unit 1 exam

decisions in the social media age

imperfect decisions because we don’t have enough data

behavior in markets

1.1 intro to economics

economics: study of how humans make decisions in scarcity

scarcity: human wants for goods, services, and resources exceed availability

resources (labor, tools, land, raw materials, time) necessary to produce

the problem of scarcity

american west is in drought, diminishing water supplies

denver producing campaigns to popularize conservation

division and specialization of labor → production innovation by adam smith

division of labor: production of good or service divided into diff workers

why division of labor increases production

specialization: allows workers with advantage to focus on parts of production

efficiency & quality & innovation → assembly line

core competency: business that focuses on few products

economies of scale: as level of production increases, avg cost of producing individual unit decreases (machinery, specialization, etc)

trade and markets

specialization requires trade (workers get paid for the work they do)

why study economics?

every major global issue (cc, poverty, political conflicts) is economic

economics critical to public policy (voting on budges, regulations)

1.2 micro and macro

microeconomics: individual agents within the economy (households, workers, businesses)

macroeconomics: economy as a whole & broad issues (growth of production, unemployment, inflation, government deficits, GDP)

micro decisions of businesses influenced by health of macroeconomy

firms more likely to hire workers when economy is growing

microeconomics

budgets of households & individuals

goods & services that fit needs & wants of micro agents

decisions on working (fulltime? parttime?)

saving decisions

how do firms decide how to operate their business?

macroeconomics

level of economic activity in society

goals: growth in standard of living, low unemployment/inflation

monetary policy: central bank’s policies that affect bank lending, interest rates, financial capital markets

fiscal policy: nations’s legislative body that involves government spending and taxes

1.3 theories and models

keynes (20th c): economics is a method of thinking

theory: simplified rep of how variables interact in an issue

model: applied/empirical rep to test theories

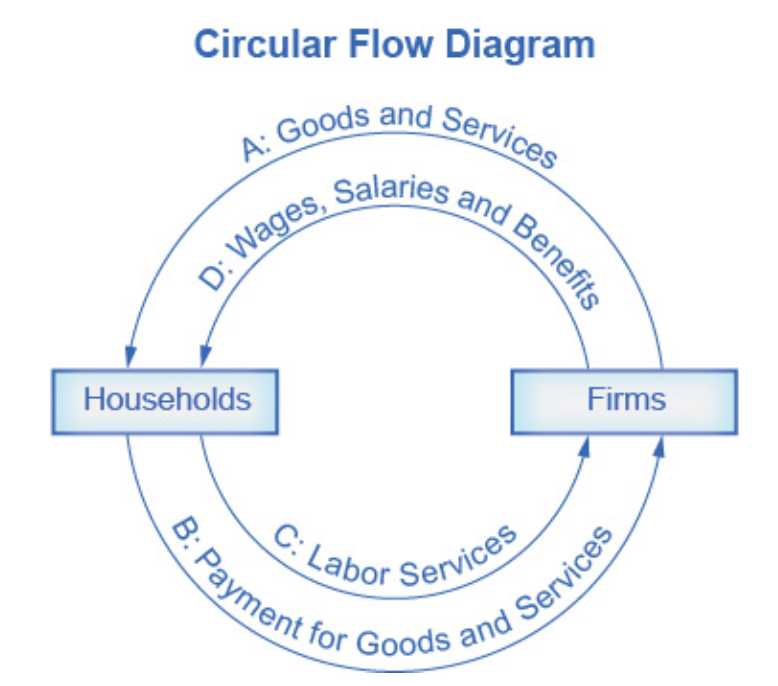

circular flow diagram: economy has households & firms in the goods and services market (firms sell, households buy) and labor market (households sell, firms buy)

labor and resources: land, capital, raw materials

1.4 economic systems

traditional economy: oldest economic system, little development, occupations in family, produce what you consume.

command economy: ruler/government determines what goods/services are produced and their prices. decides methods of production & wages for workers. provides necessities (healthcare + education). cuba & noko.

market economy: decentralized decision-making.

market: institution that brings together buyers & sellers of goods/services. new york stock exchange.

private enterprise: private individuals own and operate means of production (resources & businesses).

most economies are mixed

regulations

protect private property, prevent violence/fraud, legal contracts, collect taxes

underground economies: black markets of highly regulated economies

the rise of globalization

globalization: expanding cultural, political, economic connections

increased buying & selling of goods, services, assets across borders

international trade & financial capital flows

causes

improvements in shipping (container/cargo ships)

lower transportation costs

innovations in computing & telecommunications for management & sales

international agreements & treaties for greater trade

exports: goods & services one produces domestically, sells abroad

imports: goods & services one produces abroad, sells domestically

gross domestic product: measure of size of total production in economy

exports/gdp: share of country’s total economic production sold overseas

US below global avg - keep division of labor inside borders

Smaller economies need to trade to take adv of division of labor, specialization, and economies of scale

pushback against globalization: loss of jobs, political sovereignty, increased economic inequality (brexit, trump election)

chapter 1 review

what is economics and why is it important?

solves the problem of scarcity

modern economy displays division of labor

agents focus on areas of advantage (natural factors, skill levels)

encourages agents to learn and invent

agents take advantage of economies of scale

division & specialization of labor only work when individuals can purchase what they don’t produce in markets

microeconomics & macroeconomics

different perspectives on the economy

microeconomic: parts of the economy (individuals, firms, industries)

macroeconomic: growth in standard of living, unemployment, inflation → monetary & fiscal policy

how economists use theories & models to understand economic issues

theory isn’t an illustration of the answer to a problem

theory is a tool for determining the answer

how to organize economies: overview of economic systems

traditional, command, market-oriented economies

most societies are a mix

globalization evolves as a result of growth in commercial & financial networks

makes businesses and workers from different economies interdependent

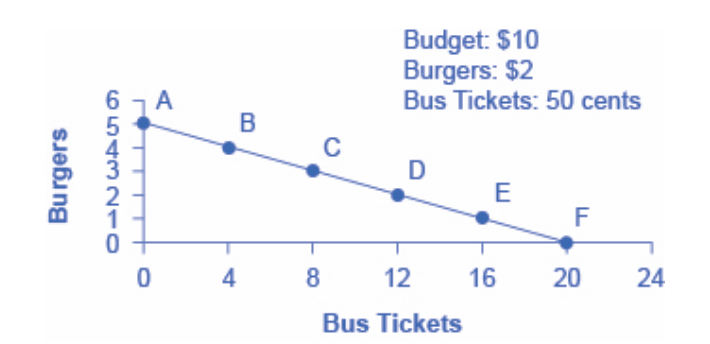

2.1 choices & budget constraint

consumption choice opportunity frontier: relative price of burgers and bus tickets determines slope of budget constraint

opportunity cost: what one must give up to obtain what is desired

cost of one item is lost opportunity to consume something else, value of next best alternative

budget = P_1 \times Q_1 + P_2 \times Q_2

P and Q are price and quantity of items purchased

budget is amount of income available to be spent

slope is the opportunity cost of good on horizontal axis

identifying opportunity cost

opportunity cost = price

marginal decision-making & diminishing marginal utility

marginal analysis: examining benefits & costs of choosing a little more or less of a good, change analysis

utility: satisfaction that goods and services desired provides

the more of some good one consumes, the more utility one obtains

law of diminishing marginal utility: as a person receives more of a good, the additional (marginal) utility from each additional unit of the good declines

a rational consumer will only purchase additional units of some product as long as the marginal utility exceeds opportunity cost

sunk costs

sunk costs: costs that were incurred in the past and cannot be recovered, shouldn’t affect current decision

