Better Money - 2. Gold standard

1. Types of gold standards

Gold standard: any monetary system in which a defined mass of gold coin is the unit of account in which prices are posted and accounts kept.

Gold coins are the medium of redemption that ordinary currency and bank accounts promise to pay.

The classical period of the international gold standard begins with the post-Civil War return of the US to gold redemption in 1879.

It ended when European governments departed from gold redeemability at the beginning of WW1.

The gold definition of the monetary unit is made tangible in a gold coin.

A gold standard does not require that gold coins are most common type of money that people use.

Currency notes are tied to gold by being redeemable for the gold-defined monetary unit.

Types of gold standard, based on the physical form of gold paid out in redemptions:

Gold coin standard

Gold bullion standard: proposed by David Ricardo, large bars of gold, compelling people to give up gold coins in favor of paper notes.

Gold-exchange standard: where domestic currency can only be redeemed for a foreign gold-standard currency.

Should commercial banks be allowed to issue gold-redeemable common currency or should legislation restrict currency to a public institution.

100% reserve gold standard: every paper dollar must be backed by one gold dollar.

Gold standard does not require government, but they have always involved themselves in it.

Creation of government mints.

Empowerment of central banks.

2. Difficulties of transacting with coins only

Silver and gold coins had limited durability.

They experienced physical wear and tear, reducing their metallic content over time.

Some people would deliberately shrink coins, through filching.

Heaviest coins were culled from circulation.

Debasement by sovereign mints, which sometimes recalled and re-issued coins with less precious metallic content.

Variously worn or lightened or debased coins lacked uniformity.

Merchants and bankers had to weigh coins.

Travelers had to pay fees to convert currencies.

They lacked portability for large-value payments.

An economy using silver coins for small-value payments also needed gold coins for large-value payments.

Gold coins lacked divisibility.

In some economies, copper coins were used for even smaller-value payments.

Exchange between these coins was not fixed.

3. Bimetallism

Bimetallism: silver and gold coins are denominated in a common unit.

Bimetallism fixed an official domestic exchange rate between gold and silver, which rarely coincided with the variable world market exchange rate.

An arbitrage opportunity is created: Buy 15 oz. silver in the world market, swap it at the mint for 1 oz. in gold coins, swap the gold coins in the market for 20 oz. of silver, and pocket 5 oz. of silver as a profit at the mint’s expense.

There are no known examples of free-market bimetallic standards.

Bimetallism requires a monetary authority.

Gresham's law: bad money drives out good.

A small move in the mint ratio to either side of the world market price ratio will banish one of the metals.

Friedman argued that in historical experience, arbitrage was limited by costs of melting coins and exporting the metal.

These costs create a range of world price ratios around the mint ratio in which both metals can circulate together.

Modern banking provided a better solution than bimetallism.

In a monometallic standard with the use of bank-issued money, both small and large payments are made in banknotes, all kept at par by redeemability for the standard metal.

