Chapter Ten: Performance Evaluation

LO 1: Understand decentralization and describe different types of responsibility centers.

What is decentralization? Describe at least four advantages and two disadvantages of decentralization. (1)

Decentralization: When a company splits speatio

Compare and contrast a cost center, revenue center, profit center, and investment center. (2)

Cost: Focus on costs only → internal departments, IT, Acct, HR, Legal.

Revenue: Focus on Revenue only → Regional sales office territory

Profit: Concerned about revenues AND cost → Stand alone store OR restaurant

Investments: Concerned about revenue + costs AND managing → Parent OR large division of a corp

Example E10-20A: Each of the following situations describes an organizational unit. Identify which type of responsibility center each underlined item is (cost, revenue, profit, or investment center).

Organization

a. Sherwin-Williams Store #1933 is located in Copley, Ohio. The store sells paints, wallpapers, and supplies to do-it-yourself customers and to professional wall covering installers. → Profit

b. The Accounting Research and Compliance Department at FirstEnergy is responsible for researching how new accounting pronouncements and rules will impact FirstEnergy’s financial statements. → Cost

c. The Southwestern Sales Region of McDermott Foods is responsible for selling the various product lines of McDermott. → Revenue

d. The Taxation Department at Verizon Communications, Inc., is responsible for preparing the federal, state, and local income and franchise tax returns for the corporation. → Cost

e. The Roseville Chipotle restaurant in Minnesota, is owned by its parent Chipotle Mexican Grill, Inc. The Roseville Chipotle, like other Chipotle restaurants, serves burritos, fajitas, and tacos and competes in the “fast-casual” dining category. → Profit

f. Trek Bicycle Corporation manufactures and distributes bicycles and cycling products under the Trek, Gary Fisher, Bontrager, and Klein brand names. → Investment

g. The Hershey Company is one of the oldest chocolate companies in the United States.Its product lines include the Mauna Loa Macadamia Nuts, Dagoba Organic Chocolates, and Joseph Schmidt Confections. → Investment

h. The Human Resources Department is responsible for recruiting and training for the Kohl’s Corporation. → Cost

i. The reservation office for Allegiant Air is responsible for both online sales and counter sales. → Revenue

j. The Claire’s at Spring Hill Mall in West Dundee, Illinois, is owned by The Claire’s Stores, Inc. → Profit

k. H & R Block Tax Services, Block Advisors, and Expat Tax Services are all divisions of their parent corporation, H & R Block. → Investment

LO 2: Develop performance reports.

Describe the layout of a performance report.

Product: (Info / data)

Actual: (Info / data)

Budget: (Info / data)

$ Variance: (Info / data)

% Variance: (Info / data)

What is a variance?

Actual vs Budget

Favorable Variance (good):

Sales > Budget

Costs < Budget

Unfavorable Variance (bad):

Sales < Budget

Costs > Budget

Management by exception: Only investigate variances which meet some threshold

Direct Fixed Costs: Specific to the division OR department

Common Fixed Costs: Company wide and allocated to the departments.

Segment Margin: This is what the segment manager is responsible for.

Give examples favorable variance be “bad” or concerning.