focus on marginal costs and benefits of current/future options

from a model with two goods to one of many goods

budget constraint diagram with two goods isn’t realistic

modern economy: thousands of goods

draw multiple budget constraints

show possible tradeoffs between many pairs

2.2 production possibilities frontier

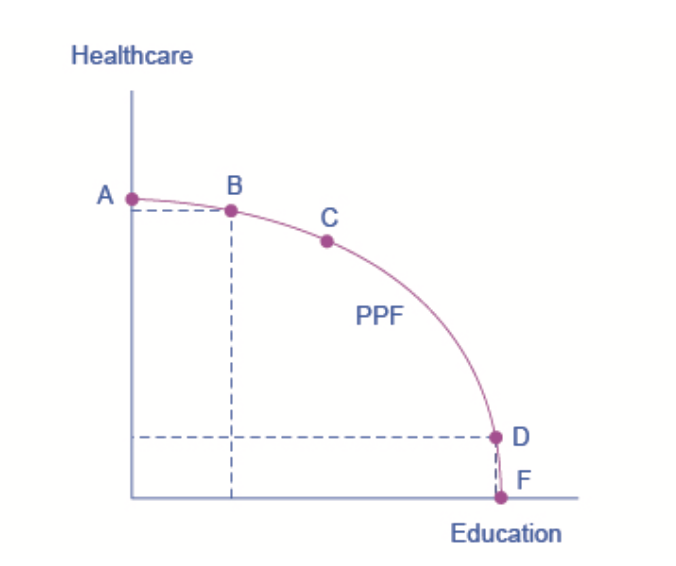

production possibilities frontier (ppf): model that explains the constraints society faces

limited resources (labor, land, capital, raw materials)

limit to quantities of goods and services it can produce

slope: opportunity cost

differences between budget cost & ppf

budget constraint is straight line

slope is relative prices of two goods

pov of individual consumer is fixed

ppf has curved shape bc of law of diminishing returns

ppf has no numbers bc no exact # of resources

the shape of the ppf and law of diminishing returns

consumption budget constraint: relative prices of two goods determines slope of budget constraint

law of diminishing returns: additional increments of resources are added to a certain purpose, marginal benefit from additional increments will decline

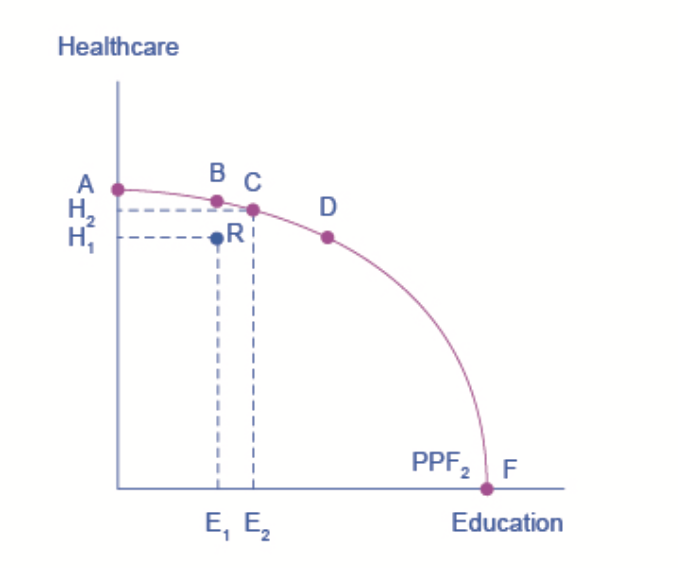

productive efficiency and allocative efficiency

economics doesn’t tell society what choices it should make

in market-oriented economy w democratic government, choices made from decisions of individuals, firms, government

efficiency: lack of waste

productive efficiency: given available inputs & tech, it’s impossible to produce more of good without decreasing quantity produced of another good

allocative efficiency: particular combination of goods & services on production possibility curve that society produces = combination that society desires

producers supply quantity of each product consumers demand

why society must choose

as resources grow (more labor, capital), economy grows

ppc shifts outwards

government tradeoffs

market economy coordinates process in which firms seek to produce goods and services in the quantity, quality, price that people want

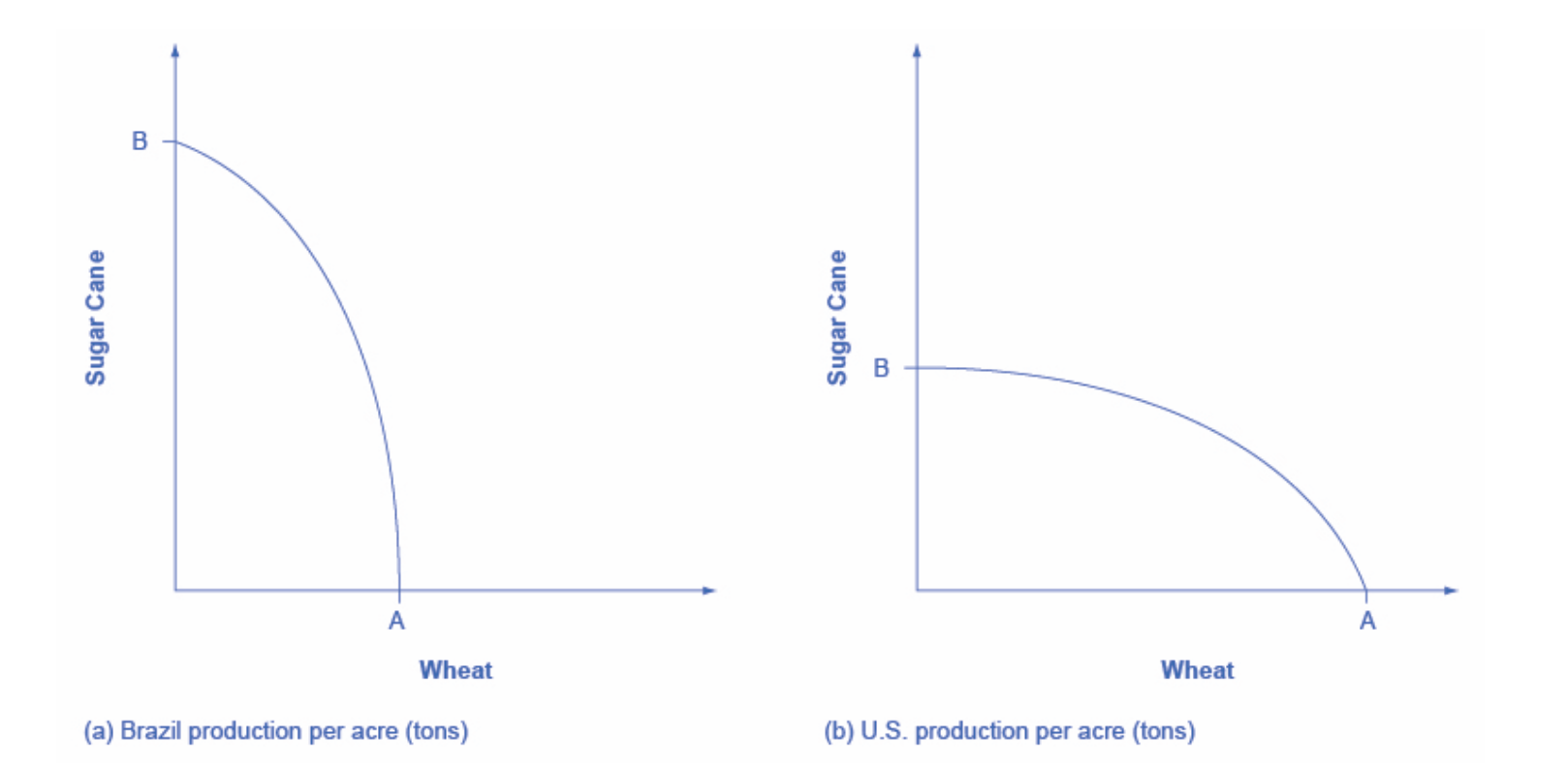

ppf and comparative advantage

countries tend to have different opportunity costs of producing

climates, geography, tech, skills

US PPF flatter = opportunity cost of wheat lower in the US

comparative advantage: country can produce a good at a lower opportunity cost than another country

international trade: countries’ differences in comparative advantage determine which goods they’ll produce and trade

manufacturers produce goods where opportunity cost is lowest, total production increases