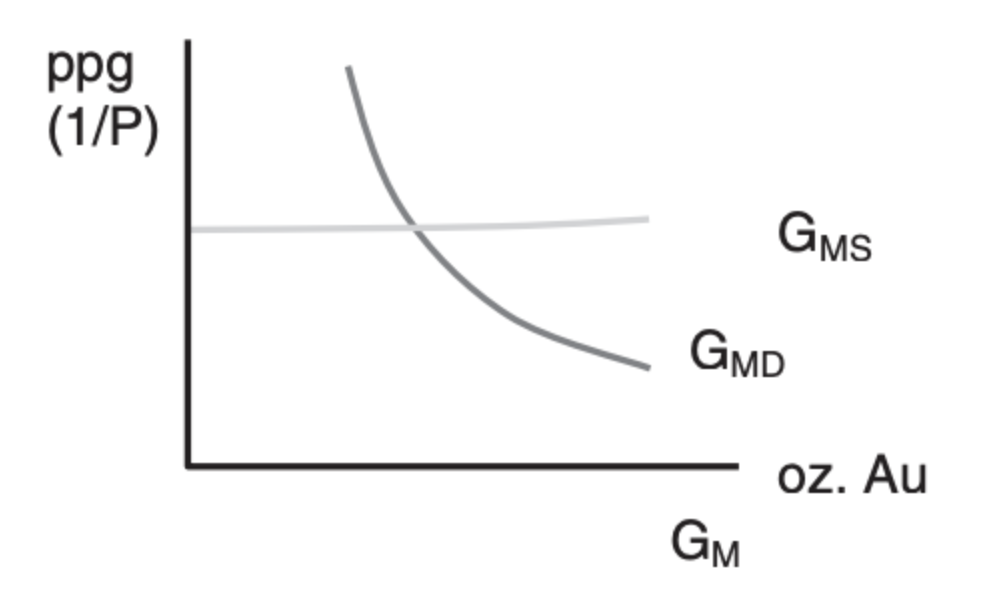

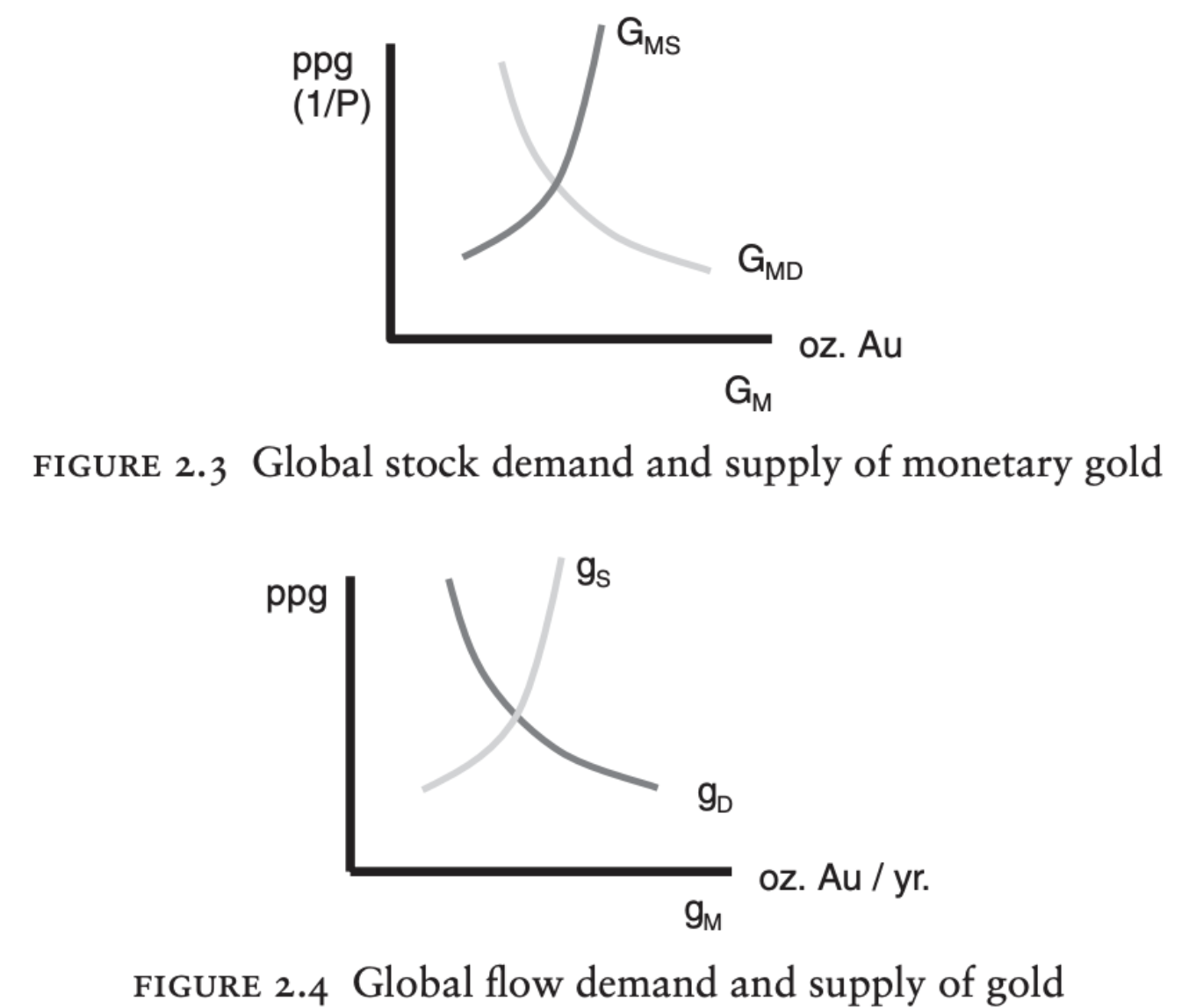

4. How market forces determine the quantity and purchasing power of gold in a small open economy

A single region can be regarded as a “price taker” for gold when it is one corner of a much larger gold-standard world.

The purchasing power of gold, or ppg for short, meaning how many bundles of goods trade for one ounce of gold.

5. Why inflation was low under the classical gold standard

Classic international gold standard had five virtues

Lower inflation rates

Lower price level uncertainty at medium to long horizons

Lower resource costs of gold mining for monetary or financial purposes

Greater global trade with a common currency between countries

Greater fiscal discipline

Inflation rate is the rate of increase of general level of prices.

Under a gold standard, the quantity of money does not expand much each year.

Gold is costly to mine and refine.

The world quantity of monetary gold grew relatively slow.

6. How market forces govern the global quantity and purchasing power of gold

The quantity of gold available in the market (supply) and the desire of consumers and industries to purchase gold (demand) interact to determine the price of gold.

Higher mining costs can lead to a reduction in the quantity of gold supplied at lower prices.

Gold is not only a monetary asset but also has various industrial applications.

The gold market is highly integrated globally, meaning that changes in one region can have ripple effects worldwide.

