CIE AS Level Accounting: Costing

Inventory Valuation

The rule for inventory valuation is that inventory is valued at the lower of cost and net realizable value.

net realizable value = selling price - costs to bring it back to a saleable condition

Methods of inventory valuation include:

First In, First Out (FIFO) | Average Cost (AVCO) | Last On, First Out (LIFO) |

|---|---|---|

method that assumes that the items purchased first will be sold first | method involves recalculating the average cost of inventory (cost per unit) after each new purchase | method that assumes that the items purchased last will be sold first |

each new purchase of inventory must be correctly recorded with its historical cost | current inventory value + value of items purchased / number of units in the inventory | |

advantages of using FIFO include:- closing inventory is based on the most recent prices paid | advantages of using AVCO include:- avoids inequality of identical items being charged differently for similar jobs | advantages of using LIFO include:- reduces the tax liability in periods of rising prices |

disadvantages of FIFO include:- unsuitable for pricing in times of volatile pricing i.e inflation | disadvantages of AVCO include:- suitable only for identical items i.e if older stock needs to go first, it will be harder to identify as all stock has been given the same costs | LIFO is not to be used when making financial reports for a business due to its advantage of reducing tax liability. The International Financing Reporting Standards (IFRS) does not allow LIFO and are, thus, not permissible under the International Accounting Standards (IAS) |

Different inventory valuation methods will affect profit for the year.

In a time of rising prices, the closing inventory valuation using the FIFO method will be higher than using AVCO. As closing inventory is deducted from the cost of sales, the profit using FIFO will be higher than if AVCO is used.

Profits in the long-term will, however, be the same.

Just-in-time, or JIT, is an inventory management method in which goods are received from suppliers only as they are needed. The business will work closely with suppliers to receive raw materials and/or products when they are needed or production has begun. This is to prevent inventory holding costs and increases the rate of inventory turnover of a business.

Perpetual inventory is also a method of inventory valuation, like FIFO and AVCO, that maintains a continuous balance of inventory available after each transaction. Periodic inventory, on the other hand, is a method of inventory valuation that is often used in small businesses that just need a valuation of their inventory at the end of the financial year.

Absorption Costing

Absorption costing is the allocation and apportionment of overheads to relevant cost centres. A cost centre is a production or service location whose costs may be attributed to cost units — units of production or service that absorbs the cost centre’s overhead costs.

There are various costs that need to be defined in absorption costing:

direct costs: costs incurred that directly relate to the production of the good or service; direct costs include:

direct materials, including carriage inwards

direct labour; this is paid for either by:

an hourly rate or wage

how much a worker produces. This is known as the piece rate

a salary

overtime payment, which comes with an overtime premium — the additional amount given to an employee for overtime working e.g time and a half for holiday pay

direct expenses, such as royalties and license fees

indirect costs: costs that aren’t directly linked to the production of the good or service; indirect materials include:

indirect materials purchased for the maintenance of the cost centre e.g cleaning materials, lubricating any oil and machinery

indirect wages for workers in the cost centre that are not directly related to manufacturing e.g supervisors, managers, cleaners

indirect expenses to keep the cost centre running for its purpose e.g rent, lighting, heating, depreciation of machinery

fixed costs: costs that remain unchanged while the level of output/activity increases/decreases e.g rent

relevant range: most fixed costs only remain fixed for a certain period of time

variable costs: costs that change based on the level of output/activity e.g direct materials, direct labour hours

semi-variable costs: costs that have a fixed portion (flat rate) and a variable portion e.g electricity

stepped costs: costs that do not change for a period of time until a certain threshold is reached e.g rent (when a new building/factory is purchased)

sunk costs: expenditure that has already been incurred before a new project is considered

Absorption costing considers all production costs, both fixed and variable. The direct costs are then either allocated to relevant cost centres (production or service departments) while the indirect costs, such as overheads, are apportioned out on a rational basis between the cost centres.

Examples of suitable bases of apportionment can be as follows:

Production overhead | Suitable basis of apportionment |

|---|---|

Heating and lighting (when not separately metered to the cost centres), rent, insurance of buildings | Floor area |

Insurance of plant, machinery, and other assets | Cost or replacement values of assets |

Depreciation | Cost or net book value of assets |

Service cost centre | Basis of apportionment |

|---|---|

Stores | Number or value of inventory orders |

Staff canteen | Number of people |

Building maintenance | Area occupied |

Plant and machinery maintenance | Number or value of machines |

There are two methods of apportioning overheads: the elimination method or the continuous allotment method. The elimination method is also known as the simplified method.

