MANSCI NOTES

LESSON 1

QUANTITATIVE APPROACHES TO DECISION MAKING

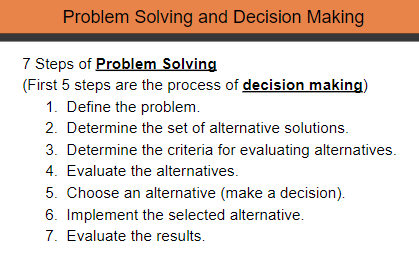

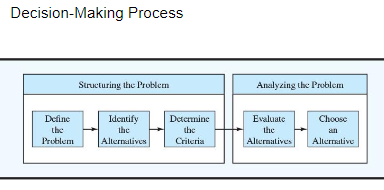

DECISION-MAKING PROCESS

- Single-criterion decision problems - objective is to find the best solution with respect to one criterion

- Multicriteria decision problems - involve more than one criteria

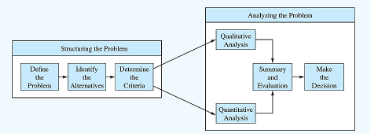

ANALYSIS PHASE OF DECISION-MAKING PROCESS

POTENTIAL REASON FOR A QUANTITATIVE ANALYSIS APPROACH TO DECISION MAKING:

- Complex

- Very important

- New

- Repetitive

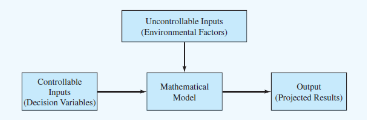

Models - representation of real objects or situations

- ICONIC MODELS - physical replicas

- ANALOG MODELS - physical in form but do not physically resemble the object being modeled

- MATHEMATICAL MODELS - represent real world problems through a system of mathematical formulas and expressions based on key assumptions, estimates, or statistical analyses

Experimenting with models:

- Requires less time

- Less expensive

- Involves less risks

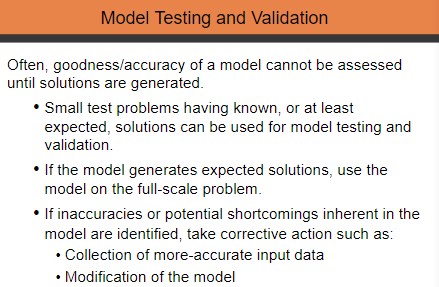

The more closely the model represents the real situation, the more accurate the conclusions and predictions will be.

MATHEMATICAL MODELS:

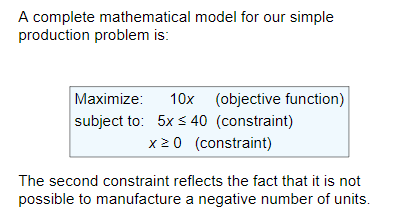

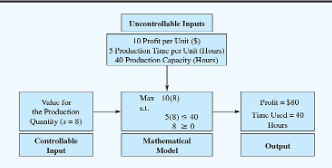

Objective Function - mathematical expression that describes the problem’s objective, such as maximizing profit or minimizing cost (10x)

Constraints - set of restrictions or limitations (production capacities, chuhcu: 5x<40)

Uncontrollable inputs - environmental factors that are not under the control of the decision maker (profit per unit, production time, production capacity, chuchu)

Decision variables - controllable inputs; decision alternatives specified by the decision maker maker (no. of units to produce)

Deterministic model - if all uncontrollable inputs to the model are known and cannot vary

Stochastic / probabilistic model - if any uncontrollable are uncertain and subject to variation

Data preparation is not a trivial step, due to the time required and the possibility of data collection errors.

