Lecture 5: Measurement of Financial Statement Elements:

Note: confusion over way slides use “less” e.g. “cost less written cost”

Think less in this case means minus

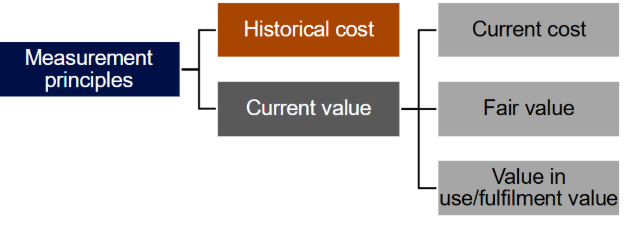

Measurement Bases:

Carrying amount (book value):

Def (BV): $ value assigned to assets & liabilities on balance sheet

Different bases → same/similar valuation (upon initial acquisition); however

Can diverge substantially over time

Historical cost:

Def (HC): cash (or equivalents) paid to acquire asset OR amount of proceeds received in exchange for an obligation (e.g. a liability).

Example:

A McDonald’s purchases a new fryer for $30000, installation costs $1500 and delivery costs $1000.

Carrying amount for fryer: 30000 + 1500 + 1000 = $32500

Current Value:

Def (CV): measurement of monetary information about asset, liability, income & expenses using data updated at measurement date.

NOTE: Current value hard to determine in inactive markets (e.g. specific antiques, outdated tech)

Specific Measurement Cases (SMC):

Receivables:

Def: Carrying amount of receivables = expected cash (or equivalents) amount TB received.

i.e., amount owing less an allowance for amounts expected to be uncollectible.

Amount Expected to be Uncollectible: usually called an allowance debt;

Estimated based on objective evidence;

E.g: Customer history, trade pattern changes, third party confirmation of non-collectability, past due status of contractual payments)

Inventory:

Def: Carrying amount of inventory which is the lower value of its cost price and net realisable value.

Cost price: price it costs you to purchase (duh),

→ any of:

→ first-in-first-out (FIFO);

→ weighted avg cost (WAC); or

→ actual cost (where inventory sold is specifically identified)

Net Realisable Value (NRV): expected selling price < expected cost associated w/ getting inventory to sellable state + cost of marketing, selling & distribution

Define inventory carrying amount based on which of these two is smaller

NCA:

Def: carrying amount of NCA w/ limited use life is their cost (or fair value) less accumulated depreciation (or amortisation).

Depreciation & Amortisation: allocation of depreciable amount of depreciable asset over estimated useful life;

This amount recognises future economic benefits of asset which is used up in reporting period

NOTE: Each class of NCA can be carried at either cost, written-down cost or fair value

Cost or written-down cost: must not have carrying amount > recoverable amount (i.e. higher of its expected selling cost less cost of disposal, and its value-in-use);

Fair Value:: need to be remeasured on regular basis; &

→ Any increase/decrease are accounted for either in revaluation surplus; or

→ Through profit/loss statement

Optimal Measurement Base?

Historical vs Current:

Context dependent;

Best = provides most decision-useful information while being reliable;

I.e: relevant (assists in decision making), faithful representation of relevant economic phenomena (objective, neutral);

Trade-offs made in many cases between relevance & reliability

Guiding Questions:

Purpose and business model: Is the asset used in operations, held to generate rentals, traded, or held for sale?

Decision-usefulness: Which measure gives users information they need (predictive/confirmatory)?

Reliability of measurement: Can you measure the base using observable market inputs or only by judgement?

Standard-setting requirements: Which bases does the applicable accounting standard permit or require?

Cost and complexity: Is it practical and cost-effective for the entity to obtain the measurement regularly?

Consistency: Is the selected policy applied consistently to the relevant class of assets and clearly disclosed?

Lecture Practice:

Premise:

A four-storey city building exists in a good commercial location. Four different businesses are looking to acquire it and will be using it differently. Identify the measurement base that each business would use to value the building in its financial statements.

Business 1:

Manufacturing firm, who will use all floors for offices and light production support.

Current Value likely more helpful since firm will be using building over an extended period of time for operations.

Correct answer: Historical cost less depreciation

Depreciation reflects business usage/consumption & historical cost shows original value;

Since business intends to use over a long time, depreciation helps ascertain use value;

Less relevant to current reporting period but relevant to periodic consumption over time;

Faithful representation which is also verifiable

Business 2:

Correct Answer: Fair Value

Market movements matter for investor; so

Up to date values are useful for decision making;

High relevance: reflects current market conditions nd value to users;

Moderate faithful representation;

When observable market price exists, representation is reliable; but

Where estimates are used, there is more judgement and therefore potential measurement error

(guessed for this one and lucked out);

Business 3:

Lower of cost and net receivable value since business needs up to date information and is planning to sell in near future w/o need for operating cash flows.

Correct

Reasoning:

Asset is essentially inventory, appropriate measurement base is its expected sale value to business;

High relevance: bc it aligns w/ economic purpose of holding asset;

Faithful representation depends on how well NRV is estimated;

If cost side is more verifiable, NRV requires judgement

Business 4:

Historical cost. No plan to sell or derive significant revenue from operating cash flows. Hence all buyers care about is the value of the site itself. Highly relevant since base aligns w/ purpose. Moderately faithful as the value of the land may change in future.

Correct.

Reasoning:

Depreciation not accounted for since building is for public use + preservation;

Users care about stewardship and service potential rather than market price;

Relevance is about service potential rather than market value and cost shows resources used;

High faithful representation for stewardship purposes as cost is verifiable

Judgement/choice associated w/ measurement:

Preparation of Financial Statements involves choices, assumptions & estimations;

Bc measurement choices exist, companies should disclose measurement bases in accounting policy notes;

Same asset and liability classes generally use same measurement bases;

Financial statement users must be aware of measurement bases employed when making inter/intra-entity comparisons;

Differences in asset values arising from changes in purchasing power of money (e.g. inflation) not taken into account; even

When single measurement system is used (e.g. historical cost)