Unit 1 Notes (Chp 1-3)

CHAPTER 1 OUTLINE:

I. Introduction

A. The word “economy” comes from the Greek word meaning “one who manages a household.”

B. This makes some sense since in the economy we are faced with many decisions (just as a household is).

C. Fundamental economic problem: resources are scarce.

D. Definition of scarcity: the limited nature of society’s resources.

E. Definition of economics: the study of how society manages its scarce resources.

II. How People Make Decisions

A. Principle #1: People Face Tradeoffs

- “There is no such thing as a free lunch.” Making decisions requires trading off one goal for another.

- Examples include how a student spends her time, how a family decides to spend its income, how the U.S. government spends tax dollars, how regulations may protect the environment at a cost to firm owners.

- A special example of a tradeoff is the tradeoff between efficiency and equity.

a. Definition of efficiency: the property of society getting the most it can from its scarce resources.

b. Definition of equity: the property of distributing economic prosperity fairly among the members of society.

c. For example, tax dollars paid by wealthy Americans and then distributed to those less fortunate may improve equity but lower the return to hard work and therefore reduce the level of output produced by our resources.

- This implies that the cost of this increased equity is a reduction in the efficient use of our resources.

- Recognizing that tradeoffs exist does not indicate what decisions should be made.

B. Principle #2: The Cost of Something Is What You Give Up to Get It

- Making decisions requires individuals to consider the benefits and costs of some action.

- What are the costs of going to college?

a. We cannot count room and board (at least all of the cost) because the person would have to pay for food and shelter even if he was not in school.

b. We would want to count the value of the student’s time since he could be working for pay instead of attending classes and studying.

- Definition of opportunity cost: whatever must be given up to obtain some item.

C. Principle #3: Rational People Think at the Margin

- Many decisions in life involve incremental decisions: Should I remain in school this semester? Should I take another course this semester? Should I study an additional hour for tomorrow’s exam?

- Definition of marginal changes: small incremental adjustments to a plan of action.

- Example: You are trying to decide how many years you should stay in school. Comparing the lifestyle of an individual with a Ph.D. to that of an individual who has dropped out of grade school would be inappropriate. You are likely deciding whether or not to remain in school for an additional year or two. Thus, you need to compare the additional benefits of another year in school (the marginal benefit) with the additional cost of staying in school for another year (the marginal cost).

D. Principle #4: People Respond to Incentives

- Because people make decisions by weighing costs and benefits, their decisions may change in response to changes in costs and benefits.

a. When the price of a good rises, consumers will buy less of it because its cost has risen.

b. When the price of a good rises, producers will allocate more resources to the production of the good because the benefit from producing the good has risen.

- Sometimes policymakers fail to understand how policies may alter incentives and behavior.

- Example: Seat belt laws increase use of seat belts and lower the incentives of individuals to drive safely. This leads to an increase in the number of car accidents. This also leads to an increased risk for pedestrians.

III. How People Interact

A. Principle #5: Trade Can Make Everyone Better Off

- Trade is not like a sports competition where one side gains and the other side loses.

- Consider trade that takes place inside your home. Certainly the family is involved in trade with other families on a daily basis. Most families do not build their own homes, make their own clothes, or grow their own food.

- Just like families benefit from trading with one another so do countries.

- This occurs because it allows for specialization in areas that countries (or families) can do best.

B. Principle #6: Markets Are Usually a Good Way to Organize Economic Activity

- Many countries that once had centrally planned economies have abandoned this system and are trying to develop market economies.

- Definition of market economy: an economy that allocates resources through the decentralized decisions of many firms and households as they interact in markets for goods and services.

- Market prices reflect both the value of a product to consumers and the cost of the resources used to produce it. Therefore, decisions to buy or produce goods and services are made based on the cost to society of providing them.

- When a government interferes in a market and restricts price from adjusting decisions that households and firms make are not based on the proper information. Thus, these decisions may be inefficient.

- Centrally planned economies have failed because they did not allow the market to work.

- FYI: Adam Smith and the Invisible Hand

a. Adam Smith’s 1776 work suggested that although individuals are motivated by self-interest, an invisible hand guides this self- interest into promoting society’s economic well-being.

b. Smith’s astute perceptions will be discussed more fully in the chapters to come.