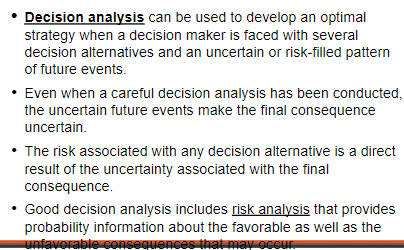

- Identify the alternative that provides the BEST OUTPUT for the model

Optimal Solution - best output

Infeasible - alternative does not satisfy all of the model constraints, thus rejected regardless of the objective function value

Feasible - alternative satisfies all of the model constraints and a candidate for best solution

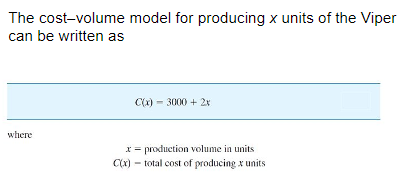

MODELS OF COST, REVENUE, AND PROFIT

- Fixed cost - portion of the total cost that does not depend on the production volume; does not change

- Variable cost - portion of the total cost that is dependent on and varies with the production value

- Marginal cost - rate of change of the total cost with respect to production volume; cost increase associated with a one-unit increase in the production volume

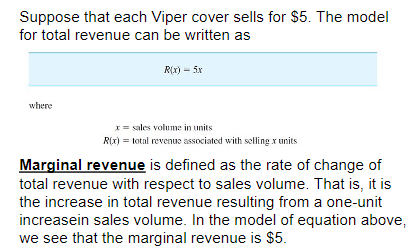

- Marginal revenue - rate of change of total revenue with respect to sales volume; increase in total revenue resulting from a one-unit increase in sales volume

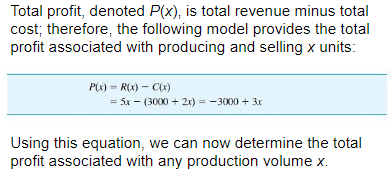

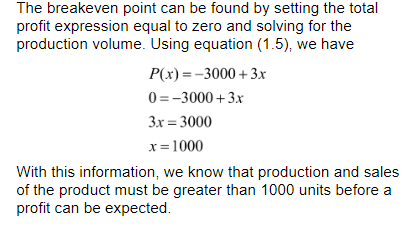

- Total profit - total revenue minus total cost

Breakeven point - volume that results in total revenue equal to total cost

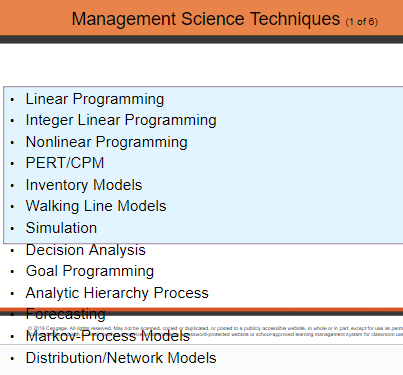

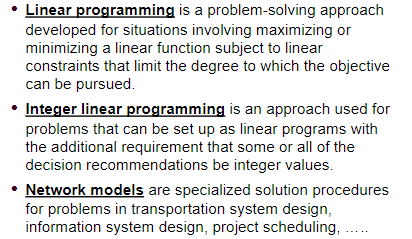

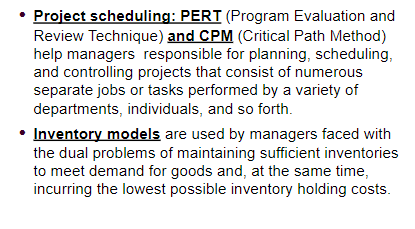

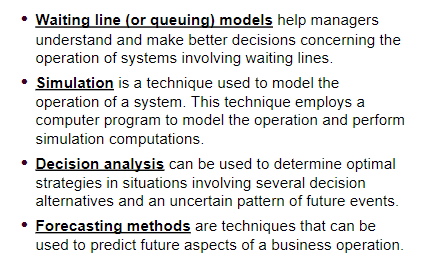

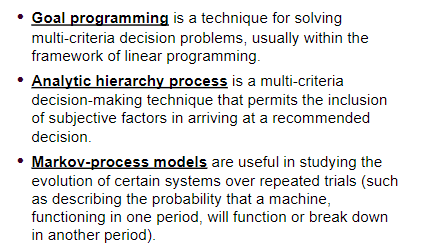

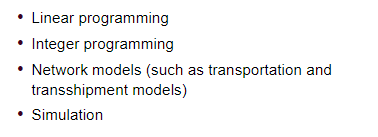

LESSON 2

LESSON 3