Market Efficiency

Market Efficiency

An efficient economy maximizes output given limited resources, improving overall welfare.

Relation to Scarcity: Efficiency is related to scarcity, as the limited resources available to producers must be used in a way that reduces waste or inefficiencies. If these are limited, people's living standards will rise.

Types of Economic Efficiencies

Productive/Technical Inefficiencies: Occur when there may be inefficiencies during process of G&S production, leading to wasted resources and increase in producers’ costs.

Allocative Inefficiencies: Refers to when the price of a product is set higher than the amount that consumers value the good.

Production Possibility Curves (PPC)

Refers to a model which shows the output of two goods produced within a market or economy.

The curve represents maximum output possible; points under curve indicate inefficiencies.

For higher production beyond the curve, more resources or technology improvements are needed.

How Markets Create Welfare

Competitive markets benefit both buyers and sellers, leading to a win-win situation. (Both gain from the trade)

Total Welfare (Community Surplus): The sum of consumer surplus and producer surplus.

Consumer Surplus

Definition: Difference between the amount the consumer is willing to pay and how much they actually pay.

When rational, consumers gain extra pleasure from purchases, contributing to overall welfare.

Producer Surplus

Definition: The difference between the market price received and the cost of producing the good.

Producers will only sell if the revenue exceeds production costs, maintaining profitability.

Market Revenue Maximization

Consumers and producers may exit a market if their surplus diminishes - happens when market equilibrium is reached.

Deadweight Loss (DWL)

Definition: the difference between the actual level of welfare generated in a market and the maximum possible level of welfare.

DWL can stem from underproduction or overproduction and prices may be set above or below the equilibrium. (market not operating at equilibrium point).

Market Failure and Deadweight Loss

Market failure means resources are not being allocated to markets in an optimal manner, resulting in community surplus not being maximised (deadweight loss.)

Causes: monopolistic power aims to satisfy wants rather than aim for profit. Decisions based on bounded rationality due to limited or incorrect information, as they suffer from biases. Unintended consequences (externalities) on third parties, leading to either positive or negative effects that are not reflected in the market prices.