Costs are less than we budgeted for

Direct materials are inferior / bad quality

Direct Labor is too unskilled

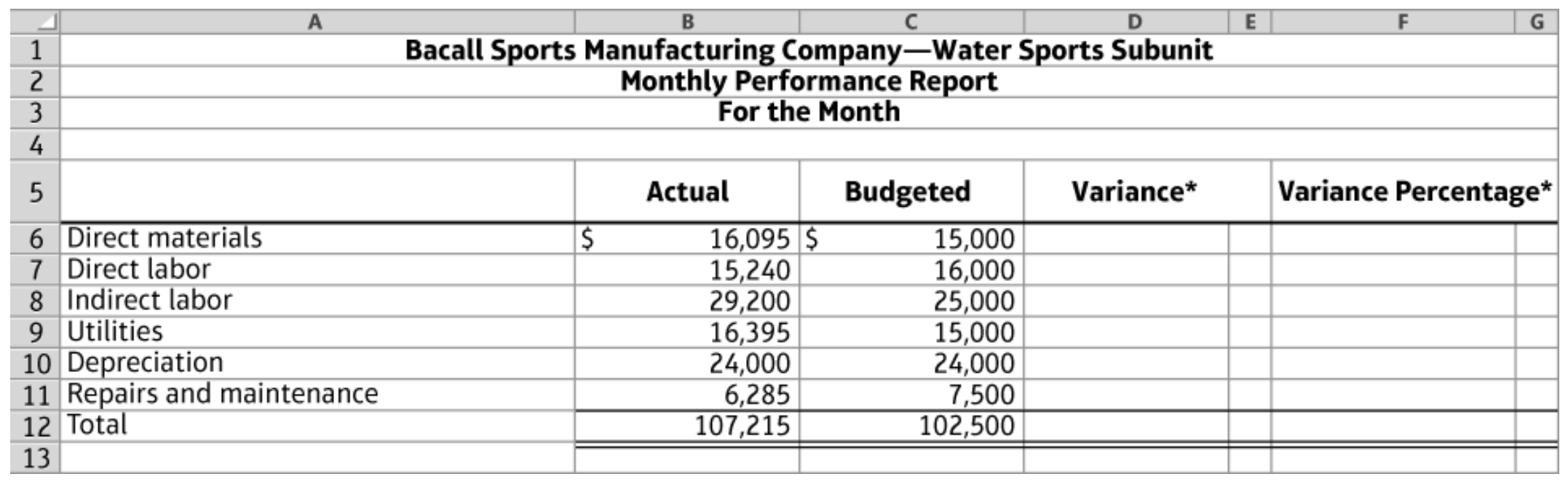

Example E10-21A Complete and analyze a performance report (Learning Objective 2): One subunit of Bacall Sports Manufacturing Company had the following financial results last month:

Requirements

1. Complete the performance evaluation report for this subunit (round to four decimals).

PIC

2. Based on the data presented, what type of responsibility center is the subunit?

Cost center

3. Which items should be investigated if part of the management’s decision criteria is to investigate all variances exceeding $2,500 or 12.5%?

Variance / Budgeted = Variance %

We should investigate Indirect Labor and Repairs and Maintenance.

4. Should only unfavorable variances be investigated? Explain.

No, because a favorable variance can still be a bad thing for a company.