Elimination (Simplified) Method

The elimination method uses bases to apportion their overheads by. Each service department has its overheads apportioned once.

Method

distinguish between production and service departments

decide on the correct bases to be used to apportion the overheads between the departments

e.g if you’re apportioning costs to the canteen department, will you charge by number of employees? Or will you choose another basis?

draw up a schedule to apportion the overheads between all of the departments

complete the schedule by apportioning the total of the overheads of each service department to each of the production departments

total up the overheads for each production department

divide the total for each department by the correct base

overhead absorption rate = budgeted overhead/budgeted (labour or machine) hours

in the OAR equation, the difference between choosing direct labour hours or direct machine hours depends on which one is more labour-intensive

if a manufacturing department uses more labour hours than machine hours (labour intensive vs. machine intensive), use direct labour hours when calculating the OAR

Continuous Allotment Method

Apportionment of each service department continues until the balance in each department reaches zero. This is a more time-consuming method. It is also known as the repeated distribution method.

Once the OAR has been calculated, it is possible to calculate the full cost of a cost unit. However, it is important to note that this method only gives an approximate estimate of what the product actually costs.

Over- and Under-absorption

The OAR is made at the start of a period. During the year, the OAR is then applied to the actual direct labour/machine hours. This will result in either under-absorption of overheads or over-absorption of overheads.

E.g A business has budgeted for 10,000 direct labour hours and $20,000 in overheads.

At the end of the year, they have 8,000 direct labour hours and $18,000 in overheads.

OAR = budgeted overheads/budgeted labour hours = 20,000/10,000 = $2 per direct labour hour

Actual overheads absorped = 2 per direct labour hour * 8,000 direct labour hours = $16,000 in actual overheads

The business spent $18,000 in overhead.

But the overheads absorbed from the OAR only comes to $16,000. This means that the business has under-absorbed by $2,000.

Over- and under-absorption can occur for a number of reasons:

faulty estimation of overheads/quantity of output i.e has the business over/underestimated their productivity for the year?

changes during the financial year that affects productivity

changes in the method of production during the year

over-absorption: actual expenditure is less than budgeted and/or the actual production is more than budgeted

under-absorption: actual expenditure is more than budgeted and/or the actual production is less than budgeted

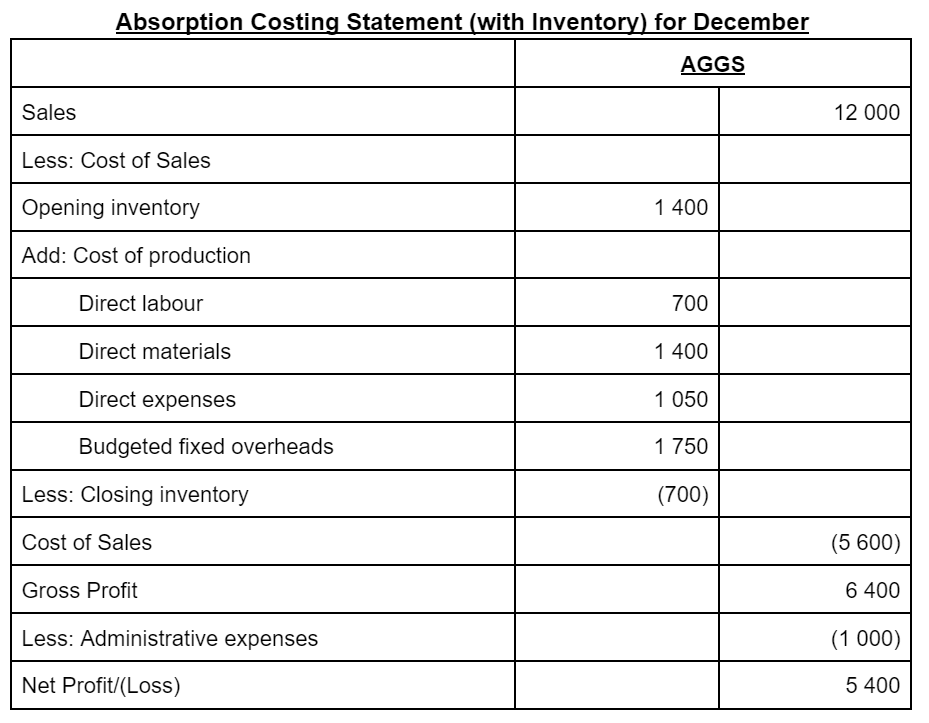

An absorption costing statement will look as follows:

The benfits and limitations of absorption costing include:

Benefits | Limitations |

|---|---|

Absorption costing recognises the fixed costs in the product cost and is therefore suitable for determining the selling price of a product | Absorption costing is not useful for decision-making purposes. In considering fixed costs as part of the product cost, managers will not have a clear understanding of whether accepting a lower price for a product is worthwhile |

Absorption costing conforms to the accruals/matching concept that requires costs to be matched with revenues for a period | Absorption costing is not useful for responsibility accounting. It would be unfair to hold managers responsible for fixed costs over which they had no control. |

Absorption costing avoids the necessity of separating fixed costs from variable costs | |

Absorption costing is the recognised method of inventory valuation |

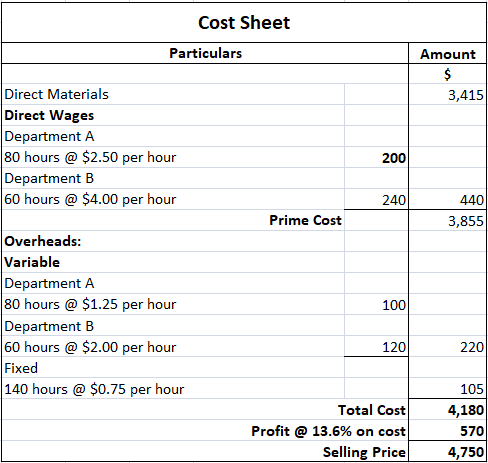

Job and Batch Costing

Job costing is the system which allocates and apportions elements of cost to a job being undertaken to a client’s specific instructions. It assigns production costs to individual units.

It is the appropriate method of product costing when production is not continuous and where each job requires different manufacturing specifications

All costs are recorded on Job Sheets (job cards).

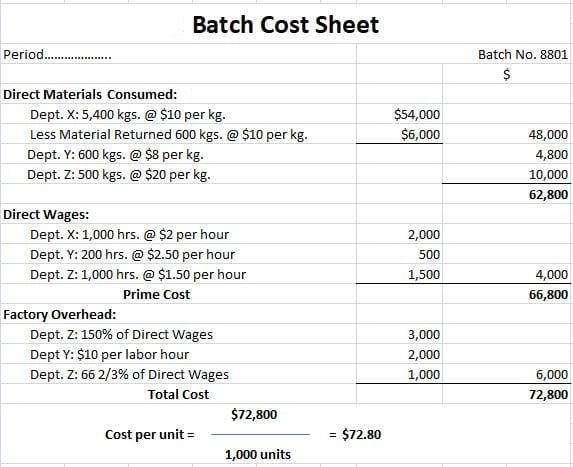

Batch costing is a method of costing used when a number of identical cost units maintain their identity throughout one or more stages of production. It is concerned with making a quantity of units.

It is used when a number of identical units are to be produced for a customer or as a component for another product being manufactured.

Each batch is costed as a job, incurring costs in the same manner. It is then averaged out to give the unit cost.

Marginal Costing

Marginal costing is a method of costing that calculates the cost of producing one extra unit. Marginal costing is used when:

calculating the break-even point for a product

considering whether to make or buy a product

calculating the cost of a special order

a business has a limiting factor that restricts its activities

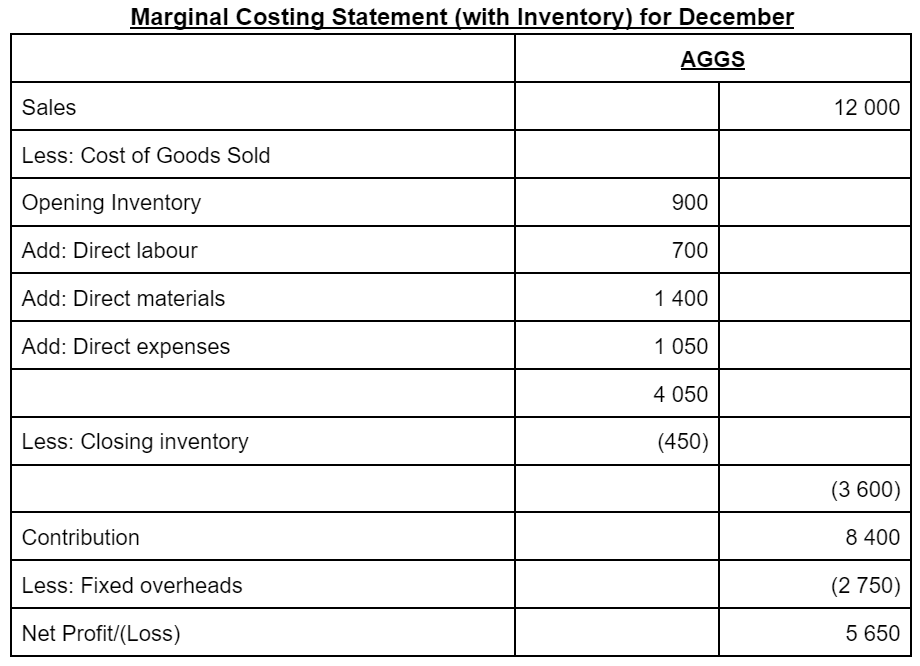

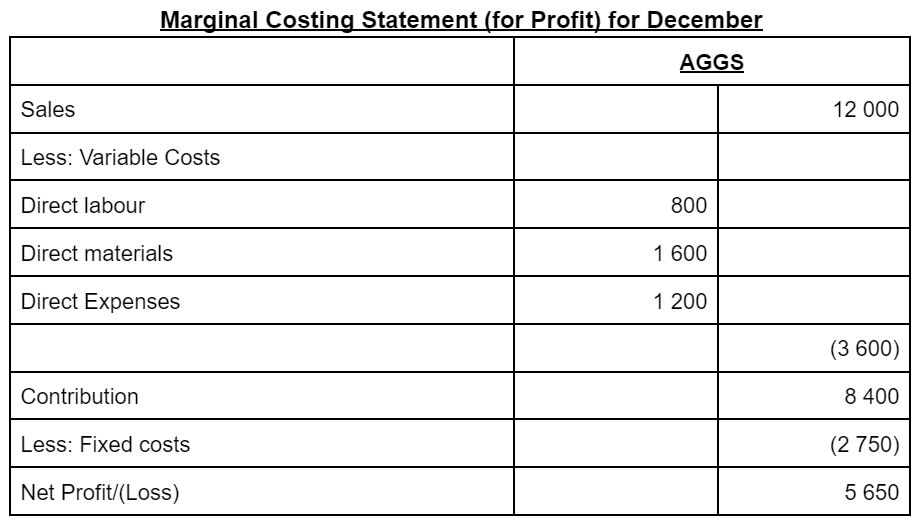

A marginal costing statement will often look like:

Contribution is the money available to pay fixed costs after the business has paid its variable costs. Once these are paid, contribution becomes profit.

To calculate the break-even point, margin of safety, contribution to sales ratio, and level of output to achieve a target profit, the following formulas can be used:

break-even in units = fixed costs/contribution per unit

break-even in sales = fixed costs/contribution per $1 of sales

contribution to sales ratio = (contribution per unit/sales price per unit) * 100

level of output to achieve a target profit = (fixed costs + target profit)/contribution per unit

