Chapter 7

Service Line Costing

One of the key elements of healthcare reform is cost reduction:

To contain costs, we need to measure costs at the individual service level.

Three methods:

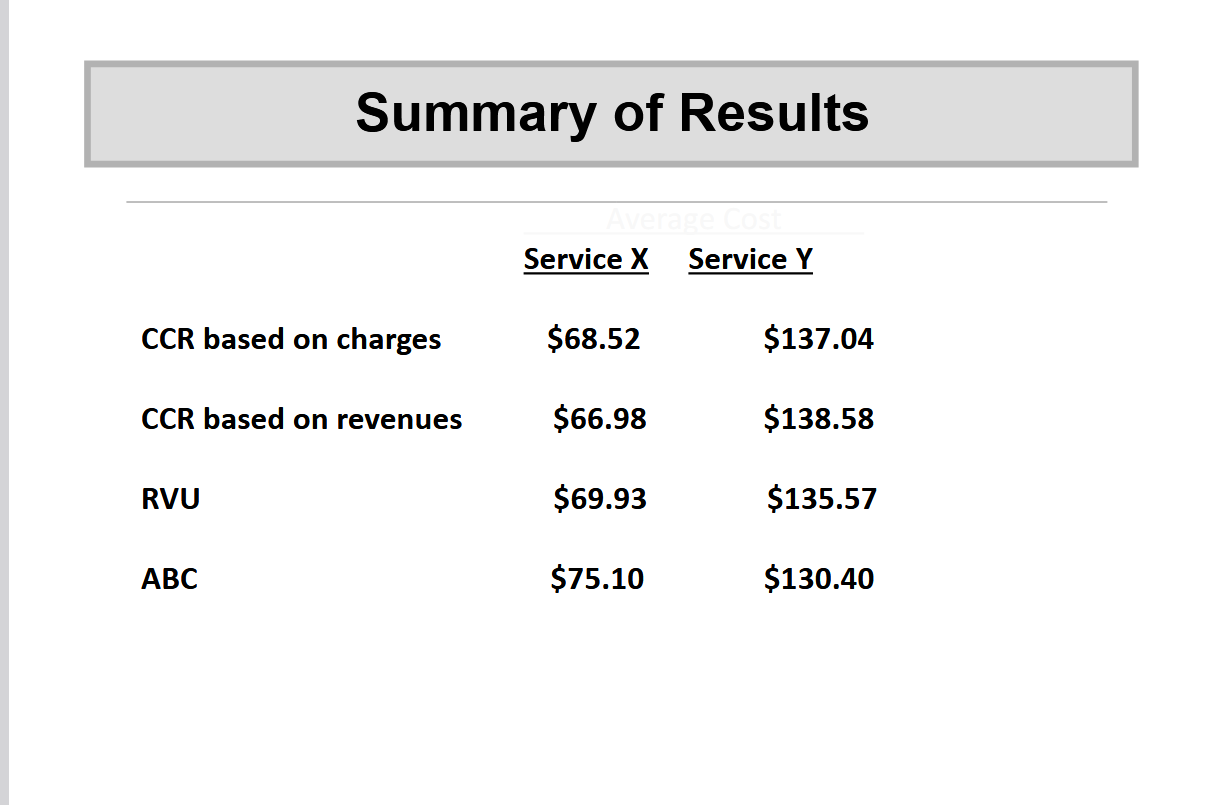

Cost-to-charge ratio (CCR)

Relative value unit (RVU)

Activity-based costing (ABC)

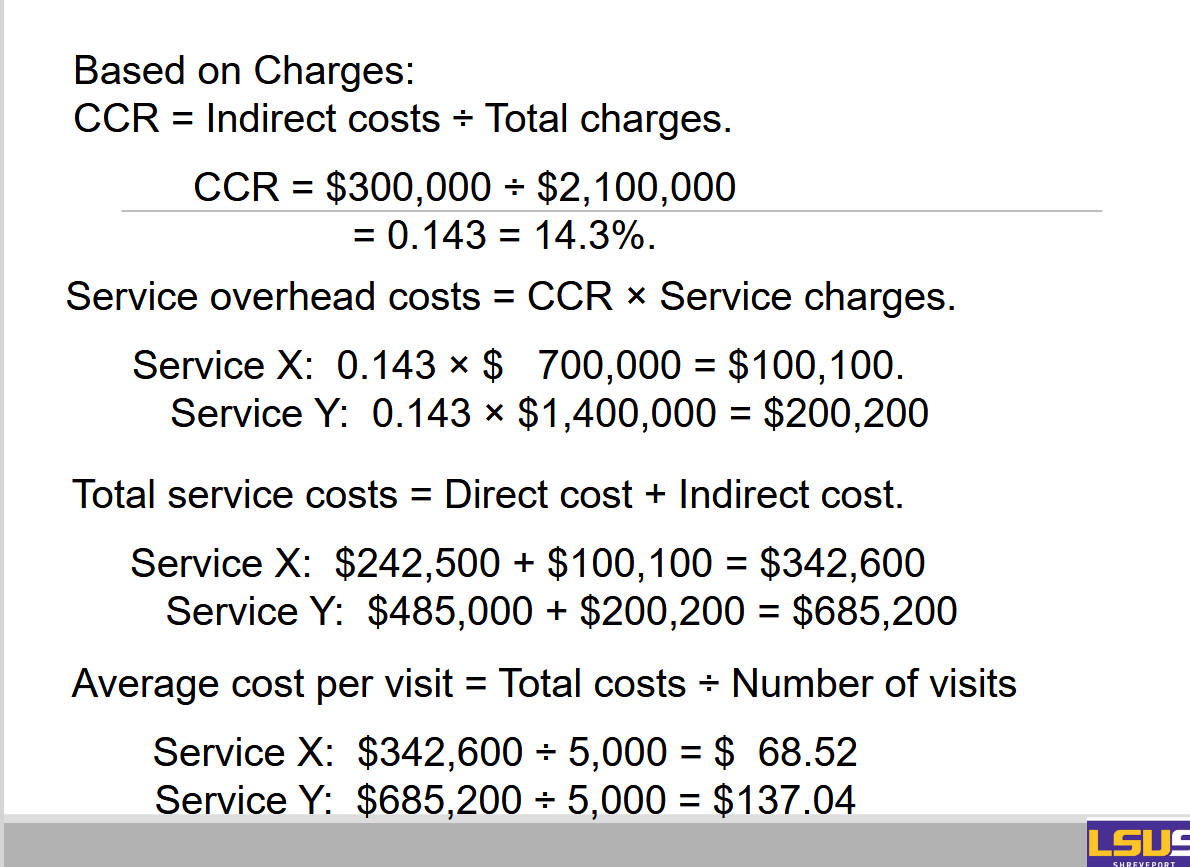

Cost-to-Charge Ratio (CCR) Method:

The CCR method is based on two assumptions:

The indirect costs allocated to individual services constitute a single cost that is proportional across all services provided.

Charges (or revenues) reflect the level of intensity of the service provided, and as a result the use of overhead services.

