Power, Strategy and the firm

Market power

An attribute of a firm that can sell its product at a range of

feasible prices, so that it can benefit by acting as a price-setter (rather than a

price-taker).

• The firm has bargaining power in its relationship with its customers to set a

high price without losing them to competitors

Sources of market power:

barriers to entry

brand loyalty

copyrights and patents

differentiated products

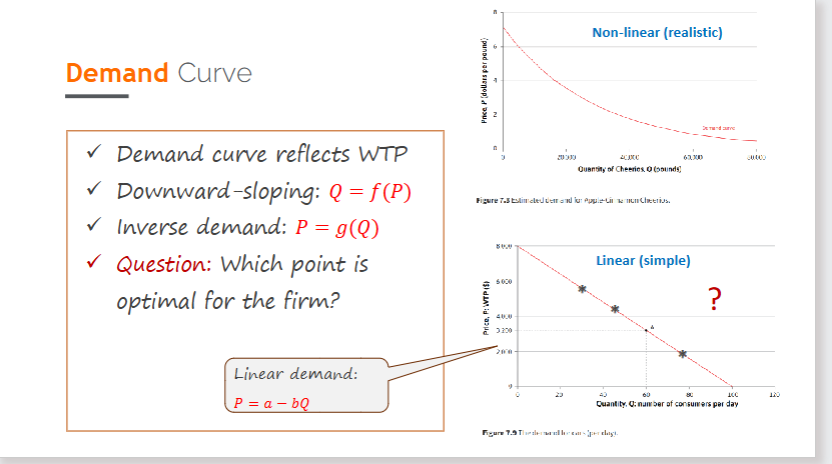

willingness to pay

consumers demonstrate their willingness to pay for different products.

• But how does the firm identify or find this information?In theory, firms can estimate the demand for their product by surveying large number of consumers (e.g: loyalty schemes/apps – data collection).

