C3: INTRODUCTION TO FINANCIAL TECHNOLLOGY (FINtech)

What is Fintech

Fintech (short for financial technology) uses technology to improve and automate financial services, making banking, investing, payments, and money management faster and more convenient.

Fintech is a broad category that includes various technologies, aiming to change how consumers and businesses access finances and compete with traditional financial services.

Fintech companies offer a range of products and services that use technology to improve financial efficiency and accessibility for consumers and businesses.

TYPES OF FINTECH

1. Mobile Wallets & Payment Apps

These apps let users make payments, transfer money, and pay bills instantly without cash or cards.

Examples:

Touch 'n Go eWallet

GrabPay

Boost

2. Crowdfunding

Platforms that allow individuals or businesses to raise small amounts of money from a large number of people, often for new products or causes.

Examples:

Kickstarter

GoFundMe

Indiegogo

3. Cryptocurrency & Blockchain

Cryptocurrencies are digital money (like Bitcoin) that use blockchain technology—a secure, transparent way to record transactions.

Examples:

Bitcoin

Ethereum

Binance

4. Robo-Advisors

Online platforms that use algorithms to provide automated investment advice, often with lower fees than human advisors.

Examples:

StashAway

Wahed Invest

Betterment

5. Stock Trading Apps

These let users buy and sell stocks easily on their phones or computers, often with low or no fees.

Examples:

Rakuten Trade (Malaysia)

eToro

Momo

6. Insurtech

Short for "insurance technology," it refers to digital tools that simplify buying, comparing, or managing insurance policies.

Examples:

PolicyStreet

Bima

Tune Protect

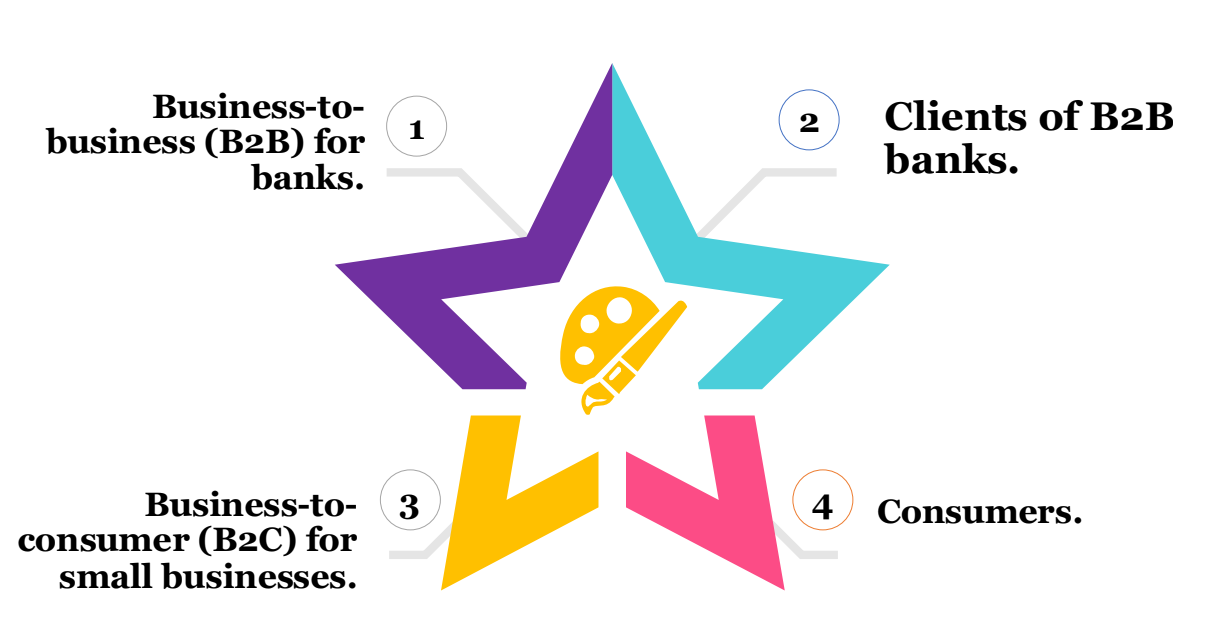

FINTECH USERS

Trends toward mobile banking, increased information, data, and more accurate analytics and decentralization of access will create opportunities for all four groups to interact in heretofore unprecedented ways.