2.3 objections to econ approach

first objection: people, firms, society don’t act like this

economic approach requires information & decision-making

maximizing utility? PPFs analysis? no.

approximation through economic analysis

second objection: people, firms, society shouldn’t act like this

self-interest isn’t moral

positive statements: describes world as it is

normative statements: how the world should be

freedom about economic choices

self-interested behavior → positive social results

economic output

invisible hand: consumers encourage businesses to offer goods and services to meet their needs

diagrams

consumption budget constraint = production possibilities frontier

tradeoff diagram illustrates scarcity, tradeoffs, econ efficiency

tradeoff: determined by relative prices of good

chapter 2 review

2.1 how individuals make choices based on their budget constraint

economic behavior involves tradeoffs in which individuals, firms, society forgo something they desire to obtain more desired

budget constraint (frontier of opportunity set) illustrates choices

relative price of choices determines slope of budget constraint

opportunity cost measures cost by what we forgo in exchange

economic decisions involve marginal analysis

law of diminishing marginal utility = more is less

sunk costs should be disregarded in making current decisions

2.2 production possibilities frontier and social choices

set of choices society faces for combination of goods and services

shape of ppf curved outward, not straight

all choices along ppf display productive efficiency (society’s resources to produce more of one good w/o decreasing production)

curvature differs by country, comparative advantage in diff goods

2.3 confronting objections to the economic approach

useful approach to understanding human behavior

positive vs normative statements & analysis

3.1 demand, supply, equilibrium

demand for goods and services

demand: amount of some good or services consumers are willing and able to purchase at each price

needs, wants, ability to pay

price: what buyer pays for a unit of specific good/service

quantity demanded: total # units consumers purchase at price

rise in price decreases quantity demanded

law of demand: inverse relationship

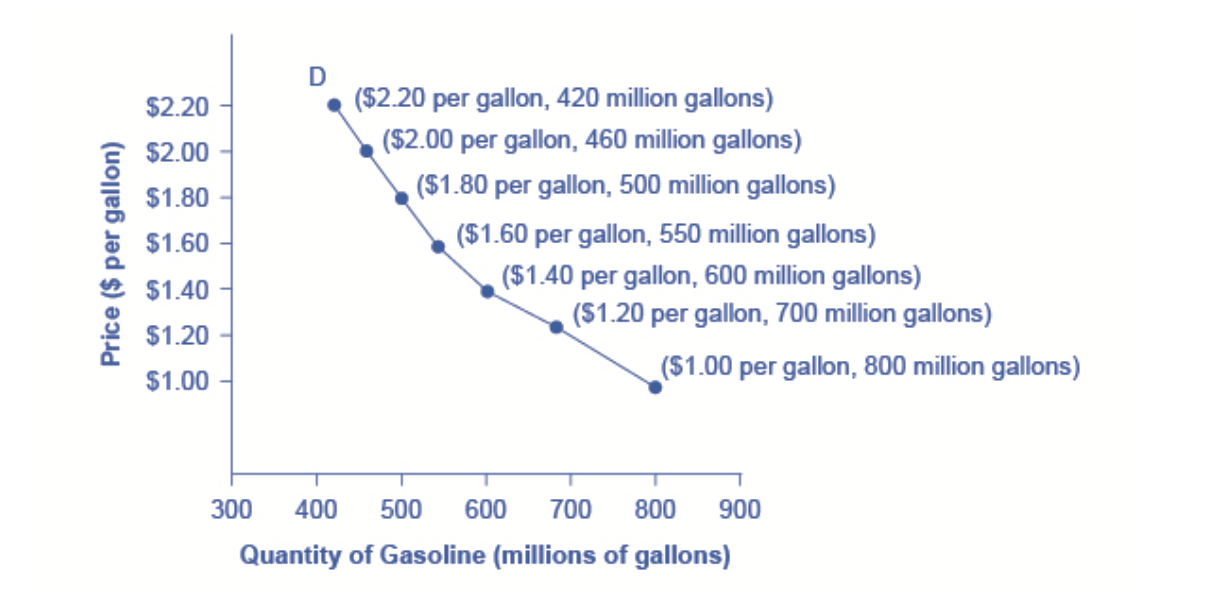

demand schedule: table that shows quantity demanded at each price

demand curve: relationship between price and quantity demanded on a graph, quantity horizontal axis, price per gallon vertical axis

demand curves slope down from left to right

law of demand: price increase, quantity demanded decrease

demand ≠ quantity demanded

demand: relationship b/w range of prices and quantities demanded at those prices (demand curve/schedule)

quantity demanded: point on demand curve

supply of goods and services

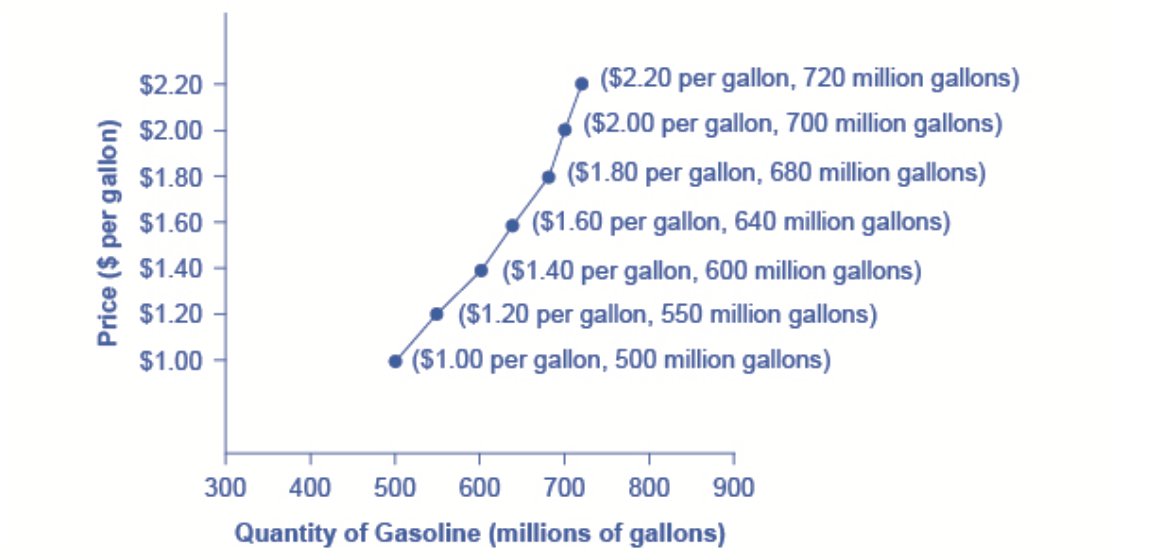

supply: amount of some good or service producer is willing to supply at each price

price: what producer receives for selling one unit

quantity supplied: rise in price causes increase

law of supply: positive relationship between price and quantity supplied

supply schedule: table that shows quantity supplied at different range of prices

supply curve: graph of relationship between price & quantity

supply curves slope up from left to right (law of supply)