• They can also look at the demand curve

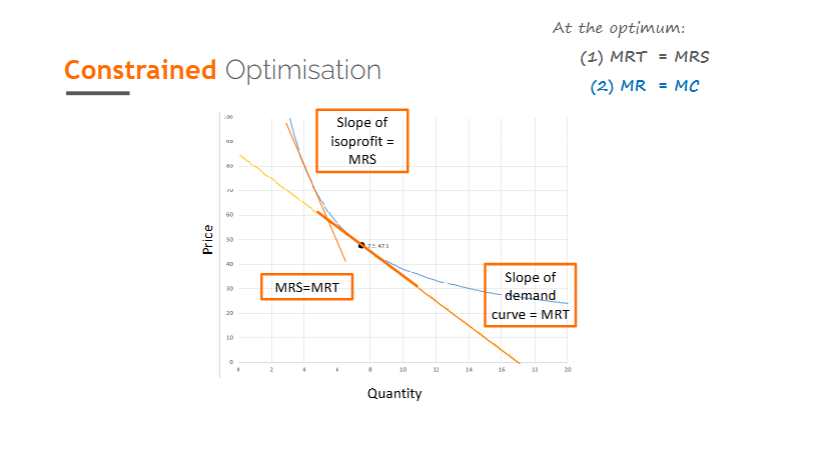

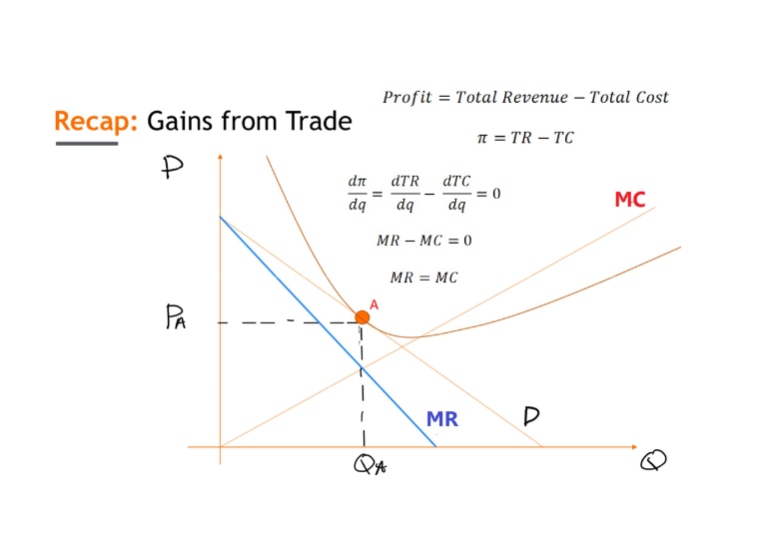

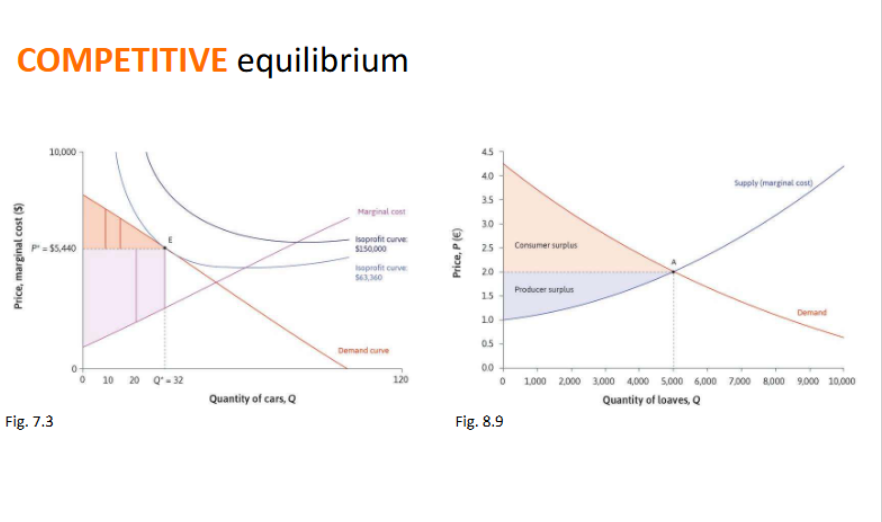

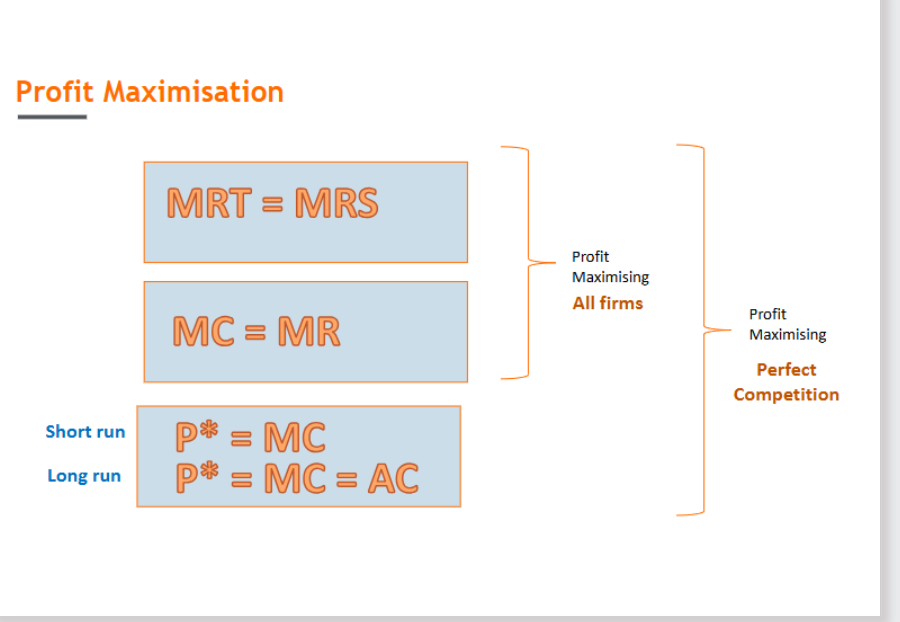

Profit Maximisation

The firm’s constrained optimization problem is analogous to the

consumer’s.Demand curve = FF, Slope =MRT

Iso-profit curves= indifference curves =MRS

Firm maximizes profits by choosing point

where MRS = MRT

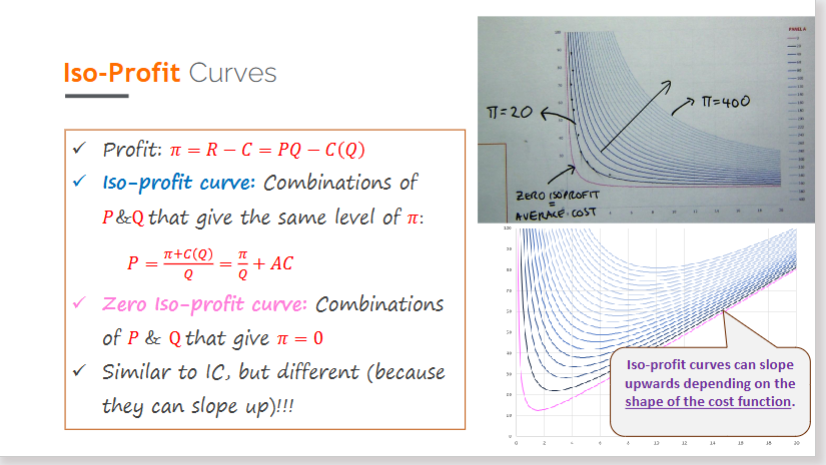

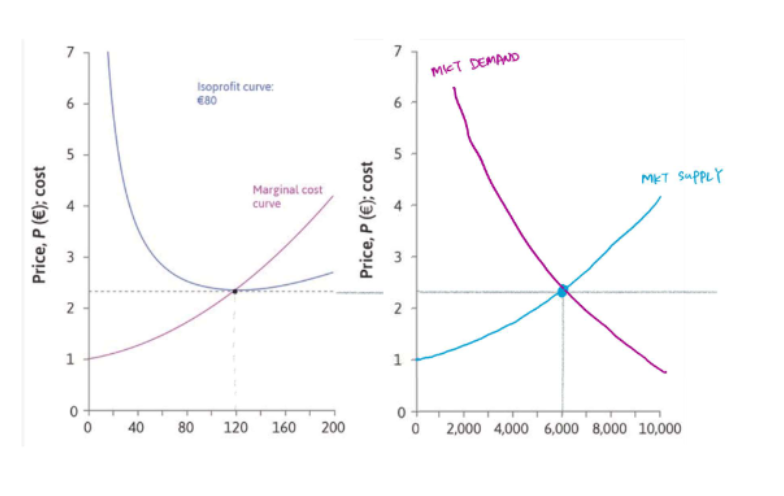

Isoprofit curves

Isoprofit curves show price-

quantity combinations that give the same profit.The shape of a firm’s cost

function affects the shape of