7. The dynamics of gold supply and demand in diagrams

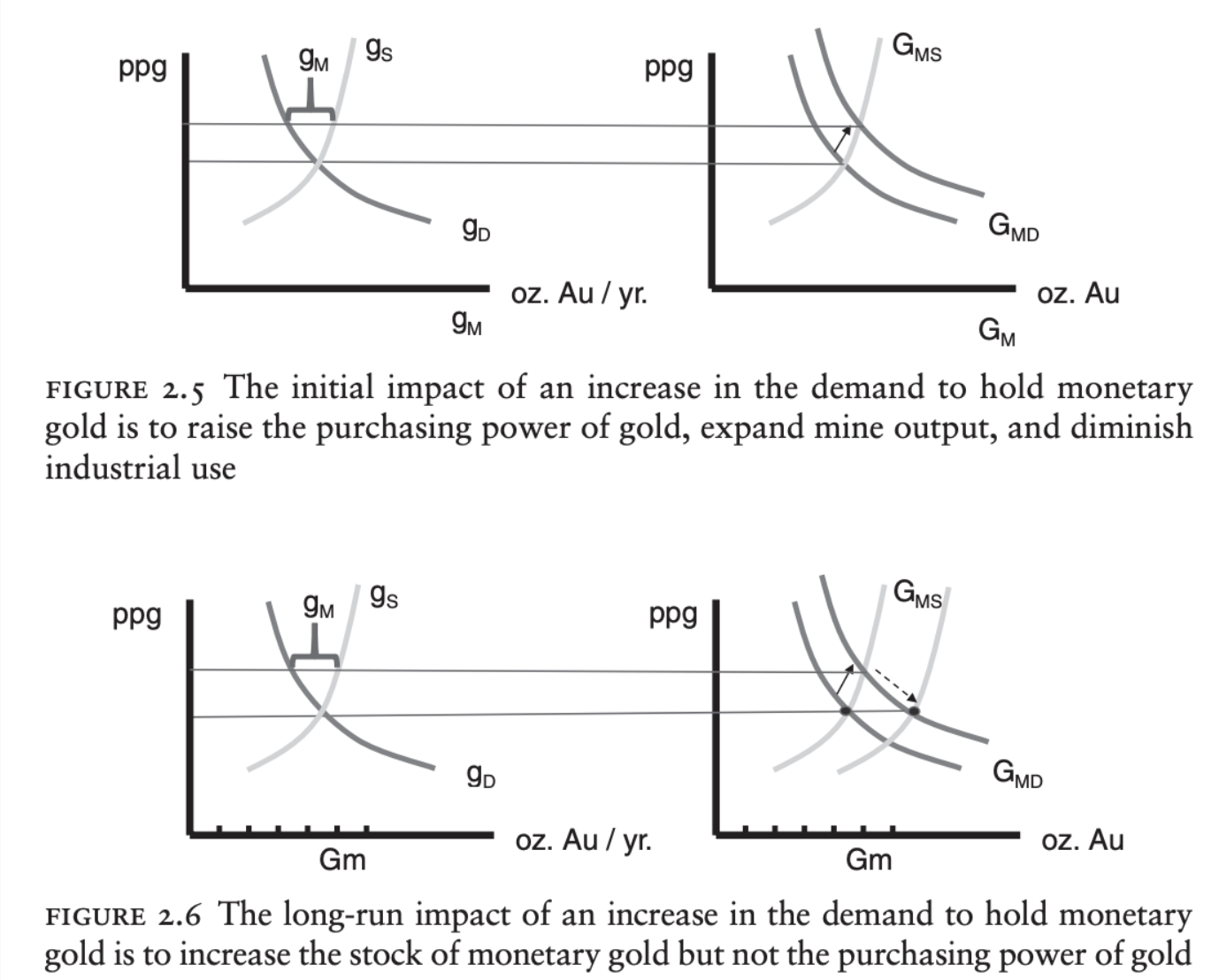

8. Supply and demand for gold in a growing economy

The demand for gold can increase significantly due to higher industrial usage.

As consumer wealth increases, there may be a greater demand for gold jewelry and investment.

The ability to increase supply is often constrained by factors such as mining costs, regulatory challenges, and the finite nature of gold reserves.

Supply may not always keep pace with rapidly growing demand, leading to fluctuations in the purchasing power of gold.

When demand outstrips supply, the purchasing power of gold may decline.

This can lead to inflationary pressures within the economy.

Economic and technological growth can influence the extraction and availability of gold in several ways.

9. Banking on a gold standard economizes on the use of gold

Adam Smith praised the voluntary replacement of gold and silver coins by bank-issued money as a boost for the economy’s production of goods and services.

Ludwig von Mises noted that the development of fractional reserve banking had spared the world much of the expense that would have been incurred if all the growth in money demand over the centuries had instead been met by gold mining.

10. The effects of shifts in flow supply and demand

Flow supply refers to the rate at which gold is produced and made available in the market, typically measured in ounces per year.

Flow demand encompasses the annual consumption of gold.

The text then explains effects and consequences of shifts in supply and demand.

11. How modern banking stabilizes the purchasing power of gold in the short run

When the public wants to hold a larger volume of bank-issued money, banks will find it profitable to expand even without additional reserves (can safely lower their reserve ratios) to meet the additional quantity demanded by holders.

Fiduciary media: banknotes or deposits in excess of gold reserves.

Competition among many issuing banks limits the danger of a large scale over-expansion.

The interbank clearing system will discipline any one bank that issues more notes or deposits than its customers want to hold.

Open competition in banking fostered prudence and standardization along with innovation and efficiency.

12. The resource cost of a gold standard

The development of modern fractional-reserve banknotes provided inexpensive substitutes for gold coin payments.

Modern banking enabled the world to release some labor and capital resources from gold mining.

We can realize still further resource cost savings by eliminating all gold reserves.

This is a common argument among economists for preferring a fiat standard over a gold standard.

However, more gold than before is being mined to be held in vaults. The hoped-for resource cost saving has not been realized.

Friedman noted that under fiat money regimes, individuals and institutions began to accumulate gold and silver as a hedge against inflation and economic instability.

This accumulation of gold required real resources to be diverted into gold production, which could have been used elsewhere in the economy.

Since the abandonment of the Bretton Woods system in 1971, inflation rates in Western nations had become higher and more variable.

This increase in inflation led individuals to view gold and silver as prudent components of their asset portfolios, further driving up demand for these metals.