2.5 - interest rate risk management

[2.4 - not examinable]

aim

to critically evaluate the issues and decisions that firms face regarding interest rate risk and its management

learning outcomes

by the end of this unit:

interest rates

definition - the price of money; the most important price in the world

determination - the rate at which demand for loanable funds [borrowing] equates to the supply of loanable funds [savings]

why are interest rates important?

interest rates influence key macroeconomic decisions:

consumption vs. saving - should individuals spend or save?

borrowing now vs. later - should firms/individuals borrow now or defer borrowing?

capital allocation - should firms hold cash, invest in CapEx, or allocate resources elsewhere?

duration decision - should firms borrow or lend short term or long term?

interest rates lie at the core of major financial economic decisions

corporate finance perspective

interest rates impact:

financing decisions:

debt vs. equity [long term financing]

loan, hire purchase, leasing [medium term financing]

cash vs. liquid assets [short term financing]

other financial topics:

investment appraisal - used as discount rates in NPV calculations

capital structure - determines cost of capital and opportunity cost

portfolio theory - defines the risk free rate of return

option pricing - used in calculating risk free return

interest rate risk

a firms financing rate is determined by:

BOE base rate + bank premium + term premium + credit risk premium

BOE base rate - the rate at which banks borrow from the bank of England

bank premium [or discount] - reflects interbank lending conditions, often referenced using SONIA [BOE base rate + bank premium]

term premium - the additional return required for lending over a longer duration, influenced by time value of money, inflation, and uncertainty over future base rates

credit risk premium - compensation for borrower default risk, which is firm-specific

fluctuations in components affect interest rate risk

assets - returns decrease if interest rates fall

liabilities - interest costs increase if rates rise

floating rate assets/liabilities - explicit exposure to interest rate changes

fixed rate asset/liabilities - no explicit risk but implicit risk arises when assets/liabilities are rolled over

short vs. long term borrowing:

short term borrowing = frequent rollovers

long term borrowing = higher term premiums and credit risks

interest rate risk management

interest rate risk management depends on:

forecasts of future interest rates

risk aversion of the firm

balance sheet structure and duration of liabilities

long term rate management = managed through capital structure decisions

short/medium term borrowers:

objective - remove uncertainty

approaches:

fixed rate loans

floating rate loans with hedges [using derivatives]

hedging instruments

forward-forward loans

forward rate agreements [FRA]

interest rate futures [RIF]

interest rate guarantees [IRG]