their isoprofit curves.(Economic) Profit = Total revenue – Total costs

(Costs include the opportunity cost of capital)

1. Iso = same profit.

2. Higher curve = higher profit.

3. Zero iso-profit = average cost line

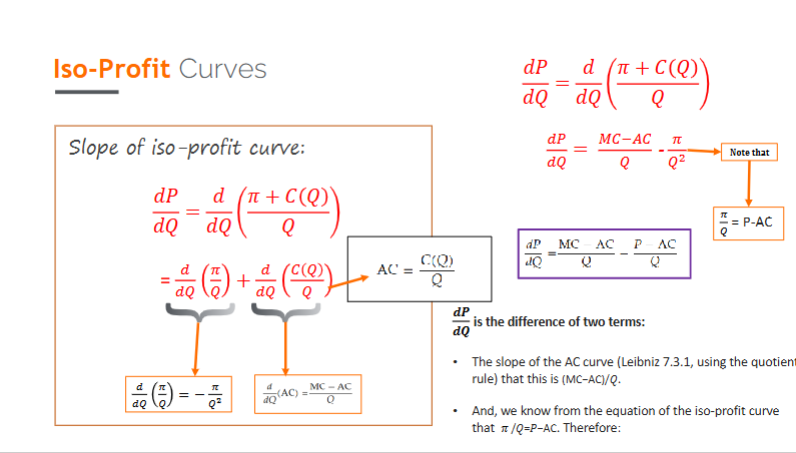

costs

The average cost (AC) is defined as the total cost divided by the number of items produced.

The marginal cost (MC) is the rate at which costs increase if 𝑄 increases (the cost of producing one more item).

the slope of iso-profit curve = (MC-P)/Q

this is the MRS

the top half of the equation is the profit margin

constrained optimisation

We establish that the firm’s pricing decision depends on the

slope of the demand curve.