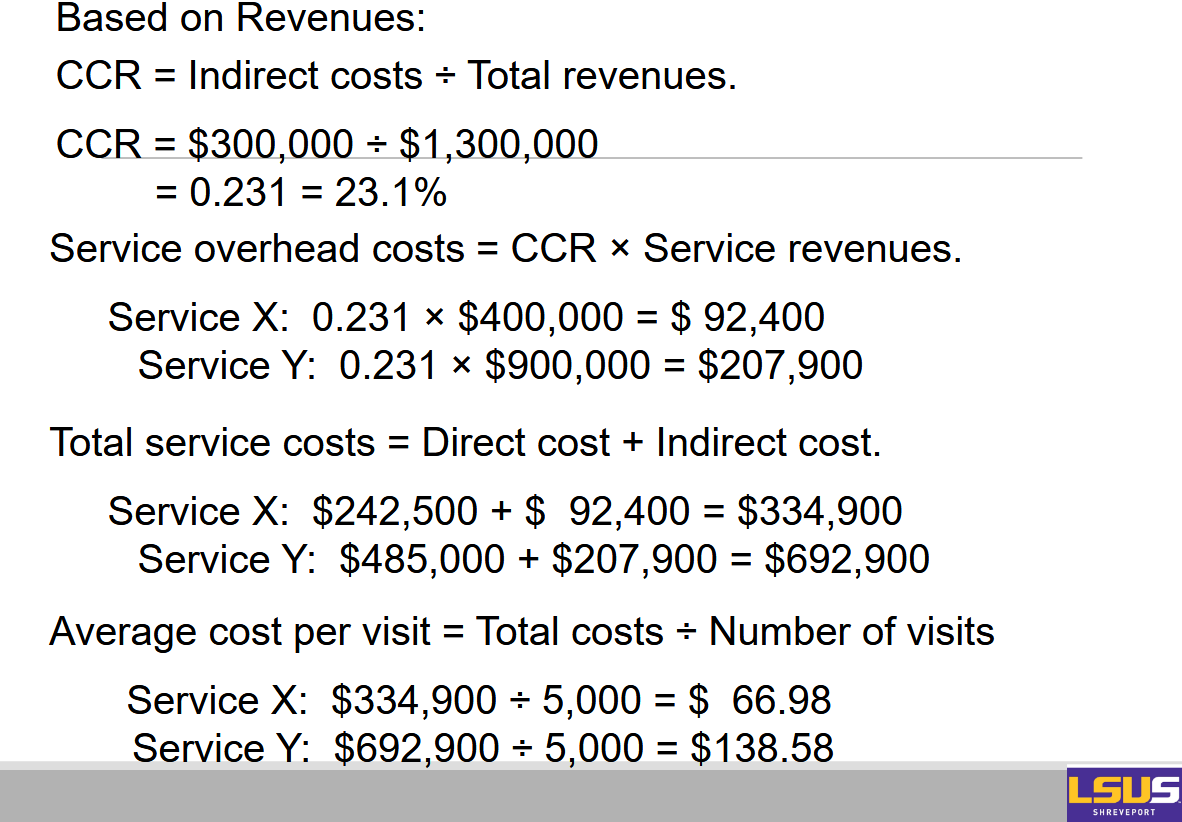

We will begin by using charges as the basis for the estimation. Then, we will repeat the calculation using revenues:

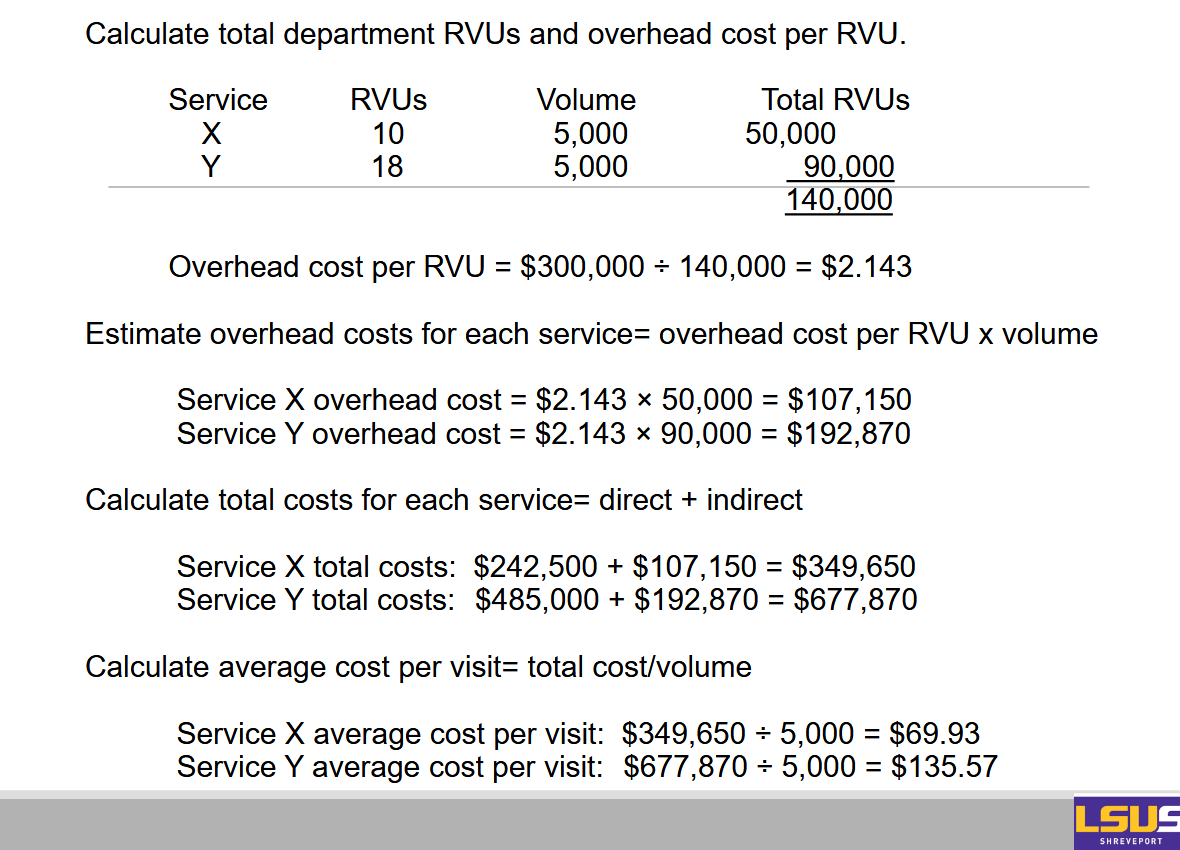

Relative Value Unit (RVU) Method

CCR vs RVU:

CCR method - Ties overhead resource consumption to charges (or revenues).

Relative value unit (RVU) method - Ties the use of overhead resources to the complexity and time required for each service as measured by relative value units (RVUs).

Activity-Based Costing (ABC)

Traditional cost allocation (such as CCR or RVU) is a top-down system.

Activity-based costing (ABC) begins with the individual activities that comprise the services provided.

