Sales and Receivables - Quick Reference Notes

Revenue Recognition

GAAP uses accrual-basis accounting; revenue is recognized when control of promised goods/services is transferred.

Service businesses: revenue in the period the service is provided.

Merchandise businesses: revenue when title passes to the customer.

Customer Incentives: terms that affect cash collection include

Sales Discounts

Sales Returns

Sales Allowances

Sales Discounts

Typical terms: a discount is available for early payment (e.g., 2/10, net 30).

Journal effect: discount reduces cash received and creates a contra-revenue account (Sales Discounts).

Net revenue = Sales Revenue − Sales Discounts.

Sales Discount – Example concepts

Sale recorded: Accounts Receivable 65,000; Service Revenue 65,000.

If discount is taken, Cash is reduced by the discount and Sales Discounts is used to reduce revenue.

Full collection pattern reflects reduction in receivable by the discount amount.

Monitoring Sales Discounts

Net Revenue shown on income statement after subtracting Sales Discounts.

Other Types of Discounts

Trade Discounts: price reductions offered to a class of customers (e.g., wholesalers).

Quantity Discounts: price reductions for bulk purchases.

Sales Returns and Allowances

Sales Return: customer returns goods.

Sales Allowance: price reduction granted due to product/service problems.

GAAP: record in the period of sale; year-end adjustments may be needed for returns near year-end.

Sales Returns and Allowances – Example (conceptual)

Recognize liability for expected returns/allowances; offset against Sales Revenue.

Types of Receivables

Accounts Receivable or Notes Receivable

Current or Noncurrent Receivable

Trade or Nontrade Receivable

Accounts Receivable vs Notes Receivable

Accounts Receivable: usually short-term, no interest, due from customers for goods/services.

Notes Receivable: formal agreement with interest rate and a maturity date.

Current vs Noncurrent

Current: maturing within 1 year or the operating cycle.

Noncurrent: maturing beyond 1 year.

Trade vs Nontrade

Trade Receivable: arises from ordinary business from customers buying inventory or services.

Nontrade Receivable: arises from other transactions (e.g., interest receivable).

Bad Debts

Bad debt = uncollectible accounts; risk that some customers will not pay.

Net realizable value: the amount of cash the company expects to collect, net of uncollectibles.

Methods to record Bad Debt Expense:

Direct Write-Off Method

Allowance Method

Cost vs Benefit of extending credit

Benefit: increases sales by facilitating customer purchases.

Cost: risk of nonpayment.

The Direct Write-Off Method

AR is written off as Bad Debt Expense when deemed uncollectible.

Journal: Bad Debt Expense (Dr); Accounts Receivable (Cr).

Generally not GAAP-compliant because it may not match expenses with related revenues.

The Allowance Method

Year-end adjusting entry estimates bad debt; creates Allowance for Doubtful Accounts (contra-asset).

Specific uncollectible accounts are written off against the allowance later.

Allowance Method – Basic Example

Bad Debt Expense Dr 25,000; Allowance for Doubtful Accounts Cr 25,000.

Effects: reduces net accounts receivable on the balance sheet and records an expense on the income statement.

Allowance Method – Basic Example (income statement and balance sheet impact)

Income statement: Bad Debt Expense reduces Net Income.

Balance sheet: Accounts Receivable net of Allowance.

Percentage of Credit Sales Method

Estimates bad debt expense based on a percentage of credit sales.

Focuses on the Income Statement.

Estimated Bad Debt Expense = Total Credit Sales × Percentage Estimated to Default.

Entries adjust Allowance for Doubtful Accounts.

Percentage of Credit Sales – Example (conceptual)

Debit Bad Debt Expense; Credit Allowance for Doubtful Accounts for the estimated amount.

When a specific customer is written off, reduce AR and offset against the allowance.

Percentage of Credit Sales – Example (2) and beyond

Past-year estimates may under- or overestimate; adjusting entries reflect current period experience.

Aging Method

Determine desired ending balance in Allowance for Doubtful Accounts based on the age of AR.

Older receivables are more likely to default; focuses on Balance Sheet and net realizable value.

Adjust Bad Debt Expense to achieve the desired ending allowance.

Aging Method – Example concepts

Begin with AR and current Allowance.

Compute ending allowance by aging AR; record Bad Debt Expense to reach that balance.

Partial Write-Offs

Reestablish AR before collecting cash from a previously written-off account.

Example pattern: Dr Accounts Receivable; Cr Allowance; then Dr Cash; Cr Accounts Receivable.

Cash Management & Accounts Receivable

Factoring & Securitization

Factoring: selling receivables to a party (the factor) for immediate cash; the factor bears collection risk and charges a fee (typically 1–3%).

Securitization: packaging large volumes of receivables into securities sold to investors.

Credit Cards

Form of factoring; merchants receive cash from the card issuer minus a fee; issuer collects from cardholder.

Debit Cards

Immediate electronic withdrawal from payer’s bank account; lowers processing costs for banks/merchants; funds are immediately transferred.

Internal Control for Sales

Proper controls ensure recorded revenue is correct.

Key steps: purchase order received; shipping and billing documents prepared; sale/receivable recorded only when order, shipping, and billing documents exist.

Internal Controls for Recording Sales Revenue

Use purchase orders and ensure PO numbers appear on shipments and invoices.

Revenue and receivable are recorded only when order, shipping, and billing are complete and documented.

Notes Receivable

Note(s) Receivable

A formal agreement with a specified interest rate and maturity date.

Principal: amount borrowed.

Interest: compensation for the use of resources; stated as an annual rate.