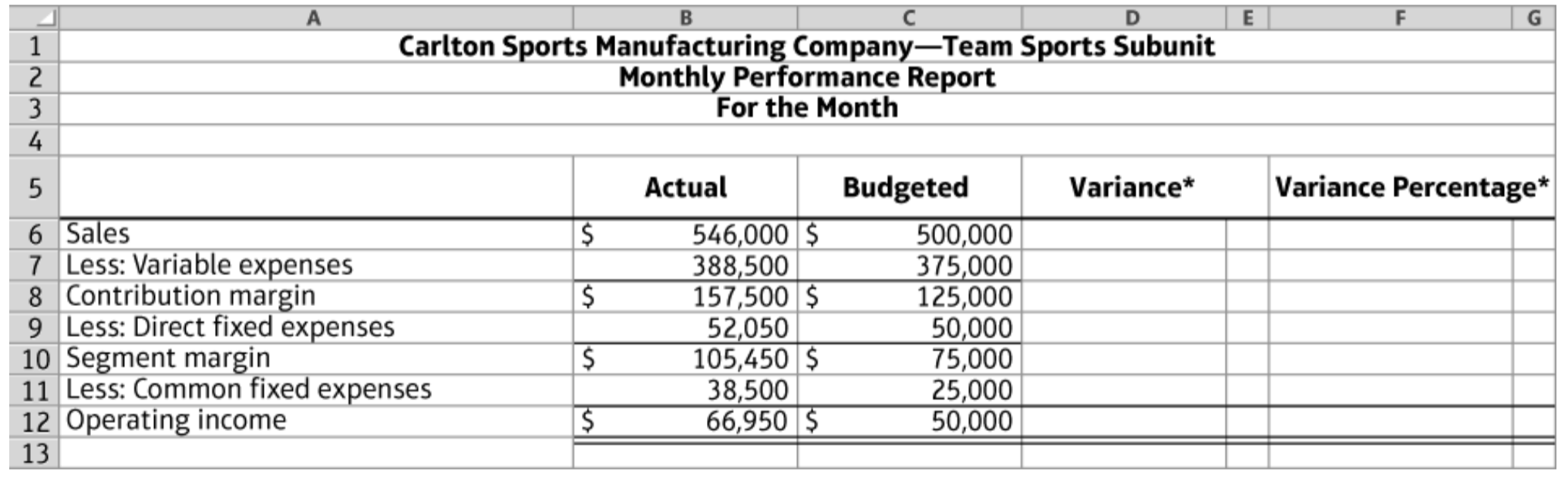

Example P10-55A Evaluate subunit performance (Learning Objectives 2 & 6): One subunit of Carlton Sports Company had the following financial results last month:

Requirements

1. Complete the performance evaluation report for this subunit (round to three decimal places).

PIC

2. Based on the data presented, what type of responsibility center is this subunit?

Profit center

3. Which items should be investigated if part of the management’s decision criteria is to investigate all variances equal to or exceeding $13,500 and exceeding 16% (both criteria must be met)?

Common fixed expenses.

NO subtotals

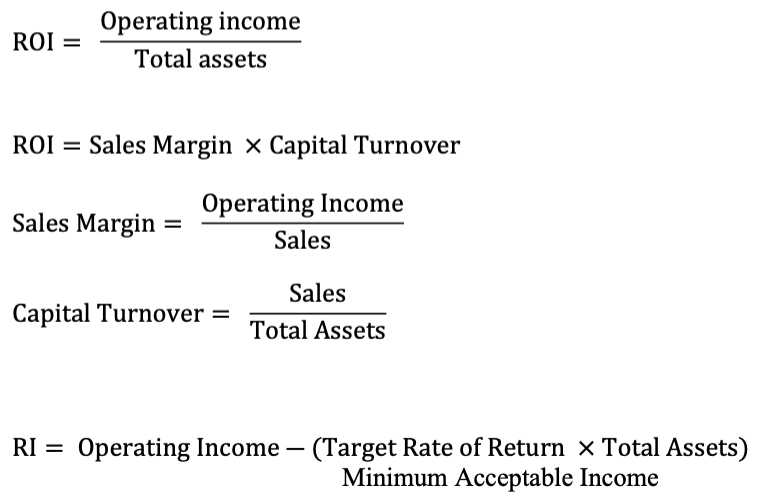

LO 3: Calculate ROI, sales margin, and capital turnover.

Review return on investment (ROI) and residual income (RI) calculations (3)

ROI: Operating Income relative to assets owned.

ROI (2): (OI /

Sales) x (Sales/ Total Assets)Sales Margin: How much operating income we earn for each $1 of sales (profitability)

Capital Turnover: How much we are earning in sales for each $1 of assets (efficiency)

RI: Did the company generate sufficient operating income to meet managemnts expectations.

Explain potential problems that could arise from using ROI as the incentive measure for managers. What are some specific actions a company might take to resolve this potential problem? (Page 698)

Drawback: Short-term focus.

Problem: Could turn down projects that would be good for the company but would take longer than a year to generate profits.

Actions: Use a longer time horizon (3 - 5 years)

Example E10-23A Compute and interpret the expanded ROI equation (Learning Objective 3): Rogers, a national manufacturer of lawn-mowing and snow-blowing equipment, segments its business according to customer type: Professional and Residential. Assume the following divisional information was available for the past year (in thousands of dollars):

Assume that management has a 25% target rate of return for each division.