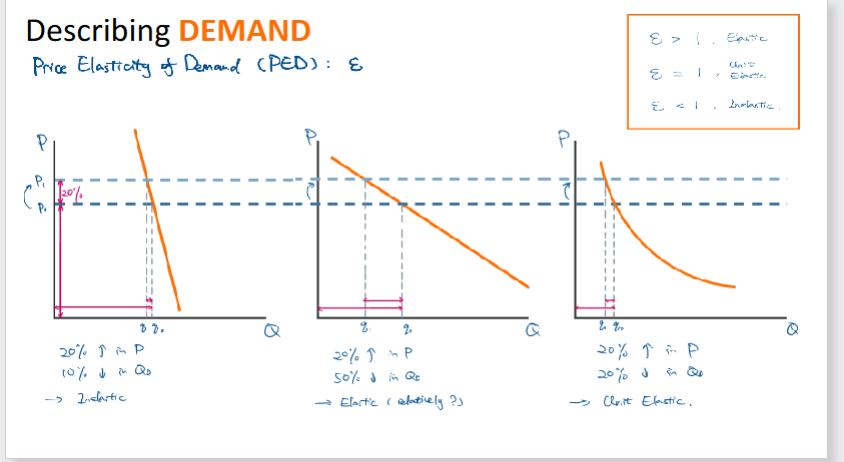

Elasticities

A firm’s pricing decisions depends on

the slope of the demand curve.Price elasticity of demand = degree of

responsiveness (of consumers) to a

price change.ε=− (% change in demand) / (% change in price)

MR is always positive when demand is

elastic.When the elasticity is below

1, MR <0

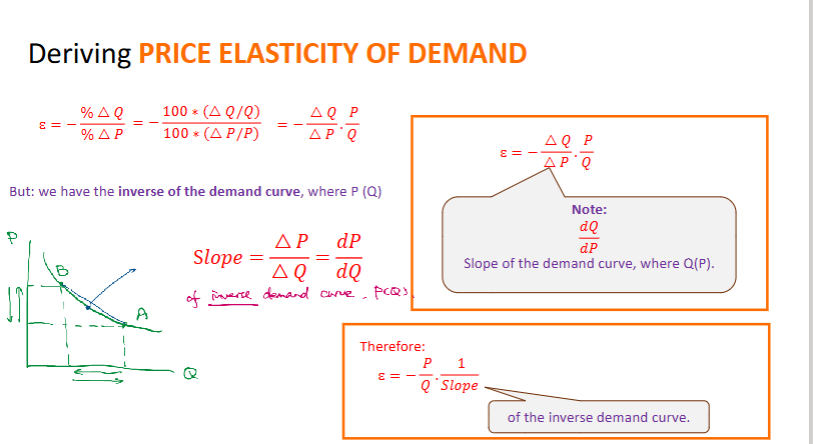

deriving price elasticity of demand

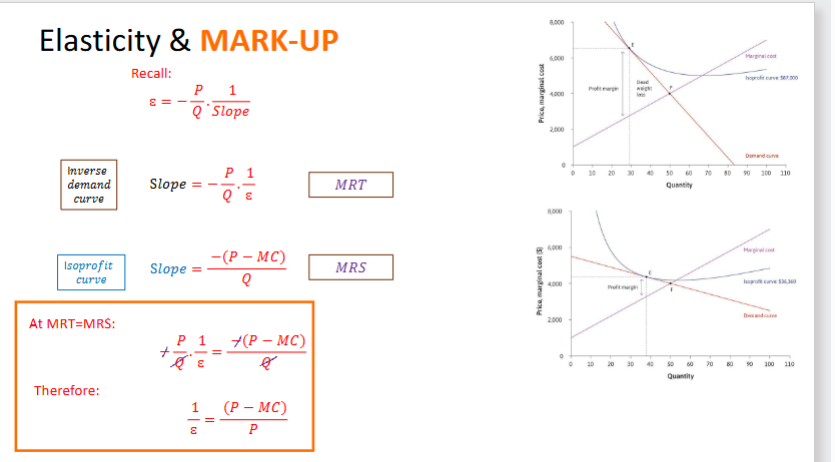

elasticities and markups

Mark-up: price minus the marginal cost divided by the

price

The Mark-Up (𝑃 − 𝑀𝐶)/P is inversely proportional to elasticity.

