Final Accounts

<<Final Account - accounting document made up of a firm’s trading account, profit and loss account and appropriation account<<

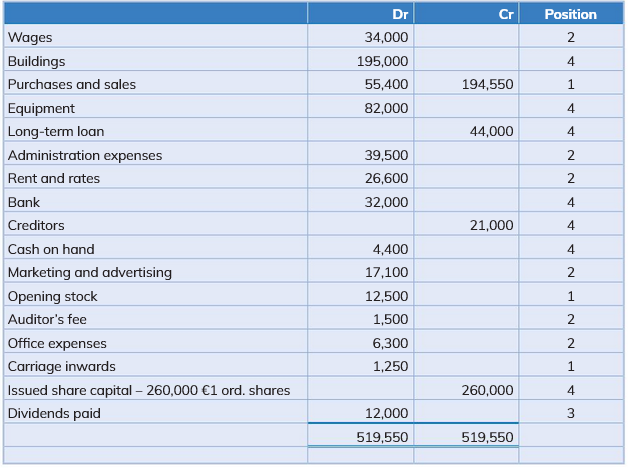

You are given the trial balance. From this you must fill out the trading account, profit and loss account and the appropriation account (income statement) and the statement of financial position.

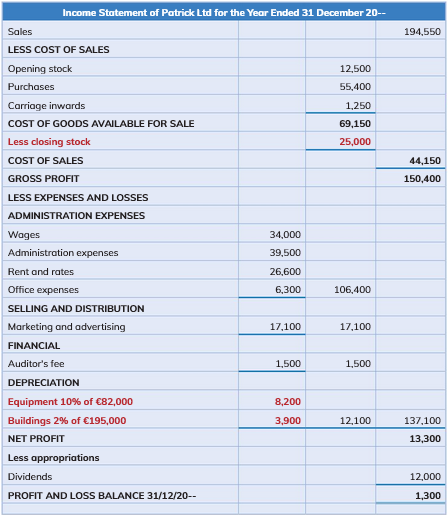

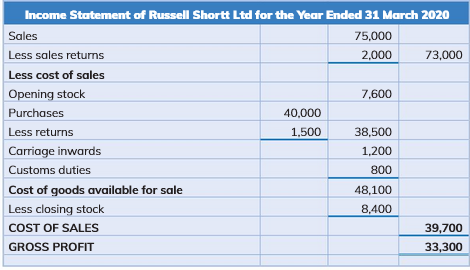

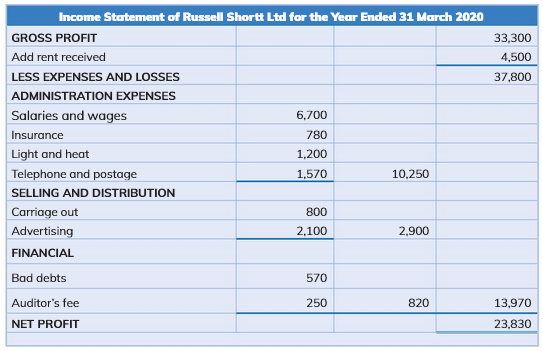

Income Statement

Trading Account - the cost of buying and selling goods. Does not take into account any other factors e.x cost of running premises, therefore only gives you Gross Profit (Loss).

Profit and Loss Account - the cost of running the business, e.x light and heat expenses, subtracted from Gross Profit, therefore gives you Net Profit (Loss) (amount of profit (or loss) the firm actually gets to keep)

Expenses divided under 3 headings:

- Financial - anything to do with banks, debts, auditors

- Selling and Distribution - anything to do with (indirectly) selling or distributing product to customers e.x marketing, repairs to delivery vans etc.

- Administration - everything else to do with running business (especially premises bills) e.x employees wages, light and heating bills, repairs to equipment etc.

These expenses are subtracted from Gross Profit

Not everything is subtracted from the Gross Profit. (Gains - money the firm receives)

ex.

- Rent received

- Interest received (from savings)

- Discounts received (from suppliers)

These gains are added to Gross Profit

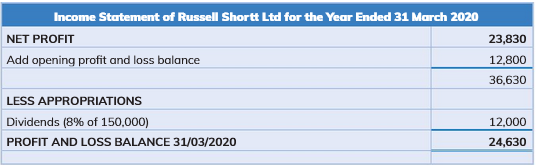

Appropriations Account - Dividends payed to shareholders from profits firm made from trading period.

Gives you Profit and Loss Balance for trading period

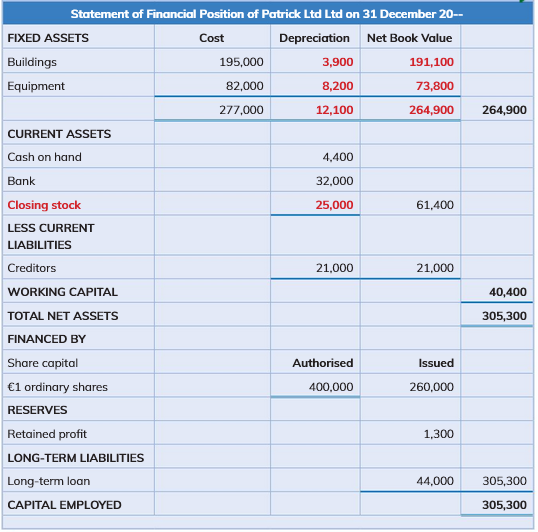

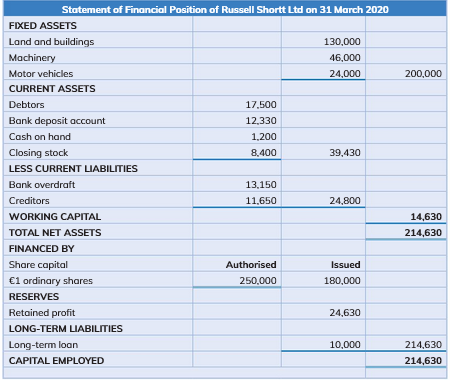

Statement of Financial Position

State of Financial Position - list of the assets, liabilities and capital of a company

Divided into 2 parts:

- Total Net Assets - fixed and current assets and liabilities

- Capital Employed - declares where business got finance for their assets

If done Statement of Financial Position is done correctly the Total Net Assets and Capital Employed should work out to be same number.

Adjustments

Closing Stock - subtract from trading account of income statement (was not sold, therefore not a cost of selling)

- show as current asset in statement of financial position (currently something firm owns that has value)

Depreciation - reduction in value of a fixed asset because of factors e.x age, usage etc.

Final Account