C. Principle #7: Governments Can Sometimes Improve Market Outcomes

- There are two broad reasons for the government to interfere with the economy: the promotion of efficiency and equity.

- Government policy can be most useful when there is market failure.

a. Definition of market failure: a situation in which a market left on its own fails to allocate resources efficiently.

- Examples of Market Failure

a. Definition of externality: the impact of one person’s actions on the well-being of a bystander.

b. Definition of market power: the ability of a single economic actor (or small group of actors) to have a substantial influence on market prices.

c. Because a market economy rewards people for their ability to produce things that other people are willing to pay for, there will be an unequal distribution of economic prosperity.

- Note that the principle states that the government can improve market outcomes. This is not saying that the government always does improve market outcomes.

IV. How the Economy as a Whole Works

A. Principle #8: A Country’s Standard of Living Depends on Its Ability to Produce Goods and Services

- Differences in living standards from one country to another are quite large.

- Changes in living standards over time are also great.

- The explanation for differences in living standards lies in differences in productivity.

- Definition of productivity: the quantity of goods and services produced from each hour of a worker’s time.

- High productivity implies a high standard of living.

- Thus, policymakers must understand the impact of any policy on our ability to produce goods and services.

B. Principle #9: Prices Rise When the Government Prints Too Much Money

- Definition of inflation: an increase in the overall level of prices in the economy.

- When the government creates a large amount of money, the value of money falls.

- Examples: Germany after World War I (in the early 1920s), the United States in the 1970s.

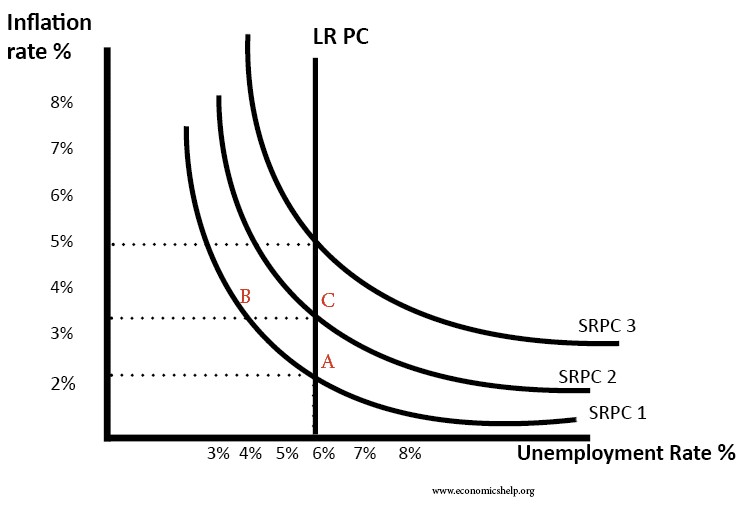

C. Principle #10: Society Faces a Short-Run Tradeoff between Inflation and Unemployment

- Definition of Phillips curve: a curve that shows the short-run tradeoff between inflation and unemployment.

- This is a controversial topic among economists.

- This tradeoff is only temporary but it can last for several years.

- The Phillips curve is important for understanding the business cycle.

- Definition of business cycle: fluctuations in economic activity, such as employment and production.

- Policymakers can exploit this tradeoff by using various policy instruments, but the extent and desirability of these interventions is of continuing debate.

CHAPTER 2 OUTLINE:

I. The Economist as Scientist

A. Economists follow the scientific method.

- Observations help us to develop theory.

- Data can be collected and analyzed to evaluate theories

- Using data to evaluate theories is more difficult in economics than in physical science because economists are unable to generate their own data and must make do with whatever data are available.

- Thus, economists pay close attention to the natural experiments offered by history.

B. Assumptions make the world easier to understand.

- Example: to understand international trade, it may be helpful to start out assuming that there are only two countries in the world producing only two goods. Once we understand how trade would work between these two countries, we can extend our analysis to a greater number of countries and goods.

- One important role of a scientist is to understand which assumptions one should make.

- Economists often use assumptions that are somewhat unrealistic but will have small effects on the actual outcome of the answer.

C. Economists use economic models to explain the world around us.

- Most economic models are composed of diagrams and equations.

- The goal of a model is to simplify reality in order to increase our understanding. This is where the use of assumptions is helpful.