Requirements (Round all of your answers to four decimal places.)

1. Calculate each division’s ROI.

Residential

Operating Income / Total Assets

68,000 / 200,000 = 0.34

Professional

Operating Income / Total Assets

153,000 / 365,000 = 0.42

2. Calculate each division’s sales margin. Interpret your results.

Residential

Operating Income / Sales

68,000 / 850,000 = 0.08

Residential earns 0.08 income for each $1 of sales.

Professional

Operating Income / Sales

153,000 / 1,095,000 = 0.14

Professional earns 0.14 income for each $1 of sales.

3. Calculate each division’s capital turnover. Interpret your results.

Residential

Sales / Total Assets

850,000 / 200,000 = 4.25

Residential is more efficient

Professional

Sales / Total Assets

1,092,000 / 365,000 = 3

Less efficient than residual

4. Use the expanded ROI formula to confirm your results from Requirement 1. What can you conclude?

Residential

Sales Margin x Capital Turnover

0.08 × 4.25 = 0.34

Professional

Sales Margin x Capital Turnover

0.14 × 3 = 0.42

5. Calculate each division’s residual income (RI). Interpret your results.

Residential

Operating Income - (Target Rate of Return x Total Assets)

68,000 - (0.25 × 200,000) = 18,000

In good shape but less profitable than professional

Professional

Operating Income - (Target Rate of Return x Total Assets)

153,000 - (0.25 × 365,000) = 62,050

In good shape and is more profitable.

LO 5: Prepare and evaluate flexible budget performance reports (2).

Why is comparing actual performance to the master budget often an “apples-to-orange comparison? How can a better comparison be made?

“Apples to orange”

Actual to master budget not directly comparable because of volume variances.

What to do?

Create a FLEXIBLE BUDGET: This is a budget using actual sales volume with budget per unit information.

What are different variances that can be reported in a performance report?

Comprehensive Budget Variance: “Apples to Oranges”