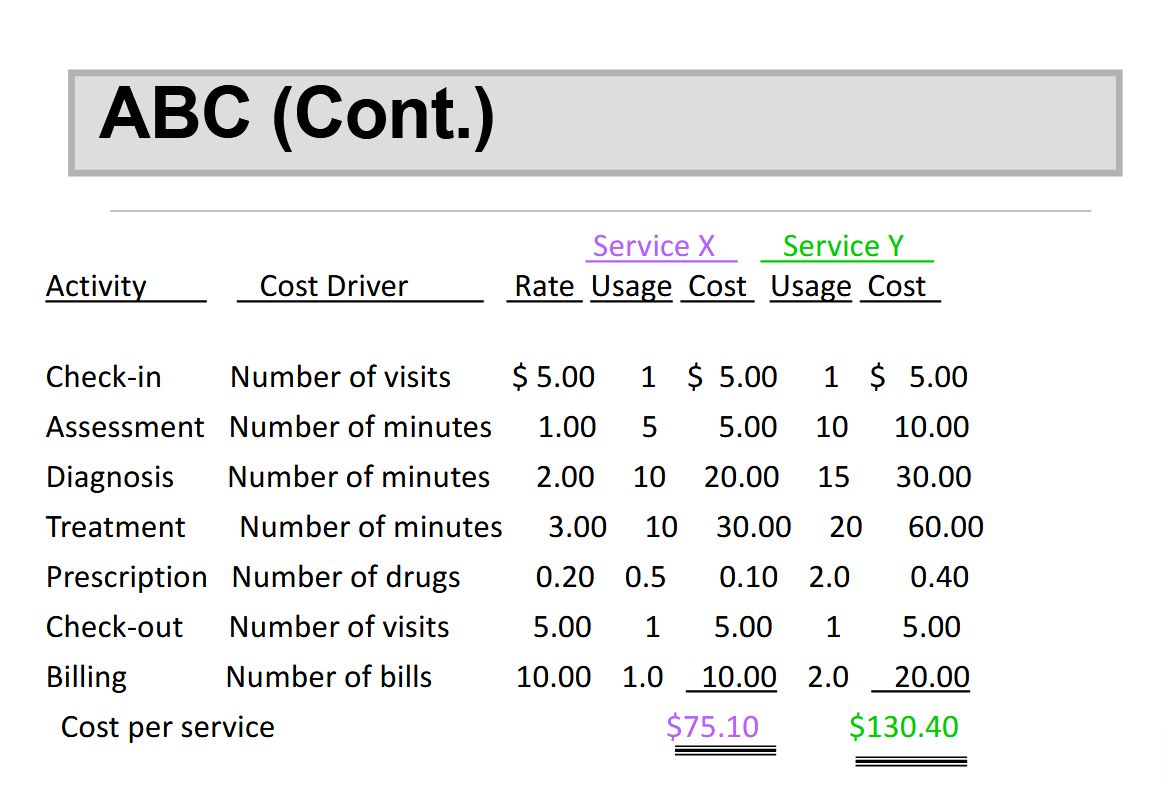

Cost allocation under ABC:

Identify the activities that are performed to provide a particular service.

Aggregate the costs of the activities.

Steps to implement ABC:

Identify the relevant activities.

Estimate the cost of each activity, including both direct and indirect.

Assign cost drivers for each activity.

Collect activity data for each service.

Calculate the total cost of the service by aggregating activity costs.

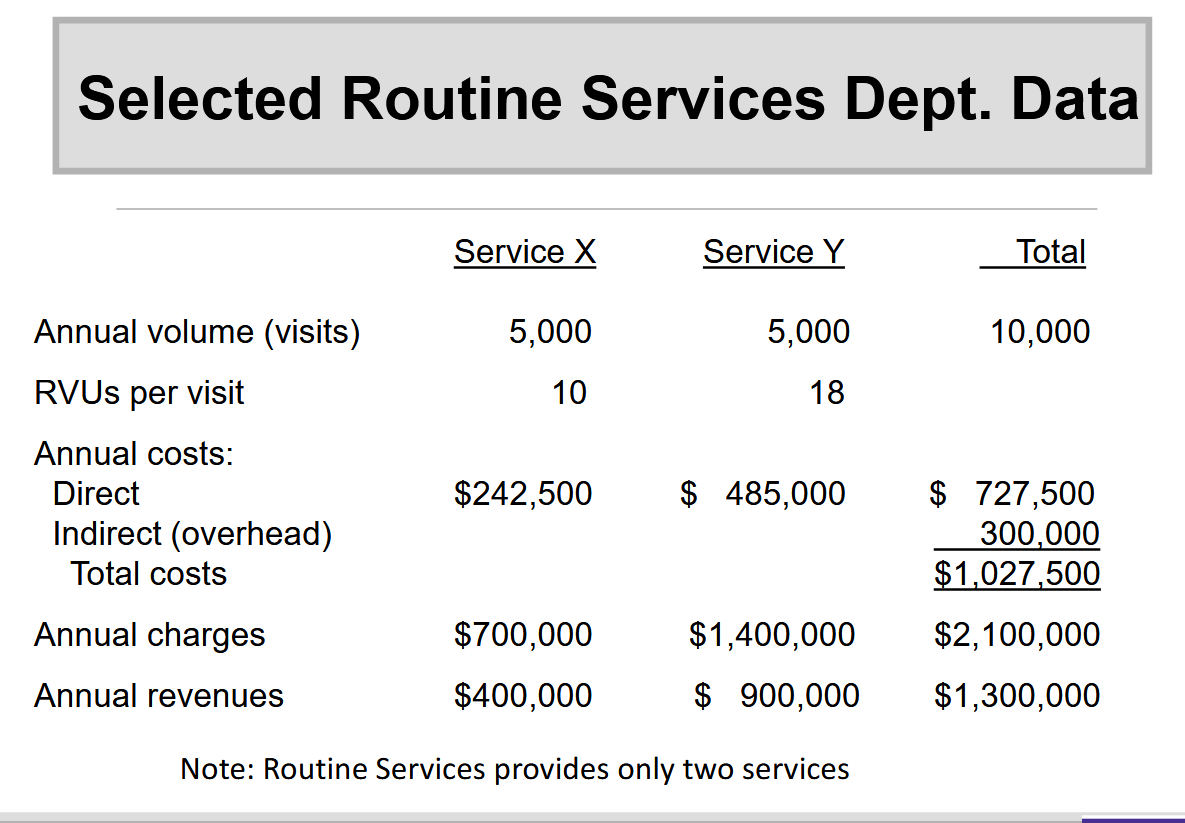

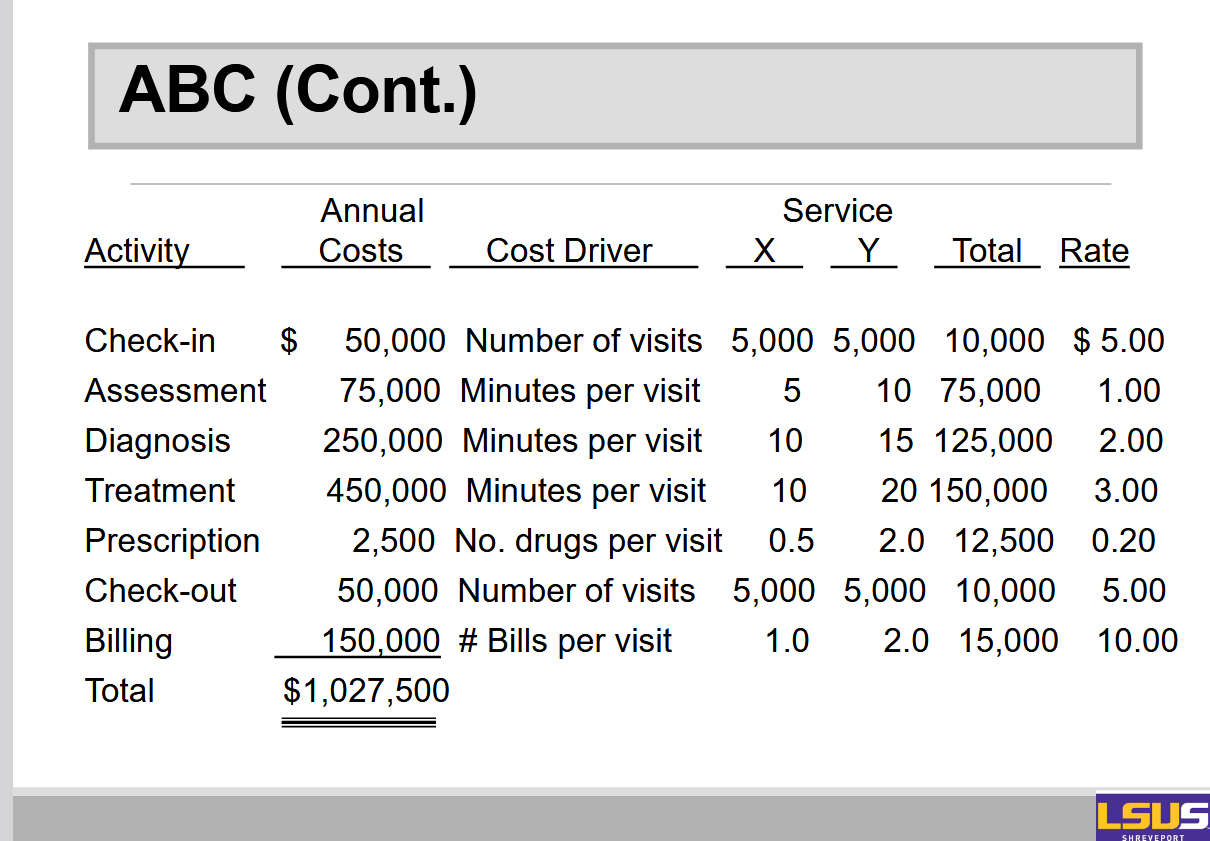

ABC Illustration

Suppose the Routine Services Department performs seven activities:

⚫ Patient check-in, including insurance verification.