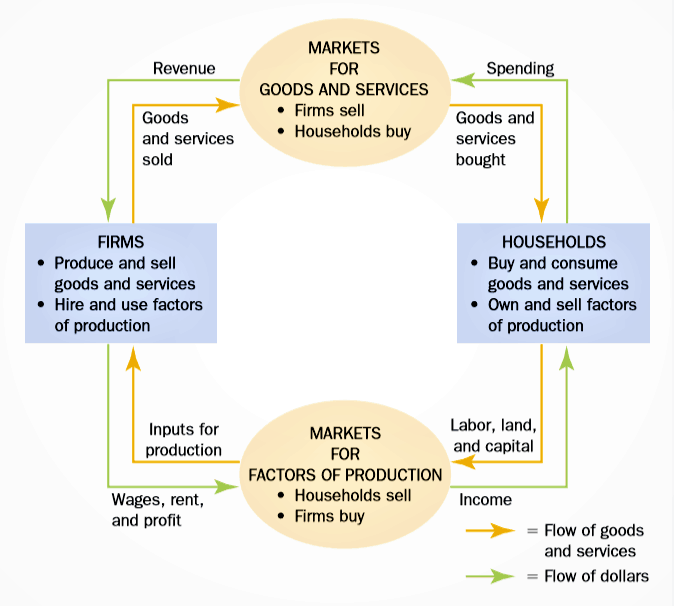

D. Our First Model: The Circular Flow Diagram

- Definition of circular-flow diagram: a visual model of the economy that shows how dollars flow through markets among households and firms.

- This diagram is a very simple model of the economy. Note that it ignores the roles of government and international trade.

a. There are two decision makers in the model: households and firms.

b. There are two markets: goods market and factor market.

c. Firms are sellers in the goods market and buyers in the factor market.

d. Households are buyers in the goods market and sellers in the factor market.

e. The inner loop represents the flows of inputs and outputs between households and firms.

f. The outer loop represents the flows of dollars between households and firms.