A lower markup means that there is a higher elasticity of demand, meaning there is more competition

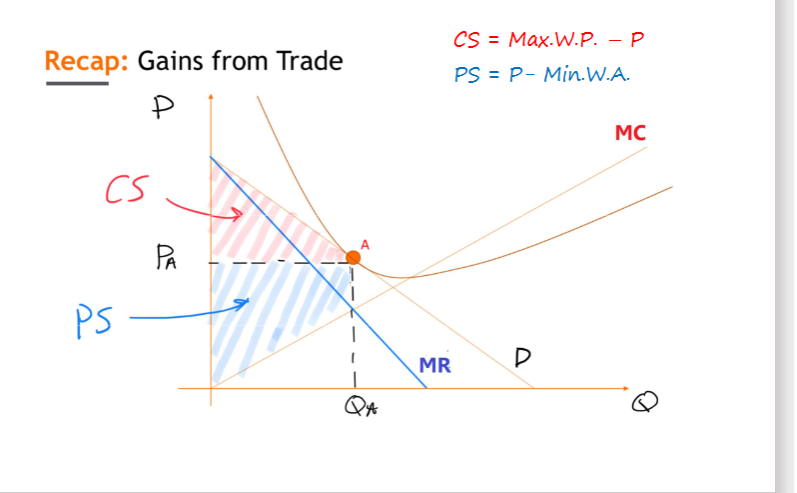

Gains from trade

For CS and PS to me maximized at equilibrium:

buyers and sellers both price-takers

the equilibrium allocation maximizes the sum of the gains achieved by trading in the market, relative to the original allocation

Competitive equilibrium is pareto efficient

However , it may not be fair if PS and CS aren’t equal, and also depends on elasticities of supply and demand