margin of safety in units = sales in units - break-even in units

margin of safety % = (margin of safety in units/sales) * 100

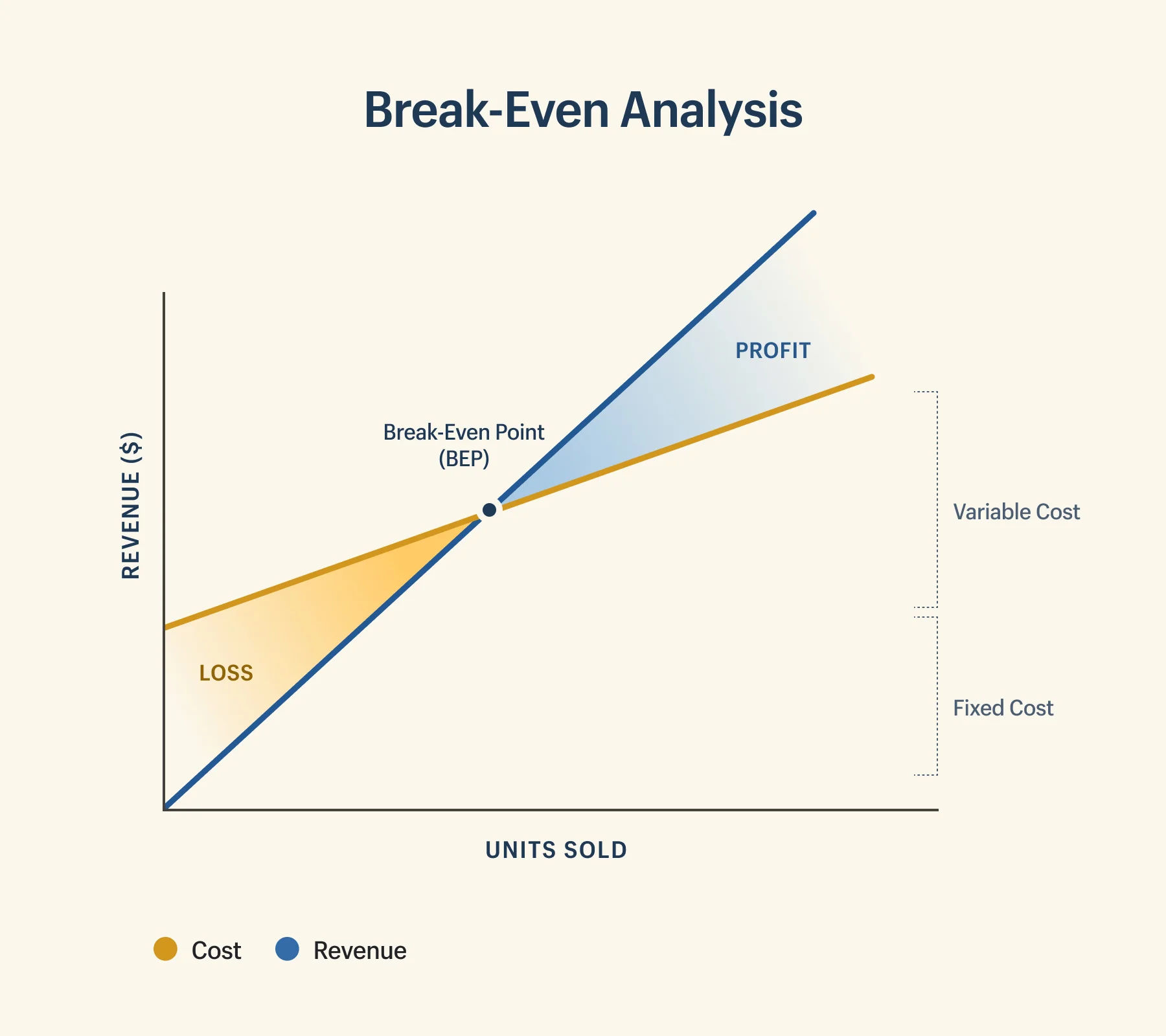

Break-Even Analysis

The break-even point is the level of output at which the business produces neither a profit nor a loss.

The limitations of a break-even analysis include:

it assumes that there are no changes in the levels of inventory

everything that is produced is assumed to be sold

it does not allow product mix

cost behaviour is assumed to be either fixed or variable, so semi-variable costs are not considered

fixed costs are assumed to remain fixed for the whole period of time, so stepped fixed costs are not considered

variable costs are assumed to be perfectly linear with the level of production

the selling price is assumed to remain fixed throughout the year

Make-or-Buy

Businesses make decisions on whether it is cheaper to make the products or buy it from some other suppliers. On a purely financial basis, to make or buy should be based on whether it has positive contribution to the business

Another principle also states that:

if the marginal cost of production is above the price quoted by the supplier, then buy from the supplier

if the marginal cost of production is below the price quoted by the supplier, then make the good

Special Orders

There are occasions when an individual order may be accepted below the normal selling price. This may be considered when there is spare capacity in the factory and other orders are not affected.

For special orders, the general rule is that the selling price must exceed the marginal cost of production. Special orders below the selling price may be useful to maintain production, avoid redundancy, promote new products, and dispose inventory no longer being sold.

Before accepting a special order, a business must consider both the financial and non-financial factors involved:

financial: does the order provide a positive contribution

non-financial;

will the order lead to further orders and expand market share?

is spare capacity being utilised?

will staff have to be retrained to make the product? will they want to be retrained?

will machinery have to be adapted if the specification of the product has been changed?

how reliable is the customer?

how much disruption to the normal trading of the business will take place?

Limiting Factors

Also known as limited resources, a firm can manufacture multiple items of product but may not have enough resources to produce all that they wish to produce. Limiting factors include:

a shortage of materials

a shortage of labour

a shortage of demand for a product

As a result, they must calculate the optimum production plan to maximise profit with the resources available.