Interest formula:

Notes Receivable – Example concepts

AR from Dover Electric moved to Notes Receivable; cash flows occur when note matures.

Interest revenue is recognized as earned; may be accrued as Interest Receivable before cash collection.

Example: 50,000 principal at 10% across various periods results in interest revenue or receivable as shown in sample entries.

Notes Receivable – Example (2) and (3)

Interest earned over a period is recorded as Interest Revenue; cash received includes principal plus accrued interest.

At year-end, accrue interest receivable for interest earned but not yet collected.

Example calculations show how to allocate principal and interest over multi-period terms.

Analyzing Sales & Receivables

Profitability Ratios

Gross Profit Margin =

Operating Margin =

Net Profit Margin =

These ratios indicate how efficiently a company converts sales into profit.

Accounts Receivable Turnover

AR Turnover =

Higher turnover indicates quicker collection of receivables.

Analyze over time to assess credit risk and collection efficiency.

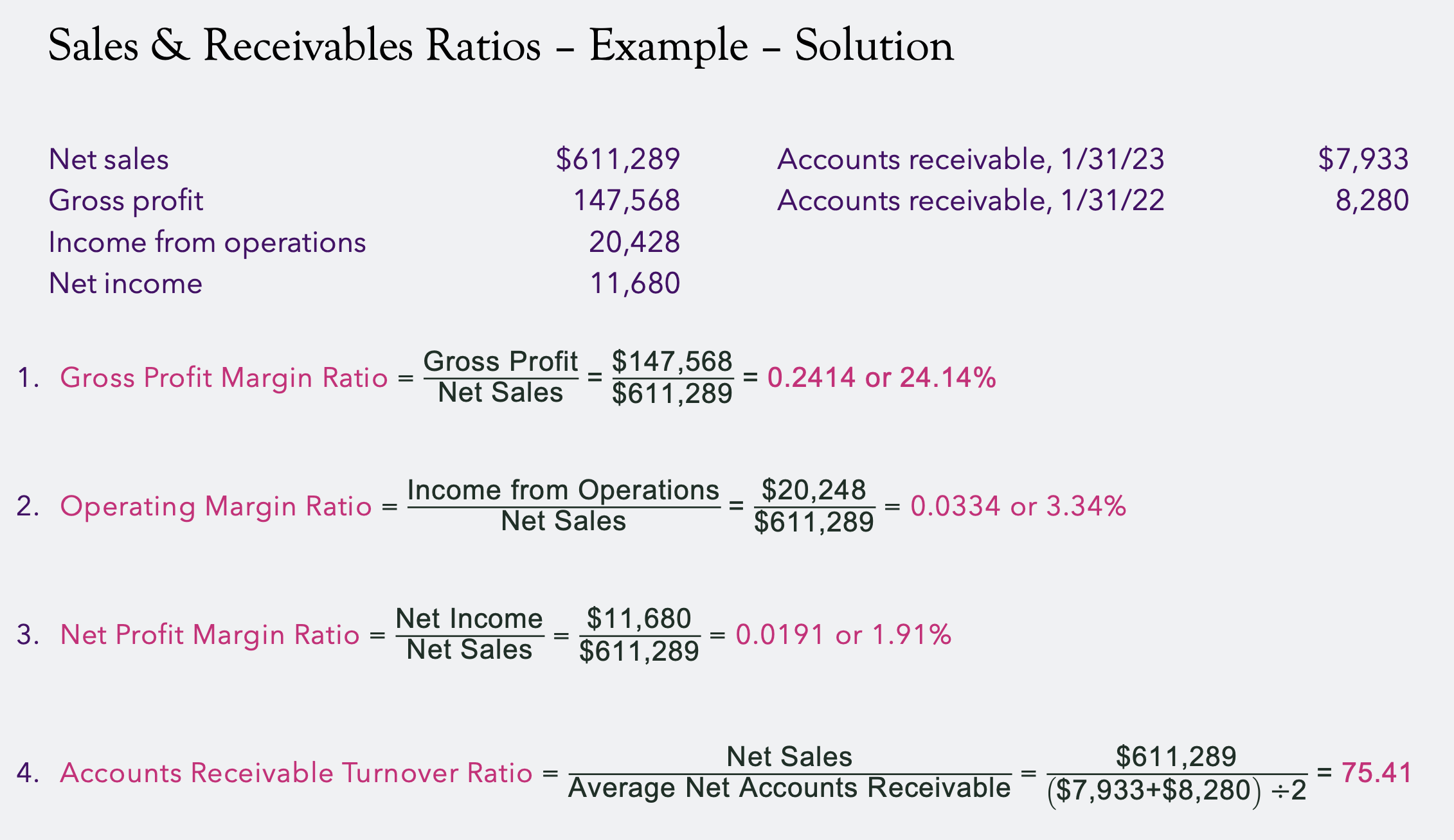

Example (from the provided data)

Net sales =

Gross profit =

Income from operations =

Net income =

Accounts receivable: 1/31/23 = , 1/31/22 =

Calculations

Gross Profit Margin = rac{147{,}568}{611{,}289} = 0.2414 ext{ or } 24.14 ext{%}

Operating Margin = rac{20{,}428}{611{,}289} = 0.0334 ext{ or } 3.34 ext{%}

Net Profit Margin = rac{11{,}680}{611{,}289} = 0.0191 ext{ or } 1.91 ext{%}

Average Net Accounts Receivable =

Accounts Receivable Turnover =

Notes

These ratios help assess profitability and receivables efficiency at a glance and are useful for quick review or reference.