⚫ Preliminary assessment.

⚫ Diagnosis.

⚫ Treatment.

⚫ Prescription writing.

⚫ Patient check-out.

⚫ Third-party-payer billing.

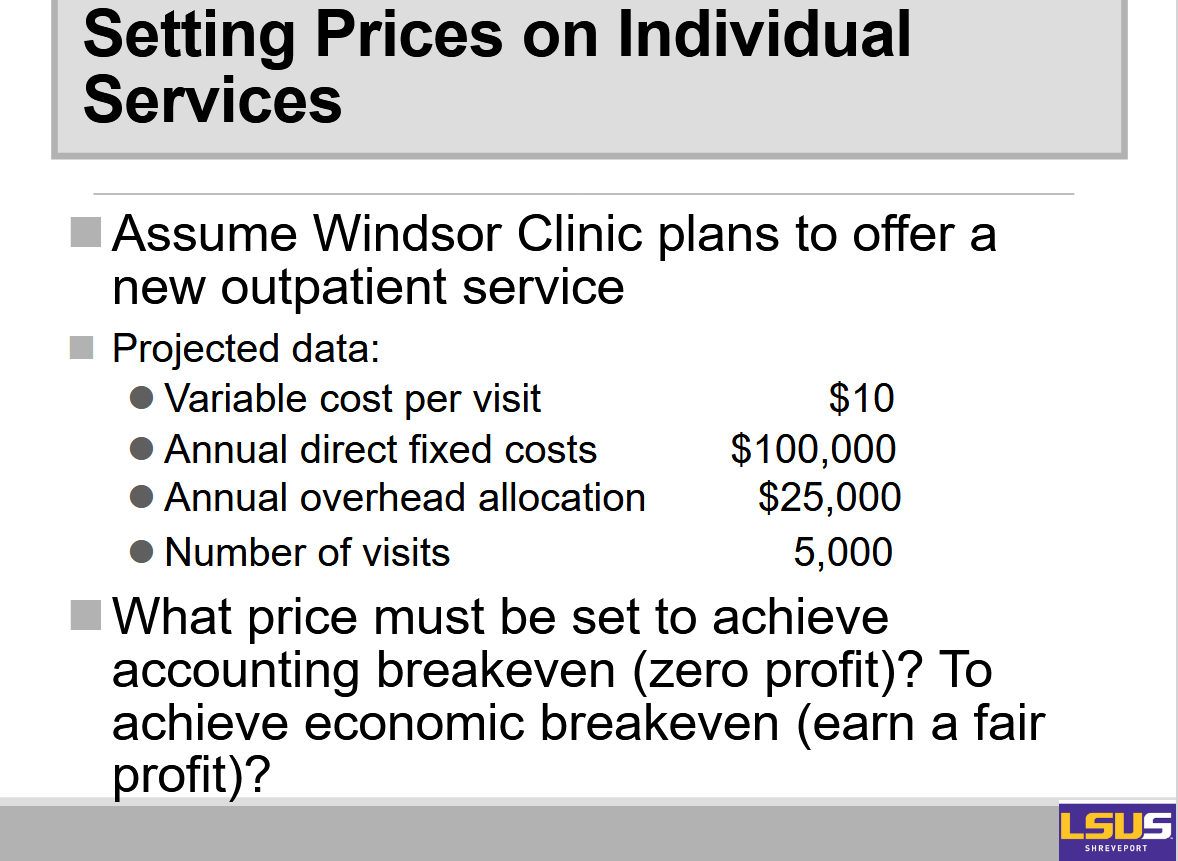

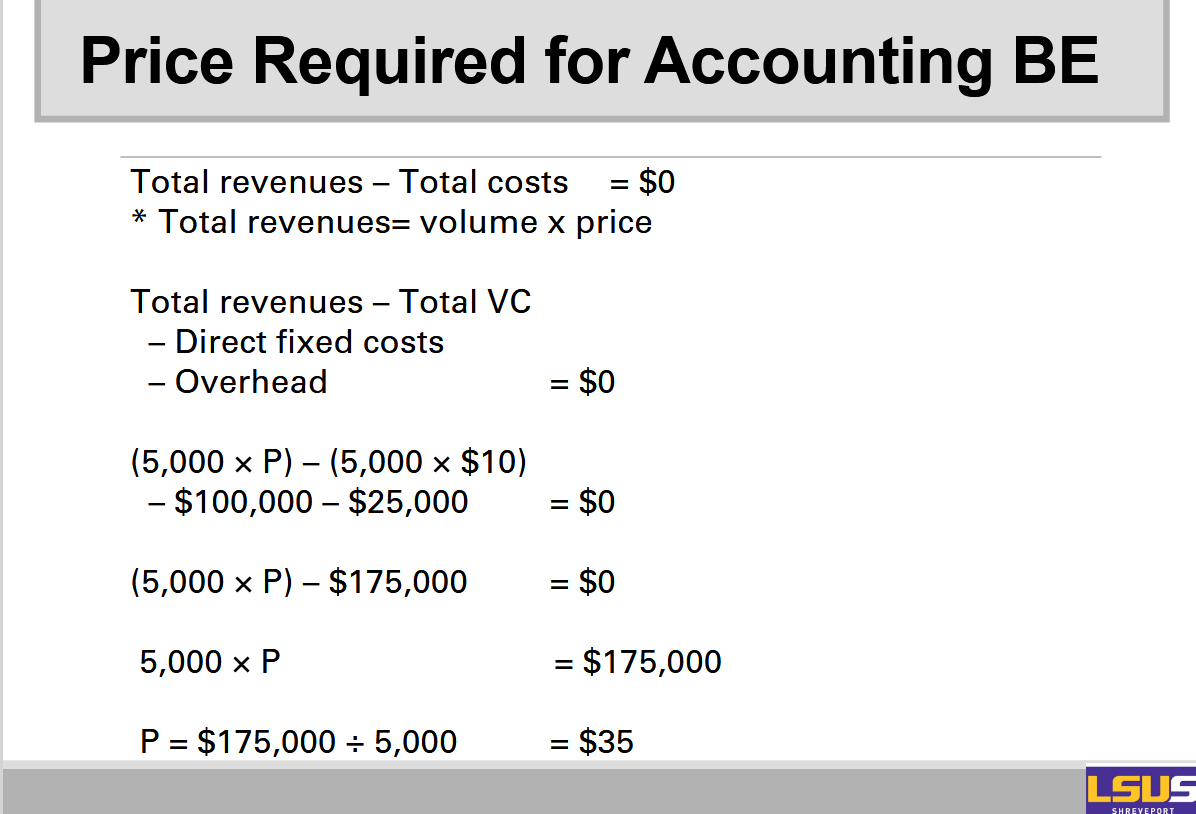

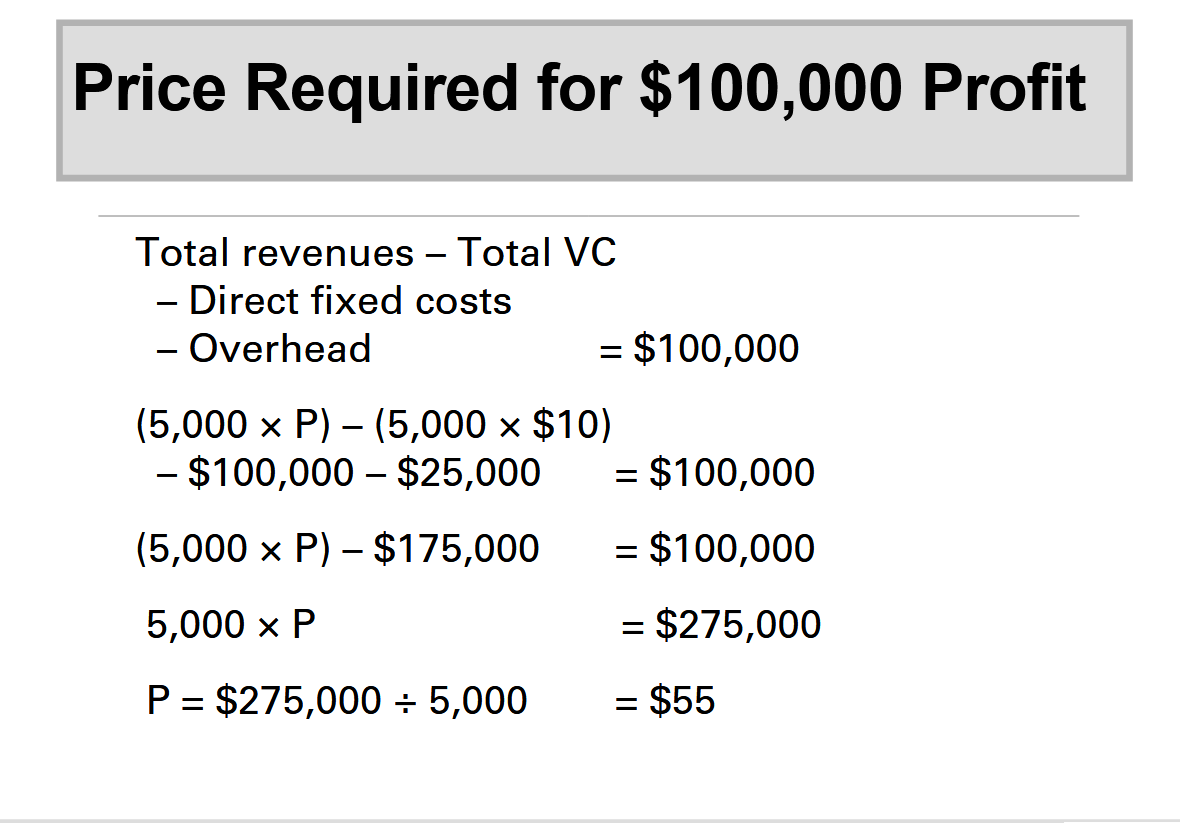

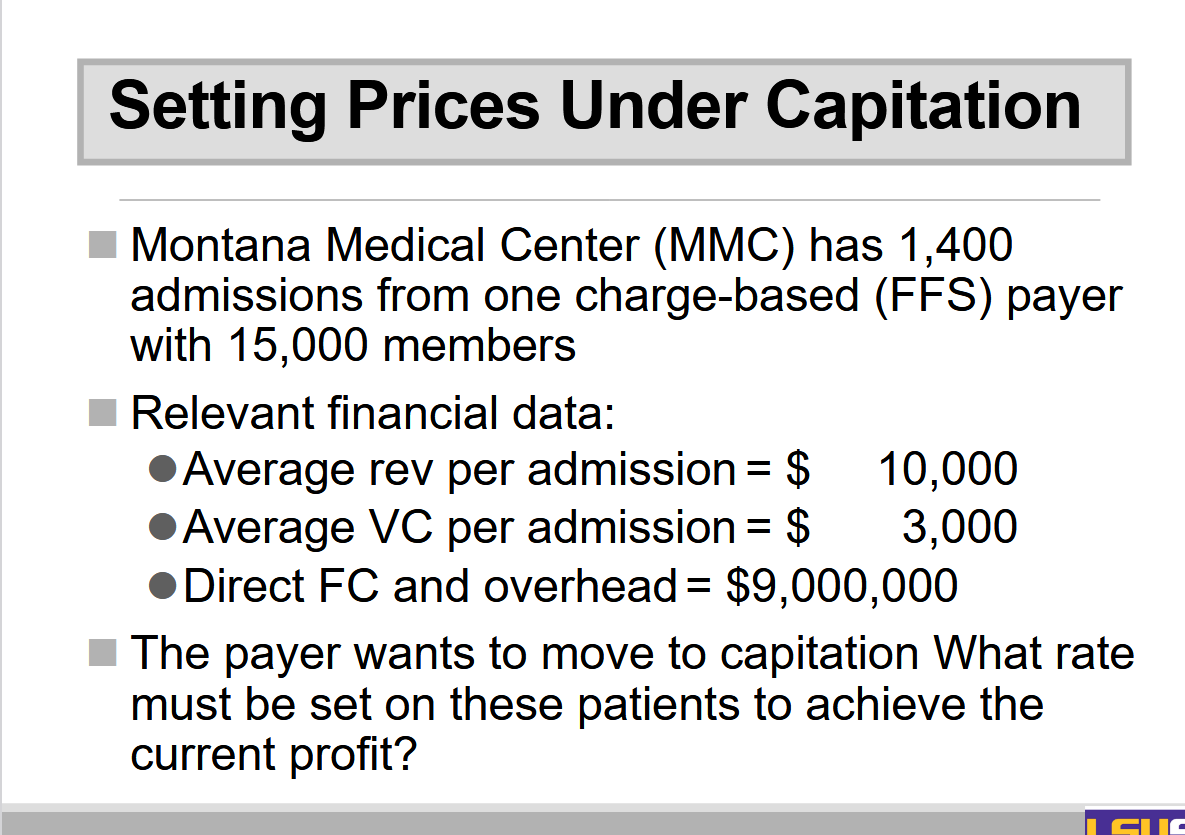

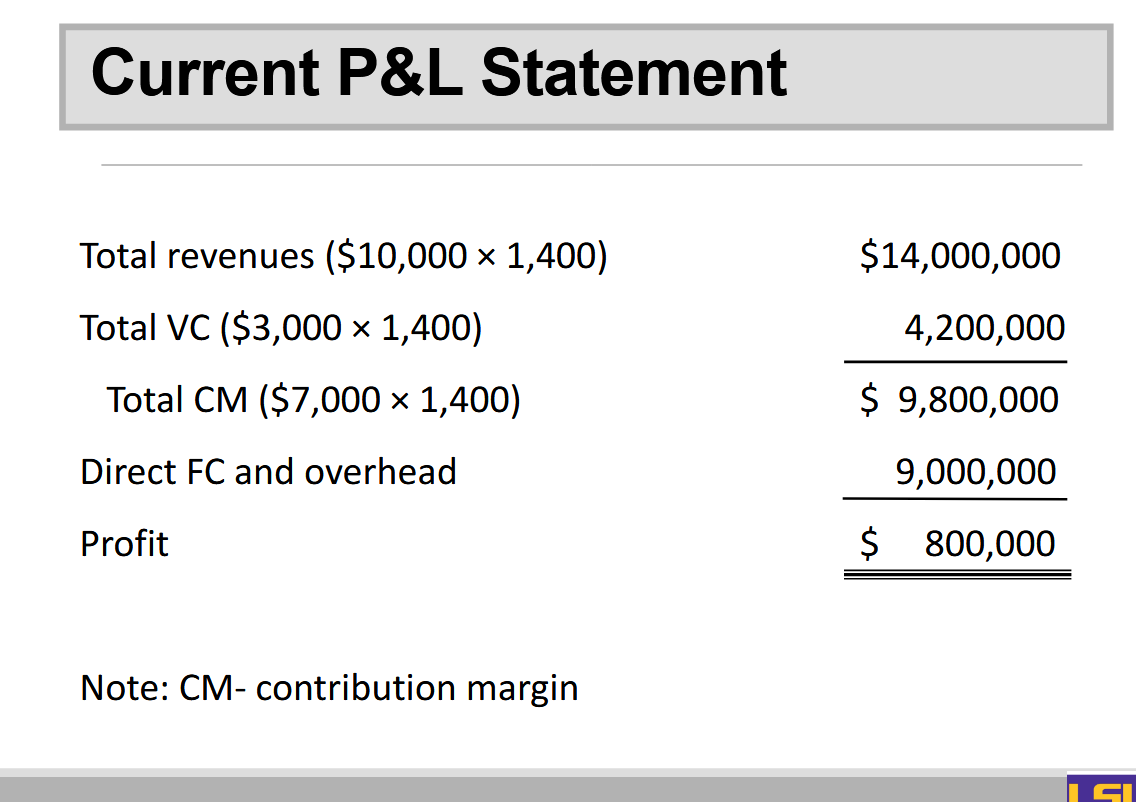

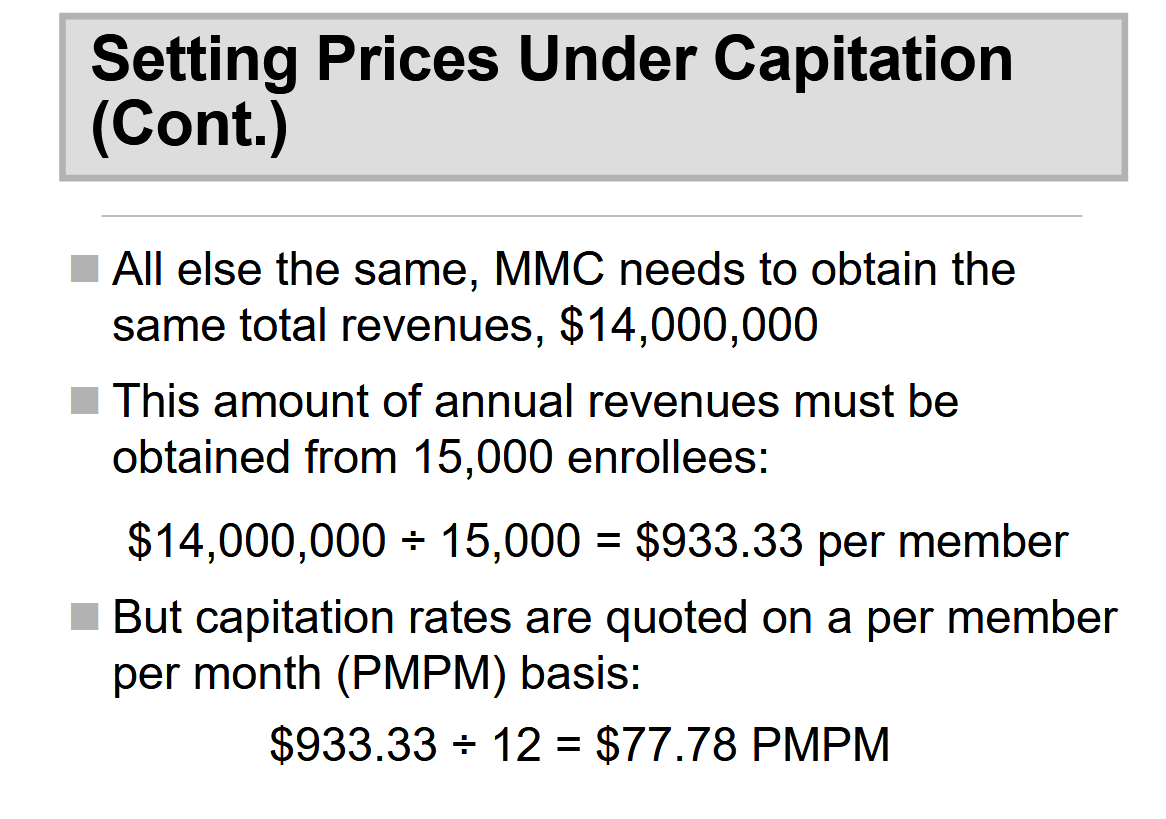

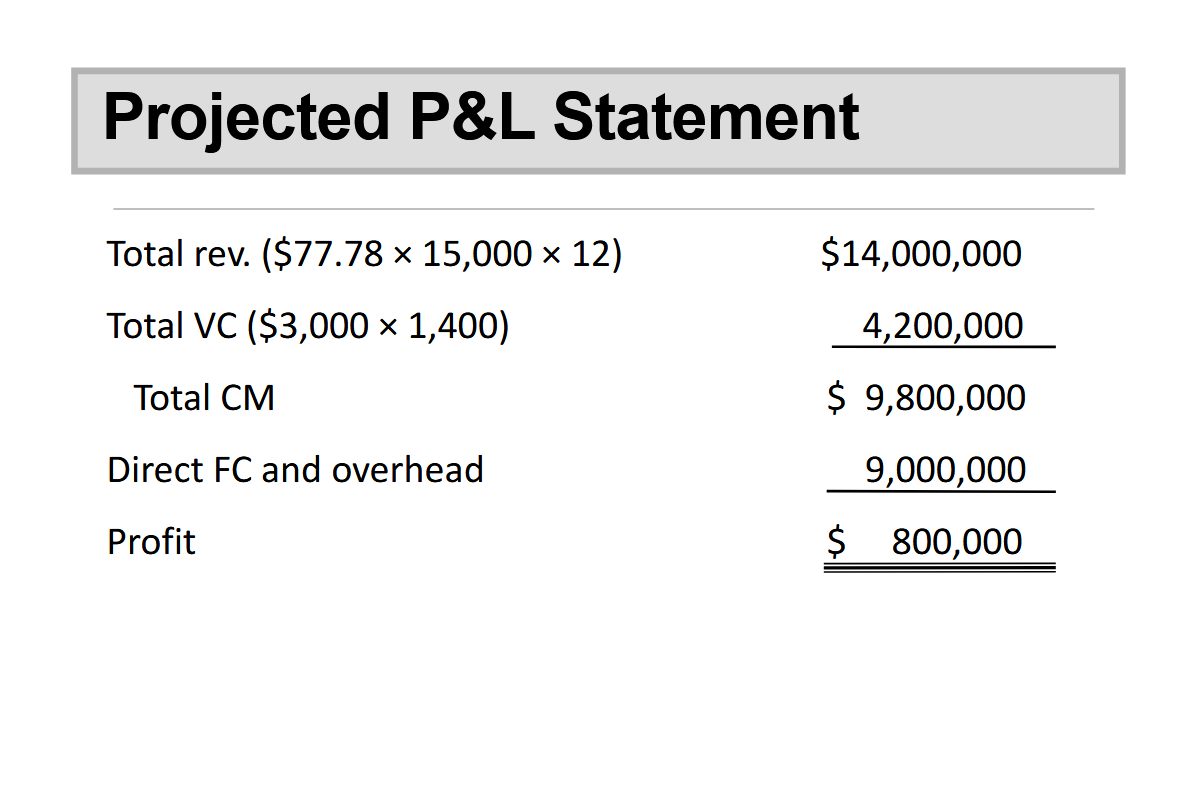

Pricing Decisions

One use of managerial accounting information within health services organizations is to:

⚫ Set the prices (and discounts) on services offered under charge-based reimbursement.

⚫ Determine the financial impact of services offered when prices are dictated

⚫ Identify the lowest feasible price when prices are negotiated.

Price Setters Versus Takers

Price setter:

⚫ A provider has market dominance, and can set its own prices (within reason).⚫ Government programs.

Price takers:

⚫ Perfectly competitive markets

⚫ Payer dominance

In many situations providers are neither pure price takers nor pure price setters and there is room for negotiation.

Pricing Strategies:

When a provider is a price setter (or when negotiation is possible), there are several theoretical bases upon which prices can be set.

The two most common are:

⚫Full cost pricing

⚫Marginal cost pricing

Full Cost Pricing:

Full cost pricing:

Prices for a service are set to cover all costs:

Direct costs:

Fixed.

Variable.

Indirect (overhead) costs

In addition, a profit component typically is added

Marginal Cost Pricing

Marginal cost pricing:

⚫ Prices for a service are set to cover incremental, or marginal, costs.

⚫ Generally, this means recovering only direct variable costs.