Method

calculate the contribution per unit for each product

calculate the contribution per limiting factor e.g per hr, per kg

rank the products in order of the highest contribution per limiting factor down to the lowest contribution per limiting factor

devise a production plan to maximise profits using the rank order

Closure of a Business

Marginal costing is also important to make the decision of whether or not to close a business unit. The business unit might be a department, product, or other profit centre and its closure is typically being considered because it is not profitable.

By closing down a business unit, it may have a negative effect on a business’ profits. As fixed costs remain fixed, regardless of the changes in output, the positive contribution that a business unit makes might have been important in covering fixed costs. Without it, the business may either suffer a loss or make less profit.

Benefits and Limitations of Marginal Costing

Uses | Benefits | Limitations | |

|---|---|---|---|

Marginal Costing | Useful for decision-making as it identifies the extra costs and revenues icurred by the production and sale of an addition unit, for example in relation to make-or-buy decisions, limiting factors. | Easily understood and applied in decision-making, as it is cost-effective. Contribution is identified which is useful, for example, in make-or-buy decisions and where there are limiting factors.Fixed costs are not included in the cost of production and therefore, there is no arbitrary apportionment of fixed costs.Marginal costing clearly shows the impact on profit of fluctuations in the volume of sales.Under- and over-absorption of overheads are not a problem as there is no need to calculate an overhead absorption rate. | Indirect and direct costs are both divided into either fixed or variable. There are no semi-variable or stepped costs taken into account.Fixed costs are not allocated to cost centres and cost units but are regarded as time-based and linked to accounting periods rather than units of output. Marginal costing is only useful for short-term decision making.Inventory should not be valued using marginal costing for a business’ financial reporting because fixed manufacturing overheads are required by IAS 2. Marginal costing may encourage selling prices that are too low because fixed costs are not considered.Marginal costing is most useful for a business that makes a single product. |

Absorption Costing | Useful for decision-making as it includes a portion of fixed costs in each cost units, for example when calculating the selling price using the pricing strategy, full cost plus | All costs are considered, so a total production cost per unit is identified.The effect of an increase in any one cost can be assessed whether direct or indirect | The final basis used to calculate the OAR may not be relevant for all of the overheads in the production department.New technology has led to a reduction in the use of labour hours as a valid basis.If inventory levels decrease, absorption costing records a lower profit than marginal as costs from previous periods are set against income. |

There are also a number of non-financial factors that managers must take into consideration:

customers — a large or important customer might put pressure on a business to provide goods at a special (lower) price. Despite being unprofitable, a business may agree to this in the short-term, in the hope or expectation that the customer will make future purchases at a higher price

human resources — a business may decide to prioritise avoiding staff redundancies. This encourages managers to accept special orders at low prices or to avoid closing a business unit unless staff can be redeployed to other parts of the business

suppliers — if a business has a strong or long-standing relationship with a supplier, then it might prefer not to make a shift from buying to making a product, despite a possible financial gain

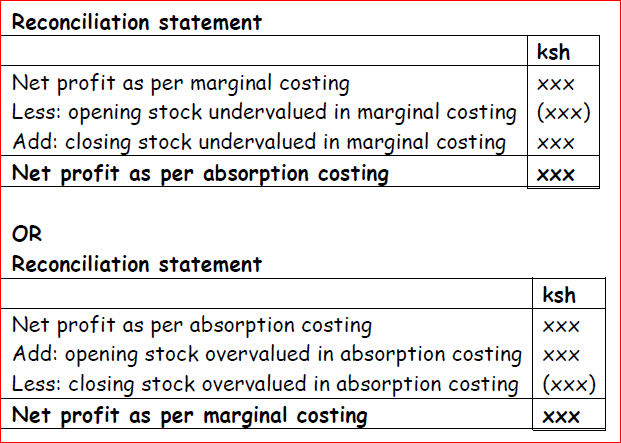

Reconciliation of Marginal and Aborption Costing

Due to the differences in marginal and absorption costing, they will produce different net profit figures. Marginal costing excludes fixed manufacturing costs in the calculate of cost of goods sold (COGS). On the other hand, absorption costing includes fixed manufacturing costs in the calculation of COGS.

As a result, a company may produce a reconciliation statement as shown:

Method

prepare income statements under both methods i.e prepare both a marginal costing income statement and an absorption costing income statement

start reconciliation statement by taking profit from any one costing method

then add or minus over/undervaluation of inventory value to profit

the final profit figure should reconcile