Market power HL

Market power is the extent to which each individual firm in an industry is able to control price at which it sells its product

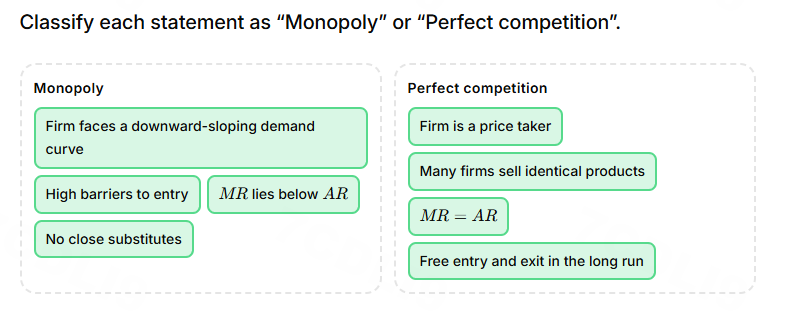

Perfect competition is where firms have no ability to control the price of their products (zero market power)

It is highly unrealistic, and it’s difficult to find markets in the real world that meet the characteristics.

A perfect competitive firm has no market power because there are many small firms, so each firm is too small to affect market price. Also the product is homogenous (the same), so consumers see no difference between sellers.

Characteristics of perfect competition

Large number of firms in the industry

All the firms in the industry sell homogenous products (identical)

There are no barriers to entry

No market power (they’re price taker)

A monopoly is where there is a single firm in a market has the greatest ability to control the price of its product, and therefore the greatest amount of market power

Characteristics of a monopoly

There is a single or dominant firm in the industry, so the single firm is the entire industry

The firm produces and sells a unique good or service, with no close substitutes

There is high barriers to entry in the industry

High barriers to entry protect the monopolist from competition, which helps maintain high market power. When entry is difficult or impossible, potential rivals cannot increase market supply, so the incumbent can sustain higher prices and abnormal profits for longe

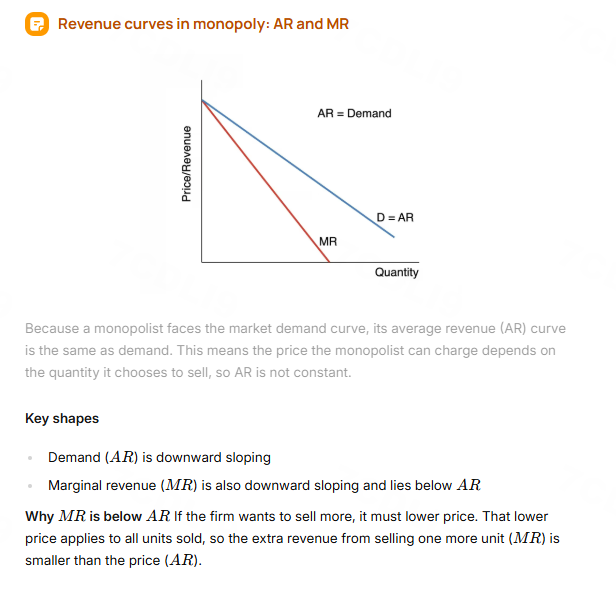

Monopoly = AR = D and MR lies below AR

When MR > 0, TR is increasing

When MR = 0, TR is at its maximum

When MR < 0, TR is falling

MONOPOLISTIC COMPETITION

Monopolistic competition is like perfect competition because there are large numbers of small firms. It differs from perfect competition mainly because of product differentiation. By trying to make its good or service different from any other, each firm tries to be like a little monopoly.

Characteristics of monopolistic power

Large number of small (or medium-sized) firms in the industry

There are no barriers to entry

There is product differentiation; each firm tries to make its product different from those of the other firms in the industry in terms of various characteristics like the quality, servicing and packaging.

Some market power

TR = Price x Quantity (firm’s total sales revenue)

AR = TR / Quantity (revenue per unit sold)

MR = ∆TR / ∆Q (the extra revenue from selling one more unit)

P = TR / Q

Profit = TR - TC

P = AR

In perfect competition, P = AR = MR

Oligopoly is a small number of large firms dominating an industry.

In oligopoly, firms are INTERDEPENDENT. Any change in price, output or advertising by one firm is likely to trigger a responce from rivals.

Interdependence in oligopoly leads to:

Non-price competition: firms compete through advertising, product differentiation and loyalty schemes, rather than changing price.

Price leadership: one firm sets the price and other firms follow, often to reduce uncertainty and avoid aggressive price competition.

Collusion: firms may coordinate to reduce competition and increase joint profit, for example, by raising prices or limiting output.

Common forms on non-price competition include:

Advertising and branding

Product quality and innovation

Customer service and loyalty programmes

Packaging and design

Characteristics of oligopoly

There is a small number of large firms; because of their small number, the firms are interdependent, because the actions of one firm affect the other. This means that each firm tries to predict what the rival firms will do

Products may be either differentiated or undifferentiated

There are high barriers of entry

Explicit costs: payments made by a firm to outsiders to acquire resources in use of production (like a firm hiring labour (worker) and pays with wage)

Implicit costs: opportunity cost of the output; sacrificed income from the use of self-owned resources by a firm

COSTS

AC = TC / Q

MC = ∆TC / ∆Q

THE MARGINAL COST ALWAYS INTERSECTS THE AVERAGE COST CURVE WHEN IT’S AT ITS MINIMUM!!!

When the marginal cost curve lies below the average cost curve, (MC < AC), average cost is falling

When the marginal cost curve lies above the average cost curve (MC > AC), average cost is increasing

An example could involve test scores. Say you have an average of 80 in your tests. If your next test score (marginal score) is greater than your average score of 80, your average will increase. If your next score is lower than your average of 80, your average will fall. This is the exact same relationship with average and marginal costs.

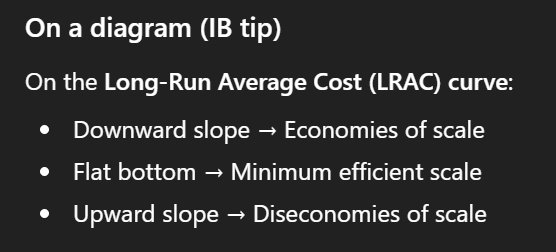

Economies of scale are decreases in average cost of production over the long run as a firm increases all its factors of production.

If average cost decreases, it means each individual unit becomes cheaper to produce

Simple example:

Imagine a firm produces:

1,000 units at a total cost of $10,000

→ Average cost = $10 per unit

Then it expands production to:

5,000 units at a total cost of $30,000

→ Average cost = $6 per unit

Even though total cost increased, cost per unit fell from $10 to $6.

That fall from $10 → $6 is the decrease in average cost.

Why this occurs:

Specialization of labour: As the scale of production increases, more workers must be employed, allowing for greater labour specialization.

Specialization of management: Larger scales of production allow for more managers to be employed, each of whom can be specialized in a particular area.

Bulk buying of inputs: As quantities of inputs purchased increase, the price per unit drops.

Diseconomies of scale are increases in the average costs of production in the long run as a firm increases its output by increasing all its output.

Why this occurs:

Coordination and monitoring difficulties: As a firm grows larger, its management may run into difficulties of coordination. Leads to inefficiencies, causing average cost to increase as the firm expands.

Communication difficulties: A larger firm size may lead to difficulties in communication between various component parts of the firm, resulting in inefficiencies and higher average costs.

Poor worker motivation: If workers begin to lose their motivation, to feel bored or care little about their work, they become less efficient, resulting in higher average costs.