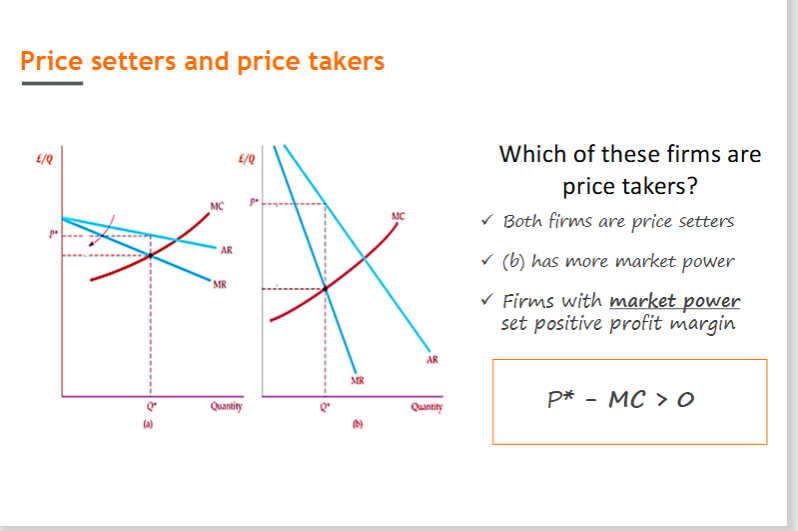

Price setters vs takers

Price setting firms have market power - they set a positive price margin

They have downward sloping AR and MR curves

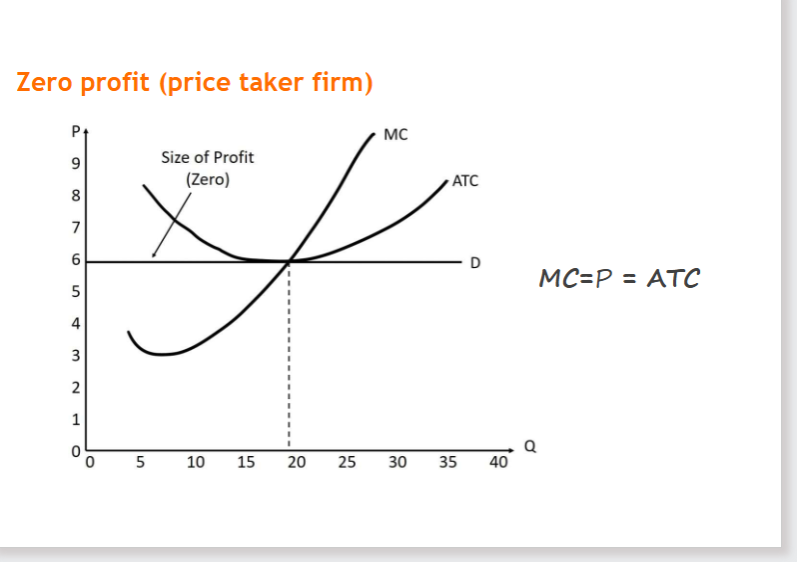

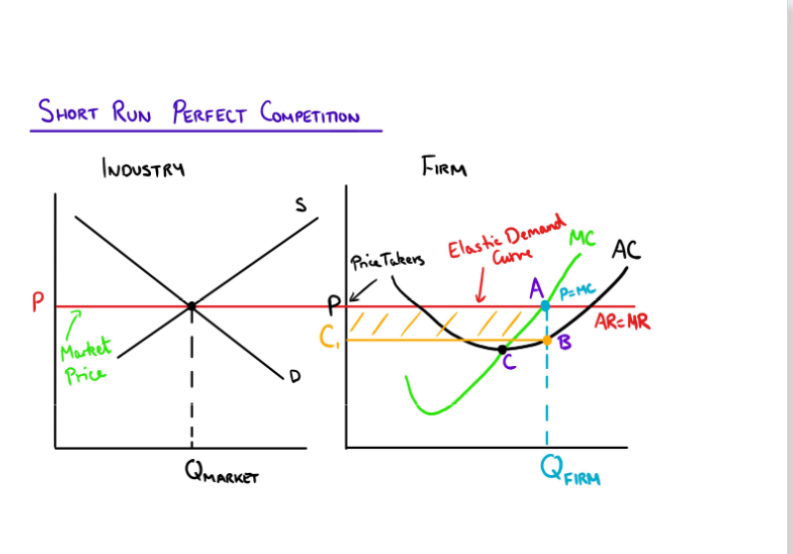

Price-taking firms have a horizontal demand curve

their price is the same no matter how much they want to sell

they have zero profit margin (p*=MC=ATC) at the optimal price and quantity

degrees of competition

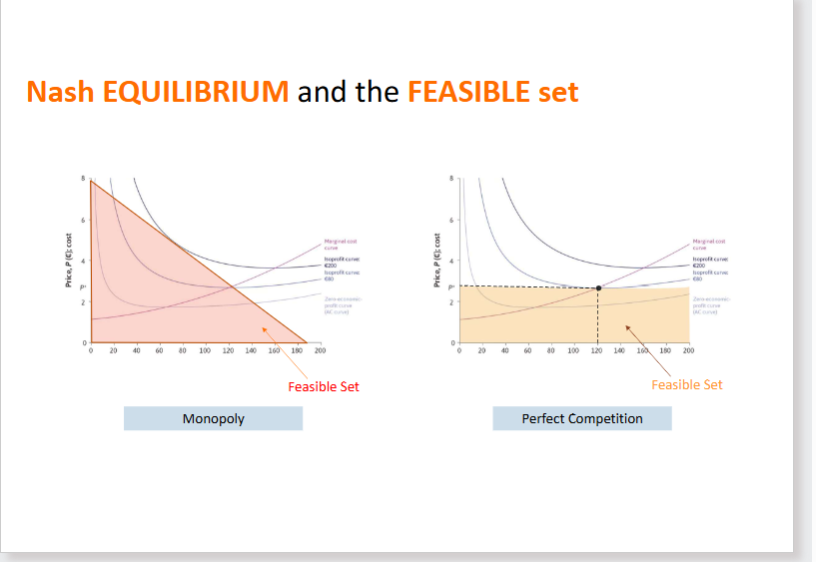

Monopoly:

Price setting power

Differentiated Products

Barriers to entry

Single Producer

Supernormal Profits possible

Pareto inefficiency possible

Perfect competition:

Price takers

Homogenous Products

No barriers to entry

Many sellers

Many buyers

Normal profits

No deadweight loss

Nash equilibrium and Feasible set

price determination

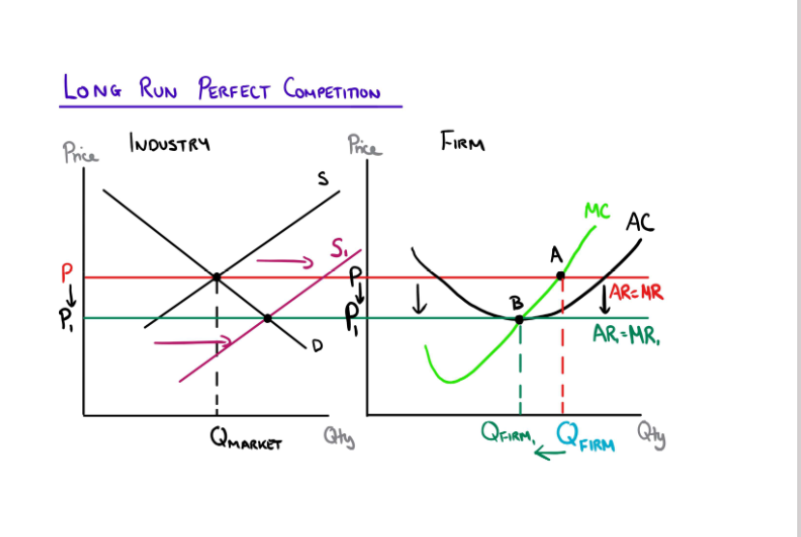

long-run price determination

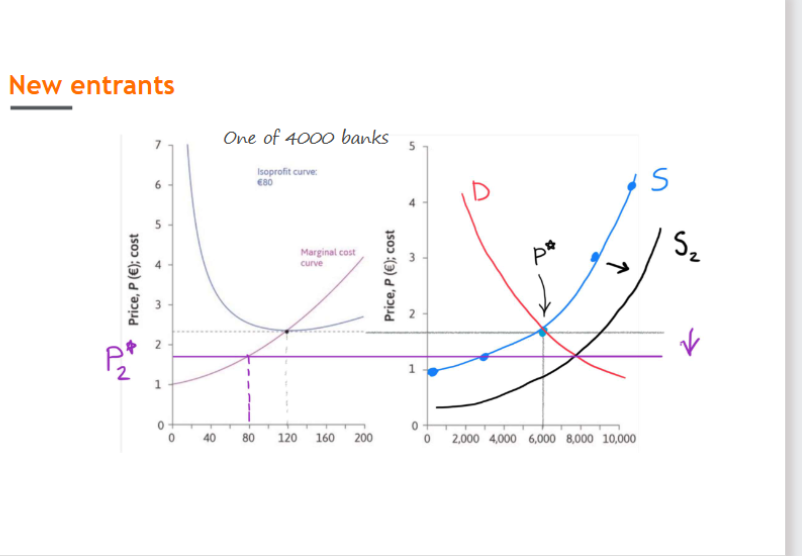

new entrants

When there are new entrants, market supply increases

This pushes the price/cost down

The optimal price falls, as firms face more competition

short vs long run competition

In perfect competition, firms are price takers

P*=MC=AC

in the long-run, if supply increases due to no barriers to entry, costs fall, the price will also fall , and the demand curve therefore shifts downwards

The market supply curve will shift

the optimal amount a firm will produce decreases (as price decreases)

Competitive equilibrium

In competitive equilibrium, all buyers and sellers are price-takers

Supply=demand at market price

In a monopoly, there is a welfare loss

In a perfectly competitive market, there is no DWL

Profit maximisation

Key terms and questions

joint surplus: Sum of producer and consumer surplus

consumer surplus: P-WTA

producer surplus: WTP-P

Reservation price: The lowest price at which someone is willing to sell a good (keeping the good is the potential seller's reservation option)

Competitive Equilibrium: A market outcome in which all buyers and sellers are price-takers, and at the prevailing market price, the quantity supplied is equal to the quantity demanded.

Price takers: Characteristic of producers and consumers who cannot benefit by offering or asking any price other than the market price in the equilibrium of a competitive market. They have no power to influence the market price.

Economies of scale: occur when doubling all of the inputs to a production process more than doubles the output. The shape of a firm's long-run average cost curve depends both on returns to scale in production and the effect of scale on the prices it pays for its inputs.

returns to scale: when doubling all of the inputs to a production process doubles the output. The shape of a firm's long-run average cost curve depends both on returns to scale in production and the effect of scale on the prices it pays for its inputs

Show how the MRS=MRT condition is related to the MR=MC condition.: MR (Marginal Revenue) reflects the value to consumers → like MRS

MC (Marginal Cost) reflects the cost of production → like MRT

Price Elasticity of Demand: It measures how much the quantity demanded of a good changes when its price changes. If a small price decrease leads to a large increase in the amount people want to buy, the demand is considered elastic.

Inelastic Demand: where the quantity demanded of a good changes very little when its price changes. Even if the price goes up or down, people will still buy about the same amount

of the good.Market failure: occurs when markets allocate resources in a Pareto-inefficient way.

why is a competitive market equilibrium a nash equilibrium: given what all other actors are doing (trading at the equilibrium price), no actor can do better than to continue what he or she is doing (also trading at the equilibrium price).