Asset Valuation with Interest Rates

Asset Valuation with Interest Rates Study Notes

Introduction

Instructor: Dr. Lu Yang, Assistant Lecturer at FSU College of Business

Focus Topic: Impact of interest rates on asset prices and valuations.

Interest Rates Overview

Interest rates significantly influence prices of various securities.

HIGH rates: borrowing is expensive, saving is more attractive

LOW rates: make borrowing more appealing and stimulates economic growth

The meaning of interest rates can vary based on:

Time Frame:

Short-term vs. Long-term

Type of Security:

Equity, bonds, etc.

Various Interest Rate Measures

Coupon Rate:

Definition: The interest rate on a bond used to calculate the annual cash flow the bond issuer promises to pay the bondholder.

Fixed % of bond’s Face Value that the issuer will pay the bondholder annually. $1000 bond, 5% coupon rate = $50 annual payments

Required Rate of Return (r):

Definition: The interest rate an investor should receive on a security given its risk. Used to calculate the fair present value of a security.

What an investor SHOULD receive on a security given it’s minimum risk. This rate calculates Fair Present Value, this is a forward-looking calculation.

FPV>=market price, this is a good deal, undervalued, or fair

FPV<=market price, overvalued, not a good deal

Expected Rate of Return (E(r)):

Definition: The interest rate an investor expects to receive on a security assuming they buy at the current market price, receive all expected payments, and sell at the end of their investment horizon.

What the market IMPLIES you will earn if you buy the security at the current market price, given all of the discounts it will pay.

ER>R, market is offering a return that JUSTIFIES the risk

ER<R, the market is not offering anything good, the risk is not justified

Realized Rate of Return (r̅):

Definition: The actual interest rate earned on an investment in a financial security. This is a historical (ex-post) measure of the interest rate.

What you ACTUALLY earned after your investment sold or matured

What you paid - PV of cash flows you received - sell price

How to measure the success or failure of an investment

(r̅)>R, this is a success

(r̅)<R, this is a failure, underperformance

Backward-looking

Required Rate of Return (r)

Definition & Purpose:

It reflects the interest rate that an investor should earn considering certain risks (e.g., default, liquidity).

It is an ex-ante measure, which is fundamental for determining the fair present value of a security.

Interpretation of Required Rate of Return

If : Security is undervalued, hence consider buying (investing in) this security.

If P̂ > P: Security is overvalued, hence consider selling (divesting from) this security.

If : Security is fairly priced given its perceived risk levels.

Where = current market price of the security.

Example Calculation of Required Rate of Return (r)

Consider a Walmart bond purchased for $890 now selling for $925, with additional projected details:

Coupon Interest: $100 per year, last payment is today.

Future Sale Price after 4 years: $960.

Required rate of return: 11.25%.

Objective: Calculate the bond’s fair present value.

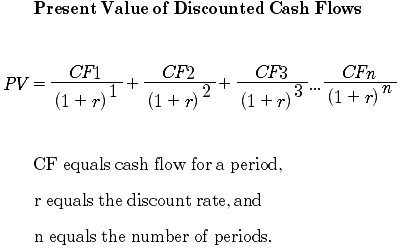

Steps for Fair Present Value Calculation

Start with the formula for present value of cash flows.

Collect necessary information regarding the bond purchase and projections.

Plug values into the required equations to derive present value.

Determine if the bond is overvalued, undervalued, or fairly priced to make investment decisions.

Expected Rate of Return (E(r))

Definition:

E(r) represents the expected interest rate on an investment based on the security’s current market price. Also considers cash flows expected to be received.

The present value of projected cash flows equals its current market price .

Interpretation of Expected Rate of Return

If : The expected cash flows justify the risk - consider buying this security.

If E(r) < r: The expected cash flows do not justify the risk - consider selling this security.

Example Calculation of Expected Rate of Return (E(r))

Similar scenario as with Required Rate of Return, calculate E(r) based on bond information, expected payments, and prospective future selling price.

Review: Key Differences Between Rates

Required and expected rates of return serve different assessment purposes:

Required Rate of Return (r): A benchmark for fair present value calculations.

Expected Rate of Return (E(r)): A reflective measure based on market pricing and potential cash flows.

In an efficient market, the current market price aligns with the fair present value.

External events affecting securities lead to changes in demand and pricing.

Realized Rate of Return (r̅)

Definition:

Represents the actual rate earned on an investment after holding it. It is an ex-post measure.

Calculation involves setting the price actually paid to equal the present value of realized cash flows.

Interpretation of Realized Rate of Return

If r̅ > r: The investor has earned more than necessary to cover the risk.

If r̅ < r: The investor has earned less than needed, indicating the investment did not meet benchmark expectations.

Bond Valuation Principles

Bond valuation utilizes time value of money principles:

Fair value of a bond equals the present value of all expected cash flows, including coupon payments and the par value at maturity, discounted at the required rate of return.

Sources of Bond Cash Flows:

Periodic coupon payments and face (par) value upon maturity.

Large lump sums at maturity

Note: If there are no coupon payments, the bond is termed a zero-coupon bond.

Bond Valuation Calculation Formula

Present value of a bond can be calculated using the formula:

Where:

= Present value of the bond

= Par or face value of the bond

= Annual interest (or coupon payment)

= Number of years until maturity

= Annual discount rate applied to cash flows.

Example Calculations of Market Value Based on Required Rate of Return

If the required rate of return is 8%:

Input values: N = 12 years, I = 4%, PMT = 50, FV = 1000 ⇒ CPT PV = -$1,152.47.

Maximum investment = $1,152.47 for the bond.

If the required rate of return is 10%:

The market value of the bond is at par = $1,000, given this rate.

If the required rate of return is 12%:

The market value computes to $874.50 for valuation.

Types of Bonds Based on Market Conditions

Premium Bond: When coupon rates exceed required rate, bond’s fair value is higher than face value.

Discount Bond: When coupon rates are below required rate, fair value is less than face value.

Par Bond: When rates are equal, fair value matches the face value.

Summary & Conclusion

Understanding the distinctions between required, expected, and realized rates of return is crucial for effective asset valuation.

Bond valuation employs present value calculations that are sensitive to changes in interest rates and market perceptions.

Questions?

Open the floor for any additional inquiries or clarifications regarding asset valuation and interest rates.