A cannot provider survive if all services are priced at marginal cost.

Cross-subsidization, or Price Shifting - When a payer (An insurance company) pays a higher reimbursement than another prayer.

Marginal cost pricing should not be used because an organization cannot survive financially if it only receives reimbursement for marginal costs.

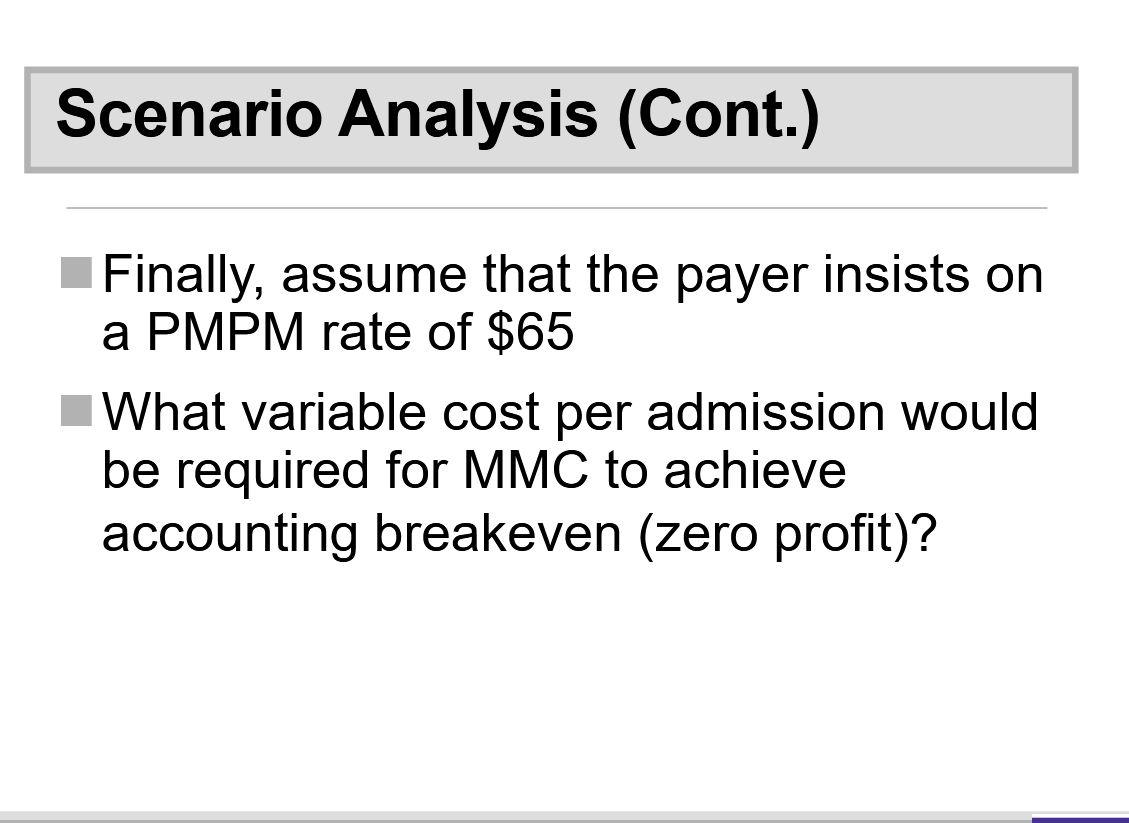

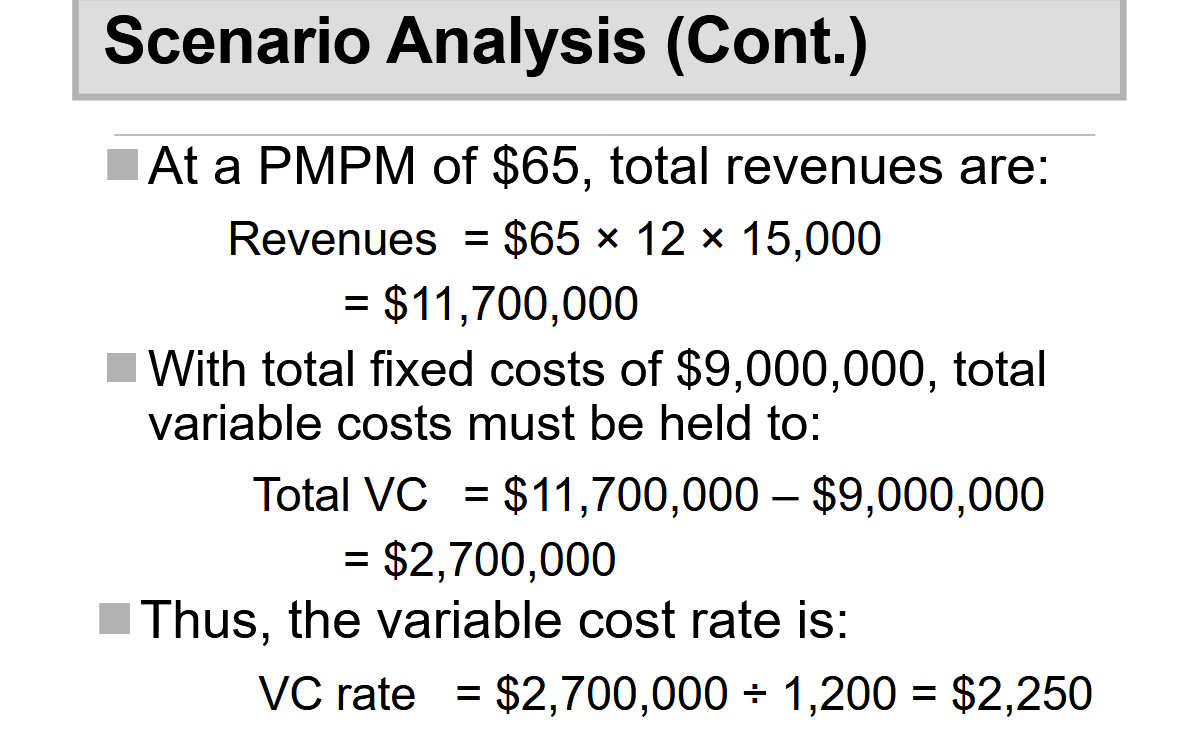

Target Costing

Target costing is a management strategy used by price takers.

Under target costing:

Revenues are projected assuming prices as given in the marketplace.

Required profits are subtracted from revenues.

The remainder is the target cost level.

The primary benefit of target costing is to remind managers that the market is dictating the price.

