The Banking System

Fractional Reserve banking

It is made up of mainly financial intermediaries they collect the savings of the economy and give to the borrowers.

Households deliver the savings while governments and businesses seek loans for investment and consumption, creating a cycle of money circulation that supports economic growth.

A bank’s balance sheet has assets on one side and liabilities and net worth on the other.

assets is something it owns and liability is something it owes, while net worth is assets - liabilities.

Customer deposits are a liability

a bank’s deposit at the federal reserve is an asset

Banks only keep a fraction (about 10%) of customer deposits as reserves, allowing them to lend out the majority of these funds to generate profit. This is fractional reserve banking.

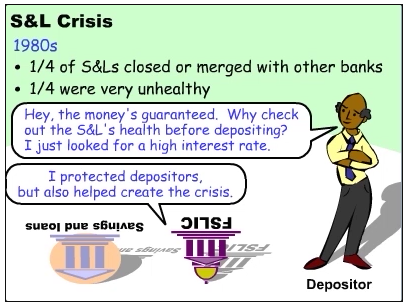

This all relies on trust, if people lose trust in their bank, a bank run occurs: many depositors ask for their money, but the bank does not have enough assets om hand

The federal depository Insurance Corporation ensures that if a bank fails, it will give you back up to $100,000

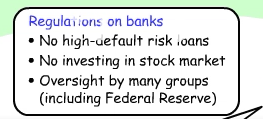

For a bank to run it needs a state or federal charter and abide by regulations like the required reserve ratio: minimum % of total deposits that must be on hand.

bank loans must be repaid as it does not get back the money deposited, so the bank’s net worth is negative

A financially troubled bank is “married“ to a more financially stable bank through a process known as a merger or acquisition, which can help stabilize its operations and restore confidence among depositors.

Federal Reserve

Was to provide money for economic activity, and oversee the health of banks and the economy.

the great depression revealed its flaws, so the federal reserve act was amended in 1933 and 1935

The high inflation of the ‘70s led to the bank deregulation act: required all depository institutions to follow the reserve ratio set by the FED.

Structure of FED

3 branches:

Board of governors: appointed by pres, confirmed by congress, and serve 1 14 year term; 1 chairperson is selected by the pres, confirmed by congress, and serves a repeatable 4-year term. headquarters is in Washington D.C.

District banks: 12, 1 per district, with a district bank pres, and district board of directors per bank

Federal Open Market Committee: 7 members of board of governors, NY Fed district Bank president (permanent member) and 4 other district bank presidents. Chairman of Board is a non-voting member.

Goals of FED

Maintain health of banking industry and economy

Does research on the economy to assess trends, make informed decisions on monetary policy, and ensure stable prices and maximum employment.

Regulates banks to ensure their safety and soundness, protecting consumers and maintaining public confidence in the financial system.

Promotes a stable financial system by providing liquidity to banks during times of crisis and acting as a lender of last resort to prevent systemic failures.

Controls the money supply, thus affecting interest rates and the whole economy

3 types of monetary policy:

Required reserve ratio: changed rarely

discount rate: is what FED charges a bank for an overnight loan; very low interest rates, but do not want to trouble the FED, so they borrow from each other.

open market operations: sales and purchases of treasury bonds by the FED.

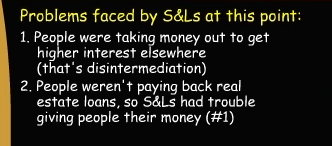

Disintermediation

occurs when people take savings out of financial intermediaries.

Is bad for banks because those savings are removed, so its reserves fall, so it may call for loans to pay it.

A thrift is a savings and loan, or credit union.

both banks and thrifts had this in common: checking accounts couldn’t pay interest, and savings couldn’t pay more than the max set by the fed