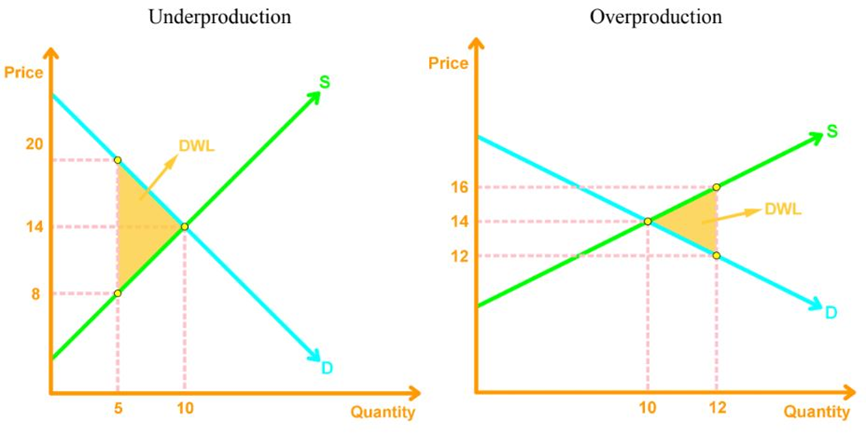

Underproduction and Overproduction

Cause of market failure

DWL on the left - Underproduction

DWL on right - Overproduction

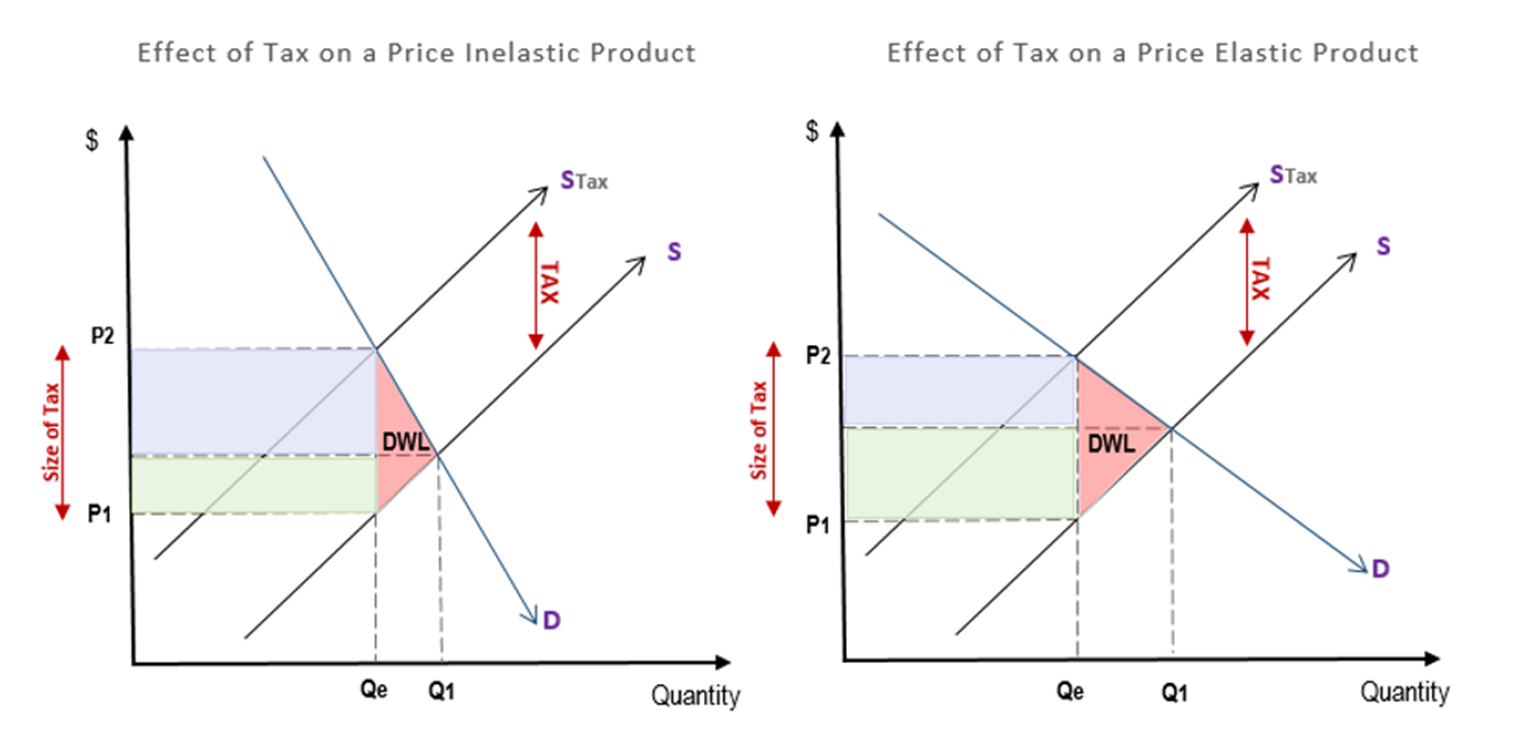

The Effects of Tax

Taxes shift the supply curve to the left upwards, affecting equilibrium price and quantity.

Price Inelastic Products (Tax): If the product is price inelastic, then there will be a large increase in the price of the good as producers know his will not decrease sales. This means that consumers carry the burden of tax for price inelastic goods, and consumer surplus decreases.

Price Elastic Products (Tax):If products are price elastic, then there will be a small increase in the price of the good meaning that producers carry most of the incidence. This is because an increase in price will cause a decrease in sales - a large fall in the quantity demanded.

