating a different type of food.

Price inelastic demand means that consumers are not that responsive to price changes. For example, if the price went up 10 percent and the quantity demanded only went down 2 percent, then demand would be considered inelastic. This might occur for products that are necessities, such as electricity. Other products might have inelastic demand because they have no good substitutes or are very cheap.

Price Elasticity of Supply

As you can probably guess, price elasticity of supply measures the change in quantity supplied relative to the change in price. Price elasticity of supply is determined by three main components: the availability of raw materials for production, available production capacity, and the time period required to produce more of the product.

1. Availability of raw materials for production

2. Available production capacity

3. Time period required to produce more of the product

Tickets to a concert, for instance, would have a very inelastic supply. There are only so many seats in the stadium. The only way to increase the number of tickets available would be to build a bigger stadium—a very time-consuming and expensive process. On the other hand, the supply of lawn mowing service is elastic. At a higher price, more people are willing to provide the service, and it's easy for more people to get into that business—it's relatively quick and inexpensive to buy a lawnmower and start mowing lawns.

"How the Price System Works"

Your final task for this lesson will be to read a chapter of Economics in One Lesson: Chapter 15: "How the Price System Works." Hazlitt will discuss several of the concepts you've learned over the last few lessons, focusing on the supply-and-demand price system. Pay particular attention to Hazlitt's description of the problem of alternative applications of labor and capital, and how that problem is solved.

Americans can choose from over a hundred million different products on Amazon alone, and there are many other options available from retailers like Walmart, grocery stores like Kroger, or local businesses like farmers' markets. The entire economy's factors of production (natural, human, and capital resources and entrepreneurship) must be split between all these different products. How in the world do producers decide how to allocate their resources? It seems like an impossible task! But, as Hazlitt writes, "It is solved precisely through the price system, . . . through the constantly changing interrelationships of costs of production, prices, and profits."

Review of Key Terms

elasticity: the degree to which buyers and sellers respond to price changes

price elasticity of demand: the change in quantity demanded relative to the change in price

price elasticity of supply: the change in quantity supplied relative to the change in price

No governmental system of bureaucrats has ever done as good a job of allocating resources as the supply-and-demand price system. Over the next two lessons, we'll learn about some of the consequences that occur when governments manipulate prices through price ceilings and price floors.