Volume Variance: Comprehensive vs. Flexible

Amount of variance due strictly to volume

Flexible Budget Variance: Actual vs Flexible Budget

Amount of variance due to something other than volume

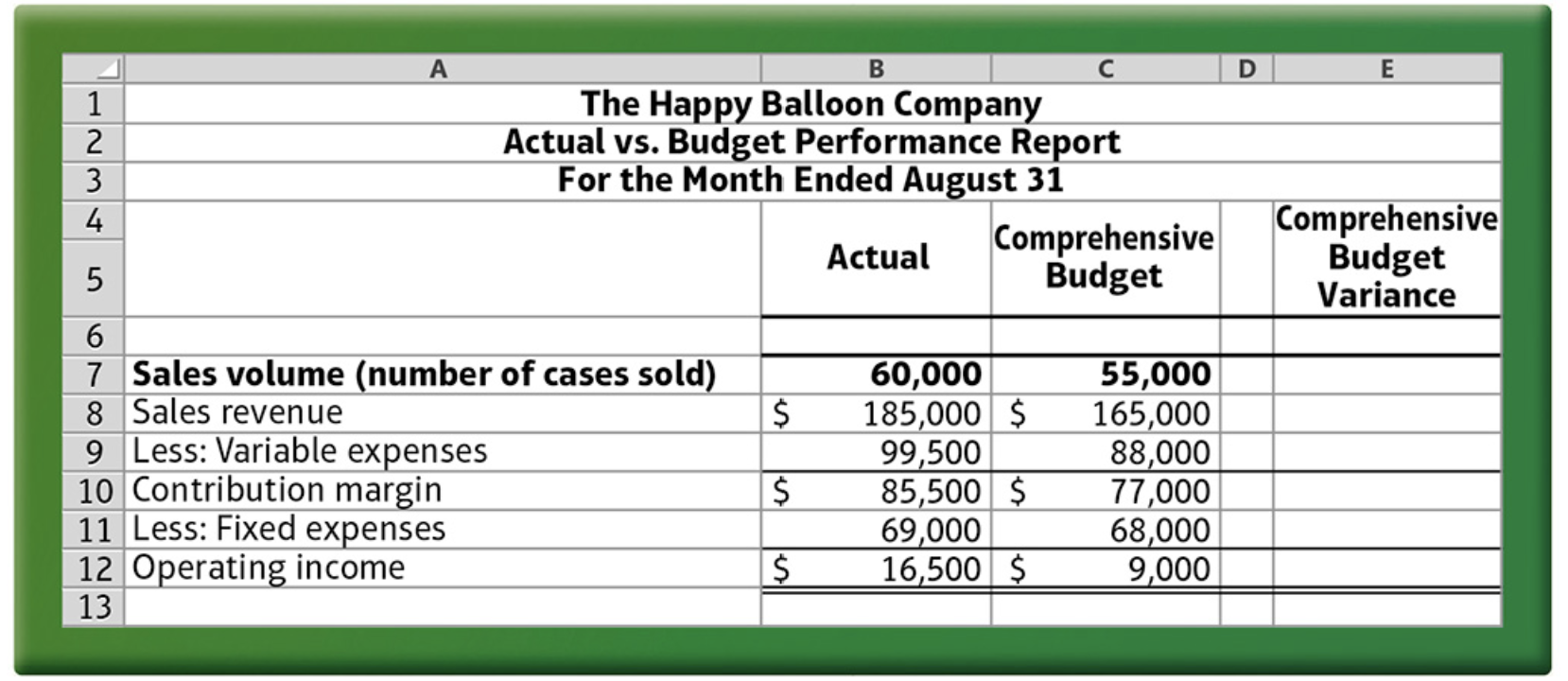

Example E10-28A Comprehensive flexible budget problem (Learning Objectives 2 & 5): The Happy Balloon Company produces party balloons that are sold in multi-pack cases. To follow is the company’s performance report in contribution margin format for August:

Requirements

1. What is the budgeted sales price per unit?

PIC

2. What is the budgeted variable expense per unit?

3. What is the budgeted fixed cost for the period?

4. Compute the comprehensive budget variances. Be sure to indicate each variance as favorable (F) or unfavorable (U).

5. Management would like to determine the portion of the comprehensive budget variance that is (a) due to volume being different than originally anticipated and (b) due to some other unexpected cause. Prepare a flexible budget performance report to address these questions, using the actual sales volume of 60,000 units and the budgeted sales volume of 55,000 units. Use the original budget assumptions for sales price, variable cost per unit, and fixed costs, assuming the relevant range stretches from 50,000 to 75,000 units.

6. Using the flexible budget performance report you prepared for Requirement 5, answer the following questions:

6(a). How much of the comprehensive budget variance (calculated in Requirement 4) for operating income is due to volume being higher than expected?

6(b). How much of the comprehensive budget variance for variable expenses is due to some cause other than volume?

3,500 (?): Something caused variable costs per unit to be higher than budget.

6(c). What could account for the flexible budget variance for sales revenue?

6(d). What is the volume variance for fixed expenses? Why is it this amount?