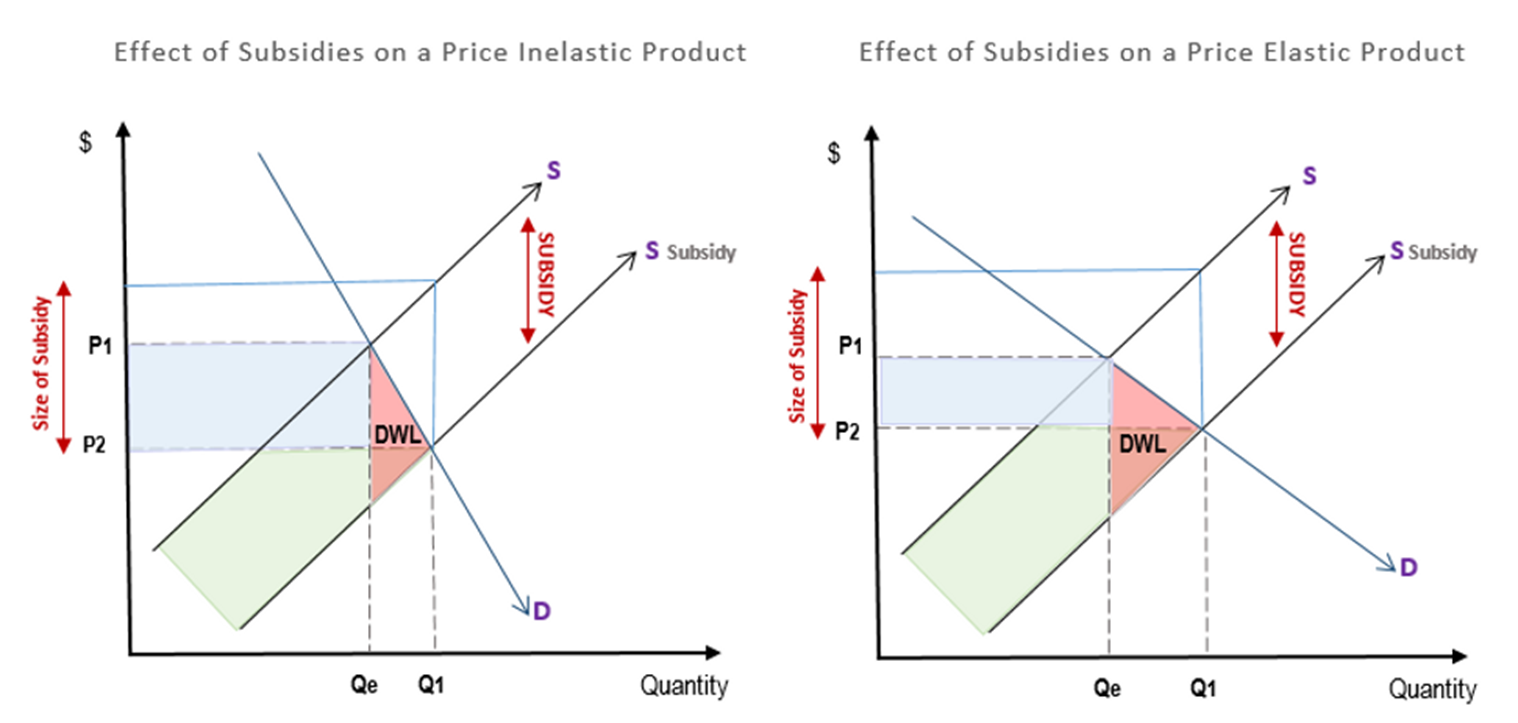

Subsidy

Subsidy: A subsidy can be defined as a payment from the government to a firm that incentives productivity or output of a good or service. This occurs to promote the production of a good with a positive benefit to society such as positive externalities, promoting local produce as opposed to imports or building employment in that industry.

Shifts supply curve downwards right.

Price Inelastic Products (Subsidy): If a product is price inelastic, then there will be a large decrease in the price of the product, meaning that the benefit of the subsidy is greatly passed onto consumers.

Price Elastic Products (Subsidy): If the product is price elastic, there will be a small decrease in the price of the product, but they purchase more goods, meaning that producers gain the most benefit from the subsidy on an elastic good, as production costs are lowered, there is only a small decrease in price and a large increase in quantity demanded.

How do taxes and Subsidies affect market efficiency?

In a normal market taxes and subsidies cause deadweight loss - reduce market efficiency.

Taxes can reduce the inefficiencies of negative externalities, as they increase the price for producers or consumers, in turn, correcting over-consumption or over-production. Comparatively, subsidies reduce the price for producers to make the product or for consumers to purchase it, therefore, it increases production or consumption of a positive externality which would otherwise be under-consumed and under-produced.

