2b. Costs

Economic cost

Economic costs are very specific and are different to accounting costs.

The economic cost of production to a firm includes the opportunity cost of production.

This includes imputed costs such as:

Labour

Financial capital

Economic costs and costs may not be the same as economic costs include opportunity costs as well.

Fixed and variable costs

A fixed cost is a cost that does not change in line with output. For example, rent on a factory must be paid regardless of whether one item is produced or a million items are produced. Some fixed costs are also considered ‘sunk costs’. These are costs that can not be retrieved should the firm shut down such as an advertising campaign.

Rent - doesn’t matter if a factory makes 10 or 1000 items the rent stays the same

Variable costs do change in line with production. These are items like materials. The more products are made, the more materials will be needed to make them.

TC = TVC + TFC

Average costs of production

The AC is the total cost divided by the level of output.

AC = TC / Q

The same principle applies to AVC and AFC

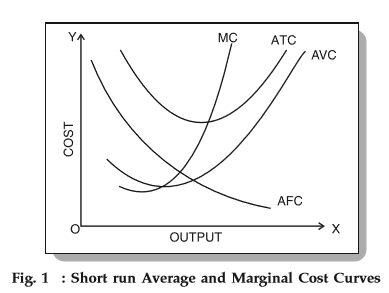

Marginal costs of production

The MC is the cost of producing one more unit. For example, if it costs £100 to produce 10 items and £105 to produce 11. The MC is £5

MC = Change in TC / Change in Q

The MC crosses ATC at the lowest possible cost/point of the curve

At the lowest point on the MC is the point of marginal diminishing returns - this makes it a short-run diagram as one variable is fixed

At first, making more lowers the cost

At the point Q and onwards they start increacing

AC and FC are linked

VC and MC are linked ( not exactly but they work when fixing graphs)

Short-Run & Long-Run

In the short run, at least one factor of production is fixed

i.e. there is a limited amount of workers, machines or raw materials

In the long run, all factors of production are variable

i.e. more workers will immigrate, more machines will be built, raw materials can be mined for

This means all costs are variable in the LR

Law of Diminishing Returns

If a firm tried to increase production in the short-run, it is often constrained by a fixed factor of production e.g. infrastructure

They can try and compensate by adding in more of other factors of production e.g. labour

However, each unit of additional labour is likely to be less efficient as the last they only have a set number of machines