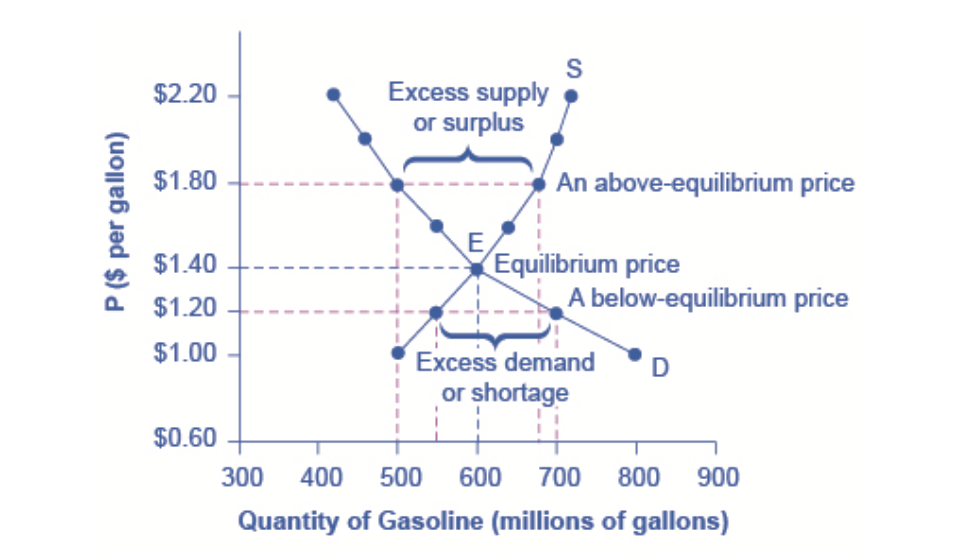

equilibrium - where demand and supply intersect

demand & supply determine price & quantity bought & sold in markets

equilibrium price: only price where plans of consumers and plans of producers agree

equilibrium quantity: amt product consumers want to buy (quantity demanded) = amt producers want to sell (quantity supplied)

economic pressures move market toward equilibrium

excess supply (surplus): quantity supplied > quantity demanded

excess demand (shortage): quantity demanded > quantity supplied

3.2 shifts in s&d

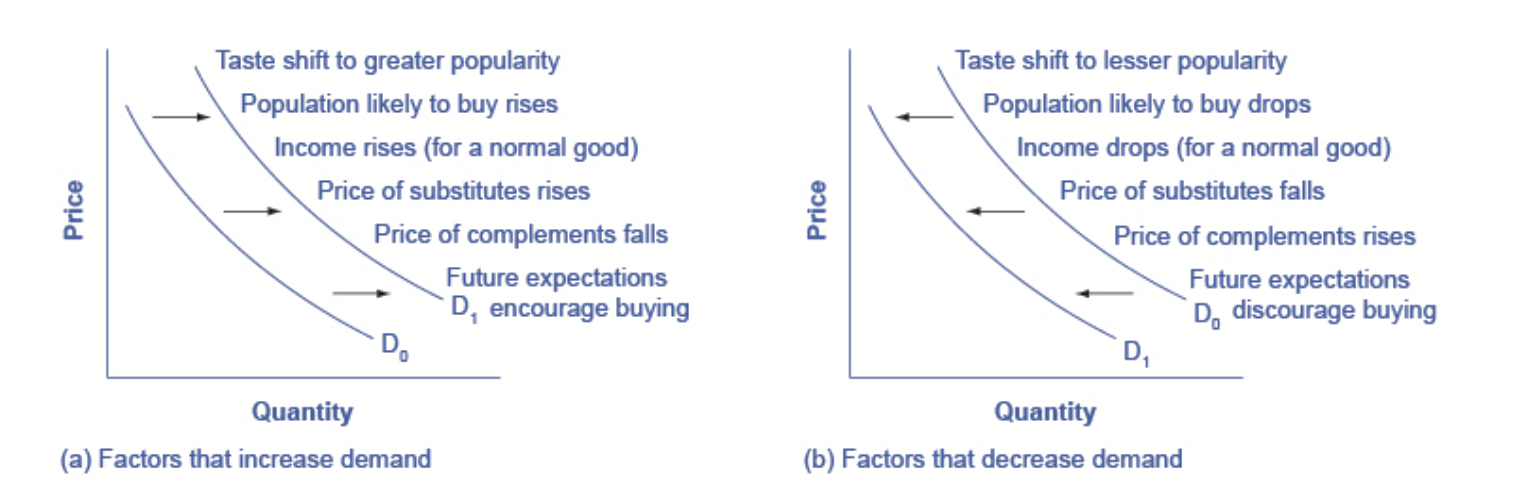

what factors affect demand?

price

willingness to purchase (tastes & preferences)

ability to purchase (income)

prices of related goods

size or composition of population (demographics)

the ceteris paribus assumption

ceteris paribus: “other things being equal”

s&d curve with all other factors held equal

all other variables constant

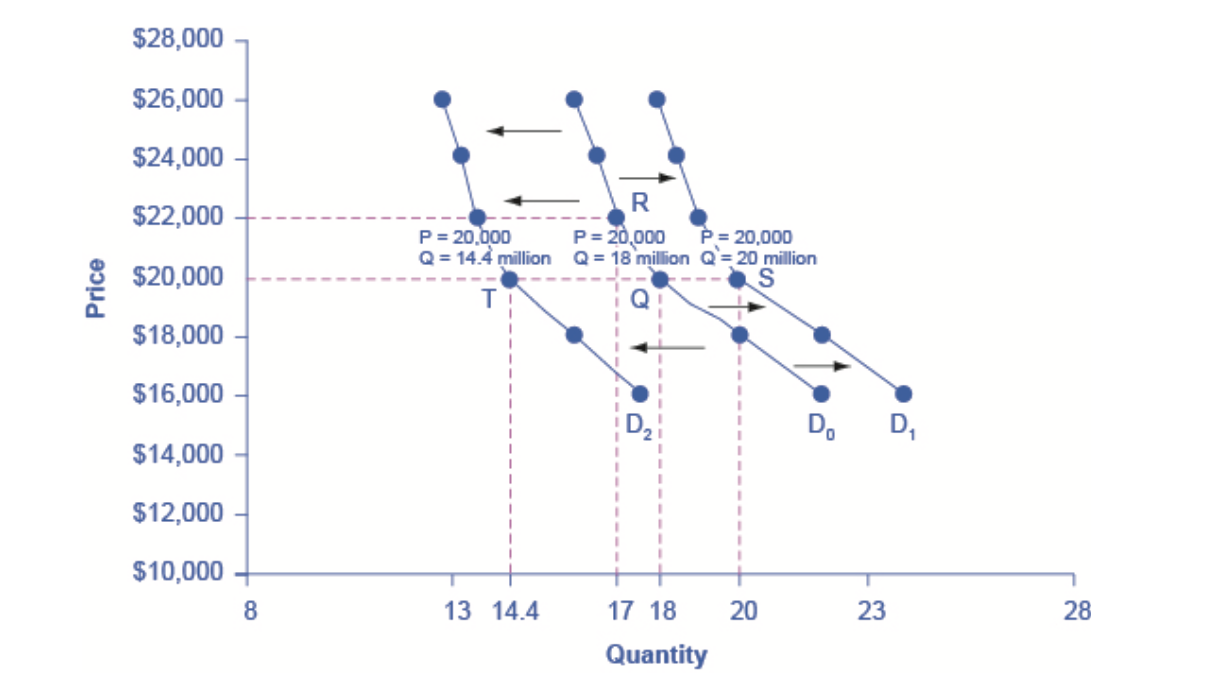

how does income affect demand?

