week1

Introduction to Investment & Risk

Learning Objectives:

Understand key concepts of investment and associated risks, including how they relate to returns.

Explore the impact of inflation on investment returns.

Differentiate between simple and compound interest.

Grasp the time value of money.

Analyze varying returns across different asset classes.

Learn strategies to reduce risk through diversification.

Identify major types of risk that investors face.

Investment Risk

Principles of Investment:

Investment decisions are made based on expectations of future returns and the associated risks.

Understanding how to calculate total returns is crucial.

Time Value of Money:

The time value of money is a financial principle that states the value of a dollar today is worth more than the value of a dollar in the future.

This philosophy holds true because money today can be invested and potentially grow into a larger amount in the future.

Present Value: The current worth of a future sum of money or stream of cash flows given a specified rate of return.

Future Value: The value of a current asset at a future date based on an assumed growth rate.

Money has greater potential earning capacity over time.

The value of money decreases over time due to inflation.

Nominal and Real Rates of Return:

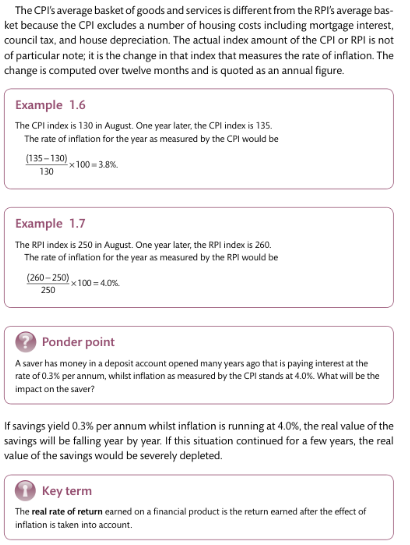

Nominal Rate: The percent increase in money that doesn’t account for inflation.

Real Rate: Nominal rate adjusted for inflation.

Formula: ext{Real Rate} = rac{1 + ext{Nominal Rate}}{1 + ext{Inflation Rate}} - 1

Interest:

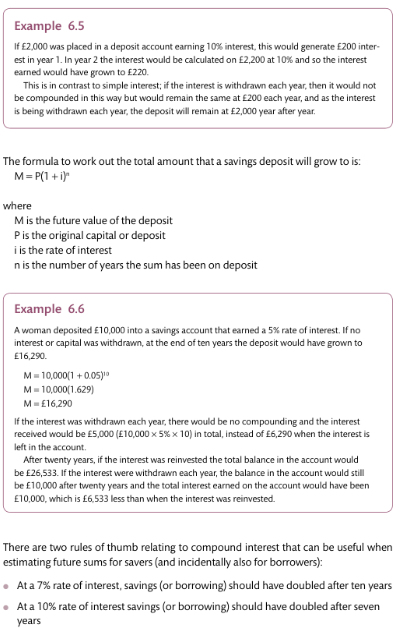

Simple Interest: Calculated on the principal amount only.

Formula: ext{SI} = P imes r imes t

Compound Interest: Calculated on the principal and also on the interest earned.

Formula A = P(1 + rac{r}{n})^{nt}

Types of Risk

Attitude to risk

An important factor that needs to be considered when undertaking personal financial planning, is an individual’s attitude to risk. A general principle is that the riskier a financial product, the greater the potential rate of return it will offer. The more secure

a product, the lower the rate of return it will offer. Some people are risk-takers, others

are risk averse, and most are somewhere between the two.

There are questionnaires that enable people to assess their personal attitude to risk.

Distinguishing Risk: Understanding various risk types helps in managing investments effectively.

Interest Rate Risk: Risk that interest rates will rise and decrease the value of securities.

Inflation Risk: The danger that inflation will erode purchasing power.

Shortfall Risk: The risk of not achieving the required return needed for future goals.

Capital Risk: The risk of losing the money one has invested.

Currency Risk: The risk of losing money due to changes in exchange rates.

Liquidity Risk: The risk of not being able to sell assets quickly or at a favorable price.

Measuring Risk

Standard Deviation: A measure of the amount of variation or dispersion of a set of values.

Alpha & Beta:

Alpha: Measures the performance of an investment relative to a market index.

Beta: Measures an investment's volatility compared to the market as a whole.

Sharpe Ratio: A measure of risk-adjusted return.

Formula: ext{Sharpe Ratio} = rac{(Rp - Rf)}{ ext{σp}} where Rp is the return of the portfolio, Rf is the risk-free rate, and σp is the standard deviation of the portfolio's excess return.

Utilizing past data and performance metrics to gauge future risk.

Diversification

Why Diversify?

Spreads risk across various investments rather than concentrating it in one.

Types of Diversification:

By Asset Class: Investing in different classes like stocks, bonds, real estate.

Within Asset Class: Investing in various sectors or industries within the same asset class.

Balancing a Portfolio:

Adjusting asset allocation based on risk tolerance and market conditions.

Diversifiable vs. Non-Diversifiable Risk:

Diversifiable Risk: Can be eliminated through diversification.

Non-Diversifiable Risk: Market risk that cannot be mitigated.

Diversification and Correlation:

Investments should have low correlation to maximize risk reduction.

Beta and Alpha in relation to portfolio diversification.

How Much Can You Diversify?

Understanding limitations in diversification and assessing optimal numbers of assets in a portfolio.

Relationship – Risk & Return

Risk & Reward: Higher potential returns are generally associated with higher risk.

High Returns with Low Risk – The Holy Grail:

Many investors seek this balance, but it is rare.

Risk-Free Rate of Return: The return expected from an absolutely risk-free investment over a specified period.

Risk Premium: The return in excess of the risk-free rate that compensates investors for taking on additional risk.

Risk Spectrum: Understanding where different investments lie on the risk-return curve is crucial for making informed investment decisions.

Inflation

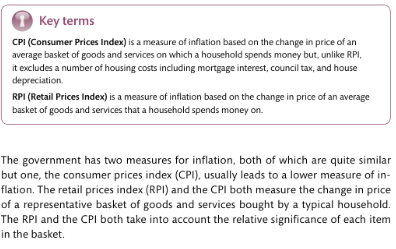

Inflation describes the situation when the cost of goods and services that households

buy, increases. This means that the purchasing power of money will fall.