caps, floors, and collars

interest rate options

interest rate swaps

forward-forward loans

example

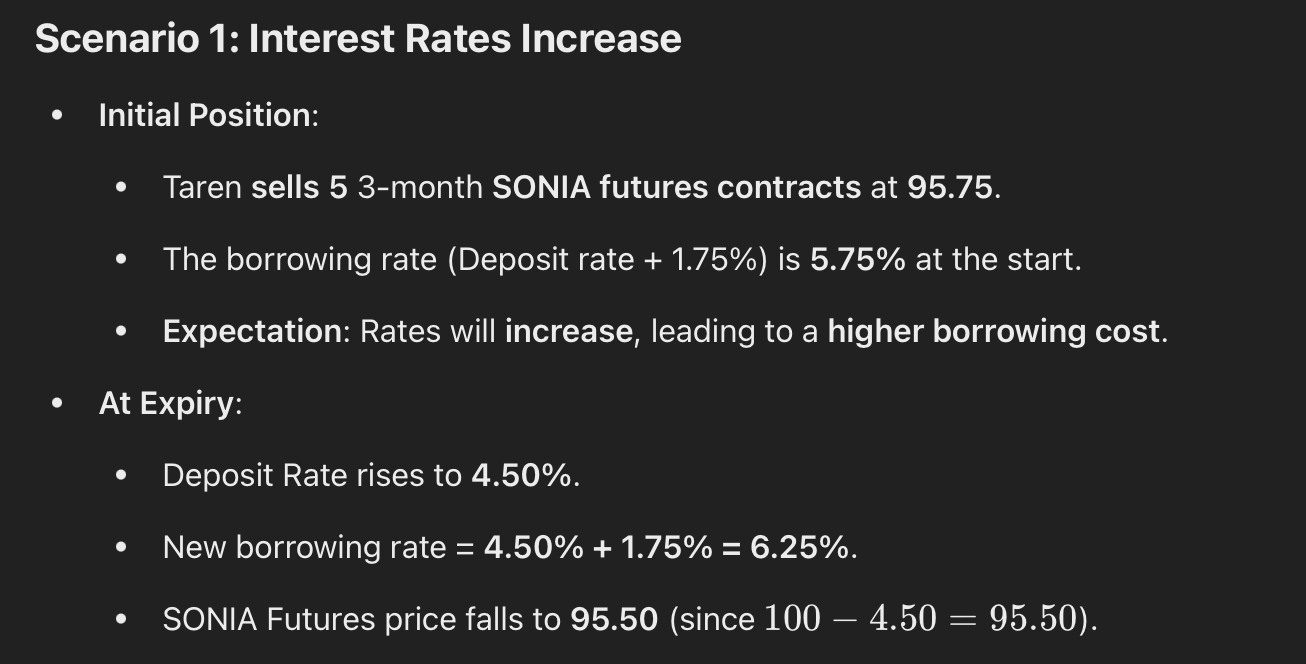

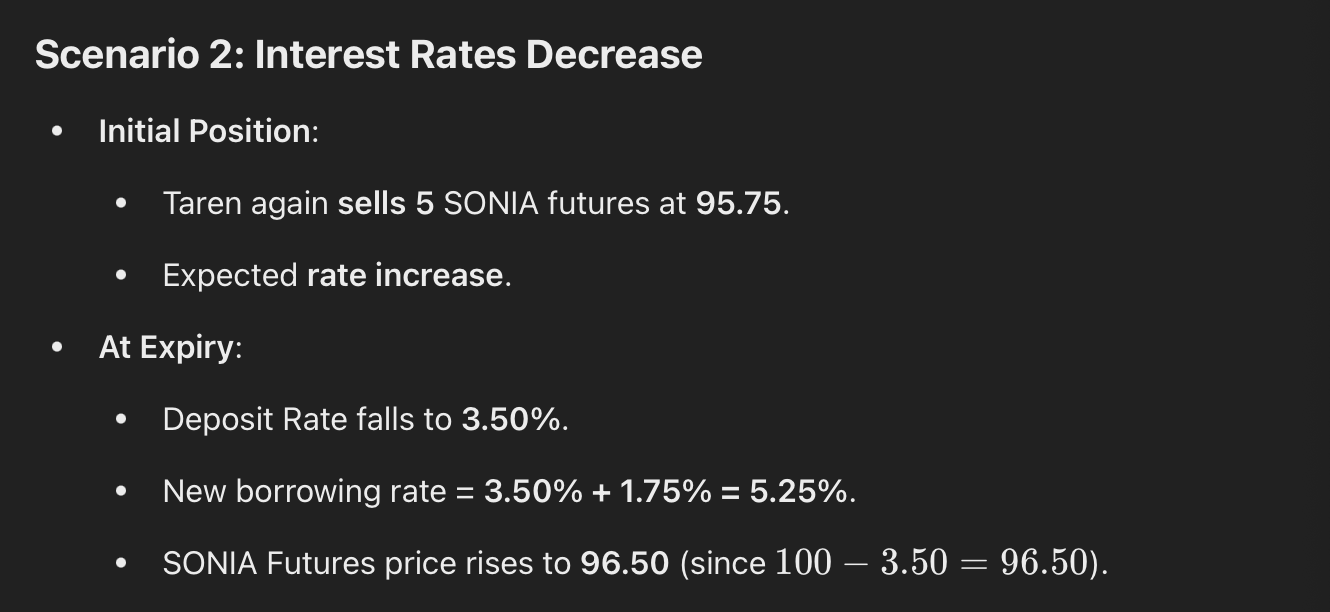

taren ltd. needs to borrow 5 mil. in 1 month for 3 months

expectations - interest rates will rise

strategy:

borrow 5 mil. today for 4 months at a lower rate

reinvest excess funds for 1 month

outcome - saves costs by borrowing at a cheaper rate

taren ltd. faces:

borrowing rates:

2.5% = 1 month

2.75% = 3 months

2.75% = 4 months

lending rate = 2% = 1 month

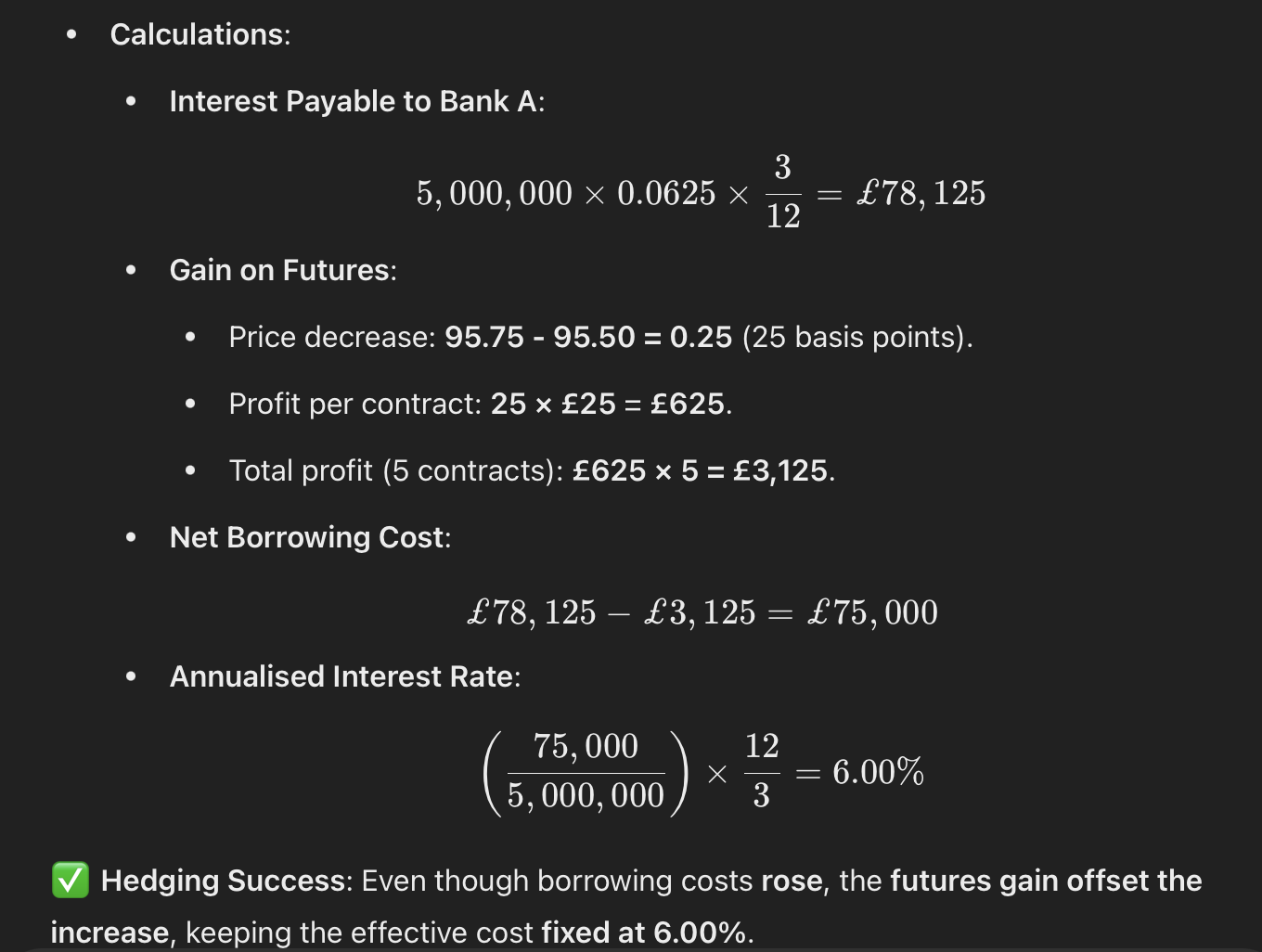

calculations:

interest payable = 5 mil. x 2.75% x 4/12 = 45, 833

interest received = 5 mil. x 2% x 1/12 = 8,333

net interest cost = 45,833 - 8,333 = 37,500

annualised rate = [37,500/5 mil.] x 12/3 = 3%

forward rate agreement [FRA]

definition - a forward contract fixing an interest rate on a specified principal for future period

nature:

both parties agree on a fixed rate

notional principal - no actual money exchange

cash settlement - the difference between the FRA rate and actual rate is settled at maturity

traded over the counter [OTC]

example:

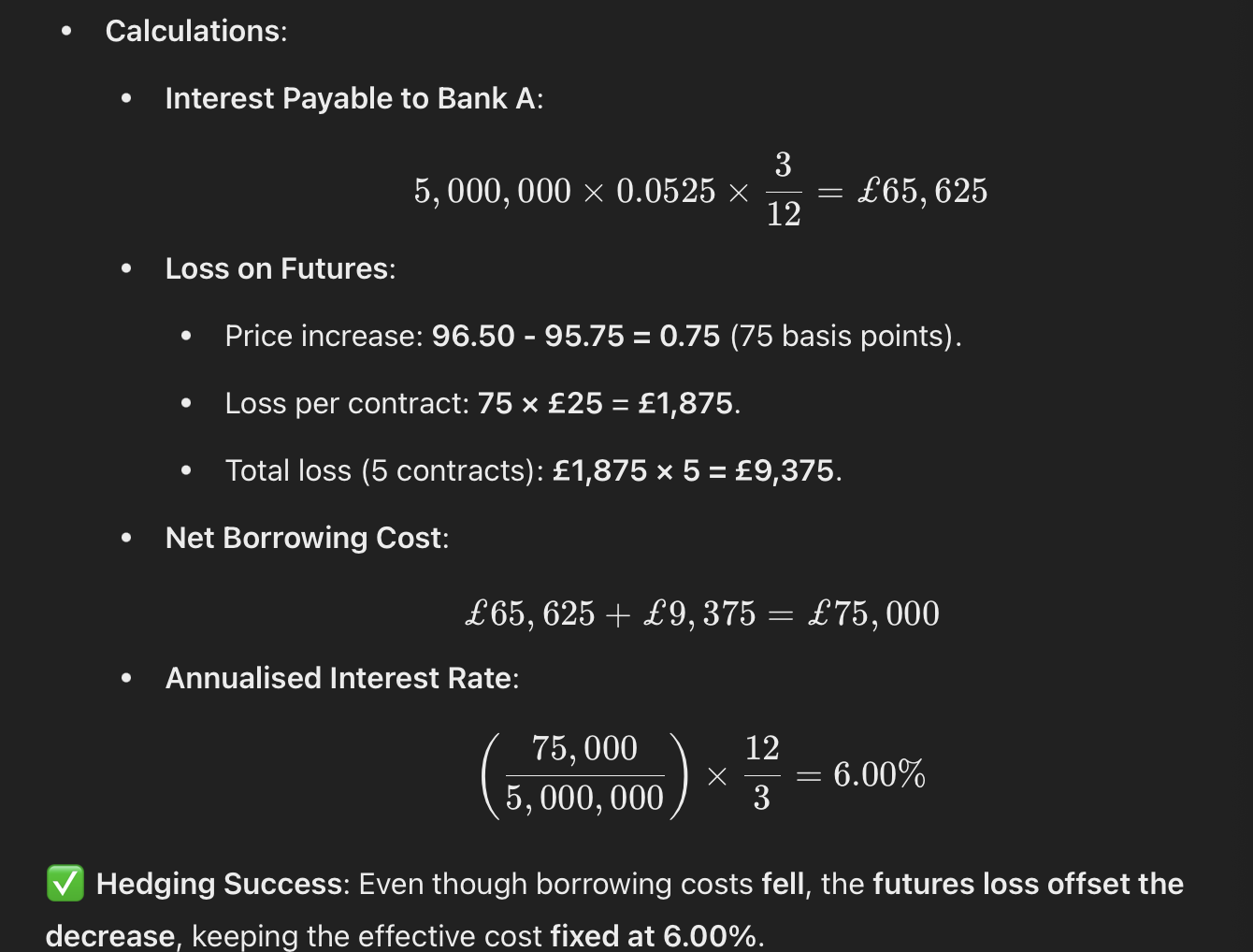

taren ltd. wants to borrow 5mil. in 1 month for 3 months

they expect borrowing rates to rise from 3% to 3.5%

solution:

borrow 5mil. at 3.5% from Bank A

buy an FRA from Bank B at 3%

calculations:

interest payable to bank A = 5mil. x 3.5% x 3/12 = 43,750

FRA payoff from bank B = 5mil. x [3.5% - 3%] x 3/12 = 6,250

net interest cost = 43,750 - 6,250 = 37,500

annualised interest rate on strategy:

[37,500/5mil.] x [12/3] = 3% — fixed no matter what happens

additional cost = [3.5% - 3%] x [3/12] x 5mil. = 6,250

rate index future [RIF] / short term interest rate future [STIR]

3 mont interest rate futures

for the UK “Short Sterling Contracts“ [ST3]

mechanism:

buying the future - right to lend at a set rate for 3 months

selling the future - right to borrow at a set rate for 3 months

exchange traded - standardised, transparent, and highly liquid

example:

contract size and maturity

size - each futures contract represents 1mil. in notional value

maturity - the contract always has a 3 month duration

expiration dates - contracts expire in march, june, september, and december

quotation format

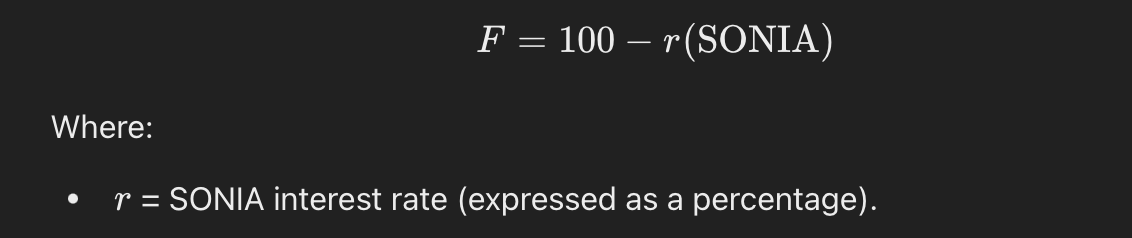

the futures price [F] is calculated using the formula:

therefore, if SONIA = 4.25%, then:

F = 100 - 4.25 = 95.75

this means if you buy a december contract at 95.75, you are effectively agreeing to lend at 4.255 for 3 months [april to june]

tick size and value

tick size - the smallest price movement is 0.005

value of one tick - 0.005 basis points [bps] = £12.50 per contract

notional value x bps = 1mil. x [0.005/100] = 50

must put bps out of percentage

contract = 3 months so its quarterly = 50/4 = 12.5

therefore:

a single tick [0.005] movement = £12.50 per contract

each contract has a notional value of 1,000,000

tick movement of 0.005 = 0.5 bps

so, 1 basis point = £25, and 0.5 bps = £12.50 per contract

example: buying a december 3M SONIA Futures contract

you buy a december contract at 95.75 [implying SONIA = 4.25%]

this means you have agreed to lend 1mil. at 4.25% for 3 months [april - june]

the contract expires in march

if interest rates rise:

assume that by expiration in march, SONIA has inc. to 5%

the new futures price is:

F = 100 - 5 = 95

since you bought at 95.75, and the price dropped to 95, you profit from this price movement

calculating profit:

change in price = 95.75 - 95 = 0.75 [which is 25 bps]

multiply out of percentage = 0.75 × 100 = 75

divide for 3 month contract = 75/4 = 25 bps

since 1 bps = £25, the profit is = £25 × 25 = £625

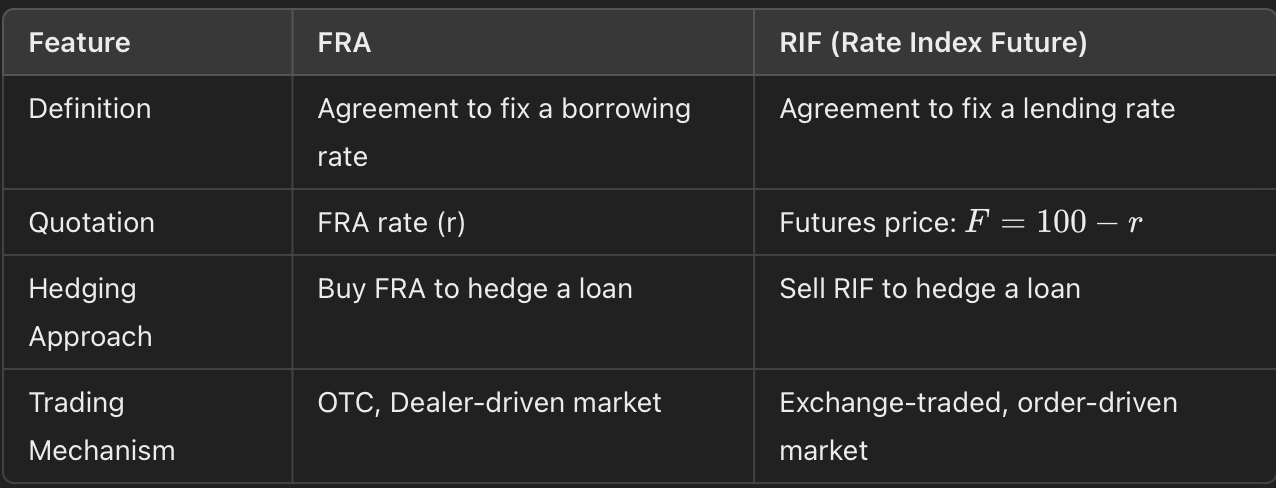

differences between FRA and IRF

advantages and disadvantages of FRA vs. IRF

FRA [forward rate agreement]

advantages:

easy to use, doesn’t require complex knowledge

customised to firm’s specific needs

no explicit margin requirement

disadvantages:

requires bilateral agreement with a dealer

no secondary market — cannot exit early

lack of pricing transparency

RIF [rate index future]:

advantages:

standardised and exchange traded

liquid secondary market — cannot exit early

transparent pricing

disadvantages:

requires knowledge of future markets

requires broker or bank access

requires margin deposits [initial and variation]

interest rate guarantees

opinions on interest rates

IRGs include caps, floors, and collars

traded OTC with SONIA as the underlying asset

short expiry dates [typically 3 months]

premium paid upfront for protection

borrowing with IRGs

if a firm expects rates to rise, it can purchase an interest rate call option

if rates increase — exercise call option and borrow at a lower pre-agreed rate

if rates decrease - do no exercise and borrow at lower market rate

cost - premium is paid upfront regardless of what happens

cap

a series of call options across different maturities

guarantees a maximum borrowing rate over a loan’s lifetime

advantage - protects against rising rates while allowing firms to benefit if rates fall

floor

a series of put options across different maturities

guarantees a minimum borrowing rate

disadvantage - if rates decrease, the firm still pays more

collar

combination of cap + floor

purpose - reduce hedging costs

the firm sells a floor [limits upside benefits] to pay for a cap [limits downside risk]

guarantees a range for borrowing costs

interest rate options

exchange traded options [e.g. 3 month short sterling options]

based on SONIA:

call option = right to deposit [lend] at a fixed rate

put option = right to borrow at a fixed rate

advantages and disadvantages of interest rate options

advan.

protects against downside risk

allows firms to benefit from favourable interest rate movements

disadvan.