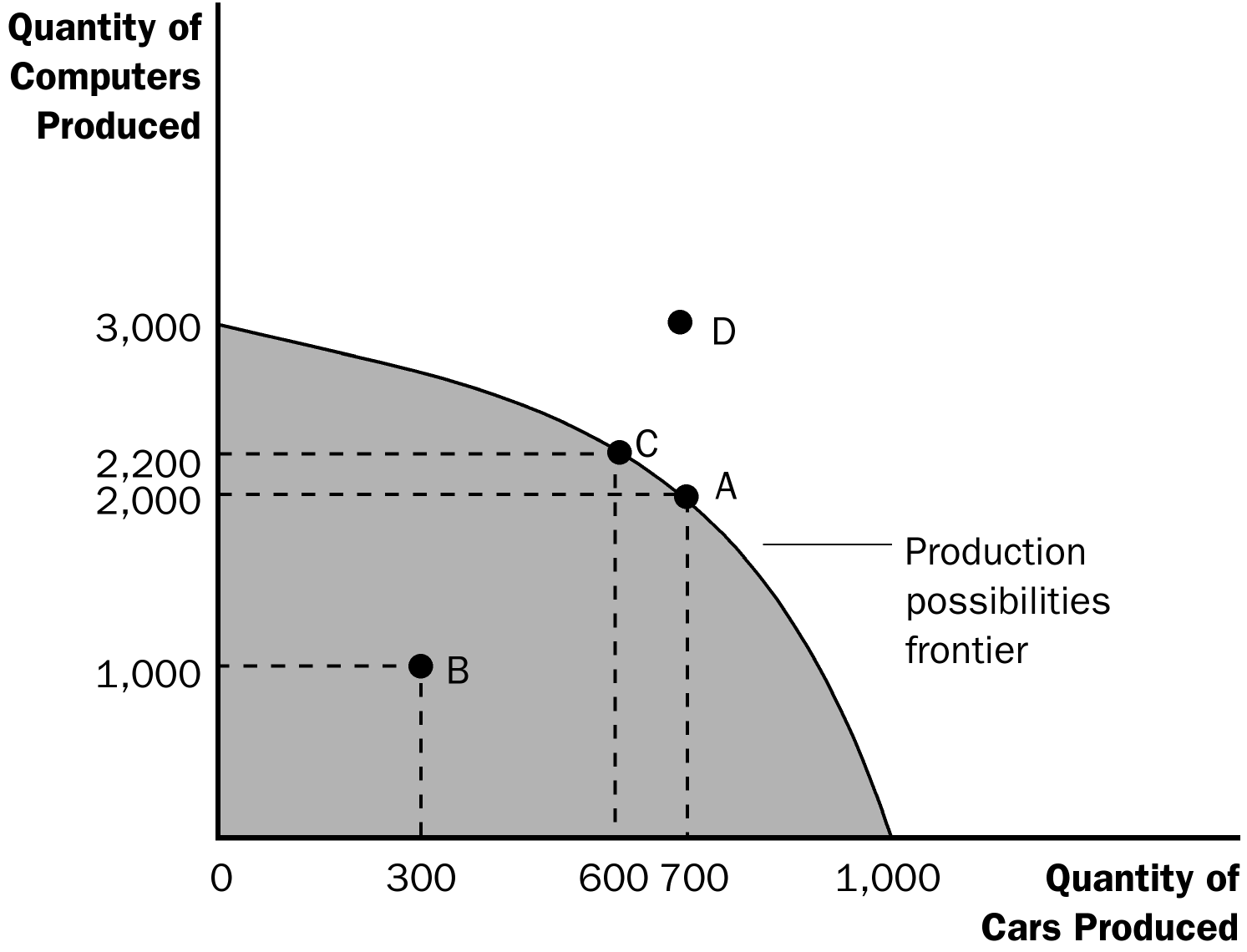

E. Our Second Model: The Production Possibilities Frontier

- Definition of production possibilities frontier: a graph that shows the combinations of output that the economy can possibly produce given the available factors of production and the available production technology.

- Example: a country that produces two goods, cars and computers.

a. If all resources are devoted to producing cars, the economy can produce 1,000 cars and zero computers.

b. If all resources are devoted to producing computers, the economy can produce 3,000 computers and zero cars.

c. If resources are divided between the two industries, the feasible combinations of output are shown on the curve.

- Production is efficient at points on the curve. This implies that the economy is getting all it can from the scarce resources it has available.

- Production at a point inside the curve is inefficient.

- Production at a point outside of the curve is not possible given the economy’s current level of resources and technology.

- The production possibilities frontier reveals Principle #1: People face tradeoffs.

a. Suppose the economy is currently producing 600 cars and 2,200 computers. To increase the production of cars to 700, the production of computers must fall to 2,000.

- Principle #2 is also shown on the production possibilities frontier: The cost of something is what you give up to get it (opportunity cost).

a. The opportunity cost of increasing the production of cars from 600 to 700 is 200 computers.

- The shape of the production possibilities frontier indicates that the opportunity cost of cars in terms of computers increases as the country produces more cars and fewer computers. This occurs because some resources are better suited to the production of cars than computers (and vice versa).

- The production possibilities frontier can shift if resource availability or technology changes.

F. Microeconomics and Macroeconomics

- Economics is studied on various levels.

a. Definition of microeconomics: the study of how households and firms make decisions and how they interact in markets.

b. Definition of macroeconomics: the study of economy-wide phenomena, including inflation, unemployment, and economic growth.

- Microeconomics and macroeconomics are closely intertwined because changes in the overall economy arise from the decisions of individual households and firms.

- Because microeconomics and macroeconomics address different questions, they sometimes take different approaches and are often taught in separate courses.

II. The Economist as Policy Adviser

A. Positive Versus Normative Analysis

- Example of a discussion of minimum-wage laws: Polly says, “Minimum-wage laws cause unemployment.” Norma says, “The government should raise the minimum wage.”

- Definition of positive statements: claims that attempt to describe the world as it is.

- Definition of normative statements: claims that attempt to prescribe how the world should be.

- Positive statements can be evaluated using data, while normative statements involve personal viewpoints.

B. Economists in Washington

- Economists are aware that tradeoffs are involved in most policy decisions.

- The president receives advice from the Council of Economic Advisers (created in 1946).

- Economists are also employed by administrative departments within the various federal agencies such as the Department of Treasury, the Department of Labor, the Congressional Budget Office, and the Federal Reserve. Table 1 lists the World Wide Web addresses of these agencies.