D0 shows initial demand

quantity demanded increases to point S with higher incomes

demand curve shifts to D1

D0 → D2 is decrease in demand due to slowdown in econ

shift in demand curve captures pattern for market as a whole

normal good: product whose demand rises when income rises

inferior good: product whose demand falls when income rises

other factors that shift demand curves

changing tastes or preferences: change quantity of good demanded at every price (shift demand curve)

changes in composition of population: shift in demand curve

substitute: good/service that we can use in place of another good/service

complement: goods that are used together

changes in expectations: about future price (or expectations about tastes and preferences, income, etc.)

shift in demand: happens when a change in some economic factor (other than price) causes different quantity to be demanded at every price

summing up factors that change demand

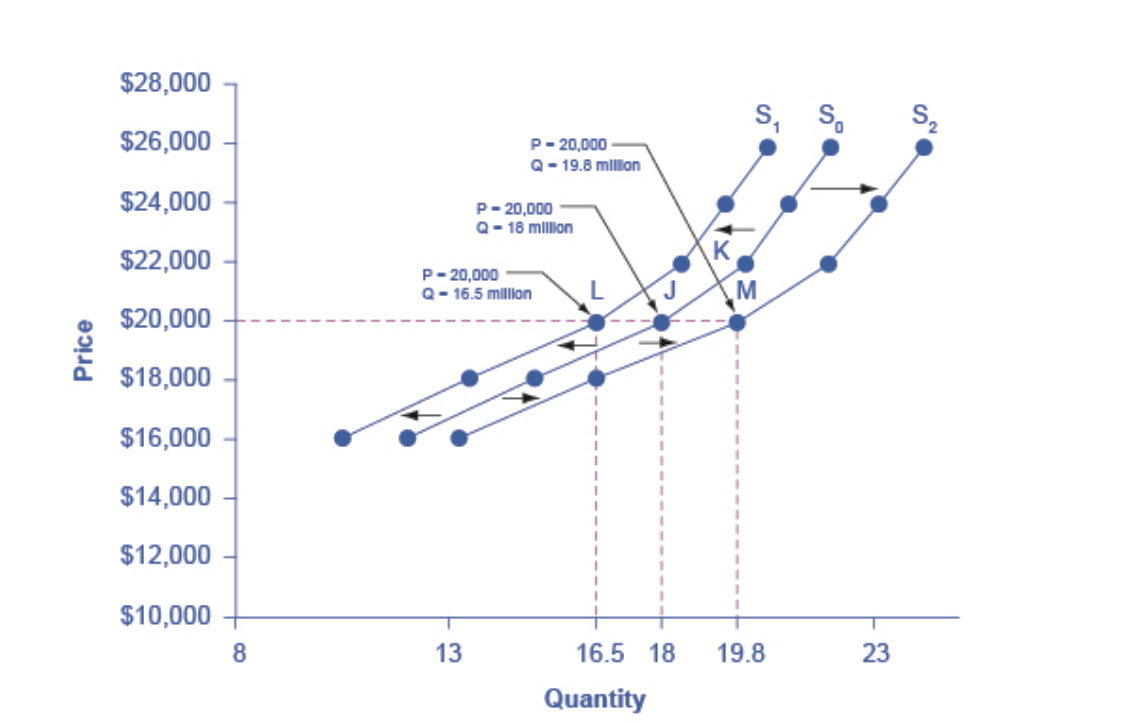

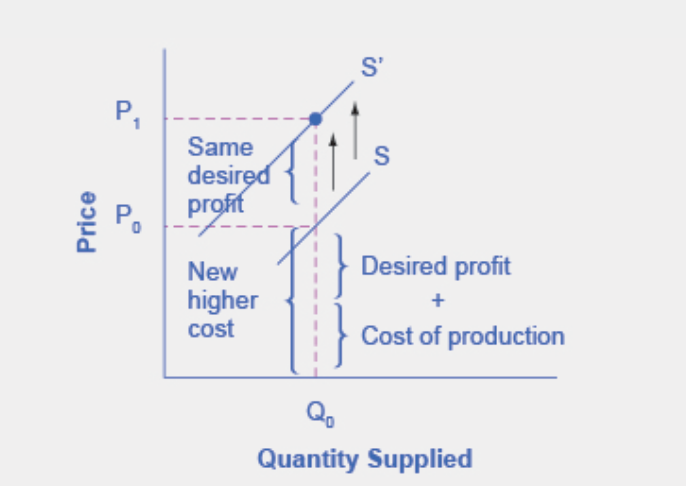

how production costs affect supply

shift in supply: change in quantity supplied at every price

inputs/factors of production: firm produces goods and services using combinations of labor, materials, and machinery

lower costs of production, prices unchanged, profits up, supply up, so supply curve shifts to the right

S0 → S1 : decreased supply (bc steel price up)

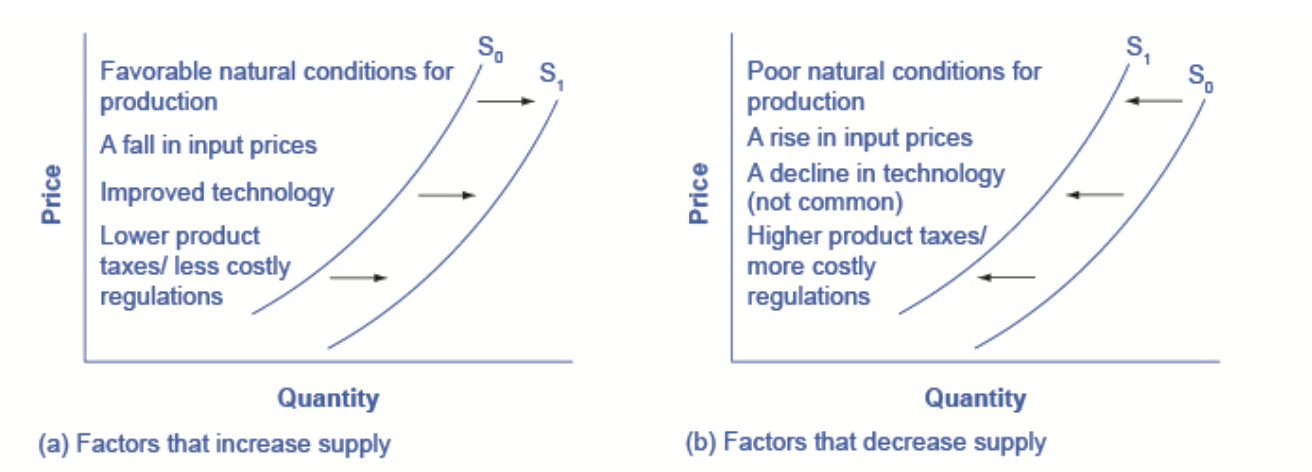

other factors that affect supply

changes in prices of inputs in production process affect cost of production → affect supply

changes in weather/natural conditions: agricultural products

new technologies for production: green revolution → right

government policies: taxes, regulations, subsidies

increase in cost causes upward (or leftward) shift of supply curve

summing up factors that change supply

3.3 changes in eq price & quantity

how does an economic event affect equilibrium price and quantity?