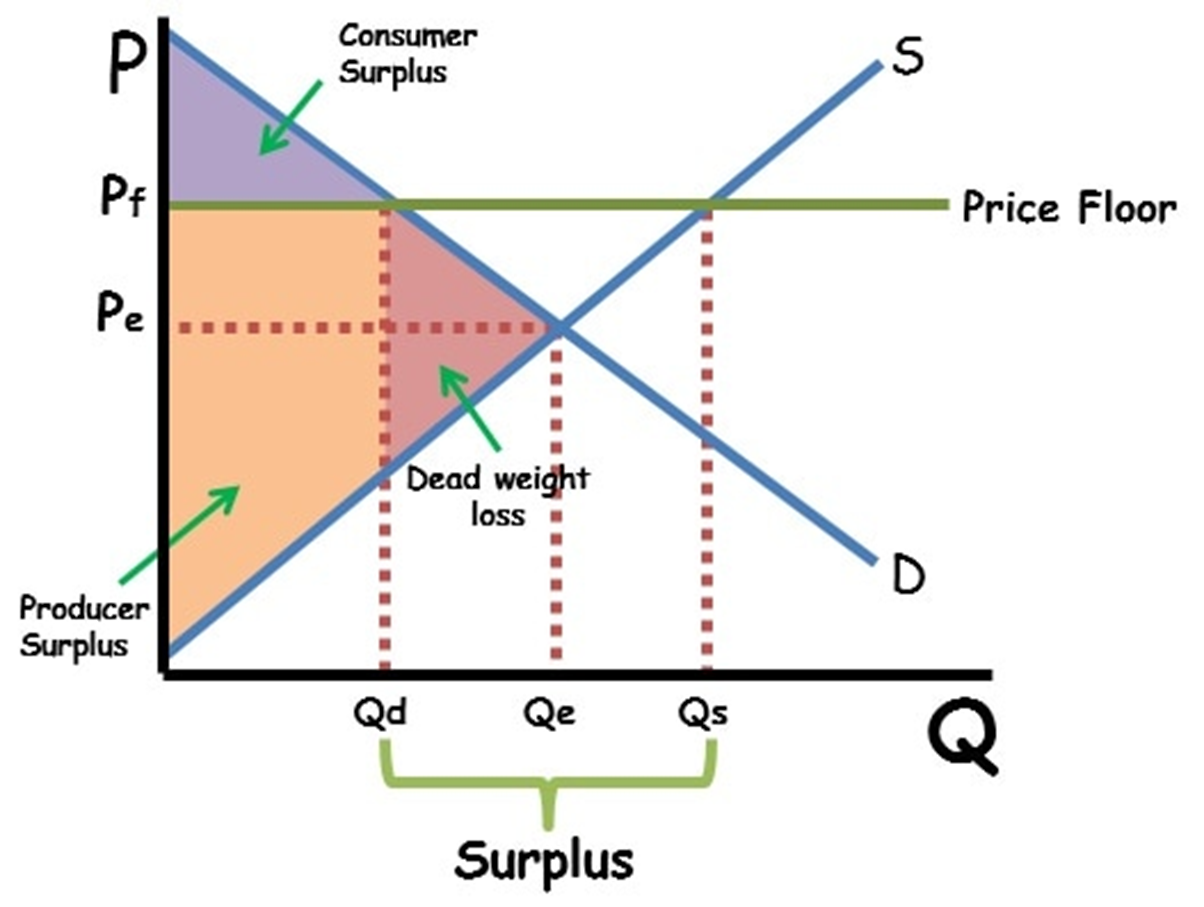

Price controls

Price controls are government-enforced maximum or minimum prices set above or below the equilibrium price for goods or services within a market.

Price Floors

Government-set minimum prices ensure stability for producers, resulting in surplus and inefficiencies.

Decrease in market size - Qd decrease

It creates a surplus or products.

It produces deadweight-loss (shown as DWL on the model.)

It reduces market efficiency as consumer surplus decreases.

Producer surplus increases, however, due to the surplus goods will go to waste due to reduced demand.

Illegal markets may form to exploit production costs to sell goods below minimum price.

Commodities Affected: Often applied to agricultural products (e.g., fruits and vegetables).