- The research and writings of economists can also indirectly affect public policy.

III. Why Economists Disagree

A. Differences in Scientific Judgments

- Economists often disagree about the validity of alternative theories or about the size of the effects of changes in the economy on the behavior of households and firms.

- Example: some economists feel that a change in the tax code that would eliminate a tax on income and create a tax on consumption would increase saving in this country. However, other economists feel that the change in the tax system would have little effect on saving behavior and therefore do not support the change.

B. Differences in Values

C. Perception Versus Reality

- While it seems as if economists do not agree on much, this is in fact not true. Table 2 contains ten propositions that are endorsed by a majority of economists.

- Almost all economists believe that rent control adversely affects the availability and quality of housing.

- While most economists oppose barriers to trade, the Bush Administration imposed large tariffs on steel in 2002.

Production Possibilities Frontier

CHAPTER OUTLINE:

I. A Parable for the Modern Economy

A. Example: two goods—meat and potatoes and two people—a cattle rancher and a potato farmer (each of whom like to consume both potatoes and meat).

1. The gains from trade are obvious if the farmer can only grow potatoes and the rancher can only raise cattle.

2. The gains from trade are also fairly obvious if, instead, the farmer can raise cattle as well as grow potatoes, but he is not as good at it and the rancher can grow potatoes in addition to raising cattle, but her land is not well suited for it.

3. The gains from trade are not as clear if either the farmer or the rancher is better at producing both potatoes and meat.