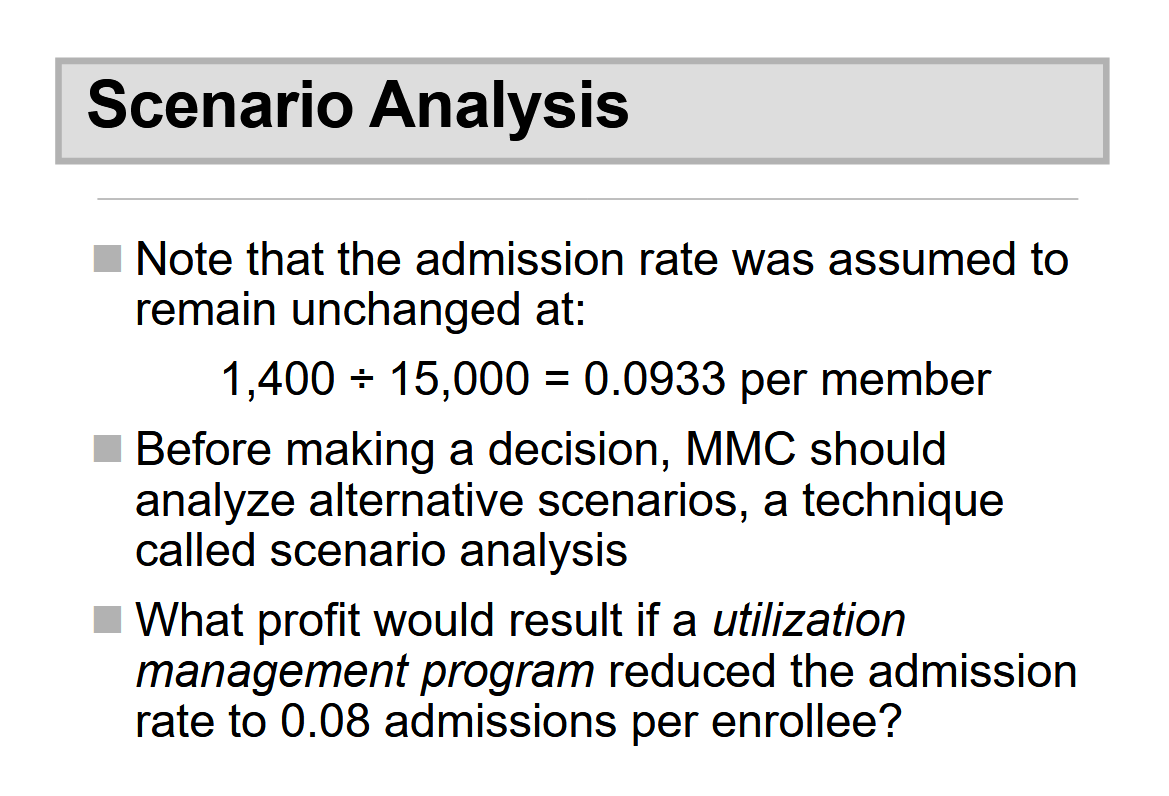

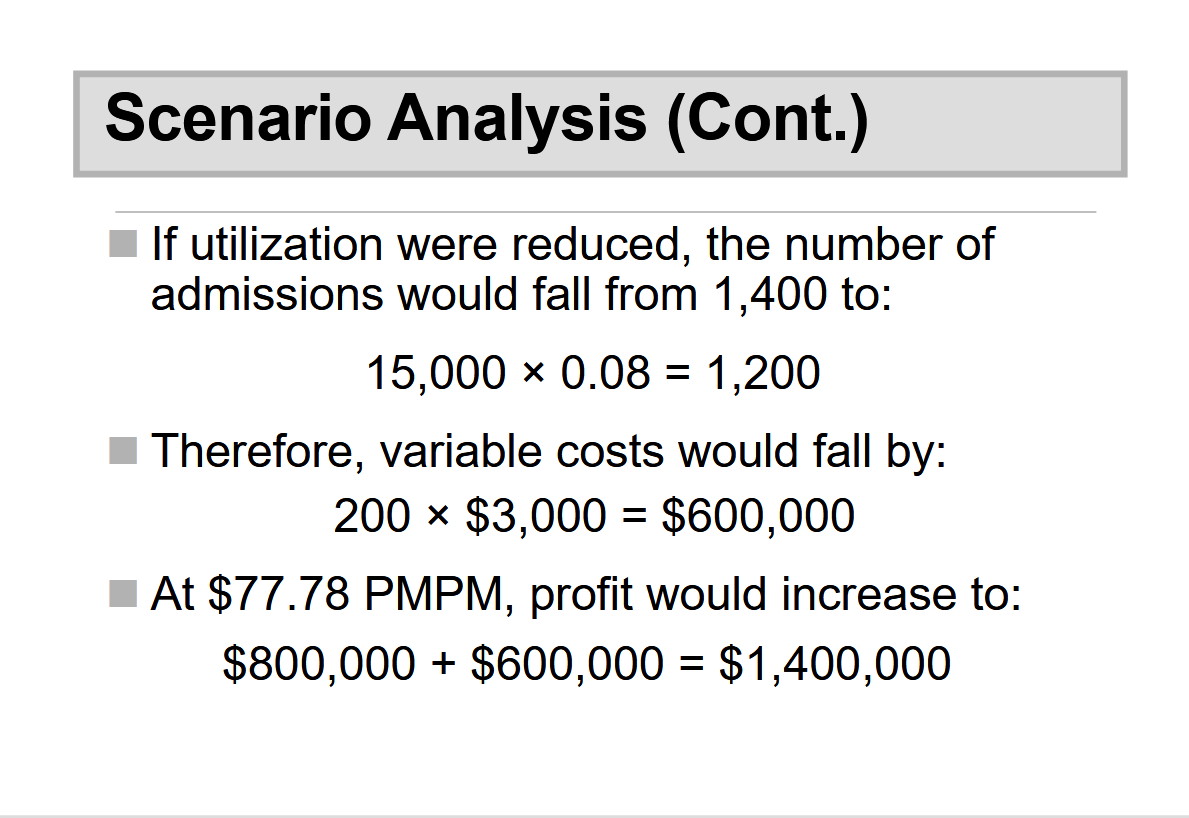

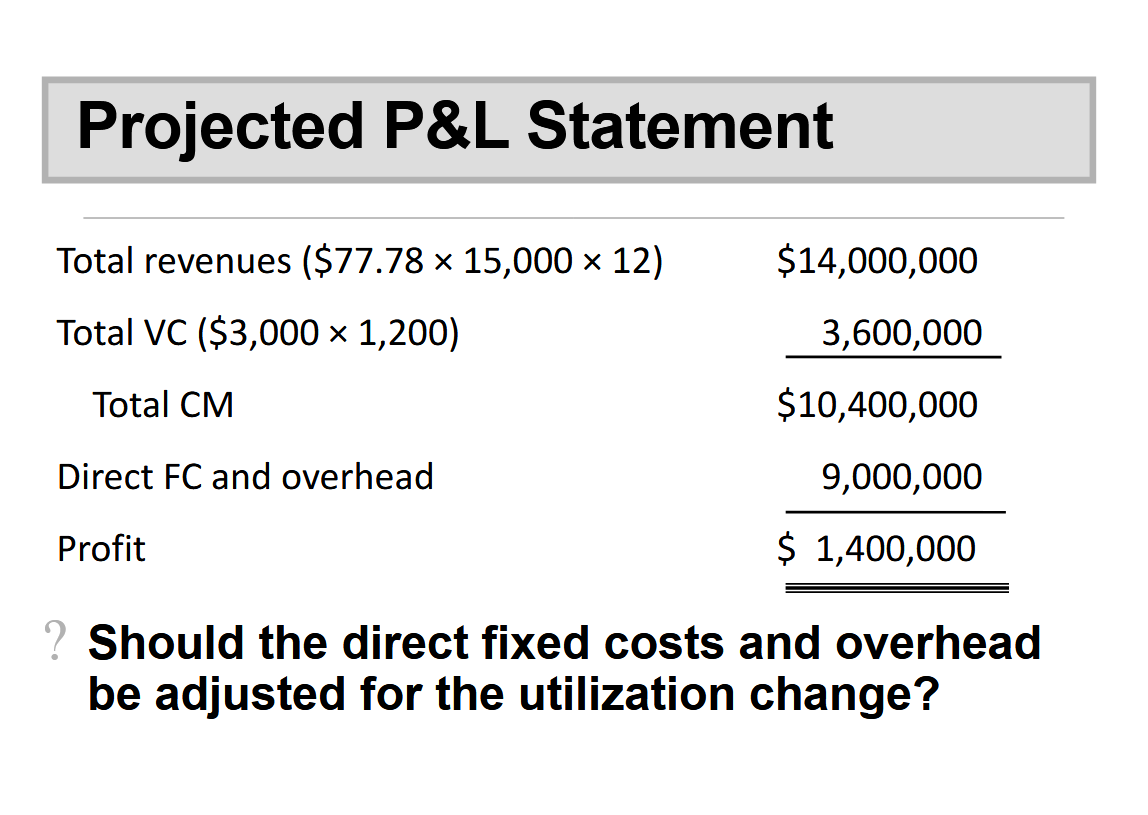

No cause these costs don’t change with volume that’s why they’re called “fixed costs”