REGULATION & FINTECH

Financial services are very heavily regulated because they deal with people's money and sensitive data.

Now that fintech companies are growing fast, governments are worried about how to regulate them properly.

When technology is added into finance, it creates new problems:

Sometimes the tech itself causes problems (like security risks).

Sometimes it's because the tech industry moves too fast and ignores traditional financial rules.

Example:

Automation (using machines and software to do tasks) and digitizing data (storing everything online) make fintech companies a target for hackers.

Hackers have attacked credit card companies and banks before, showing how easy it can be to break into digital systems and cause major damage.

If a hack happens, customers worry: Who is responsible? What happens if their personal or financial information gets stolen?

Also, there's a culture clash:

Tech companies often believe in “Move fast and break things” — they like to launch products quickly and fix problems later.

But finance is conservative and cautious because mistakes with money can be very serious.

When tech and finance clash, bad things can happen.

Real-life example:

Zenefits, a startup company, broke California’s insurance laws by letting people who weren't properly licensed sell insurance.

As a result, they got fined heavily:

USD 980,000 fine from the SEC (Securities and Exchange Commission)

USD 7 million fine to California’s Department of Insurance.

In short:

As fintech grows, regulations struggle to keep up. Fintech companies face security risks and legal troubles if they move too fast without following the strict rules of the financial world.

ADVANTAGES OF FINTECH

1. Lower Fees and Better Rates

Fintech companies often charge lower fees than traditional banks and offer better interest rates because they use technology to reduce costs.

Example:

Online banks like Wise (for money transfers) offer cheaper fees than normal banks.

Investment apps like StashAway charge lower management fees than regular investment firms.

2. Lower Thresholds for Investment

Fintech makes investing easier and cheaper, allowing you to start with a small amount of money, not thousands.

Example:

Apps like Wahed Invest or Raiz let you start investing with as little as RM5 or RM10.

3. Lower Thresholds for Loans

Fintech platforms allow people to borrow small amounts easily, without needing to apply for big loans at traditional banks.

Example:

Funding Societies offers small business loans to startups and small businesses that would struggle to get loans from a bank.

4. Ease of Use and Convenience

Fintech services are built to be simple, fast, and available 24/7 through apps and websites — no need to go to a branch!

Example:

Touch ‘n Go eWallet lets you pay bills, transfer money, and shop — all through your phone anytime, anywhere.

CLASSIC CHARACTERISTICS

1. Customer-Centric

Fintech focuses on making services better and easier for customers, giving them what they want fast.

Example:

Revolut offers customers a super simple app for currency exchange and budgeting — all designed for user convenience.

2. Legacy-Free

Fintech companies don’t have old systems like traditional banks, so they can build faster and cheaper with the latest technology.

Example:

Wise (formerly TransferWise) built a new money transfer system without relying on old, slow bank networks.

3. Asset-Light

Fintech firms own fewer physical assets (like branches or ATMs), saving money and focusing on digital services.

Example:

GrabPay provides a payment platform without owning any physical banks or stores.

4. Scalable

Fintech businesses can grow quickly to serve millions of people because digital services can easily handle more users without needing more physical locations.

Example:

ShopeePay grew across Southeast Asia fast by just expanding its app — no need for building new branches.

5. Simple

Fintech apps are designed to be very easy to use, so even people with little tech knowledge can handle their money easily.

Example:

Touch 'n Go eWallet makes it simple to reload, pay bills, or transfer money in just a few clicks.

6. Innovation

Fintech always looks for new and better ways to solve financial problems using technology.

Example:

Bitcoin introduced a completely new type of money — digital and decentralized.

7. Compliance-Light

Fintech firms often start with fewer regulations than traditional banks, allowing them to move faster — but they still need to catch up with rules later.

Example:

Early peer-to-peer lending platforms like Funding Societies grew fast before full regulations caught up with them.