draw demand & supply model before economic change

law of demand: slope of demand curve

law of supply: slope of supply curve

shift variables for demand

shift variables for supply

find initial equilibrium values for price & quantity

decide whether economic change affects demand or supply

decide whether effect on demand or supply causes curve to shift right or left, sketch new curve

identity new equilibrium

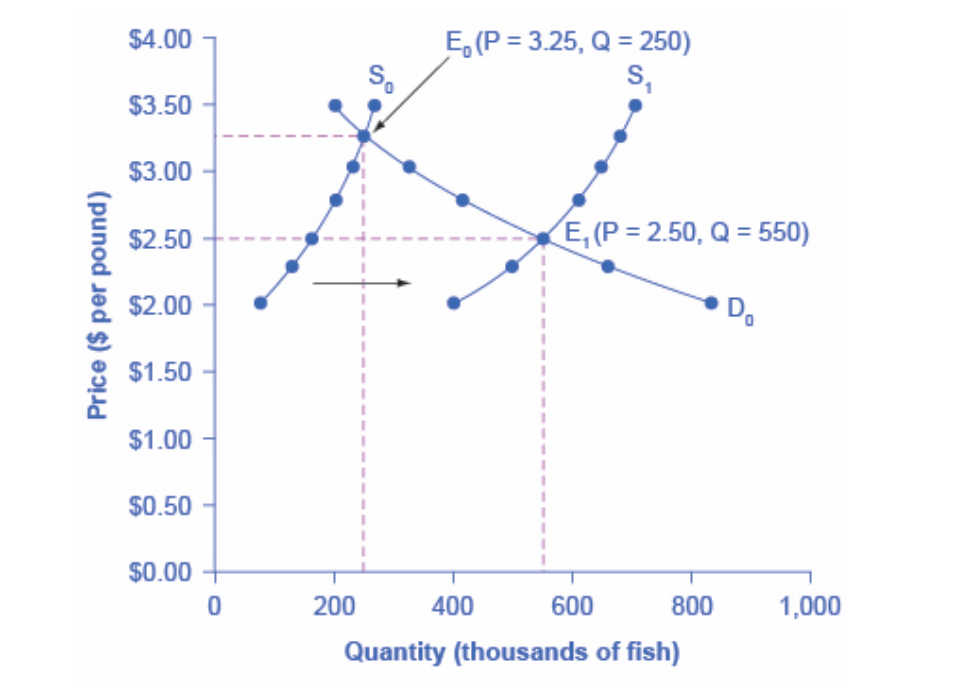

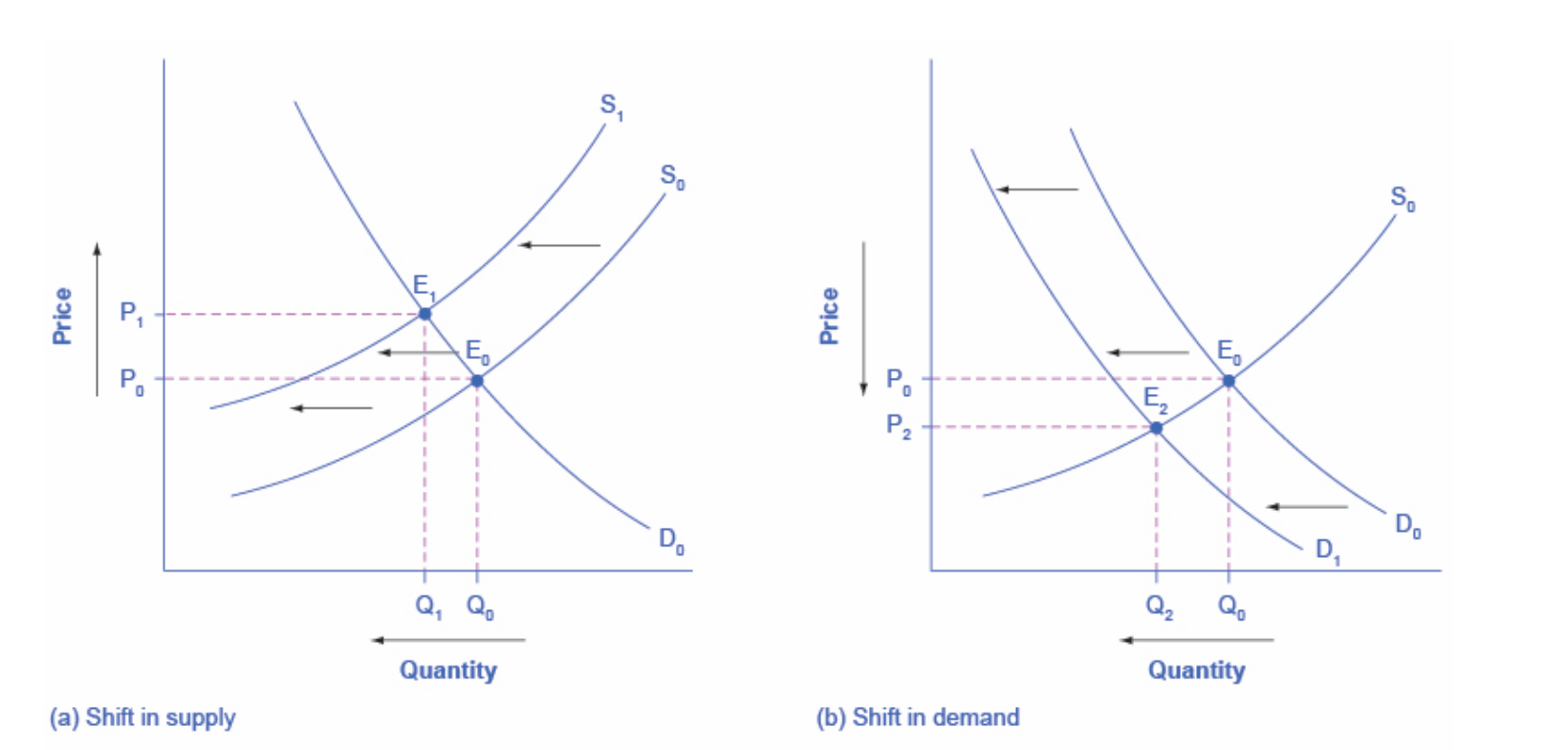

good weather for salmon fishing

weather conditions excellent for commercial salmon fishing

draw demand & supply model to illustrate market for salmon before good weather conditions

good weather affects supply

supply curve shifts to the right

compare equilibrium prices (higher quantity, lower price)

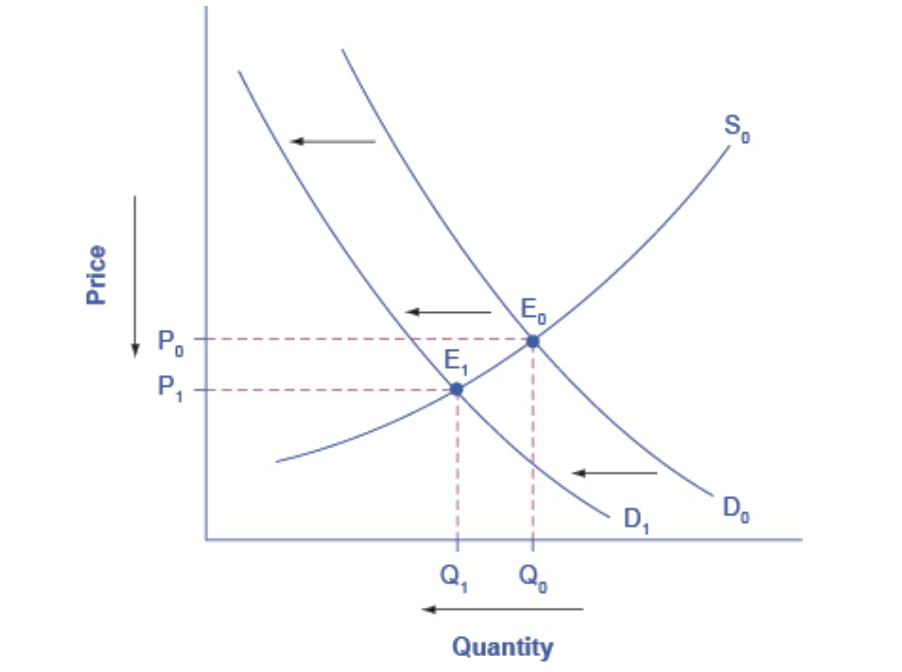

newspapers and the internet

tastes from print news → digital sources

demand and supply model in before market

change in tastes causes change in demand

lower quantity demanded, shift to left

new equilibrium (lower quantity, lower price)