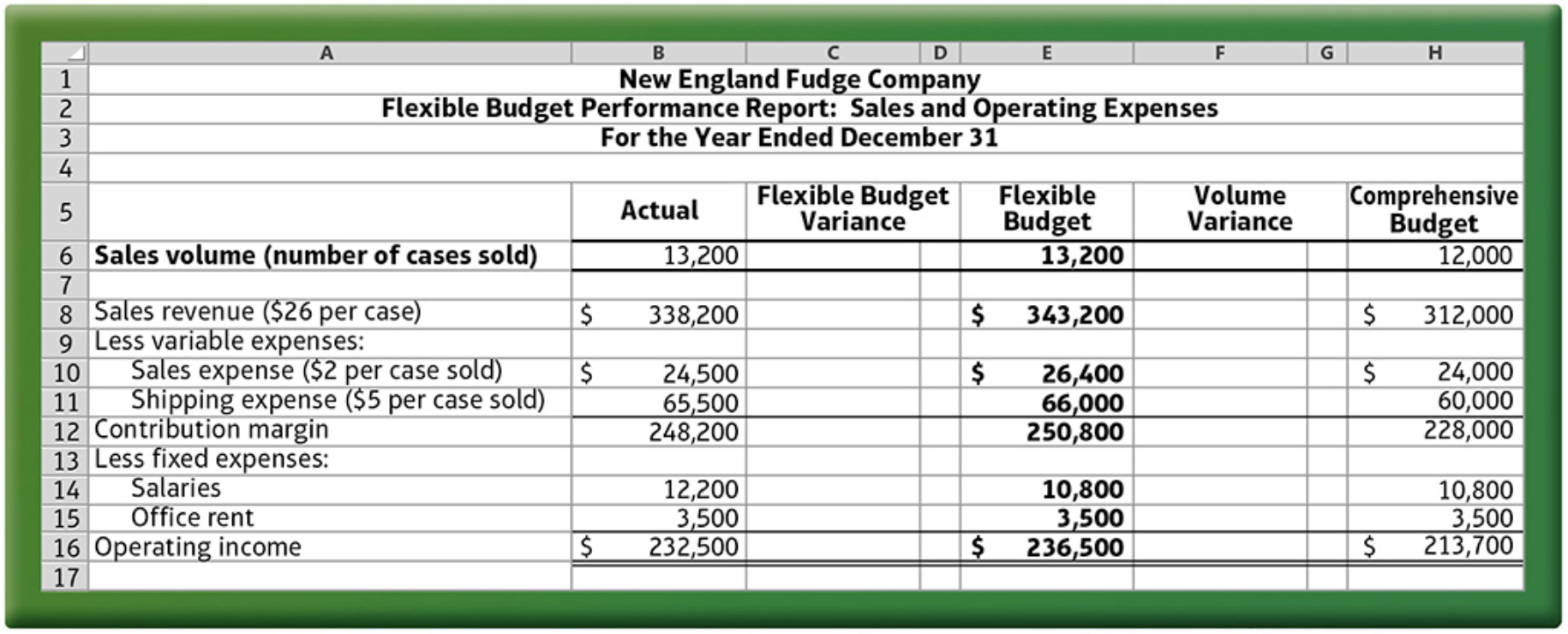

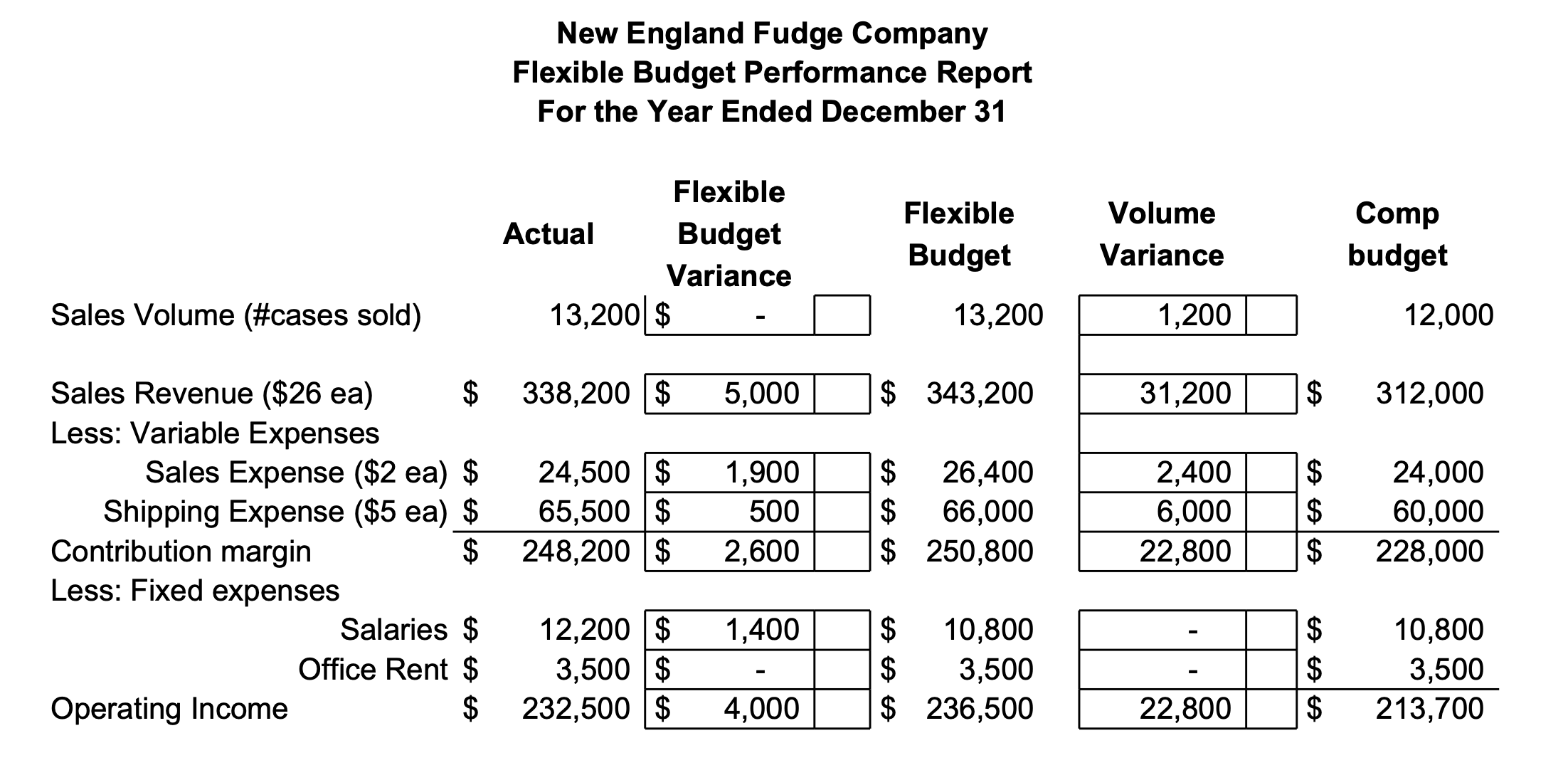

Example S10-13 Complete a comprehensive budget performance report (Learning Objective 5): The following table contains a hypothetical partial comprehensive budget performance report for New England Fudge Company. Fill in the Missing amounts. Be sure to indicate whether variances are favorable (F) or unfavorable (U).

Solution:

LO 6: Describe the balanced scorecard and identify KPIs for each perspective.

List and describe the four perspectives of the balanced scorecard. Give examples of key performance indicators (KPIs) for each perspective. (PG 712) (2)

Financial perspective

“How do we look to shareholders?”

Sales growth

Sale margin

Gross Profit

ROI

Customer perspective

“How do customers see us?”

Customer satisfaction

Rating

Number of repeat customers

Internal business perspective

“At what business processes must we excel to satisfy customer and financial objectives?”

New product development time

Defect rate

Average wait time

Learning and growth perspective

“Can we continue to improve and create value?”