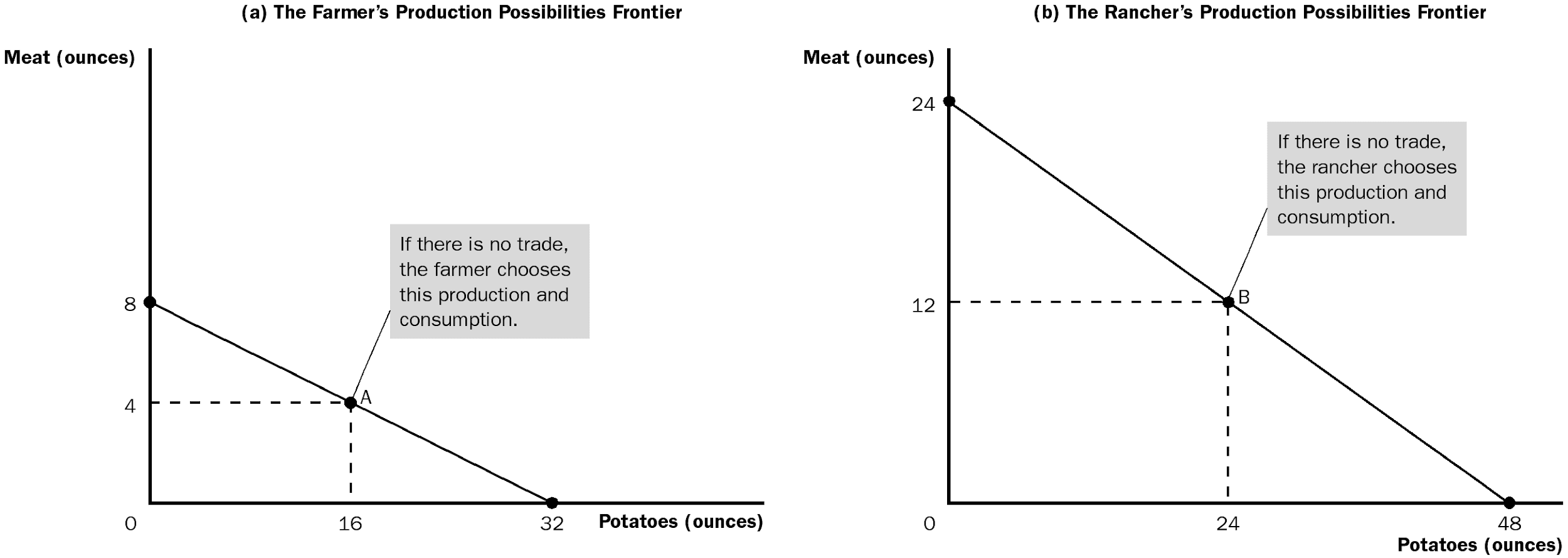

B. Production Possibilities

1. The farmer and rancher both work 8 hours per day and can use this time to grow potatoes, raise cattle, or both.

2. Table 1 shows the amount of time each takes to produce 1 ounce of either good:

| Minutes Needed to Make 1 Ounce of: | Amount Produced in 8 Hours | |

|---|---|---|

| Meat | Potatoes | Meat |

| Farmer | 60 min./oz. | 15 min./oz. |

| Rancher | 20 min./oz. | 10 min./oz. |

3. The production possibilities can also be graphed.

a. These production possibilities frontiers are drawn linearly instead of being bowed out. This assumes that the farmer's and the rancher's technology for producing meat and potatoes allows them to switch between producing one good and the other at a constant rate.

b. As we saw in Chapter 2, these production possibilities frontiers represent the principles of tradeoffs and opportunity costs.

4. We will assume that the farmer and rancher divide their time equally between raising cattle and growing potatoes.

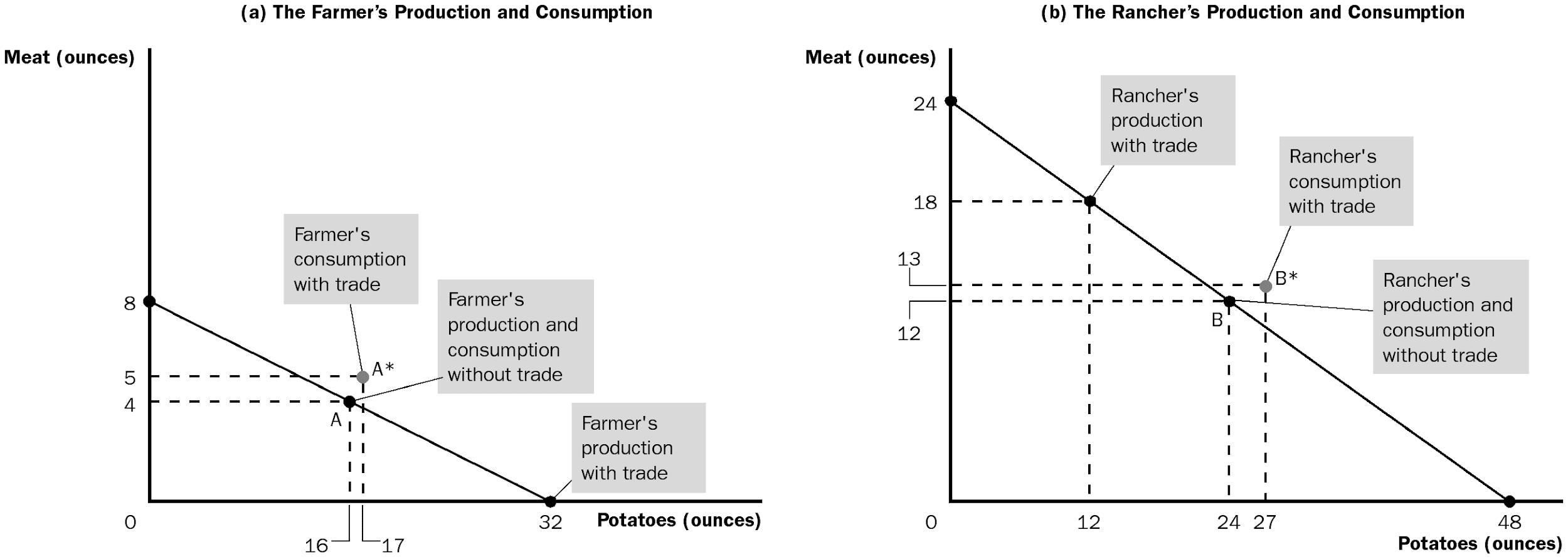

a. The farmer produces (and consumes) at point A—16 ounces of potatoes and 4 ounces of meat.

b. The rancher produces (and consumes) at point B—24 ounces of potatoes and 12 ounces of meat.