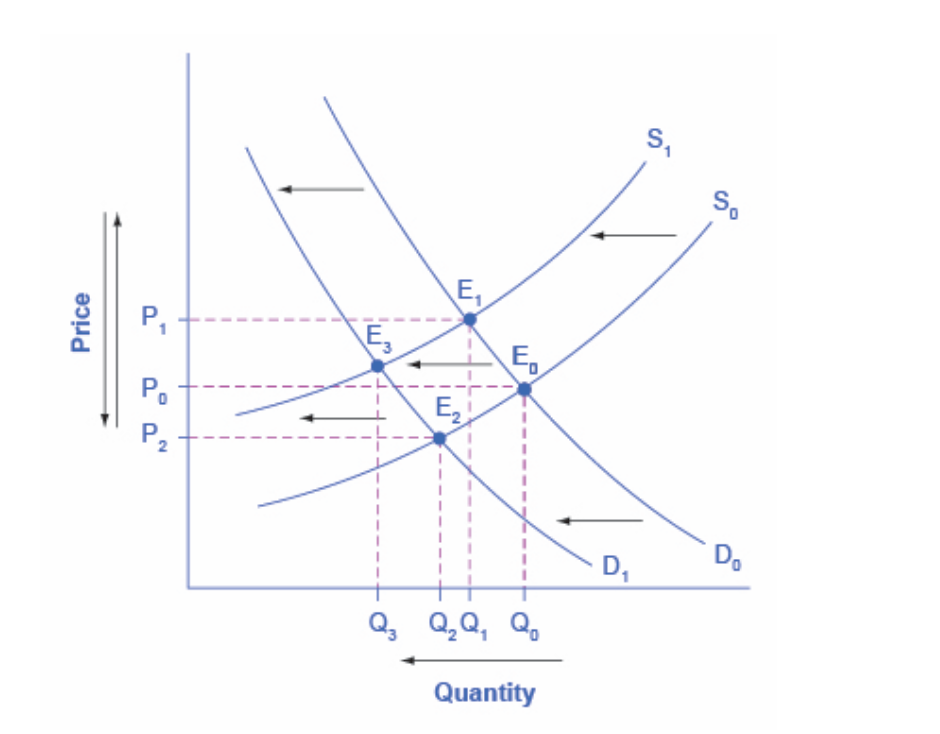

interconnections and speed of adjustments in real markets

demand for cars up bc of rising incomes & population

decrease bc of rising gas prices (complementary good)

supply for cars increase bc of innovative new tech

decrease bc of new gv regs requiring pollution tech

ceteris paribus assumption

combine analyses to see net effect

combined example

postal service

a) higher labor compensation → leftward shift in supply curve, decrease in equilibrium quantity, increase in equilibrium price

b) change in tastes away from postal services → leftward shift in demand curve, decrease in equilibrium quantity, decrease in equilibrium price

effect on quantity: decrease in equilibrium quantity

effect on price: unclear

difference between shifts of demand or supply vs movements

drought shifts back supply curve of crops

lower equilibrium quantity, higher equilibrium price

higher or lower price never shifts supply curve

price change leads to movement along supply curve

3.4 price ceilings & floors

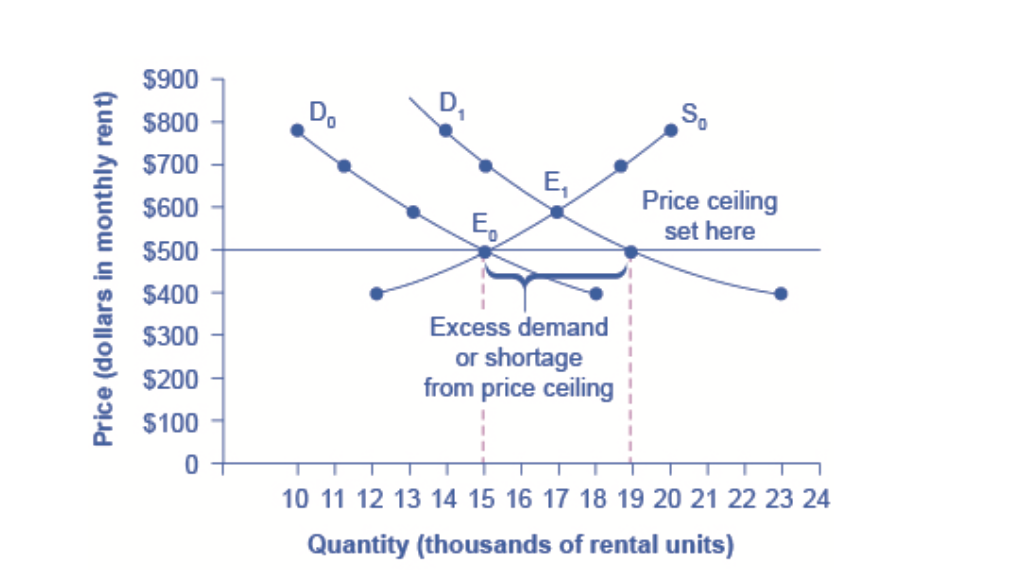

price ceilings

price controls: laws that government enact to regulate prices

price ceilings: keep price from rising above certain level

price floor: keep price from falling below given level

price ceiling: legal max price one pays for some good/service

keep prices affordable

rent control in urban areas (ny, dc, san francisco)

landlords spend less on maintenance and essentials

you do not get something for nothing (opportunity cost)

“cheaper” housing than market requires = lower quality

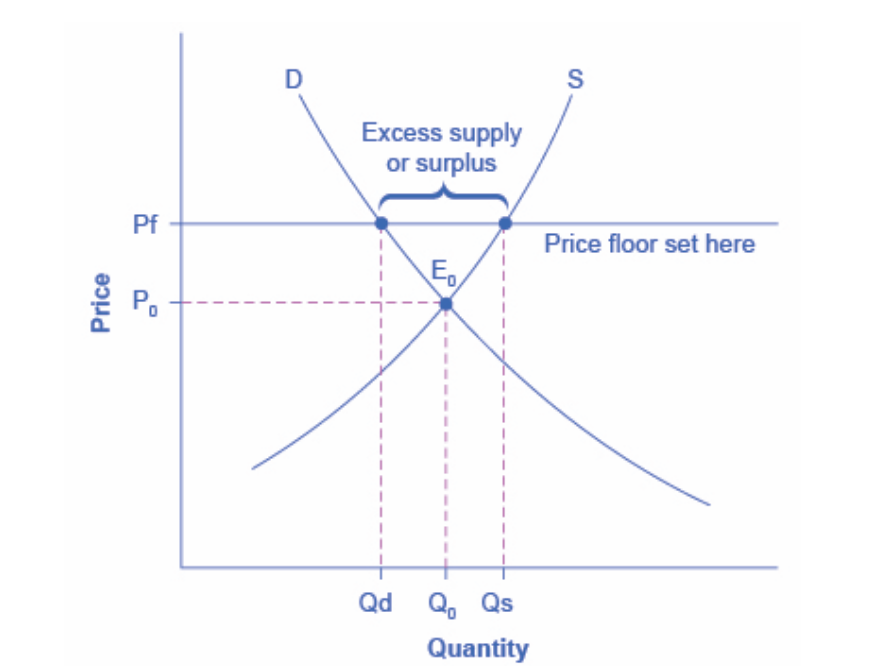

price floors

price floor: lowest price one can legally pay for good/service

minimum wage: full time worker should afford basic standard of living

as cost of living rises, congress raises federal min wage

“price supports”: government enters market and buys product

adding demand to keep prices higher

quantity supplied in excess of quantity demanded

in high-income areas (us, europe, japan) spend 1b per day supporting farmers

taxpayers and consumers of food pay costs

3.5 demand, supply, efficiency

efficiency: impossible to improve situation of one party wo imposing cost on another

efficiency in d&s model: economy getting as much benefit as possible from scarce resources, all possible gains from trade achieved (optimal amt good and service produced, consumed)