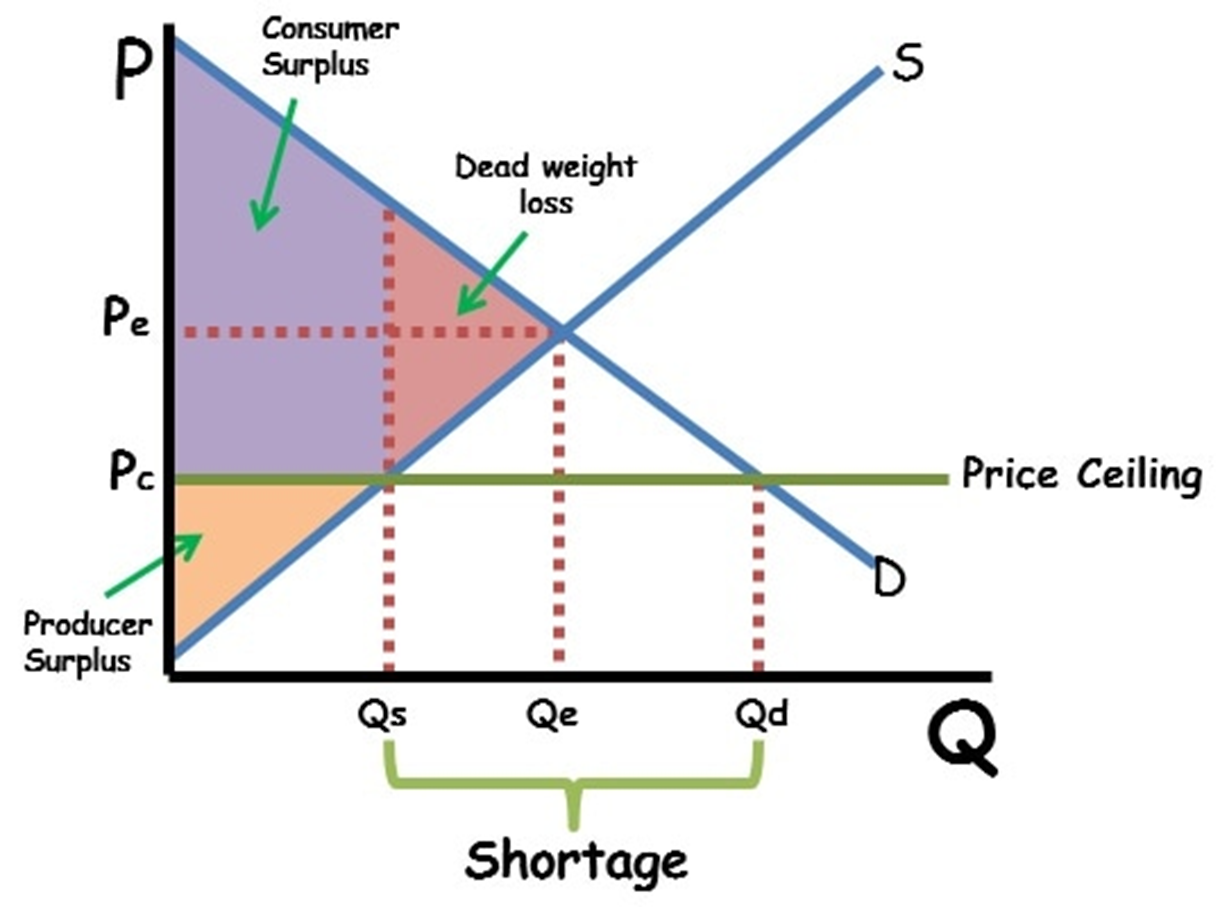

Price Ceilings

A maximum price enforced to keep prices affordable for consumers and to prevent price gouging.

Prices below equilibrium increase in quantity demanded, but lowers producers’ willingness to supply.

It reduces market efficiency as producer surplus decreases.

Creates shortages

Decrease in market size (Producers will reduce the output and quality of the products as a result of reduced prices.)

Consumer surplus increases, however, due to the shortage some consumers may miss out on buying the product. This creates black market prices as an effect.

Example: Staple foods might have a price ceiling as they are necessities for households and must be affordable for all.