independent notes

modigliani and miller

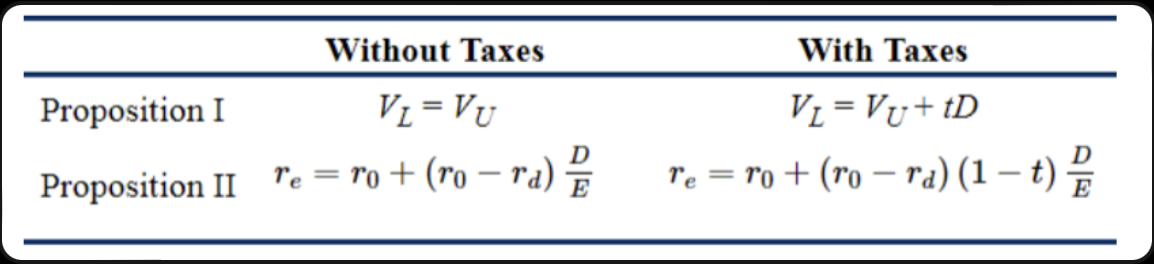

proposition 1 - irrelevance of capital structure

in a perfect world [no, taxes, no bankruptcy costs etc.], the value of a company is not affected by how it is financed, whether it uses only debt, equity, or a mix of both.

i.e. imagine a company as a pie. M&M p.1 says it doesn’t matter how you slice that pie, [debt vs. equity]; the size of the pie remains the same

why? - because investors can always “adjust” their won risk by buying or selling debt and equity themselves. so, how the company chooses to finance itself shouldn’t change its overall value

implication - in an ideal world, companies shouldn’t worry too much about whether they’re financed more by debt or equity, because it won’t affect the company’s overall value. the market would see them as equally valuable no matter how they split their financing.

proposition 2 - cost of equity and debt

in a perfect world, as a company takes on more debt, its cost of equity [the return shareholders demand] increases. this is because equity holders take on more risk when the company has more debt [since debt holders are paid first if things go wrong]

i.e. if a company borrows more [takes on more debt], its shareholders demand a higher return because the company becomes riskier to them

why? - more debt means higher interest payments, and in case of trouble, the company has to repay debt holders first. so, shareholders want compensation for the extra risk

implication - even though a company may increase its debt to finance its operations [which is often cheaper than equity], the overall cost of financing remains the same because the equity holders will demand a higher return for the increased risk. essentially, the ‘cheaper‘ debt doesn’t actually save money in the end

in the real world [with taxes]

when you add taxes into the mix, things change a bit because debt has a tax benefit [interest on debt is tax deductible, while dividends paid to shareholders are not]. this means that taking on debt can actually increase a company’s value, which is one reason why many companies use a mix of debt and equity.

with taxes - p.1 gets modified. the more debt a company has, the more it benefits from tax savings, and thus more debt can increase the company’s value

with taxes - p.2 also still applies, but the cost of capital [overall] may decrease slightly due to those tax advantages on debt .

trade off theory, pecking order theory, and market timing theory

these are 3 different theories that build on or offer alternatives to M&M propositions. they explain how real-world companies make capital structure decisions [how much debt vs. equity they should use].

trade off theory

this argues that companies balance the benefits and costs of debt when deciding how much debt to use. it recognises that debt offers tax benefits [since interest is tax deductible], but also increases the risk of financial distress or bankruptcy

how it works - companies aim to find the optimal amount of debt that maximises their value. they trade off:

the tax shield of debt [a benefit]

the costs of financial distress [a downside] like bankruptcy risk or agency costs [conflicts between shareholders and debt holders]

relation to M&M - in p.1, debt didn’t affect the value of a company. but the trade off theory relaxes this unrealistic assumption and acknowledges that in the real world, there are both benefits and costs to debt. this is why companies don’t just pile on debt even if it reduces taxes - they also weigh the risk of going bankrupt.

pecking order theory

this says that companies prefer to finance themselves in a specific order based on the cost of financing and information asymmetry [when management knows more about the firm than outside investors]. the hierarchy is:

internal financing [retained earnings] - companies prefer to use their won profits first, as this doesn’t involve taking on new debt or issuing new shares

debt financing - if external financing is needed, companies prefer debt because it’s less risky than equity from an info standpoint [it doesn’t signal bad news to investors]

equity financing [issuing new shares] - issuing new equity is the last resort because it often sends a negative signal to the market [investors might think the company is overvalued or struggling if it issues new shares]

how it works - companies don’t have a debt to equity ratio like in the trade off theory. instead, they follow a hierarchy of funding, based on what’s easiest and least likely to scare investors

relation to M&M - this theory contrasts with M&M, which assumes perfect information [everyone knows the same things], and says capital structure doesn’t matter. the pecking order theory acknowledges information asymmetry and suggests that the choice between debt and equity financing depends on how the investors perceive the company’s actions

market timing theory

this says that companies try to time the market when deciding whether to issue debt or equity when deciding whether to issue debt or equity. in other words, companies choose the type of financing that’s more favourable depending on market conditions:

if stock prices are high [and the companies equity is overvalued], the company will issue equity

if interest rates are low, [and borrowing is cheap], the company will issue debt

how it works - managers look at market conditions and time their financing choices based on when it’s cheapest to raise capital. they’ll issue equity when they think their stock is overvalued and debt when interest rates are favourable

relation to M&M - MTT is very different from M&M’s world of perfect markets, where timing wouldn’t matter because prices would always reflect true value. in the real world, however, market conditions are not always perfect, and companies try to take advantages of market inefficiencies

how these theories relate to M&M’s ideas

M&M’s propositions suggest that, in a perfect world [no taxes, no bankruptcy, perfect information], it doesn’t matter how a company is financed. in the real world, these other theories build on that:

TOT adds taxes and bankruptcy costs, suggesting firms balance the tax benefits of debt with the risks of financial distress

POT focuses on information asymmetry and says companies have a natural order of preference for financing [internal funds — debt — equity]

MTT introduces the idea that firms time the market, issuing debt or equity based on current market conditions and opportunities

in practice, these theories help explain why companies don’t strictly follow M&M’s ideal world, and instead use different combinations of debt and equity financing depending on their situation, market conditions, and available information

wk 4 notes

capital structure; managerial incentives and information

miller [1997] suggest a general approach for choosing between debt and equity to finance a company. other theories explain how companies actually make these decisions;

theories on capital structure

trade off theory:

companies balance the tax benefits of debt [since interest on debt is tax deductible] with the risk of financial distress [like bankruptcy] when choosing how much debt to take on

example - M&M’s revised formula shows that the market value of a firm is affected by taxes and bankruptcy costs:

Vl = Vu + [tC x B] - Vfd where:

Vu = market value of firm without debt [unleveraged]

tC x B = tax shield from debt

Vfd = cost of financial distress

takeaway - companies should aim for the right amount of debt that balances benefits [tax savings] and costs [bankruptcy risk]

pecking order theory:

companies prefer to use internal funds [like retained earnings] first because it’s the cheapest, then debt, and finally equity because issuing new shares is the most expensive and risky option

example - Nesbat industries needs £25 mil. for a project

if they use retained earnings, the cost to shareholders is exactly £25 mil

if they issue debt at 15%, they’ll have to repay £28.75 mil. in 2 yrs [25 × 1.1.5]

if cost of capital is 6% , present value in 2 yrs will be equal to £25.58 mil [25/1.06²]

if they issue equity, and its underpriced by 5%, they’ll need to issue £26.32 mil in new shares

25/[1 - 5%] = 26.32

takeaway - retained earnings are the cheapest option, followed by debt, and equity is the most expensive

market timing theory:

companies issue debt or equity depending on market conditions. if stock prices are low [undervalued], they issue debt. if stock prices are high [overvalued], they issue equity

example - Cov ltd. has a project that will either make the company worth 100 mil. or 200 mil. in a yr. the CEO knows the project will succeed, but the investors aren’t sure. the CEO can issue:

10m debt - signals confidence and suggests the company is undervalued

110m debt - might be seen as risky

takeaway - CEO’s use private information to make financing decisions and signal their confidence to the market

determinants of capital structure

here’s how different firm characteristics relate to the use of debt [leverage]:

profitability:

firms with higher profits typically use less debt because they have enough internal funds to finance projects. highly profitable firms don’t need to borrow as much

growth:

firms with high growth potential tend to use less debt because growth projects are riskier, and too much debt can limit future investment opportunities

tangibility:

firms with more tangible assets [like real estate firms] can take on more debt because these assets can be used as collateral. in contrast, tech firms [with intangible assets like patents] may use less debt.

earnings volatility:

companies with unstable cash flows [like R&D firms] typically use less debt because they can’t predict their income as reliably. stable firms, like utility companies, can afford more debt

size:

larger firms usually take on more debt because they are seen as less risky by lenders. they have a more established track record.

bond ratings:

firms with higher bond ratings can issue more debt at a lower interest rate because lenders see them as safe. high rated firms often have better access to cheap financing

agency issues and capital structure

agency cost of debt:

over investment [asset substitution] - when a company is struggling, shareholders might push for risky projects that could harm the company but benefit them if things go well [at the expense of debt holders]

under investment [debt overhang] - a company is distress might avoid for good projects because most profits would go to paying off debt, not benefitting shareholders

example - a manager at XYZ ltd. might choose project A [with 40 mil. loss] because if it succeeds, shareholders gain big, but if it fails, the company can default, leaving debt holders with the loss. this is a case of over investment. project B is safer but doesn’t benefit shareholders as much

agency cost of equity:

managers may not always act in shareholder’s best interests. they might waste money on unprofitable projects, empire building, or managerial perks

solution - leverage [debt] can reduce these agency costs by forcing managers to focus on profitability [since they have to make regular interest payments]

financial distress

financial distress occurs when a company’s operating cash flows are insufficient to cover their current obligations, such as paying interest on debt, trade credits, or other financial commitments. this can occur due to several reasons:

excessive debt - the company may have taken on too much debt, leading to high interest payments that exceed its earnings

poor operational performance - declining sales, rising costs, or inefficient operation reduce cashflow

economic downturns - external factors like recessions, market crashes, or industry declines can reduce demand for a company’s products or services

mismanagement - poor decision making, over investment in unprofitable projects, or excessive spending can strain resources

unexpected events - crises like lawsuits, natural disasters, or pandemics can disrupt operations and create sudden financial strain

when these factors overwhelm a firms ability to generate enough cash, financial distress occurs.

direct costs of financial distress include legal and admin costs during bankruptcy

indirect costs include loss of sales, reputation, and key employees when a firm is struggling to pay its debts

possible strategies for a firm in distress:

expand operations - acquire new ventures or increase production to reduce risk

contract operations - shut down unprofitable divisions to focus on profitable ones

financial policies - cut dividends or restructure debt to improve cash flow

external control - let large investors take control of the company

management change - replace the CEO or top management to improve performance

bankruptcy - as a last resort, wind down the company

conclusion

in summary, companies must carefully balance the use of debt and equity based on their specific circumstances, taking into account factors like profitability, growth, and market conditions. different theories like TOT, POT, and MTT help explain how companies can make these decisions. finally, agency issues can arise, but leverage can help keep management focused on profitability.