premium paid upfront [cost incurred regardless of market movement]

interest rate swaps [IRS]

plain vanilla interest rate swap

exchange of fixed vs. floating interest payments between 2 parties

party A - wants to pay floating and receive fixed

party B - wants to pay fixed and receive floating

transforming a liability using IRS

a company can use an interest rate swap to convert its debt profile:

example:

company A - currently pays fixed 5.2%

company B - currently pays floating SONIA + 0.8%

swap terms:

company A:

pays SONIA [floating]

receives 5% fixed

new net rate - SONIA + 0.2% [floating liability]

company B:

pays 5% fixed

receives SONIA

new net rate - 5.8% [fixed liability]

both companies get the type of loan structure they prefer

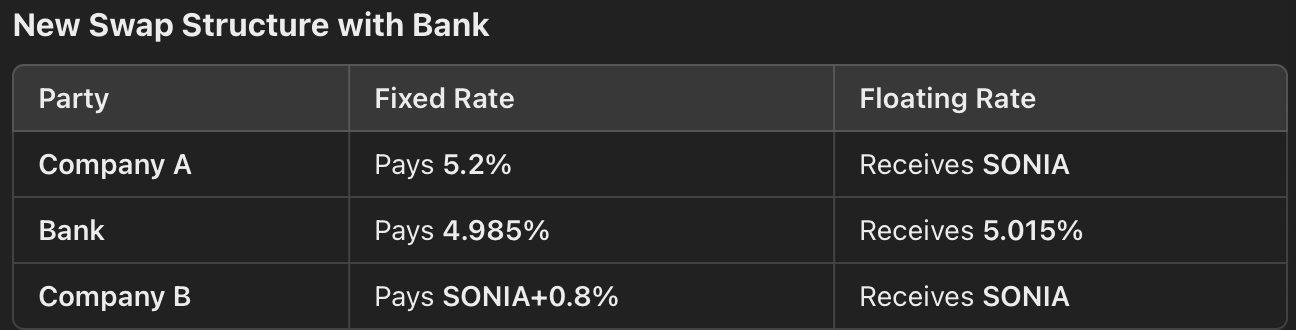

interest rate swaps [IRS] with a bank

swaps are usually arranged through banks

banks earn 3-4 [0.03% - 0.04%] basis points for arranging offsetting transactions

outcome:

company A now pays SONIA +0.215% instead of SONIA +0.2%

company B now pays 5.815% instead of 5.8%

bank earns 3 basis points in total

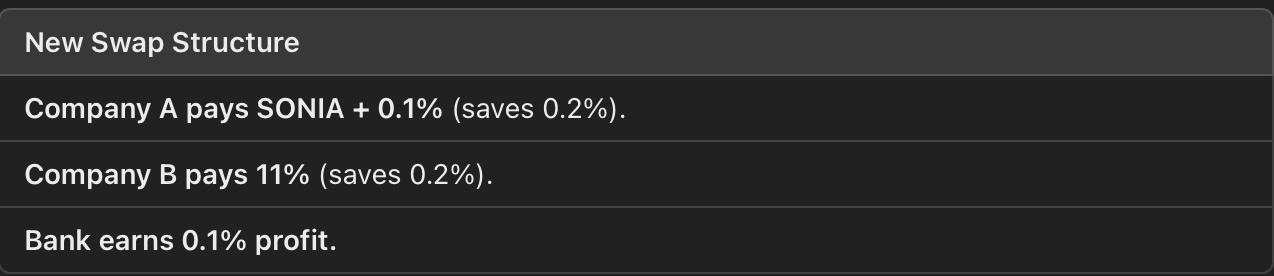

comparative advantage in swaps

companies should borrow in the market where they have a comparative advantage

key observations:

company A has an advantage in the fixed rate market [lower cost]

company B has an advantage in the floating rate market

total swap gain:

difference in fixed - difference in floating = 1.2% - 0.7% = 0.5%

each company benefits from a 0.25% cost reductions

including a bank in the swap

if a bank is involved, it earns 10 basis points [0.1%], which is shared between both companies

discussion - IRS hedging benefitd

why use an IRS?

hedges interest rate risk effectively

firms get preferred interest structure [fixed vs. floating]

lower borrowing costs due to comparative advantage

good for medium term hedging [5 yrs]

are there disadvantages?

potential counterparty risk

complexity compared to simple loans

bank fees reduce the total savings