C. Specialization and Trade

1. Suppose the rancher suggests that the farmer specialize in the production of potatoes and then trade with the rancher for meat.

a. The rancher will spend 6 hours a day producing meat (18 ounces) and 2 hours a week growing potatoes (12 ounces).

b. The farmer will spend 8 hours a day growing potatoes (32 ounces).

c. The rancher will trade 5 ounces of meat for 15 ounces of potatoes.

2. End results:

a. The rancher produces 18 ounces of meat and trades 5 leaving him with 13 ounces of meat. He also grows 12 ounces of potatoes and receives 15 ounces in the trade, leaving him with 27 ounces of potatoes.

b. The farmer produces 32 ounces of potatoes and trades 15 leaving him with 17 ounces. He also receives 5 ounces of meat in the trade with the rancher.

3. In both cases, they are able to consume quantities of potatoes and meat after the trade that they could not reach before the trade.

II. The Principle of Comparative Advantage

A. Absolute Advantage

1. Definition of absolute advantage: the comparison among producers of a good according to their productivity.

2. The rancher has an absolute advantage in the production of both potatoes and meat.

B. Opportunity Cost and Comparative Advantage

1. Definition of opportunity cost: whatever must be given up to obtain some item.

a. For the rancher, the opportunity cost of producing an ounce of potatoes is ½ ounce of meat (because it takes 10 minutes to produce 1 ounce of potatoes).

b. For the farmer, the opportunity cost of producing 1 ounce of potatoes is only ¼ ounce of meat (because it takes 15 minutes to produce 1 ounce of potatoes).

c. The opportunity cost of producing 1 ounce of meat is the inverse of the opportunity cost of producing 1 ounce of potatoes.

2. Definition of comparative advantage: the comparison among producers of a good according to their opportunity cost.

a. The farmer has a lower opportunity cost of producing potatoes and therefore has a comparative advantage in the production of potatoes.

b. The rancher has a lower opportunity cost of producing meat and therefore has a comparative advantage in the production of meat.

3. Because the opportunity cost of producing one good is the inverse of the opportunity cost of producing the other, it is impossible for a person to have a comparative advantage in the production of both goods.

C. Comparative Advantage and Trade

1. When specialization in a good occurs (assuming there is a comparative advantage), total output will grow.

2. As long as the opportunity cost of producing the goods differs across the two individuals, both can gain from specialization and trade.

a. The rancher buys 15 ounces of potatoes for 5 ounces of meat. The price of each ounce of potatoes is 1/3 ounce of meat. This is lower than the rancher's opportunity cost of ½ ounce of meat and is therefore beneficial to the rancher.

b. The farmer buys 5 ounces of meat with 15 ounces of potatoes. This implies that the price of each ounce of meat is 3 ounces of potatoes, which is lower than the farmer's opportunity cost of 4 ounces of potatoes. Thus, trade also benefits the farmer.

III. FYI: The Legacy of Adam Smith and David Ricardo

A. In Adam Smith's 1776 book An Inquiry into the Nature and Causes of the Wealth of Nations, he writes of the ability of producers to benefit through specialization and trade.

B. In David Ricardo's 1817 book Principles of Political Economy and Taxation, Ricardo develops the theory of comparative advantage and argues against restrictions on free trade.

C. The benefits of free trade are an issue that is generally agreed upon by most economists, and the theories and arguments developed by these two individuals 200 years ago are still used today.

IV. Applications of Comparative Advantage

A. Should Tiger Woods Mow His Own Lawn?

1. Given Wood's athleticism, it is entirely possible that he could mow his lawn faster than most men.

2. This implies that he has an absolute advantage.

3. However, if the opportunity cost of his time is $10,000 (his pay to film a commercial for Nike), it is likely that someone else will have a comparative advantage in mowing his lawn.

4. Both he and the person hired will be better off as long as he pays the individual more than the individual's opportunity cost and less than $10,000.

B. Should the United States Trade with Other Countries?

1. Just as individuals can benefit from specialization and trade, so can the populations of different countries.

2. Definition of imports: goods produced abroad and sold domestically.

3. Definition of exports: goods produced domestically and sold abroad.

4. The principle of comparative advantage suggests that each good should be produced by the country with a comparative advantage in producing that good (smaller opportunity cost).

5. Through specialization and trade, countries can have more of all goods to consume.

6. Trade issues among nations are more complex. Individuals can be made worse off even when the country as a whole is made better off.