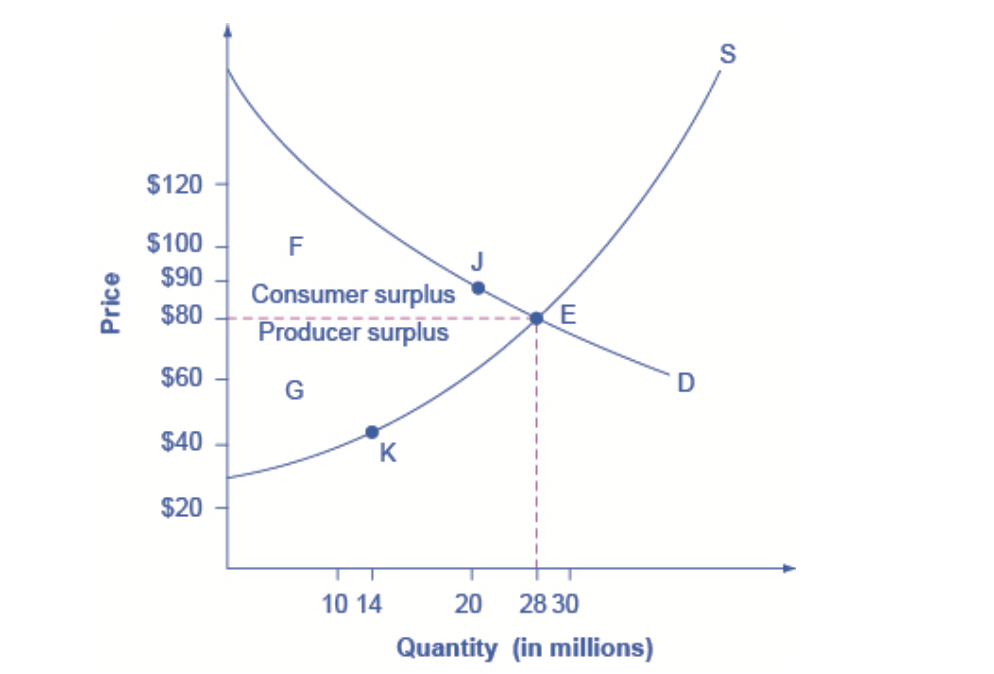

consumer surplus, producer surplus, social surplus

consumer surplus: amt individuals willing to pay - amt actually paid, area labeled F (area above market price, below demand curve)

producer surplus: amt seller paid for good - seller’s actual cost, area labeled G (area between market price & supply curve below equilibrium)

social surplus: sum of consumer surplus + producer surplus (economic surplus, total surplus), F+G

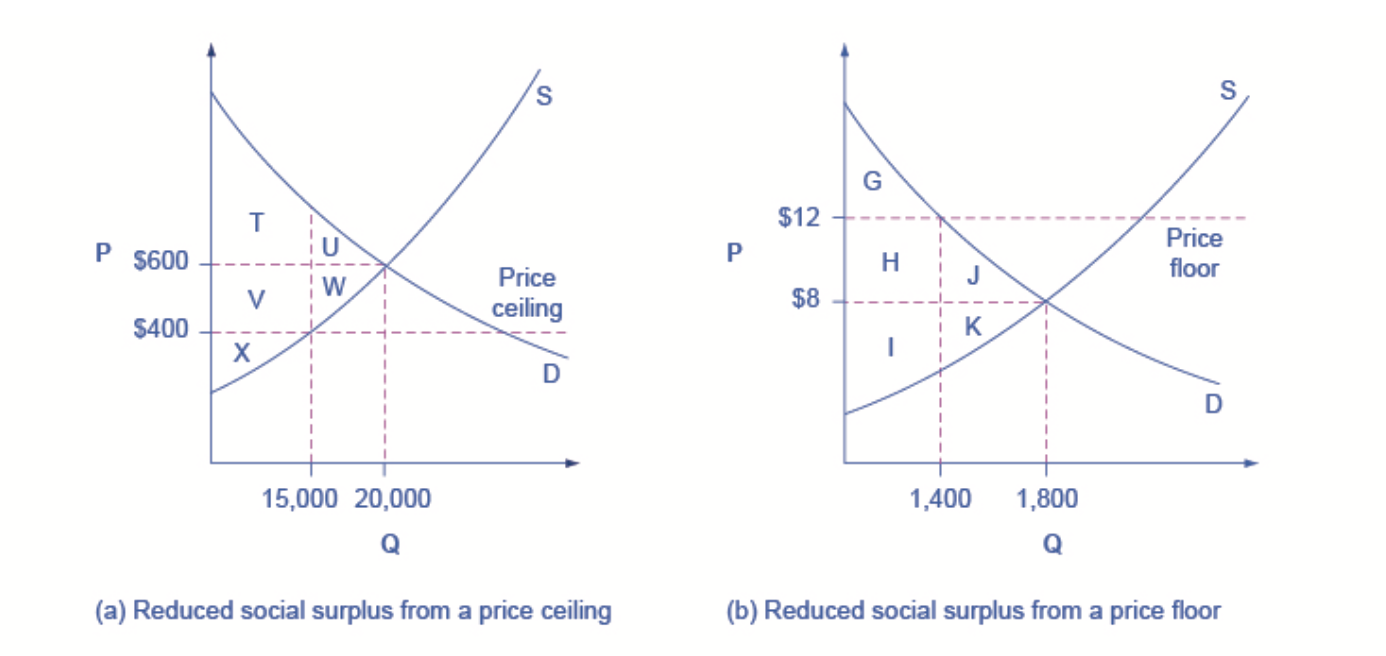

inefficiency of price floors and price ceilings

prevent market from adjusting to equilibrium price and quantity

inefficient outcome

transfer consumer surplus to producers or vice versa

deadweight loss: loss in social surplus that occurs when economy produces at an inefficient quantity, U+W

demand and supply as a social adjustment mechanism

demand and supply model emphasizes prices not set only by demand or only by supply, but by interaction between the two

adjustments of equilibrium in market-oriented economy without government direction or oversight

chapter 3 review

3.1 demand, supply, and equilibrium in markets for goods and services

demand schedule: table shows quantity demanded at diff prices in market

demand curve: relatoinship bw quantity demanded and price in given market on graph

law of demand: higher price = lower quantity demanded

supply schedule: quantity supplied at diff prices

supply curve: quantity supplied & price on graph

law of supply: higher price = higher quantity supplied

equilibrium price & quantitiy: where s&d curves intersect

if price below equilibrium, quantity demanded > supplied, shortage

3.2 shifts in demand and supply for goods and services

ceteris paribus: other things being equal

factors that shift demand curve cause diff quantity demanded

changes in tastes, population, income, prices of substitute/complement goods, expectations abt future conditions and prices

factors that shift supply curve cause diff quantity to be supplied

input prices, natural conditions, tech, gov taxes, regs, subsidies

3.3 changes in equilibrium price and quantity: four-step

sketch s&d diagram to see what market looks like before event

decide whether event affects supply or demand

decide whether effect on supply or demand is pos/neg

compare new equilibrium price and quantity to original

3.4 price ceilings and price floors

price ceilings prevent price from rising above certain level

price ceiling below equilibrium price → shortage

price floors prevent price falling below certain level

price floor above equilibrium price → surplus

3.5 demand, supply, efficiency

consumer surplus: gap between price consumers willing to pay (preferences) and market equilibrium price

producer suplus: gap between price producers willing to sell (costs) and market equilibrium price

social surplus: sum of consumer + producer surplus

total surplus: larger at equilibrium quantity and price than at any other quantity and price

deadweight loss: loss in total surplus when economy produces at inefficient quantity