Employee satisfaction

Training

Employee suggestions implemented

Percent of employees in problem solving teams

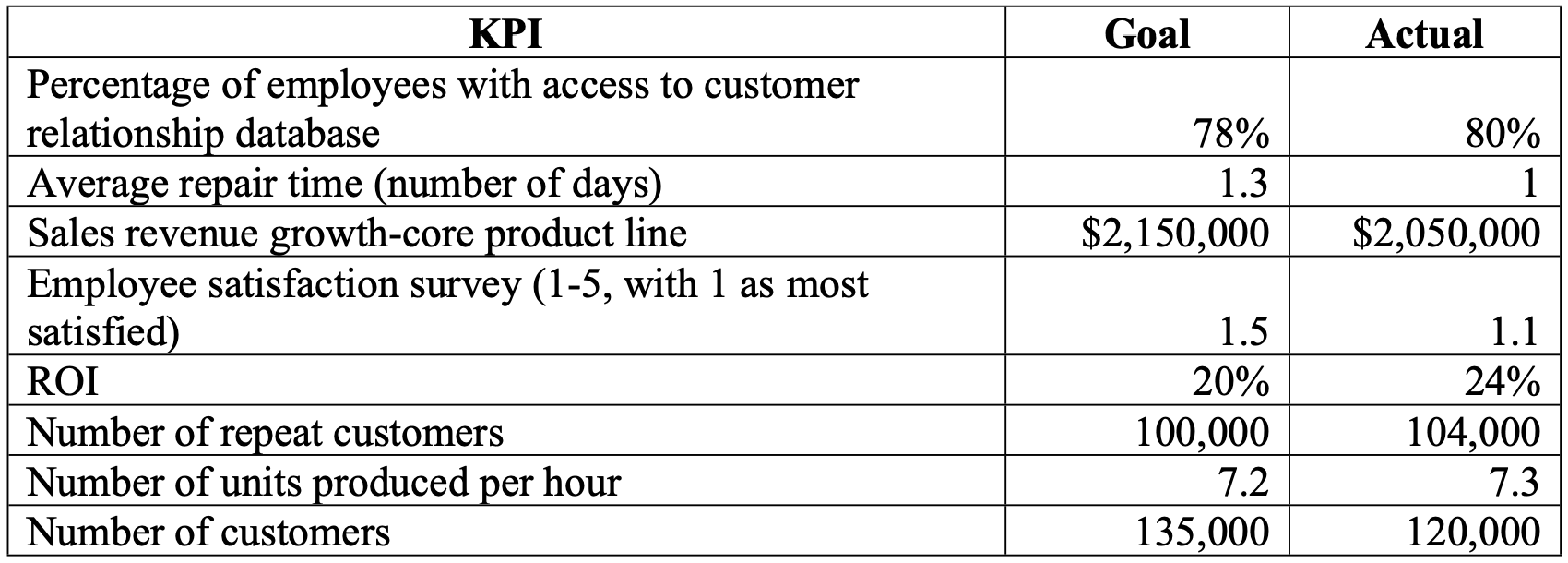

Example E10-31A Construct a balanced scorecard (Learning Objective 6: Dakota Corporation is preparing its balanced scorecard for the past quarter. The balanced scorecard contains four perspectives: financial, customer, internal business process, and learning and growth. Through its strategic management planning process, Dakota Corporation has selected two specific objectives for each of the four perspectives; these specific objectives are listed in the following table:

Specific Objective:

1. Increase sales of core product line: Financial

2. Improve production efficiency: Internal Business

3. Increase number of employees with access to customer relationship database: Learning and Growth

4. Increase number of customers: Customer

5. Improve post-sales service: Internal Business

6. Increase customer retention: Customer

7. Increase Return on Investment (ROI): Financial

8. Improve employee morale: Learning and Growth

Dakota Corporation has collected key performance indicators (KPIs) to measure progress toward achieving its specific objectives. The following table contains the KPIs and corresponding data that Dakota Corporation has collected for the past quarter.

Requirement

Prepare a balanced scorecard for Dakota Corporation using the form on the following page. For each of the specific objectives listed, place that objective under the appropriate perspective heading in the report. Select a KPI from the list of KPIs that would be appropriate to measure progress toward each objective. (There are two specific objectives for each perspective and one KPI for each of the specific objectives.) In the last column in the balanced scorecard report, place a check mark if the associated KPI goal has been achieved.

LO 7: Describe basic data visualization types and uses.

LO 8: Apply Excel to use the ABS and IF functions to calculate and label variances.